Las Vegas Sands Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

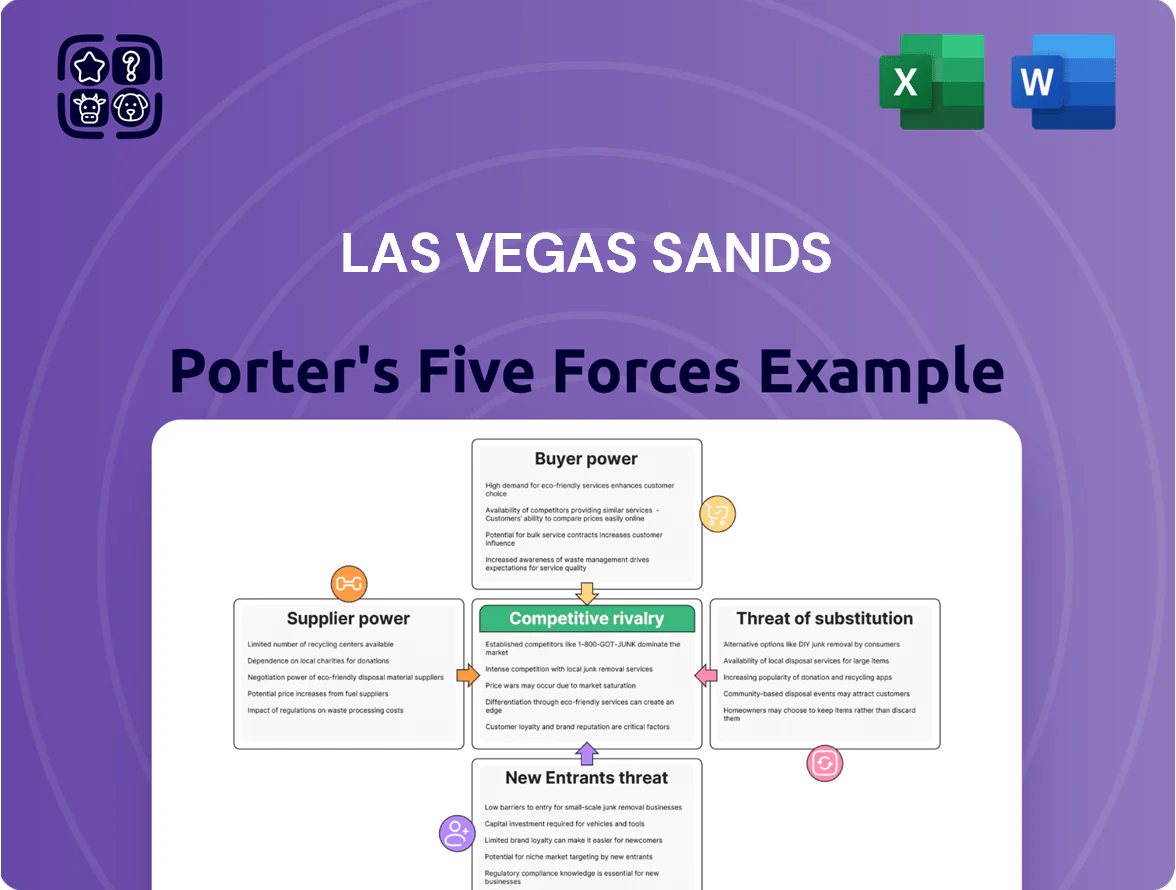

Las Vegas Sands faces intense rivalry from integrated resort competitors, high buyer power from travel-savvy customers, and regulatory and capital-intensive barriers that limit new entrants while supplier leverage for premium assets remains moderate.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Las Vegas Sands’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Gaming Equipment Providers

The high-end slot machine and electronic table market is concentrated among Light & Wonder and International Game Technology (IGT), giving suppliers moderate bargaining power over Las Vegas Sands because their tech is essential to operations.

Still, Sands' scale—operating 41 properties as of 2025 and sourcing thousands of cabinets—lets it secure volume discounts; public filings show major casino orders can cut unit costs by 10–20%.

Limited Availability of Prime Real Estate

The supply of land for integrated resorts in Macau and Singapore is extremely scarce and tightly controlled by governments, making them the de facto primary suppliers of operating rights and land; Macau granted just 6 gaming concessions for 650,000 annual visitors per casino district in 2024, while Singapore limits Marina Bay Sands-style sites to a handful of government-approved plots. This creates high dependency for Las Vegas Sands, which must meet strict regulatory and concession conditions to retain land use and revenue streams, and risks losing access if compliance or renegotiation fails.

Specialized Labor and Talent Retention

Las Vegas Sands depends on a large, skilled workforce from front-line hospitality to security and casino managers; in 2024 the company reported 46,000 global employees, highlighting scale-sensitive labor needs. In Macau and Singapore, union activity and local-hire rules raise labor bargaining power, forcing higher compliance and recruitment costs—Macau’s minimum wages rose ~6% in 2023. LVS must match market pay and benefits to retain talent; labor costs represented ~22% of operating expenses in 2024, so wage pressure can squeeze margins.

Utility and Infrastructure Dependencies

Large integrated resorts like Las Vegas Sands consume huge amounts of energy, water, and telecoms—MGM reported Strip resorts used ~120–150 kWh per occupied room night in 2023, so Sands faces similar scale and cost exposure.

Most utilities in Nevada and Macau are regional monopolies or state-owned, leaving Sands with effectively zero bargaining power over rates and service terms.

Energy price swings and tighter environmental rules (e.g., Nevada emissions limits, Macau water-reuse mandates) can cut margins; a 10% rise in energy costs can reduce resort EBITDA by 2–4%.

- High consumption: ~120–150 kWh/room-night

- Zero supplier bargaining power

- 10% energy cost rise → EBITDA −2–4%

- Regulatory shifts (water, emissions) raise capex/opex

Luxury Brand and Retail Partnerships

Las Vegas Sands depends on top luxury brands to occupy about 1.2 million sq ft of retail (Marina Bay Sands + Venetian portfolio), driving high-spend visitors; top-tier labels thus hold strong bargaining power since their logos underpin the resorts' luxury positioning.

If a flagship tenant exits, average spend per high-net-worth guest (estimated $4,500 per trip in 2024) and footfall could fall, hurting F&B and gaming revenues tied to retail draw.

- Luxury retail = key traffic driver, ~1.2M sq ft total

- Top brands wield leverage; presence crucial to brand identity

- Loss of anchors risks lower HNW spend (~$4,500/trip)

- Renegotiation pressure on rents and revenue-sharing

Supplier leverage splits: concessions, utilities, luxury tenants strong; gaming moderate

Suppliers wield mixed power: gaming-machine makers (Light & Wonder, IGT) have moderate leverage, utilities and land/concession authorities (Macau, Singapore) have high leverage, luxury retail tenants hold strong leverage, and labor/wage rules (46,000 employees in 2024; labor ~22% of opex) create additional pressure; a 10% energy price rise cuts EBITDA ~2–4%.

| Supplier | Key metric | Power |

|---|---|---|

| Gaming machines | 2 suppliers; bulk discounts 10–20% | Moderate |

| Land/concessions | 6 Macau concessions (2024); few SG plots | High |

| Labor | 46,000 employees (2024); labor ~22% opex | Moderate–High |

| Utilities | 120–150 kWh/room-night; regional monopolies | High |

| Luxury retail | ~1.2M sq ft; HNW spend ~$4,500/trip (2024) | High |

What is included in the product

Tailored Porter's Five Forces analysis for Las Vegas Sands that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats, with strategic commentary to inform investor decks and corporate strategy.

A concise Porter's Five Forces snapshot for Las Vegas Sands—quickly gauge supplier, buyer, competitive, entrant, and substitute pressures to inform strategic moves.

Customers Bargaining Power

High Price Sensitivity in Leisure Segments

General tourists and leisure travelers face many global vacation choices and can compare prices instantly online, raising their bargaining power; TripAdvisor data shows 72% of leisure bookings in 2024 were influenced by price comparisons.

This price-sensitive segment switches destinations or hotel brands for promotions and value, so Sands faces high churn risk during weak demand months; MGM and Wynn promotional discounts climbed ~15% in 2023-24.

As a result, Las Vegas Sands must spend heavily on loyalty and marketing—Sands reported sales & marketing expenses of $1.1 billion in FY2024—to retain these guests.

Leverage of VIP and High-Roller Clients

A small group of VIP and high-roller clients account for roughly 25–35% of Las Vegas Sands’ gaming revenue; losing a handful can swing quarterly EBITDA by millions, so the firm grants outsized concessions like elevated credit lines, private suites, and bespoke comps. In 2024 LVS reported VIP/rolling chip volumes concentrated in Macau VIP rooms, reinforcing bargaining power as operators match personalized offers to retain play.

Corporate and MICE Group Influence

Corporate and MICE group clients wield strong bargaining power over Las Vegas Sands because large bookings—often planned 1–3 years ahead—can cover thousands of room nights and 100,000+ sq ft of convention space, forcing concessions on rates and F&B. In 2024 Sands’ Macau and US properties reported group ADR discounts averaging 12–18% vs transient rates, and group bookings drove ~28% of consolidated RevPAR in 2024. To lock multi-year contracts, Sands offers tailored packages, volume-based rebates, and F&B credits that compress margins but secure occupancy and ancillary spend.

Low Switching Costs for Casual Gamblers

For casual gamblers the cost to switch from Las Vegas Sands to nearby rivals like Wynn or MGM is effectively zero; walkable clusters such as Macau’s Cotai Strip and the Las Vegas Strip let patrons move venues in minutes. In 2024 Macau reported 34% of VIP and mass gamblers visiting multiple properties per trip, so Sands faces constant churn pressure. That forces ongoing refreshes of floor games, F&B, and shows to retain spend.

- Zero incremental travel cost — walkable casino clusters

- 34% of Macau gamblers visit multiple properties (2024)

- High churn → continuous product/amenity investment

Information Transparency and Online Reviews

With travel platforms and social media, guests see prices and reviews instantly; 89% of travelers in 2024 said online reviews influenced their booking, raising customer leverage over Las Vegas Sands (LVS).

Real-time ratings and platforms like Tripadvisor and Google mean guests can enforce service standards; LVS’s Las Vegas and Macau revenue (2024: LVS net revenue $13.4B) is exposed to swift reputational swings.

Negative digital sentiment can redirect traffic fast—studies show a 1-star drop can cut bookings by ~20%—so collective online voice gives modern travelers tangible bargaining power.

- 89% travelers (2024) rely on reviews

- 1-star drop ≈ 20% fewer bookings

- LVS 2024 net revenue $13.4B at reputational risk

Price-sensitive travelers, VIPs & MICE force LVS to spend $1.1B to protect $13.4B revenue

Customers hold high bargaining power: price-sensitive leisure travelers (72% influenced by price comparisons in 2024) can switch destinations instantly, VIPs drive 25–35% of gaming revenue and demand bespoke concessions, and large MICE clients secure 12–18% group ADR discounts; LVS spent $1.1B on sales & marketing in FY2024 to defend share and reported $13.4B net revenue in 2024.

| Metric | 2024 |

|---|---|

| Leisure price-influenced bookings | 72% |

| VIP share of gaming revenue | 25–35% |

| Group ADR discount vs transient | 12–18% |

| S&M expenses (FY2024) | $1.1B |

| LVS net revenue | $13.4B |

Preview Before You Purchase

Las Vegas Sands Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Las Vegas Sands you'll receive immediately after purchase—no surprises, no placeholders. It’s the full, professionally formatted document ready for download and use the moment you buy. The file contains complete assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. Instant access upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Las Vegas Sands faces intense rivalry from integrated resort competitors, high buyer power from travel-savvy customers, and regulatory and capital-intensive barriers that limit new entrants while supplier leverage for premium assets remains moderate.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Las Vegas Sands’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Gaming Equipment Providers

The high-end slot machine and electronic table market is concentrated among Light & Wonder and International Game Technology (IGT), giving suppliers moderate bargaining power over Las Vegas Sands because their tech is essential to operations.

Still, Sands' scale—operating 41 properties as of 2025 and sourcing thousands of cabinets—lets it secure volume discounts; public filings show major casino orders can cut unit costs by 10–20%.

Limited Availability of Prime Real Estate

The supply of land for integrated resorts in Macau and Singapore is extremely scarce and tightly controlled by governments, making them the de facto primary suppliers of operating rights and land; Macau granted just 6 gaming concessions for 650,000 annual visitors per casino district in 2024, while Singapore limits Marina Bay Sands-style sites to a handful of government-approved plots. This creates high dependency for Las Vegas Sands, which must meet strict regulatory and concession conditions to retain land use and revenue streams, and risks losing access if compliance or renegotiation fails.

Specialized Labor and Talent Retention

Las Vegas Sands depends on a large, skilled workforce from front-line hospitality to security and casino managers; in 2024 the company reported 46,000 global employees, highlighting scale-sensitive labor needs. In Macau and Singapore, union activity and local-hire rules raise labor bargaining power, forcing higher compliance and recruitment costs—Macau’s minimum wages rose ~6% in 2023. LVS must match market pay and benefits to retain talent; labor costs represented ~22% of operating expenses in 2024, so wage pressure can squeeze margins.

Utility and Infrastructure Dependencies

Large integrated resorts like Las Vegas Sands consume huge amounts of energy, water, and telecoms—MGM reported Strip resorts used ~120–150 kWh per occupied room night in 2023, so Sands faces similar scale and cost exposure.

Most utilities in Nevada and Macau are regional monopolies or state-owned, leaving Sands with effectively zero bargaining power over rates and service terms.

Energy price swings and tighter environmental rules (e.g., Nevada emissions limits, Macau water-reuse mandates) can cut margins; a 10% rise in energy costs can reduce resort EBITDA by 2–4%.

- High consumption: ~120–150 kWh/room-night

- Zero supplier bargaining power

- 10% energy cost rise → EBITDA −2–4%

- Regulatory shifts (water, emissions) raise capex/opex

Luxury Brand and Retail Partnerships

Las Vegas Sands depends on top luxury brands to occupy about 1.2 million sq ft of retail (Marina Bay Sands + Venetian portfolio), driving high-spend visitors; top-tier labels thus hold strong bargaining power since their logos underpin the resorts' luxury positioning.

If a flagship tenant exits, average spend per high-net-worth guest (estimated $4,500 per trip in 2024) and footfall could fall, hurting F&B and gaming revenues tied to retail draw.

- Luxury retail = key traffic driver, ~1.2M sq ft total

- Top brands wield leverage; presence crucial to brand identity

- Loss of anchors risks lower HNW spend (~$4,500/trip)

- Renegotiation pressure on rents and revenue-sharing

Supplier leverage splits: concessions, utilities, luxury tenants strong; gaming moderate

Suppliers wield mixed power: gaming-machine makers (Light & Wonder, IGT) have moderate leverage, utilities and land/concession authorities (Macau, Singapore) have high leverage, luxury retail tenants hold strong leverage, and labor/wage rules (46,000 employees in 2024; labor ~22% of opex) create additional pressure; a 10% energy price rise cuts EBITDA ~2–4%.

| Supplier | Key metric | Power |

|---|---|---|

| Gaming machines | 2 suppliers; bulk discounts 10–20% | Moderate |

| Land/concessions | 6 Macau concessions (2024); few SG plots | High |

| Labor | 46,000 employees (2024); labor ~22% opex | Moderate–High |

| Utilities | 120–150 kWh/room-night; regional monopolies | High |

| Luxury retail | ~1.2M sq ft; HNW spend ~$4,500/trip (2024) | High |

What is included in the product

Tailored Porter's Five Forces analysis for Las Vegas Sands that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats, with strategic commentary to inform investor decks and corporate strategy.

A concise Porter's Five Forces snapshot for Las Vegas Sands—quickly gauge supplier, buyer, competitive, entrant, and substitute pressures to inform strategic moves.

Customers Bargaining Power

High Price Sensitivity in Leisure Segments

General tourists and leisure travelers face many global vacation choices and can compare prices instantly online, raising their bargaining power; TripAdvisor data shows 72% of leisure bookings in 2024 were influenced by price comparisons.

This price-sensitive segment switches destinations or hotel brands for promotions and value, so Sands faces high churn risk during weak demand months; MGM and Wynn promotional discounts climbed ~15% in 2023-24.

As a result, Las Vegas Sands must spend heavily on loyalty and marketing—Sands reported sales & marketing expenses of $1.1 billion in FY2024—to retain these guests.

Leverage of VIP and High-Roller Clients

A small group of VIP and high-roller clients account for roughly 25–35% of Las Vegas Sands’ gaming revenue; losing a handful can swing quarterly EBITDA by millions, so the firm grants outsized concessions like elevated credit lines, private suites, and bespoke comps. In 2024 LVS reported VIP/rolling chip volumes concentrated in Macau VIP rooms, reinforcing bargaining power as operators match personalized offers to retain play.

Corporate and MICE Group Influence

Corporate and MICE group clients wield strong bargaining power over Las Vegas Sands because large bookings—often planned 1–3 years ahead—can cover thousands of room nights and 100,000+ sq ft of convention space, forcing concessions on rates and F&B. In 2024 Sands’ Macau and US properties reported group ADR discounts averaging 12–18% vs transient rates, and group bookings drove ~28% of consolidated RevPAR in 2024. To lock multi-year contracts, Sands offers tailored packages, volume-based rebates, and F&B credits that compress margins but secure occupancy and ancillary spend.

Low Switching Costs for Casual Gamblers

For casual gamblers the cost to switch from Las Vegas Sands to nearby rivals like Wynn or MGM is effectively zero; walkable clusters such as Macau’s Cotai Strip and the Las Vegas Strip let patrons move venues in minutes. In 2024 Macau reported 34% of VIP and mass gamblers visiting multiple properties per trip, so Sands faces constant churn pressure. That forces ongoing refreshes of floor games, F&B, and shows to retain spend.

- Zero incremental travel cost — walkable casino clusters

- 34% of Macau gamblers visit multiple properties (2024)

- High churn → continuous product/amenity investment

Information Transparency and Online Reviews

With travel platforms and social media, guests see prices and reviews instantly; 89% of travelers in 2024 said online reviews influenced their booking, raising customer leverage over Las Vegas Sands (LVS).

Real-time ratings and platforms like Tripadvisor and Google mean guests can enforce service standards; LVS’s Las Vegas and Macau revenue (2024: LVS net revenue $13.4B) is exposed to swift reputational swings.

Negative digital sentiment can redirect traffic fast—studies show a 1-star drop can cut bookings by ~20%—so collective online voice gives modern travelers tangible bargaining power.

- 89% travelers (2024) rely on reviews

- 1-star drop ≈ 20% fewer bookings

- LVS 2024 net revenue $13.4B at reputational risk

Price-sensitive travelers, VIPs & MICE force LVS to spend $1.1B to protect $13.4B revenue

Customers hold high bargaining power: price-sensitive leisure travelers (72% influenced by price comparisons in 2024) can switch destinations instantly, VIPs drive 25–35% of gaming revenue and demand bespoke concessions, and large MICE clients secure 12–18% group ADR discounts; LVS spent $1.1B on sales & marketing in FY2024 to defend share and reported $13.4B net revenue in 2024.

| Metric | 2024 |

|---|---|

| Leisure price-influenced bookings | 72% |

| VIP share of gaming revenue | 25–35% |

| Group ADR discount vs transient | 12–18% |

| S&M expenses (FY2024) | $1.1B |

| LVS net revenue | $13.4B |

Preview Before You Purchase

Las Vegas Sands Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Las Vegas Sands you'll receive immediately after purchase—no surprises, no placeholders. It’s the full, professionally formatted document ready for download and use the moment you buy. The file contains complete assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. Instant access upon payment.