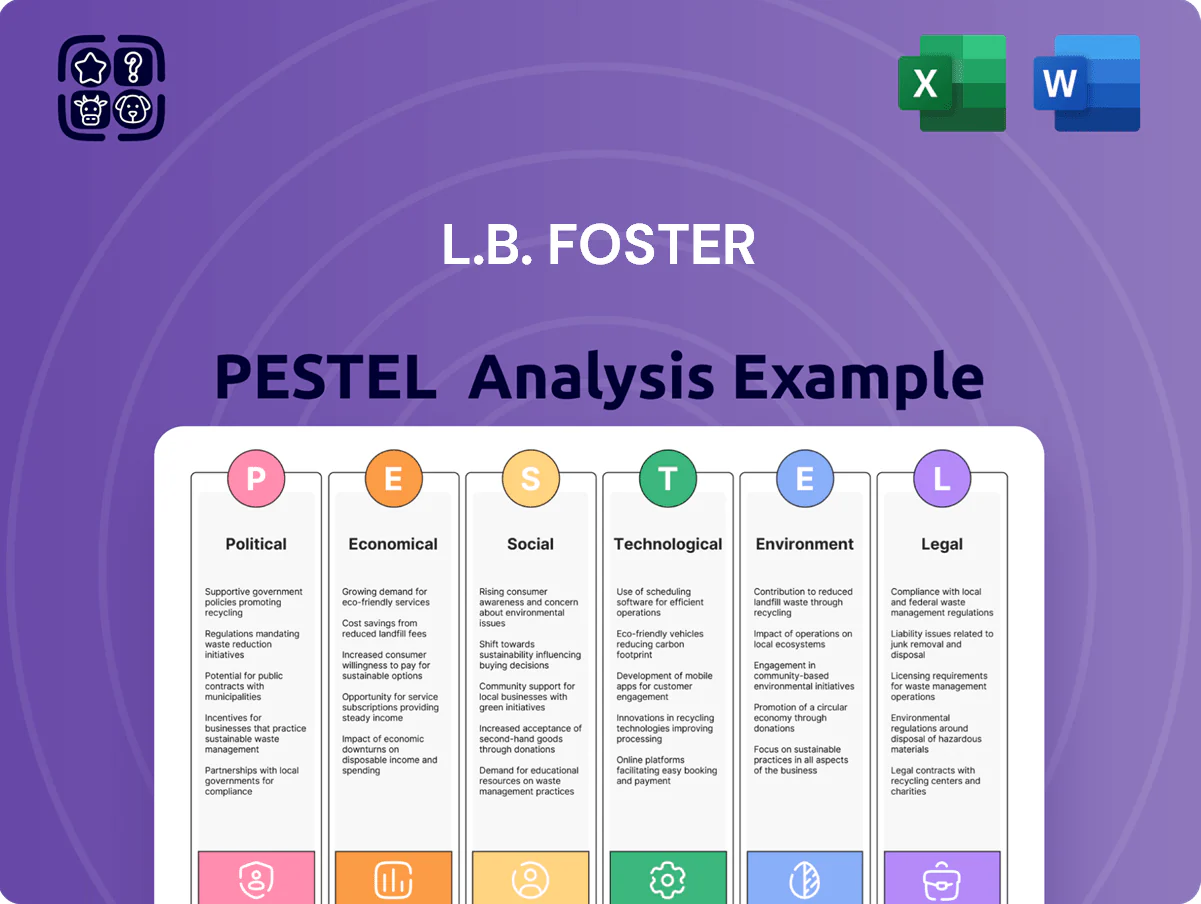

L.B. Foster PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our concise PESTLE Analysis of L.B. Foster—highlighting regulatory risks, infrastructure demand trends, and tech-driven opportunities shaping its future; perfect for investors and strategists seeking clear, actionable intelligence. Purchase the full report to access the complete breakdown, editable charts, and recommendations ready for immediate use.

Political factors

Infrastructure Investment and Jobs Act funding

The continued disbursement of $1.2 trillion from the Infrastructure Investment and Jobs Act through 2025 is a primary driver for L.B. Foster, with estimated federal allocations of ~$110 billion for rail and $110 billion for highways supporting demand for the company’s steel and concrete solutions.

Buy America compliance requirements

Strict domestic sourcing mandates under the Build America, Buy America Act favor domestic manufacturers like L.B. Foster; with U.S. content thresholds rising to 55% for iron/steel and higher for construction materials in 2024, L.B. Foster’s compliant supply chain positions it for priority on federally funded transit and bridge projects.

International trade and tariff policies

Ongoing US tariffs on steel and aluminum raised input costs for L.B. Foster, with US Section 232 tariffs adding roughly 10–25% to imported coil prices in 2024, pressuring gross margins on rail and piling segments where materials comprise ~30% of COGS; tariff-driven cost pass-through shapes North American pricing strategy and contributed to a 2024 YTD margin squeeze versus 2023; deteriorating US-China and EU-Russia relations risk supply-chain disruptions and could slow expansion of friction-management sales in Europe and Asia, where 2024 rail infrastructure spend varies—e.g., EU investment plans ~€80bn (2024–27) and Asia-Pacific rail capex growth ~4–6% in 2024—affecting market access and revenue forecasts.

Government transit and rail subsidies

Political support for passenger rail and urban transit drives trackwork and friction management demand; U.S. federal transit obligations authorized $91.4 billion in FY2024 formula and discretionary grants, boosting projects that benefit L.B. Foster’s rail segment.

Legislative focus on cutting highway congestion increases subsidies to commuter rail authorities—Amtrak and regional agencies saw combined federal/state funding rise 6% in 2023–24—supporting predictable orders.

Shifts to austerity or reduced transit appropriations, however, could dent rail revenues: a 10% funding cut across major commuter agencies might reduce addressable market for track products and services by an estimated $200–400 million annually.

- FY2024 U.S. transit grants $91.4B — positive for rail orders

- 2023–24 federal/state transit funding +6% — improves demand visibility

- Potential 10% funding cut could shrink addressable market ~$200–400M

Geopolitical stability in global operations

Geopolitical instability in markets where L.B. Foster has plants or sales offices can delay production and contracts; by end‑2025 the company flags supply‑chain exposure for specialty components tied to 18% of project cost in some rail contracts. US alignment with trading partners remains vital for exports—US rail tech tariffs and export controls could affect revenues given 22% of 2024 sales were international.

- 18% specialty component exposure in some projects

- 22% of 2024 sales international

- End‑2025 monitoring of supply and export risks

Infrastructure boom lifts L.B. Foster but tariffs, materials costs and export risks bite

Federal infrastructure funding (IIJA $1.2T through 2025) and FY2024 transit grants $91.4B boost demand for L.B. Foster’s rail and highway products; Build America, Buy America sourcing (2024 iron/steel ~55% U.S. content) favors domestic supply. Tariffs (Section 232) raised imported coil costs ~10–25% in 2024, squeezing margins as materials ≈30% of COGS; 22% of 2024 sales were international, exposing exports to geopolitical/export-control risk.

| Metric | Value |

|---|---|

| IIJA total | $1.2T (through 2025) |

| FY2024 transit grants | $91.4B |

| U.S. content (iron/steel) | ~55% (2024) |

| Tariff impact on imported coil | ~10–25% (2024) |

| Materials as % of COGS | ~30% |

| International sales | 22% (2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect L.B. Foster across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific regulatory context.

Concise PESTLE summary of L.B. Foster, visually segmented by category for quick interpretation and easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Raw material price volatility

Raw material price volatility—notably a 22% year‑over‑year rise in steel and a 15% increase in cement prices through 2024–2025—significantly pressures L.B. Foster’s margin profile as of late 2025.

Such swings in global commodity markets force the company to adopt agile pricing models and use hedging; L.B. Foster reported a 10–12% increase in commodity hedging coverage in 2025.

During inflationary cycles, input cost spikes can compress margins when long‑term contracts prevent full pass‑through; industry data show margins for infrastructure manufacturers fell by ~180 basis points in 2024–2025 when costs outpaced contract escalators.

Interest rate environment impact

At end-2025, the US federal funds rate near 5.25%–5.50% raised financing costs for infrastructure, increasing capital expenses for L.B. Foster’s equipment and potentially delaying private construction as higher rates squeezed developer returns.

Higher borrowing pushed municipal bond yields—10-year muni yields averaging ~3.8% in 2025—making some public projects more costly, while any easing in 2025–early 2026 would spur municipal issuance and project restarts.

Labor market conditions and costs

Tight U.S. labor market for skilled fabricators, engineers, and manufacturing staff—unemployment near 3.7% in 2025 Q4—keeps upward pressure on wages, with manufacturing average hourly earnings up about 4.5% year-over-year as of 2025. L.B. Foster must balance competitive pay against productivity to protect margins in infrastructure contracts. Accelerated automation investments, which reduced labor hours by an estimated 7–10% in comparable peers in 2024, are a strategic response to rising human capital costs.

Currency exchange rate fluctuations

With operations in the UK and Canada, L.B. Foster faces transaction and translation exposure as USD movements vs GBP and CAD alter reported revenue; a 10% USD appreciation would reduce foreign-reported USD earnings materially given 2024 international revenue of roughly $150m.

Regional economic health—UK GDP growth ~0.5% (2024 est.) and Canada ~1.4% (2024 est.)—shapes demand for rail friction management systems tied to infrastructure spending.

- Transaction/translation risk from USD/GBP/CAD volatility

- 10% USD move could materially swing ~2024 $150m international revenue

- UK growth ~0.5% and Canada ~1.4% (2024) affect local demand

Global supply chain resilience

The 2025 economic landscape demands resilient, diversified supply chains to prevent manufacturing bottlenecks; global shipping delays rose by 18% in 2024, increasing lead times for construction materials. Disruptions in logistics can postpone delivery of piling and bridge products, risking contract penalties and revenue loss—construction sector delays cost an estimated $120 billion globally in 2024. Effective lead-time management directly influences L.B. Foster’s market share amid tighter global capacity.

- 2024 shipping delays +18%

- Construction delays cost ~$120B (2024)

- Lead-time control = key competitive factor

Rising steel/cement costs, higher rates and FX risk threaten margins and international revenue

Commodity-driven margin pressure: steel +22% and cement +15% (2024–25); hedging coverage +10–12% (2025). Higher rates (fed funds ~5.25–5.50% end‑2025) raised CAPEX/financing; muni yields ~3.8% (2025). Tight labor (unemp ~3.7%, manufacturing AHE +4.5% y/y 2025) and USD strength risk on ~$150m 2024 international revenue; UK GDP ~0.5%, Canada ~1.4% (2024).

| Metric | Value |

|---|---|

| Steel | +22% |

| Cement | +15% |

| Fed funds | 5.25–5.50% |

| Muni yield | ~3.8% |

| Unemp | 3.7% |

| Intl revenue (2024) | $150m |

Same Document Delivered

L.B. Foster PESTLE Analysis

The preview shown here is the exact L.B. Foster PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use, with no placeholders or teasers.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our concise PESTLE Analysis of L.B. Foster—highlighting regulatory risks, infrastructure demand trends, and tech-driven opportunities shaping its future; perfect for investors and strategists seeking clear, actionable intelligence. Purchase the full report to access the complete breakdown, editable charts, and recommendations ready for immediate use.

Political factors

Infrastructure Investment and Jobs Act funding

The continued disbursement of $1.2 trillion from the Infrastructure Investment and Jobs Act through 2025 is a primary driver for L.B. Foster, with estimated federal allocations of ~$110 billion for rail and $110 billion for highways supporting demand for the company’s steel and concrete solutions.

Buy America compliance requirements

Strict domestic sourcing mandates under the Build America, Buy America Act favor domestic manufacturers like L.B. Foster; with U.S. content thresholds rising to 55% for iron/steel and higher for construction materials in 2024, L.B. Foster’s compliant supply chain positions it for priority on federally funded transit and bridge projects.

International trade and tariff policies

Ongoing US tariffs on steel and aluminum raised input costs for L.B. Foster, with US Section 232 tariffs adding roughly 10–25% to imported coil prices in 2024, pressuring gross margins on rail and piling segments where materials comprise ~30% of COGS; tariff-driven cost pass-through shapes North American pricing strategy and contributed to a 2024 YTD margin squeeze versus 2023; deteriorating US-China and EU-Russia relations risk supply-chain disruptions and could slow expansion of friction-management sales in Europe and Asia, where 2024 rail infrastructure spend varies—e.g., EU investment plans ~€80bn (2024–27) and Asia-Pacific rail capex growth ~4–6% in 2024—affecting market access and revenue forecasts.

Government transit and rail subsidies

Political support for passenger rail and urban transit drives trackwork and friction management demand; U.S. federal transit obligations authorized $91.4 billion in FY2024 formula and discretionary grants, boosting projects that benefit L.B. Foster’s rail segment.

Legislative focus on cutting highway congestion increases subsidies to commuter rail authorities—Amtrak and regional agencies saw combined federal/state funding rise 6% in 2023–24—supporting predictable orders.

Shifts to austerity or reduced transit appropriations, however, could dent rail revenues: a 10% funding cut across major commuter agencies might reduce addressable market for track products and services by an estimated $200–400 million annually.

- FY2024 U.S. transit grants $91.4B — positive for rail orders

- 2023–24 federal/state transit funding +6% — improves demand visibility

- Potential 10% funding cut could shrink addressable market ~$200–400M

Geopolitical stability in global operations

Geopolitical instability in markets where L.B. Foster has plants or sales offices can delay production and contracts; by end‑2025 the company flags supply‑chain exposure for specialty components tied to 18% of project cost in some rail contracts. US alignment with trading partners remains vital for exports—US rail tech tariffs and export controls could affect revenues given 22% of 2024 sales were international.

- 18% specialty component exposure in some projects

- 22% of 2024 sales international

- End‑2025 monitoring of supply and export risks

Infrastructure boom lifts L.B. Foster but tariffs, materials costs and export risks bite

Federal infrastructure funding (IIJA $1.2T through 2025) and FY2024 transit grants $91.4B boost demand for L.B. Foster’s rail and highway products; Build America, Buy America sourcing (2024 iron/steel ~55% U.S. content) favors domestic supply. Tariffs (Section 232) raised imported coil costs ~10–25% in 2024, squeezing margins as materials ≈30% of COGS; 22% of 2024 sales were international, exposing exports to geopolitical/export-control risk.

| Metric | Value |

|---|---|

| IIJA total | $1.2T (through 2025) |

| FY2024 transit grants | $91.4B |

| U.S. content (iron/steel) | ~55% (2024) |

| Tariff impact on imported coil | ~10–25% (2024) |

| Materials as % of COGS | ~30% |

| International sales | 22% (2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect L.B. Foster across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific regulatory context.

Concise PESTLE summary of L.B. Foster, visually segmented by category for quick interpretation and easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Raw material price volatility

Raw material price volatility—notably a 22% year‑over‑year rise in steel and a 15% increase in cement prices through 2024–2025—significantly pressures L.B. Foster’s margin profile as of late 2025.

Such swings in global commodity markets force the company to adopt agile pricing models and use hedging; L.B. Foster reported a 10–12% increase in commodity hedging coverage in 2025.

During inflationary cycles, input cost spikes can compress margins when long‑term contracts prevent full pass‑through; industry data show margins for infrastructure manufacturers fell by ~180 basis points in 2024–2025 when costs outpaced contract escalators.

Interest rate environment impact

At end-2025, the US federal funds rate near 5.25%–5.50% raised financing costs for infrastructure, increasing capital expenses for L.B. Foster’s equipment and potentially delaying private construction as higher rates squeezed developer returns.

Higher borrowing pushed municipal bond yields—10-year muni yields averaging ~3.8% in 2025—making some public projects more costly, while any easing in 2025–early 2026 would spur municipal issuance and project restarts.

Labor market conditions and costs

Tight U.S. labor market for skilled fabricators, engineers, and manufacturing staff—unemployment near 3.7% in 2025 Q4—keeps upward pressure on wages, with manufacturing average hourly earnings up about 4.5% year-over-year as of 2025. L.B. Foster must balance competitive pay against productivity to protect margins in infrastructure contracts. Accelerated automation investments, which reduced labor hours by an estimated 7–10% in comparable peers in 2024, are a strategic response to rising human capital costs.

Currency exchange rate fluctuations

With operations in the UK and Canada, L.B. Foster faces transaction and translation exposure as USD movements vs GBP and CAD alter reported revenue; a 10% USD appreciation would reduce foreign-reported USD earnings materially given 2024 international revenue of roughly $150m.

Regional economic health—UK GDP growth ~0.5% (2024 est.) and Canada ~1.4% (2024 est.)—shapes demand for rail friction management systems tied to infrastructure spending.

- Transaction/translation risk from USD/GBP/CAD volatility

- 10% USD move could materially swing ~2024 $150m international revenue

- UK growth ~0.5% and Canada ~1.4% (2024) affect local demand

Global supply chain resilience

The 2025 economic landscape demands resilient, diversified supply chains to prevent manufacturing bottlenecks; global shipping delays rose by 18% in 2024, increasing lead times for construction materials. Disruptions in logistics can postpone delivery of piling and bridge products, risking contract penalties and revenue loss—construction sector delays cost an estimated $120 billion globally in 2024. Effective lead-time management directly influences L.B. Foster’s market share amid tighter global capacity.

- 2024 shipping delays +18%

- Construction delays cost ~$120B (2024)

- Lead-time control = key competitive factor

Rising steel/cement costs, higher rates and FX risk threaten margins and international revenue

Commodity-driven margin pressure: steel +22% and cement +15% (2024–25); hedging coverage +10–12% (2025). Higher rates (fed funds ~5.25–5.50% end‑2025) raised CAPEX/financing; muni yields ~3.8% (2025). Tight labor (unemp ~3.7%, manufacturing AHE +4.5% y/y 2025) and USD strength risk on ~$150m 2024 international revenue; UK GDP ~0.5%, Canada ~1.4% (2024).

| Metric | Value |

|---|---|

| Steel | +22% |

| Cement | +15% |

| Fed funds | 5.25–5.50% |

| Muni yield | ~3.8% |

| Unemp | 3.7% |

| Intl revenue (2024) | $150m |

Same Document Delivered

L.B. Foster PESTLE Analysis

The preview shown here is the exact L.B. Foster PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use, with no placeholders or teasers.