Lecta SA Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

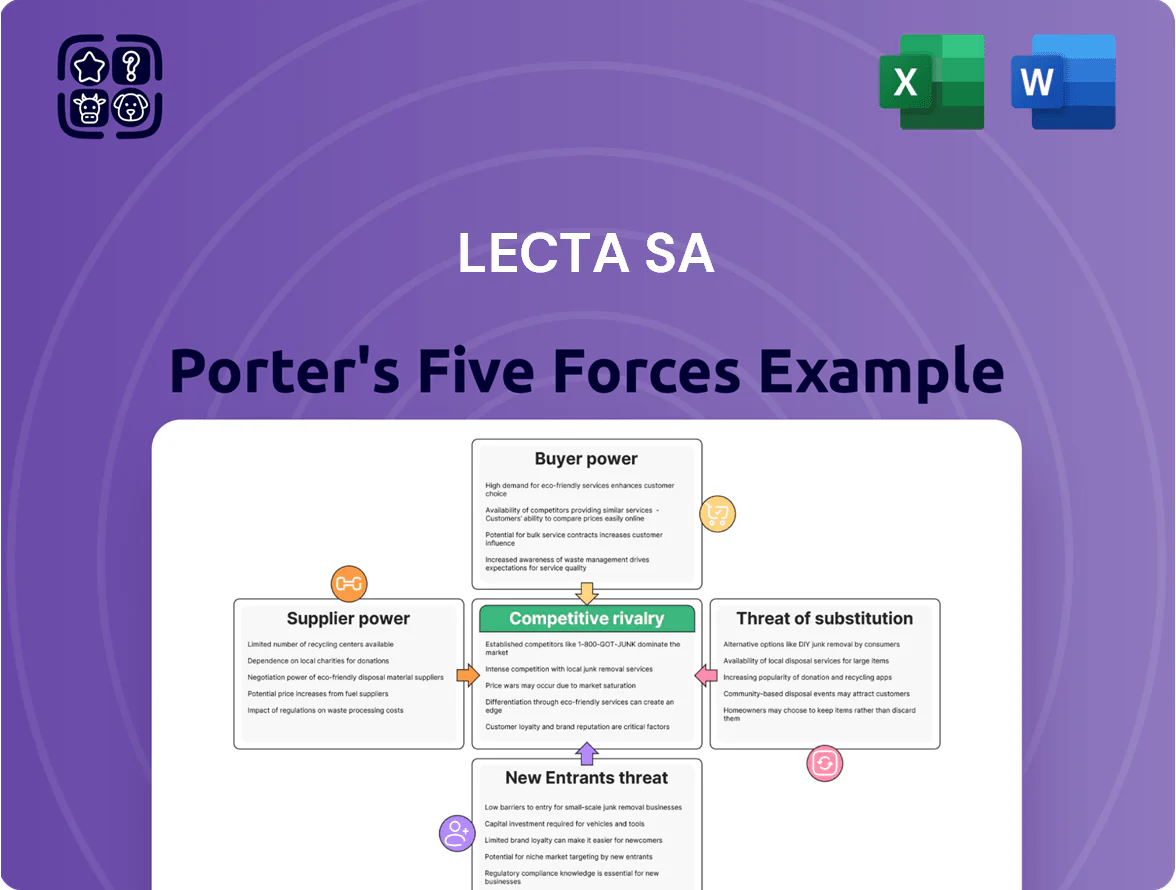

Lecta SA operates in a mature, commoditized paper market where supplier concentration and buyer price sensitivity shape margins, while moderate barriers and niche differentiation temper new entrant and substitute threats; competitive rivalry remains intense among European producers. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Lecta SA’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of raw material pulp prices

Lecta is exposed to volatile wood-pulp prices—global softwood pulp rose 28% in 2024 and averaged $900/ton in H1 2025, driven by lower Scandinavian harvests and strong Asian demand.

Large pulp suppliers (e.g., Suzano, CMPC) held market power in late 2025, enabling price-setting during tight supply windows and pressuring Lecta’s gross margins by an estimated 150–300 bps in 2025 YTD.

Maintaining margins requires dynamic hedging, multi-sourcing, and long-term contracts; Lecta reported 12% of pulp bought via fixed-price contracts in 2024, leaving material risk.

Energy market fluctuations in the European region

Paper making is energy intensive, so Lecta SA remains highly exposed to European gas and electricity prices; industrial power rates rose ~45% in 2022 and, while wholesale prices fell ~60% by end-2024, average EU industrial electricity still ran near €0.18/kWh in 2024, keeping margins tight.

Energy suppliers retain leverage: a handful of gas exporters and utilities control pipeline and LNG capacity, so price pass-through risks persist for pulp and coating inputs.

Any new Russia-Ukraine flare-up, Nord Stream disruptions, or EU carbon (ETS) tightening could spike costs rapidly; a 10% gas price jump can add several percentage points to Lecta’s COGS on thin paper margins.

Concentration of chemical and additive providers

Supplier concentration for specialty chemicals and minerals gives few vendors pricing and timing power; in 2024 roughly 60–70% of advanced coating additives came from top five global suppliers, raising cost volatility for Lecta SA.

Innovative or sustainable components command premiums—price spreads of 15–30%—so Lecta must secure long-term contracts and dual sourcing to protect its premium coated-paper margins.

Sustainability and certification requirements

Suppliers of FSC or PEFC certified timber and recycled fibers gained bargaining power as EU rules like the 2023 Nature Restoration Law and 2024 EU Deforestation Regulation raised compliance costs; certified wood premiums rose ~12–18% in 2024, squeezing pulp buyers.

Lecta mandates FSC/PEFC inputs to meet regs and customer demand, so its sourcing is tied to a small certified supplier pool that can push prices and tighter lead times, raising COGS and margin pressure.

- Certified supplier pool small — premiums +12–18% (2024)

- EU regs: 2023 Nature Restoration Law; 2024 Deforestation Regulation

- Lecta requires FSC/PEFC — increases COGS and supply risk

Logistics and transportation provider leverage

Logistics and transportation providers wield rising leverage over Lecta SA because heavy paper distribution depends on continent-wide shipping and trucking networks; diesel price spikes (EU diesel up ~28% in 2023 vs 2021) and EU driver shortages (estimated 400,000 shortfall in 2022) let carriers push rates up.

Higher freight costs and spot-rate volatility raise Lecta's cost per tonne and risk of delivery delays; reliance on third-party carriers makes price pass-through harder in competitive paper markets.

- Diesel +28% (2021–2023 EU)

- Driver shortfall ~400,000 (EU, 2022)

- Higher spot freight → margin pressure per tonne

- Third-party dependence increases service risk

Supplier squeeze: pulp, energy and freight lift costs and shave 150–300bps off Lecta margins

Suppliers (pulp, energy, coatings, certified fiber, logistics) hold strong leverage over Lecta SA: pulp suppliers concentrated (Suzano/CMPC) pushed 2024–H1 2025 pulp to ~$900/t (softwood +28% in 2024), certified wood premiums +12–18% (2024), EU industrial electricity ~€0.18/kWh (2024), and freight/diesel shocks (diesel +28% 2021–2023) all pressured margins ~150–300 bps.

| Input | Key 2024–2025 data |

|---|---|

| Pulp (softwood) | $900/t avg H1 2025; +28% 2024 |

| Certified wood | Premium +12–18% (2024) |

| Electricity (EU) | €0.18/kWh avg (2024) |

| Freight/diesel | Diesel +28% (2021–2023) |

What is included in the product

Tailored Porter's Five Forces for Lecta SA, revealing competitive intensity, buyer/supplier leverage, threat of entrants and substitutes, and strategic barriers that shape its pricing power and profitability.

A concise, one-sheet Porter's Five Forces summary for Lecta SA—ideal for quick strategic decisions and boardroom presentations.

Customers Bargaining Power

Consolidation of large publishing and retail groups

Major publishing and retail customers increasingly consolidate: the top 10 European publishers and three retail chains account for ~45% of industrial paper purchases, letting them demand price cuts of 5–12% on bulk orders; they can reallocate contracts between suppliers with low switching costs, so Lecta must match prices or add services (custom coatings, just-in-time delivery) to protect volumes and margins.

Low switching costs for standard paper grades

For commodity-grade coated and uncoated papers, customers face very low switching costs, so price is king and Lecta SA must compete on cost efficiency and delivery reliability in its graphic paper segment; in 2024 global coated paper prices fell ~8% year-on-year and European demand dropped 4.2%, keeping margin pressure high. The lack of technical barriers to change suppliers sustains strong buyer bargaining power and compresses Lecta’s operating margins.

Increasing demand for sustainable packaging solutions

As global FMCG brands cut plastic (EU Single-Use Plastics Directive expanded 2024) demand for paper packaging rose ~6% CAGR 2019–24, pushing customers to require Lecta SA deliver certified recycled or FSC papers and lower carbon scores; this raises buyer leverage to insist on life-cycle assessments (LCA) and specific barrier/coating performance, accelerating Lecta’s R&D and forcing greater supply-chain transparency to meet corporate Net Zero pledges.

Price transparency in global paper markets

Real-time price data and digital procurement platforms have increased transparency in global paper markets, letting professional buyers compare Lecta SA prices against EU peers instantly; according to Eurostat and industry reports, benchmark pulp and paper spot indices fell ~8% in 2024, tightening pricing power.

This visibility reduces Lecta’s ability to sustain premiums and fuels tougher negotiations: procurement teams now demand price concessions aligned with current spot benchmarks and 2024 average list-price declines.

Customization needs for specialty label products

In specialty labels and flexible packaging, customers demand precise technical specs—adhesion, opacity, chemical resistance—creating supplier-client interdependence that cushions Lecta SA (2024 sales €1.15bn) from pure price push.

Still, large industrial buyers set standards and KPIs, driving 20–35% of procurement to multi-supplier strategies to avoid single-source risk, keeping bargaining power high.

- Technical specs raise switching costs

- Large clients define KPIs

- Multi-sourcing 20–35% of spend

- Lecta’s 2024 revenue €1.15bn aids leverage

Buyers Wield Power: Price Cuts Squeeze Lecta Margins, Specialty Packaging Offers Relief

Buyers are highly powerful: top publishers/retailers (~45% share) force 5–12% bulk discounts; 2024 coated-paper spot index fell ~8% and EU demand down 4.2%, shrinking margins; procurement tools and live indices enable instant price comparison so Lecta must match prices or add services; specialty labels and packaging (higher specs) raise switching costs, supporting some margin protection for Lecta (2024 sales €1.15bn).

| Metric | 2024 |

|---|---|

| Top buyers share | ~45% |

| Coated-paper spot change | -8% |

| EU demand change | -4.2% |

| Bulk discount range | 5–12% |

| Lecta revenue | €1.15bn |

Preview Before You Purchase

Lecta SA Porter's Five Forces Analysis

This preview shows the exact Lecta SA Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Lecta SA operates in a mature, commoditized paper market where supplier concentration and buyer price sensitivity shape margins, while moderate barriers and niche differentiation temper new entrant and substitute threats; competitive rivalry remains intense among European producers. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Lecta SA’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of raw material pulp prices

Lecta is exposed to volatile wood-pulp prices—global softwood pulp rose 28% in 2024 and averaged $900/ton in H1 2025, driven by lower Scandinavian harvests and strong Asian demand.

Large pulp suppliers (e.g., Suzano, CMPC) held market power in late 2025, enabling price-setting during tight supply windows and pressuring Lecta’s gross margins by an estimated 150–300 bps in 2025 YTD.

Maintaining margins requires dynamic hedging, multi-sourcing, and long-term contracts; Lecta reported 12% of pulp bought via fixed-price contracts in 2024, leaving material risk.

Energy market fluctuations in the European region

Paper making is energy intensive, so Lecta SA remains highly exposed to European gas and electricity prices; industrial power rates rose ~45% in 2022 and, while wholesale prices fell ~60% by end-2024, average EU industrial electricity still ran near €0.18/kWh in 2024, keeping margins tight.

Energy suppliers retain leverage: a handful of gas exporters and utilities control pipeline and LNG capacity, so price pass-through risks persist for pulp and coating inputs.

Any new Russia-Ukraine flare-up, Nord Stream disruptions, or EU carbon (ETS) tightening could spike costs rapidly; a 10% gas price jump can add several percentage points to Lecta’s COGS on thin paper margins.

Concentration of chemical and additive providers

Supplier concentration for specialty chemicals and minerals gives few vendors pricing and timing power; in 2024 roughly 60–70% of advanced coating additives came from top five global suppliers, raising cost volatility for Lecta SA.

Innovative or sustainable components command premiums—price spreads of 15–30%—so Lecta must secure long-term contracts and dual sourcing to protect its premium coated-paper margins.

Sustainability and certification requirements

Suppliers of FSC or PEFC certified timber and recycled fibers gained bargaining power as EU rules like the 2023 Nature Restoration Law and 2024 EU Deforestation Regulation raised compliance costs; certified wood premiums rose ~12–18% in 2024, squeezing pulp buyers.

Lecta mandates FSC/PEFC inputs to meet regs and customer demand, so its sourcing is tied to a small certified supplier pool that can push prices and tighter lead times, raising COGS and margin pressure.

- Certified supplier pool small — premiums +12–18% (2024)

- EU regs: 2023 Nature Restoration Law; 2024 Deforestation Regulation

- Lecta requires FSC/PEFC — increases COGS and supply risk

Logistics and transportation provider leverage

Logistics and transportation providers wield rising leverage over Lecta SA because heavy paper distribution depends on continent-wide shipping and trucking networks; diesel price spikes (EU diesel up ~28% in 2023 vs 2021) and EU driver shortages (estimated 400,000 shortfall in 2022) let carriers push rates up.

Higher freight costs and spot-rate volatility raise Lecta's cost per tonne and risk of delivery delays; reliance on third-party carriers makes price pass-through harder in competitive paper markets.

- Diesel +28% (2021–2023 EU)

- Driver shortfall ~400,000 (EU, 2022)

- Higher spot freight → margin pressure per tonne

- Third-party dependence increases service risk

Supplier squeeze: pulp, energy and freight lift costs and shave 150–300bps off Lecta margins

Suppliers (pulp, energy, coatings, certified fiber, logistics) hold strong leverage over Lecta SA: pulp suppliers concentrated (Suzano/CMPC) pushed 2024–H1 2025 pulp to ~$900/t (softwood +28% in 2024), certified wood premiums +12–18% (2024), EU industrial electricity ~€0.18/kWh (2024), and freight/diesel shocks (diesel +28% 2021–2023) all pressured margins ~150–300 bps.

| Input | Key 2024–2025 data |

|---|---|

| Pulp (softwood) | $900/t avg H1 2025; +28% 2024 |

| Certified wood | Premium +12–18% (2024) |

| Electricity (EU) | €0.18/kWh avg (2024) |

| Freight/diesel | Diesel +28% (2021–2023) |

What is included in the product

Tailored Porter's Five Forces for Lecta SA, revealing competitive intensity, buyer/supplier leverage, threat of entrants and substitutes, and strategic barriers that shape its pricing power and profitability.

A concise, one-sheet Porter's Five Forces summary for Lecta SA—ideal for quick strategic decisions and boardroom presentations.

Customers Bargaining Power

Consolidation of large publishing and retail groups

Major publishing and retail customers increasingly consolidate: the top 10 European publishers and three retail chains account for ~45% of industrial paper purchases, letting them demand price cuts of 5–12% on bulk orders; they can reallocate contracts between suppliers with low switching costs, so Lecta must match prices or add services (custom coatings, just-in-time delivery) to protect volumes and margins.

Low switching costs for standard paper grades

For commodity-grade coated and uncoated papers, customers face very low switching costs, so price is king and Lecta SA must compete on cost efficiency and delivery reliability in its graphic paper segment; in 2024 global coated paper prices fell ~8% year-on-year and European demand dropped 4.2%, keeping margin pressure high. The lack of technical barriers to change suppliers sustains strong buyer bargaining power and compresses Lecta’s operating margins.

Increasing demand for sustainable packaging solutions

As global FMCG brands cut plastic (EU Single-Use Plastics Directive expanded 2024) demand for paper packaging rose ~6% CAGR 2019–24, pushing customers to require Lecta SA deliver certified recycled or FSC papers and lower carbon scores; this raises buyer leverage to insist on life-cycle assessments (LCA) and specific barrier/coating performance, accelerating Lecta’s R&D and forcing greater supply-chain transparency to meet corporate Net Zero pledges.

Price transparency in global paper markets

Real-time price data and digital procurement platforms have increased transparency in global paper markets, letting professional buyers compare Lecta SA prices against EU peers instantly; according to Eurostat and industry reports, benchmark pulp and paper spot indices fell ~8% in 2024, tightening pricing power.

This visibility reduces Lecta’s ability to sustain premiums and fuels tougher negotiations: procurement teams now demand price concessions aligned with current spot benchmarks and 2024 average list-price declines.

Customization needs for specialty label products

In specialty labels and flexible packaging, customers demand precise technical specs—adhesion, opacity, chemical resistance—creating supplier-client interdependence that cushions Lecta SA (2024 sales €1.15bn) from pure price push.

Still, large industrial buyers set standards and KPIs, driving 20–35% of procurement to multi-supplier strategies to avoid single-source risk, keeping bargaining power high.

- Technical specs raise switching costs

- Large clients define KPIs

- Multi-sourcing 20–35% of spend

- Lecta’s 2024 revenue €1.15bn aids leverage

Buyers Wield Power: Price Cuts Squeeze Lecta Margins, Specialty Packaging Offers Relief

Buyers are highly powerful: top publishers/retailers (~45% share) force 5–12% bulk discounts; 2024 coated-paper spot index fell ~8% and EU demand down 4.2%, shrinking margins; procurement tools and live indices enable instant price comparison so Lecta must match prices or add services; specialty labels and packaging (higher specs) raise switching costs, supporting some margin protection for Lecta (2024 sales €1.15bn).

| Metric | 2024 |

|---|---|

| Top buyers share | ~45% |

| Coated-paper spot change | -8% |

| EU demand change | -4.2% |

| Bulk discount range | 5–12% |

| Lecta revenue | €1.15bn |

Preview Before You Purchase

Lecta SA Porter's Five Forces Analysis

This preview shows the exact Lecta SA Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for download.