Lazydays Porter's Five Forces Analysis

From Overview to Strategy Blueprint

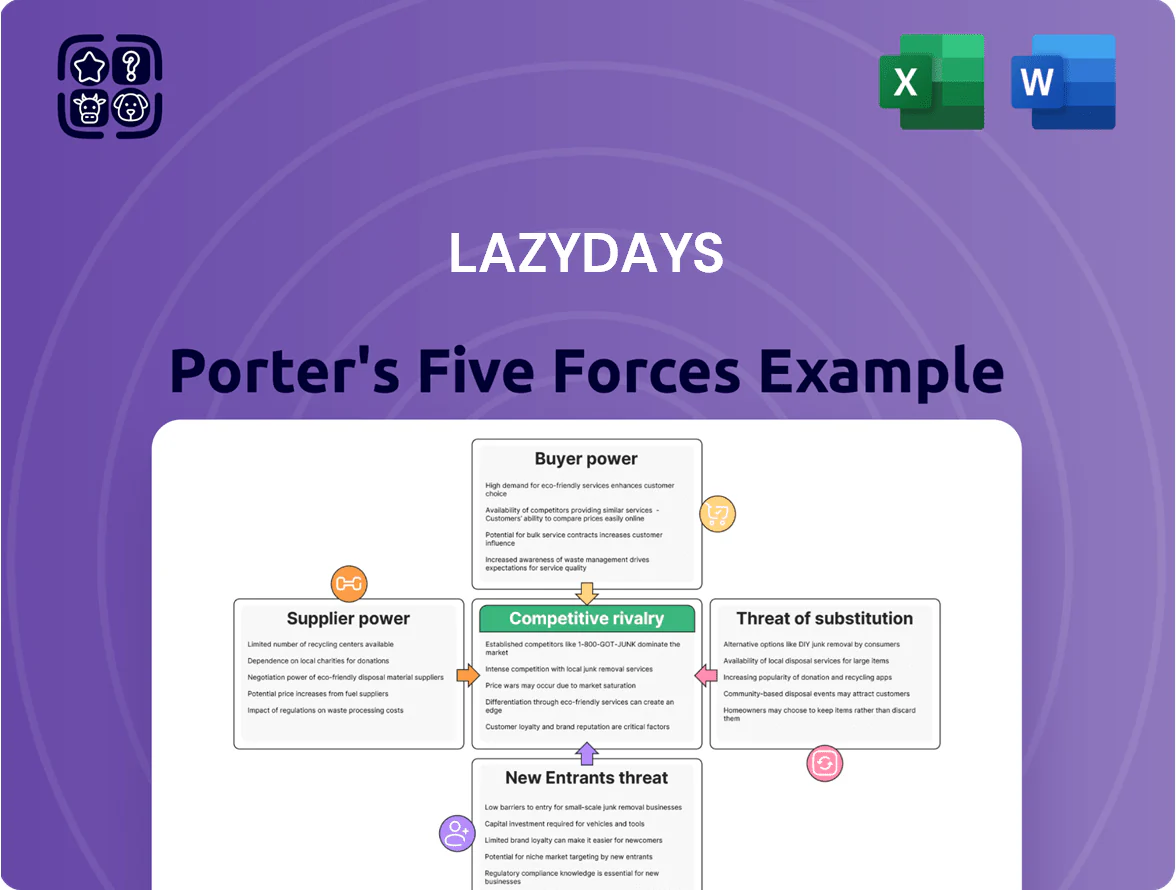

Lazydays faces moderate buyer power, niche supplier relationships, and heightened rivalry as RV demand cycles shift, with potential new entrants and substitutes posing variable threats to margins.

This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Lazydays’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Major RV Manufacturers

The RV manufacturing industry is highly concentrated, with Thor Industries and Forest River holding roughly 60% of U.S. market share combined in 2025, giving suppliers strong pricing power over dealers like Lazydays. This concentration lets manufacturers influence wholesale prices and prioritize inventory allocation, reducing Lazydays’ leverage in negotiations. As a result, Lazydays faces compressed gross margins—dealer gross profit per unit declined about 4–6% industrywide in 2024–25—limiting margin recovery without higher retail prices.

Exclusive Dealership Agreements

Manufacturers use territory-based exclusive dealership agreements that restrict which dealers can sell high-demand RV brands in given regions, making Lazydays dependent on key suppliers for popular models.

As of 2025, top brands supply roughly 60% of U.S. RV retail volume; losing one major partner could cut Lazydays’ inventory mix and sales by an estimated 15–30% in affected markets.

Rising Input and Logistics Costs

Suppliers face volatile aluminum and electronics prices—aluminum rose ~45% from 2020–2024 and semiconductor shortages pushed module costs 30% by 2023—plus higher freight: US spot container rates averaged $3,200 per FEU in 2022 vs $1,600 pre‑pandemic. By late 2025 manufacturers commonly pass >60% of input and logistics hikes to Lazydays, forcing it to absorb margin hits or raise RV retail prices.

Technological Integration and Proprietary Parts

- Proprietary parts raise supplier dependency

- OEM parts ≈35% of service revenue (2024)

- Warranty fulfilment used 18% of service hours

- Stock-outs can cut service profit 3–6%

Supply Chain Lead Times

Supply chain lead times shape Lazydays’ sales rhythm: delayed RV deliveries in 2024 averaged 8–12 weeks vs pre‑pandemic 4–6, straining peak spring demand and reducing throughput.

Manufacturers can prioritize large dealer groups; when production cutbacks hit in Q3 2025, top networks received ~40% of constrained build slots, squeezing smaller dealers.

Lazydays must time floor‑plan draws and preserve $30–50M in liquidity buffers to cover 60–90 day inventory financing swings and avoid interest drag.

- Avg lead time 2024: 8–12 weeks

- Pre‑pandemic lead time: 4–6 weeks

- Top networks got ~40% of slots in Q3 2025

- Recommended liquidity buffer: $30–50M

OEM Dominance Risks: 60% Market Share Cuts Dealer Margins, Service Profits & Sales

Suppliers hold strong leverage: top OEMs (Thor, Forest River) control ~60% U.S. RV supply (2025), enabling price pushes and exclusive territories that compressed dealer gross per unit ~4–6% in 2024–25; OEM parts made ~35% of service revenue (2024) and warranty work used 18% of service hours, so stock-outs cut service profit ~3–6% and losing a major brand could cut Lazydays’ sales 15–30% in affected markets.

| Metric | Value |

|---|---|

| Top OEM share (2025) | ~60% |

| Dealer gross/unit decline (2024–25) | 4–6% |

| OEM parts share of service rev (2024) | ~35% |

| Warranty service hours (2024) | 18% |

| Service profit hit from stock-outs | 3–6% |

| Sales loss if major brand lost | 15–30% |

What is included in the product

Tailored Porter's Five Forces analysis for Lazydays that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive trends impacting market share and profitability.

A concise, one-sheet Porter’s Five Forces view for Lazydays—ideal for fast strategic decisions and boardroom slides.

Customers Bargaining Power

Price Transparency and Digital Research

By 2025, online tools and forums let buyers compare RV prices instantly across dealers; 72% of RV shoppers use online price research before visiting (Statista, 2024), so transparency raises customer bargaining power.

Shoppers now demand price matching or better financing terms—e.g., average RV loan APRs fell to 6.8% in 2024, so competitive financing is a win trigger.

Lazydays must compete on service, certified inspections, and bundled warranties to keep churn below industry retail switch rates of ~18% annually.

Discretionary Nature of RV Purchases

RVs are high-ticket luxury buys—median new RV price rose to about $110,000 in 2024—so most households treat them as discretionary spending.

When GDP slows or the 30-year mortgage-equivalent RV loan rate climbs (RV loan rates averaged ~7.5% in 2024), buyers can delay purchases with little lifestyle impact.

That leverage pushes Lazydays to offer deeper incentives, flexible financing, and seasonal discounts to close deals during downturns.

Availability of Financing Options

The buyer's leverage hinges on external loan access: in 2024 U.S. RV loan originations rose 18% to $10.2 billion, so shoppers often secure lower APRs from banks or credit unions than dealers offer.

If customers find cheaper financing, Lazydays' in-house F&I revenue—about 12–15% of dealership profit per Cox Automotive benchmarks—falls, cutting a key margin stream.

That risk forces Lazydays to match market rates and bundle warranty/service deals; in 2025 many dealers targeted sub-6% APRs for prime borrowers to retain loyalty.

Growth of the Used RV Market

A robust secondary RV market boosts customer bargaining power by offering lower-cost alternatives to new units; in 2024 the used RV market grew ~8% to ~$21.5 billion in U.S. retail value, widening choice for price-sensitive buyers.

Buyers can opt for private sales or used-only dealers if new RVs seem overpriced, forcing Lazydays to make its certified pre-owned (CPO) offers—warranty, inspection, financing—clearly superior.

- Used market ≈ $21.5B (2024)

- Growth ~8% YoY (2024)

- Private/used dealers increase price pressure

- Lazydays CPO must beat price+warranty

Low Switching Costs for Service and Parts

Low switching costs let RV owners take Lazydays-bought vehicles to local independents for repairs, so Lazydays faces constant pressure on service quality and price; this matters because 2024 data show independent RV service share rose ~12% year-over-year in key markets.

Customer retention in service is essential for margins—aftermarket service can deliver 20–30% gross margins—but keeping customers is hard given abundant independent shops and price transparency.

- Independent shops up ~12% (2024)

- Aftermarket margins 20–30%

- Low switching costs = price/service pressure

Buyers seize power: online research up 72%, used RVs $21.5B — dealers fight back with sub-6% APRs

Buyers gained power: 72% research online (Statista, 2024), used RV market ~$21.5B (+8% YoY, 2024), and RV loan originations $10.2B (+18%, 2024), pushing Lazydays to match sub-6% dealer APRs, deeper incentives, CPO warranties, and service bundles to protect 12–15% F&I profit and 20–30% aftermarket margins.

| Metric | 2024 |

|---|---|

| Online research | 72% |

| Used market | $21.5B (+8%) |

| RV loan originations | $10.2B (+18%) |

| Dealer F&I profit | 12–15% |

Preview the Actual Deliverable

Lazydays Porter's Five Forces Analysis

This preview shows the exact Lazydays Porter’s Five Forces analysis you'll receive—fully formatted, professionally written, and ready for immediate download after purchase; no placeholders, samples, or mockups, just the complete deliverable you can use right away.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Lazydays faces moderate buyer power, niche supplier relationships, and heightened rivalry as RV demand cycles shift, with potential new entrants and substitutes posing variable threats to margins.

This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Lazydays’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Major RV Manufacturers

The RV manufacturing industry is highly concentrated, with Thor Industries and Forest River holding roughly 60% of U.S. market share combined in 2025, giving suppliers strong pricing power over dealers like Lazydays. This concentration lets manufacturers influence wholesale prices and prioritize inventory allocation, reducing Lazydays’ leverage in negotiations. As a result, Lazydays faces compressed gross margins—dealer gross profit per unit declined about 4–6% industrywide in 2024–25—limiting margin recovery without higher retail prices.

Exclusive Dealership Agreements

Manufacturers use territory-based exclusive dealership agreements that restrict which dealers can sell high-demand RV brands in given regions, making Lazydays dependent on key suppliers for popular models.

As of 2025, top brands supply roughly 60% of U.S. RV retail volume; losing one major partner could cut Lazydays’ inventory mix and sales by an estimated 15–30% in affected markets.

Rising Input and Logistics Costs

Suppliers face volatile aluminum and electronics prices—aluminum rose ~45% from 2020–2024 and semiconductor shortages pushed module costs 30% by 2023—plus higher freight: US spot container rates averaged $3,200 per FEU in 2022 vs $1,600 pre‑pandemic. By late 2025 manufacturers commonly pass >60% of input and logistics hikes to Lazydays, forcing it to absorb margin hits or raise RV retail prices.

Technological Integration and Proprietary Parts

- Proprietary parts raise supplier dependency

- OEM parts ≈35% of service revenue (2024)

- Warranty fulfilment used 18% of service hours

- Stock-outs can cut service profit 3–6%

Supply Chain Lead Times

Supply chain lead times shape Lazydays’ sales rhythm: delayed RV deliveries in 2024 averaged 8–12 weeks vs pre‑pandemic 4–6, straining peak spring demand and reducing throughput.

Manufacturers can prioritize large dealer groups; when production cutbacks hit in Q3 2025, top networks received ~40% of constrained build slots, squeezing smaller dealers.

Lazydays must time floor‑plan draws and preserve $30–50M in liquidity buffers to cover 60–90 day inventory financing swings and avoid interest drag.

- Avg lead time 2024: 8–12 weeks

- Pre‑pandemic lead time: 4–6 weeks

- Top networks got ~40% of slots in Q3 2025

- Recommended liquidity buffer: $30–50M

OEM Dominance Risks: 60% Market Share Cuts Dealer Margins, Service Profits & Sales

Suppliers hold strong leverage: top OEMs (Thor, Forest River) control ~60% U.S. RV supply (2025), enabling price pushes and exclusive territories that compressed dealer gross per unit ~4–6% in 2024–25; OEM parts made ~35% of service revenue (2024) and warranty work used 18% of service hours, so stock-outs cut service profit ~3–6% and losing a major brand could cut Lazydays’ sales 15–30% in affected markets.

| Metric | Value |

|---|---|

| Top OEM share (2025) | ~60% |

| Dealer gross/unit decline (2024–25) | 4–6% |

| OEM parts share of service rev (2024) | ~35% |

| Warranty service hours (2024) | 18% |

| Service profit hit from stock-outs | 3–6% |

| Sales loss if major brand lost | 15–30% |

What is included in the product

Tailored Porter's Five Forces analysis for Lazydays that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive trends impacting market share and profitability.

A concise, one-sheet Porter’s Five Forces view for Lazydays—ideal for fast strategic decisions and boardroom slides.

Customers Bargaining Power

Price Transparency and Digital Research

By 2025, online tools and forums let buyers compare RV prices instantly across dealers; 72% of RV shoppers use online price research before visiting (Statista, 2024), so transparency raises customer bargaining power.

Shoppers now demand price matching or better financing terms—e.g., average RV loan APRs fell to 6.8% in 2024, so competitive financing is a win trigger.

Lazydays must compete on service, certified inspections, and bundled warranties to keep churn below industry retail switch rates of ~18% annually.

Discretionary Nature of RV Purchases

RVs are high-ticket luxury buys—median new RV price rose to about $110,000 in 2024—so most households treat them as discretionary spending.

When GDP slows or the 30-year mortgage-equivalent RV loan rate climbs (RV loan rates averaged ~7.5% in 2024), buyers can delay purchases with little lifestyle impact.

That leverage pushes Lazydays to offer deeper incentives, flexible financing, and seasonal discounts to close deals during downturns.

Availability of Financing Options

The buyer's leverage hinges on external loan access: in 2024 U.S. RV loan originations rose 18% to $10.2 billion, so shoppers often secure lower APRs from banks or credit unions than dealers offer.

If customers find cheaper financing, Lazydays' in-house F&I revenue—about 12–15% of dealership profit per Cox Automotive benchmarks—falls, cutting a key margin stream.

That risk forces Lazydays to match market rates and bundle warranty/service deals; in 2025 many dealers targeted sub-6% APRs for prime borrowers to retain loyalty.

Growth of the Used RV Market

A robust secondary RV market boosts customer bargaining power by offering lower-cost alternatives to new units; in 2024 the used RV market grew ~8% to ~$21.5 billion in U.S. retail value, widening choice for price-sensitive buyers.

Buyers can opt for private sales or used-only dealers if new RVs seem overpriced, forcing Lazydays to make its certified pre-owned (CPO) offers—warranty, inspection, financing—clearly superior.

- Used market ≈ $21.5B (2024)

- Growth ~8% YoY (2024)

- Private/used dealers increase price pressure

- Lazydays CPO must beat price+warranty

Low Switching Costs for Service and Parts

Low switching costs let RV owners take Lazydays-bought vehicles to local independents for repairs, so Lazydays faces constant pressure on service quality and price; this matters because 2024 data show independent RV service share rose ~12% year-over-year in key markets.

Customer retention in service is essential for margins—aftermarket service can deliver 20–30% gross margins—but keeping customers is hard given abundant independent shops and price transparency.

- Independent shops up ~12% (2024)

- Aftermarket margins 20–30%

- Low switching costs = price/service pressure

Buyers seize power: online research up 72%, used RVs $21.5B — dealers fight back with sub-6% APRs

Buyers gained power: 72% research online (Statista, 2024), used RV market ~$21.5B (+8% YoY, 2024), and RV loan originations $10.2B (+18%, 2024), pushing Lazydays to match sub-6% dealer APRs, deeper incentives, CPO warranties, and service bundles to protect 12–15% F&I profit and 20–30% aftermarket margins.

| Metric | 2024 |

|---|---|

| Online research | 72% |

| Used market | $21.5B (+8%) |

| RV loan originations | $10.2B (+18%) |

| Dealer F&I profit | 12–15% |

Preview the Actual Deliverable

Lazydays Porter's Five Forces Analysis

This preview shows the exact Lazydays Porter’s Five Forces analysis you'll receive—fully formatted, professionally written, and ready for immediate download after purchase; no placeholders, samples, or mockups, just the complete deliverable you can use right away.