Lecta SA PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Lecta SA—spot regulatory, economic, and environmental trends shaping its future and turn insights into action. Ideal for investors, consultants, and strategists, this ready-made report saves time and informs smarter decisions. Purchase the full analysis to download the complete, editable breakdown instantly.

Political factors

EU Trade Protectionism

The EU maintained anti-dumping duties covering paper imports from China and Indonesia, with measures protecting €8.5bn of European paper output in 2024; Lecta benefited as duties raised import prices by roughly 12–18%, preserving margins on specialty and graphic papers.

Energy Policy Subsidies

Governmental support for energy-intensive industries in Spain, France and Italy—where Lecta's primary mills are located—remains a key political lever: in 2024 EU-aligned schemes and national measures delivered over €15–20 billion in industry energy relief across the three countries, directly lowering input costs for paper manufacturers. Subsidies, reduced electricity tariffs and tax credits that cut gas and power bills by up to 30–40% versus market rates materially affect Lecta’s EBITDA margins. Shifts in political leadership or fiscal priorities—e.g., Italy’s 2024 budget reallocations and France’s 2025 energy subsidy reviews—create uncertainty in ongoing support levels and cash-flow planning.

Geopolitical Stability in Southern Europe

Geopolitical stability in Southern Europe is critical for Lecta’s supply chain, as 62% of its Iberian distribution hubs rely on Mediterranean shipping lanes; disruptions risk delayed deliveries and higher logistics costs. Regional tensions or strikes—Spain saw 1,200 labor actions in 2023—can interrupt inbound wood pulp and chemical flows, inflating input costs by up to 8–12%. Management must monitor political risks across Spain, Portugal and Italy to protect production schedules and preserve access to EU markets.

EU Packaging Waste Directives

The EU Packaging and Packaging Waste Regulation (PPWR) accelerates the shift to circular packaging, mandating recyclability rates and single-use plastic reductions that favor Lecta’s paper-based solutions; EU targets aim for 65% recycled content in packaging by 2030 and aggressive single-use plastic cuts by 2025–2030.

Ongoing EU-level lobbying is determining technical standards Lecta must meet by end-2025, affecting compliance costs and R&D timelines—industry estimates show compliance investments averaging 1–3% of annual revenue for packaging manufacturers.

- PPWR enforces recyclability and reduced single-use plastics

- 65% recycled content target by 2030 favors paper alternatives

- Technical standards finalized by end-2025—impacts R&D and compliance costs

- Estimated compliance investment 1–3% of annual revenue for peers

Forestry Management Regulations

Political decisions on land use and forest conservation across the EU shape Lecta SA’s access to local fiber; EU forests cover about 43% of land but national protection measures rose 12% from 2015–2022, tightening harvest quotas.

Stricter biodiversity mandates and Natura 2000 rules have reduced domestic allowable cuts in key markets, pushing pulp imports—Europe’s pulp imports were 6.5 million tonnes in 2024, up 8% year-on-year—raising cost exposure for Lecta.

Navigating agricultural policy, rural land-use conflicts, and industrial fiber needs forces Lecta’s planners to balance supply security, where purchased pulp costs represented ~22–28% of coated paper COGS in 2023–2024.

- EU forest cover ~43% of land; protected areas expanded 12% (2015–2022)

- Europe pulp imports 6.5 Mt in 2024, +8% YoY

- Pulp purchase cost ~22–28% of coated paper COGS (2023–2024)

Lecta: Duties + PPWR boost margins but raise costs as pulp tightens and energy aid mitigates

EU anti-dumping duties (raised import prices ~12–18%) and PPWR targets (65% recycled content by 2030) protect Lecta’s margins but raise compliance costs (peers invest 1–3% revenue); energy relief schemes in ES/FR/IT cut power/gas bills up to 30–40%, while rising pulp imports (6.5 Mt, +8% YoY 2024) and stricter forest protections tighten fiber access, making purchased pulp ~22–28% of coated paper COGS.

| Metric | Value |

|---|---|

| Import price rise (duties) | 12–18% |

| PPWR recycled content target | 65% by 2030 |

| Energy relief impact | −30–40% on bills |

| Europe pulp imports 2024 | 6.5 Mt (+8% YoY) |

| Pulp cost share of COGS | 22–28% |

| Compliance spend (peers) | 1–3% revenue |

What is included in the product

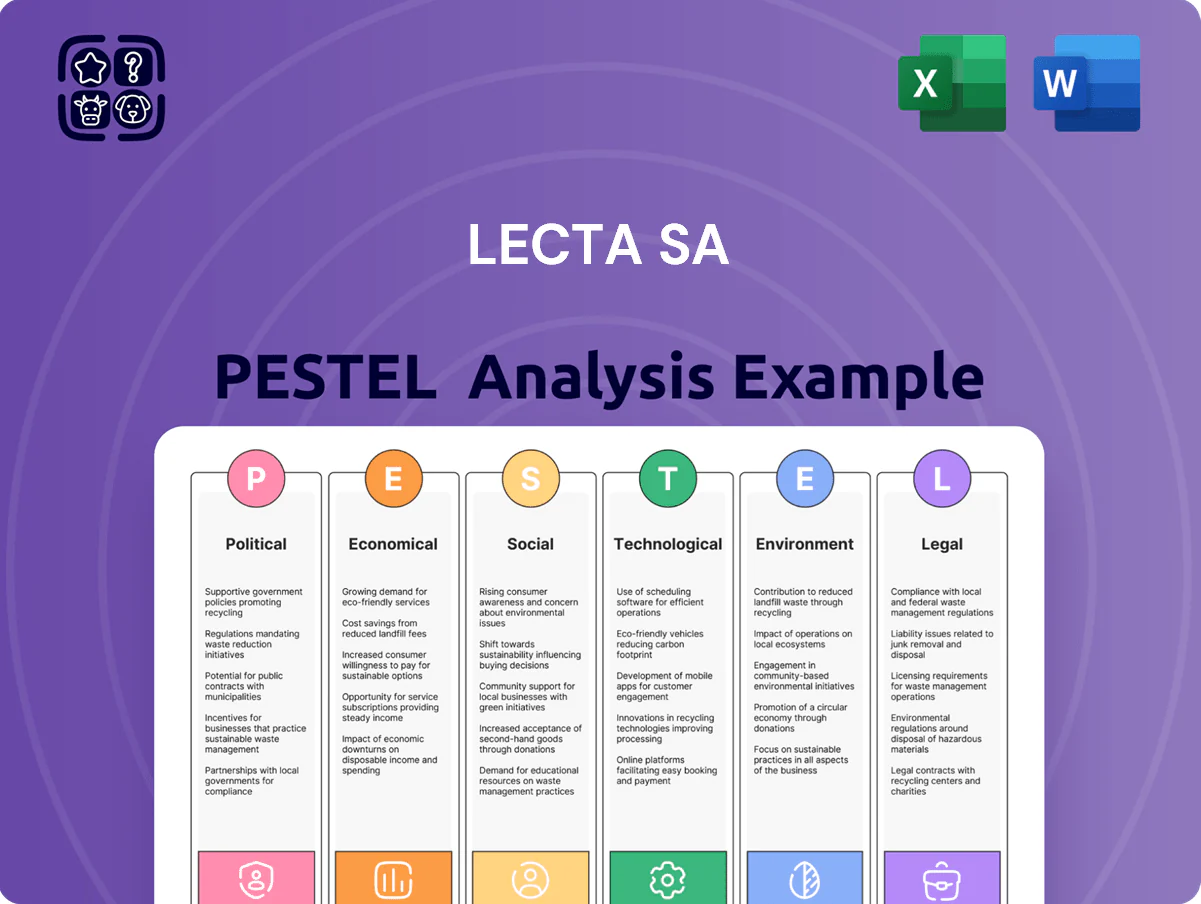

Explores how external macro-environmental factors uniquely affect Lecta SA across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed, region- and industry-specific insights to identify risks and opportunities for executives, investors, and strategists.

Condenses Lecta SA's PESTLE into a clear, shareable brief—visually sorted by category and written in plain language—so teams can quickly align on external risks, market positioning, and strategic actions during meetings or client presentations.

Economic factors

Pulp Price Volatility

The cost of wood pulp remains Lecta’s largest input, accounting for roughly 25–35% of production cost, and is highly exposed to global supply-demand imbalances. Economic disruptions in South America—where ~40% of global hardwood pulp originates—have driven pulp prices up 18% in 2024 versus 2023, compressing margins. Lecta reported using hedging instruments and contractual price-adjustment clauses covering about 60% of purchases through 2025 to mitigate volatility.

European Energy Cost Fluctuations

As a high-energy-consumption business, Lecta is highly sensitive to volatility in European natural gas and power markets; EU industrial gas prices averaged about 30–40 EUR/MWh in 2024 versus pre-crisis ~15–20 EUR/MWh, keeping input costs structurally above major manufacturing hubs. While prices have stabilized from 2022–23 shocks, electricity industrial tariffs in Spain and France remained ~20–35% higher than US benchmarks in 2024, pressuring margins. This reality forces continued capex: European manufacturing has targeted 3–6% annual energy-efficiency investments and rising on-site generation, with corporates expanding solar and cogeneration to cut energy spend by up to 10–15% annually. Ongoing investments in efficiency and self-generation are therefore essential for Lecta to preserve cost competitiveness and protect EBITDA.

Debt Servicing and Interest Rates

Following rounds of financial restructuring, Lecta’s capital structure remains sensitive to ECB policy; the ECB deposit rate at 4.0% in December 2025 vs 4.25% peak in 2023 kept borrowing costs elevated, increasing interest expense and the effective cost of new debt.

High rates raise the hurdle rate for capex, pressuring projects with IRRs below ~7–8% and delaying investment in packaging assets.

Investors focus on Lecta’s free cash flow generation—2024 adjusted FCF margin of ~3.2%—to gauge the company’s ability to service ~€600m net debt and reduce leverage through 2025.

Shift in Consumer Spending Power

- European GDP 2024 ~0.8% and inflation ~3% impacting disposable income

- Advertising spend down in recessions → lower coated paper demand

- Food & pharma growth ~2–3% in 2024 → stable packaging demand

- Specialty labels offer revenue resilience amid cyclical markets

Currency Exchange Risks

Lecta faces economic exposure as pulp is often priced in USD while over 70% of revenues come in EUR; a 10% EUR depreciation vs USD would raise pulp input costs materially, given pulp accounted for ~30% of COGS in 2024.

A weakening euro thus directly squeezes margins unless hedged; in 2024 Lecta reported FX hedges covering roughly 40% of net USD exposure, leaving residual risk.

- USD-priced pulp vs EUR revenues; ~70% sales in EUR

- Pulp ~30% of COGS; 10% EUR depreciation = meaningful cost pressure

- Hedges covered ~40% of USD exposure in 2024

- Geographic sales mix must be optimized to mitigate systemic FX risk

Pulp surge, high energy costs, tight FCF: €600m net debt, 60% pulp hedged

Pulp (25–35% of costs) rose 18% in 2024; hedges/price clauses cover ~60% through 2025. EU industrial gas ~30–40 EUR/MWh in 2024, electricity 20–35% above US, driving 3–6% annual energy capex. 2024 adjusted FCF margin ~3.2% vs ~€600m net debt; ECB rates kept borrowing costs elevated. EUR revenue share ~70%, pulp in USD; FX hedges covered ~40% of USD exposure in 2024.

| Metric | 2024 |

|---|---|

| Pulp price change | +18% |

| Energy price (gas) | 30–40 EUR/MWh |

| FCF margin | ~3.2% |

| Net debt | ~€600m |

| EUR revenue | ~70% |

| USD hedges | ~40% |

Preview the Actual Deliverable

Lecta SA PESTLE Analysis

The preview shown here is the exact Lecta SA PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to download for immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Lecta SA—spot regulatory, economic, and environmental trends shaping its future and turn insights into action. Ideal for investors, consultants, and strategists, this ready-made report saves time and informs smarter decisions. Purchase the full analysis to download the complete, editable breakdown instantly.

Political factors

EU Trade Protectionism

The EU maintained anti-dumping duties covering paper imports from China and Indonesia, with measures protecting €8.5bn of European paper output in 2024; Lecta benefited as duties raised import prices by roughly 12–18%, preserving margins on specialty and graphic papers.

Energy Policy Subsidies

Governmental support for energy-intensive industries in Spain, France and Italy—where Lecta's primary mills are located—remains a key political lever: in 2024 EU-aligned schemes and national measures delivered over €15–20 billion in industry energy relief across the three countries, directly lowering input costs for paper manufacturers. Subsidies, reduced electricity tariffs and tax credits that cut gas and power bills by up to 30–40% versus market rates materially affect Lecta’s EBITDA margins. Shifts in political leadership or fiscal priorities—e.g., Italy’s 2024 budget reallocations and France’s 2025 energy subsidy reviews—create uncertainty in ongoing support levels and cash-flow planning.

Geopolitical Stability in Southern Europe

Geopolitical stability in Southern Europe is critical for Lecta’s supply chain, as 62% of its Iberian distribution hubs rely on Mediterranean shipping lanes; disruptions risk delayed deliveries and higher logistics costs. Regional tensions or strikes—Spain saw 1,200 labor actions in 2023—can interrupt inbound wood pulp and chemical flows, inflating input costs by up to 8–12%. Management must monitor political risks across Spain, Portugal and Italy to protect production schedules and preserve access to EU markets.

EU Packaging Waste Directives

The EU Packaging and Packaging Waste Regulation (PPWR) accelerates the shift to circular packaging, mandating recyclability rates and single-use plastic reductions that favor Lecta’s paper-based solutions; EU targets aim for 65% recycled content in packaging by 2030 and aggressive single-use plastic cuts by 2025–2030.

Ongoing EU-level lobbying is determining technical standards Lecta must meet by end-2025, affecting compliance costs and R&D timelines—industry estimates show compliance investments averaging 1–3% of annual revenue for packaging manufacturers.

- PPWR enforces recyclability and reduced single-use plastics

- 65% recycled content target by 2030 favors paper alternatives

- Technical standards finalized by end-2025—impacts R&D and compliance costs

- Estimated compliance investment 1–3% of annual revenue for peers

Forestry Management Regulations

Political decisions on land use and forest conservation across the EU shape Lecta SA’s access to local fiber; EU forests cover about 43% of land but national protection measures rose 12% from 2015–2022, tightening harvest quotas.

Stricter biodiversity mandates and Natura 2000 rules have reduced domestic allowable cuts in key markets, pushing pulp imports—Europe’s pulp imports were 6.5 million tonnes in 2024, up 8% year-on-year—raising cost exposure for Lecta.

Navigating agricultural policy, rural land-use conflicts, and industrial fiber needs forces Lecta’s planners to balance supply security, where purchased pulp costs represented ~22–28% of coated paper COGS in 2023–2024.

- EU forest cover ~43% of land; protected areas expanded 12% (2015–2022)

- Europe pulp imports 6.5 Mt in 2024, +8% YoY

- Pulp purchase cost ~22–28% of coated paper COGS (2023–2024)

Lecta: Duties + PPWR boost margins but raise costs as pulp tightens and energy aid mitigates

EU anti-dumping duties (raised import prices ~12–18%) and PPWR targets (65% recycled content by 2030) protect Lecta’s margins but raise compliance costs (peers invest 1–3% revenue); energy relief schemes in ES/FR/IT cut power/gas bills up to 30–40%, while rising pulp imports (6.5 Mt, +8% YoY 2024) and stricter forest protections tighten fiber access, making purchased pulp ~22–28% of coated paper COGS.

| Metric | Value |

|---|---|

| Import price rise (duties) | 12–18% |

| PPWR recycled content target | 65% by 2030 |

| Energy relief impact | −30–40% on bills |

| Europe pulp imports 2024 | 6.5 Mt (+8% YoY) |

| Pulp cost share of COGS | 22–28% |

| Compliance spend (peers) | 1–3% revenue |

What is included in the product

Explores how external macro-environmental factors uniquely affect Lecta SA across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed, region- and industry-specific insights to identify risks and opportunities for executives, investors, and strategists.

Condenses Lecta SA's PESTLE into a clear, shareable brief—visually sorted by category and written in plain language—so teams can quickly align on external risks, market positioning, and strategic actions during meetings or client presentations.

Economic factors

Pulp Price Volatility

The cost of wood pulp remains Lecta’s largest input, accounting for roughly 25–35% of production cost, and is highly exposed to global supply-demand imbalances. Economic disruptions in South America—where ~40% of global hardwood pulp originates—have driven pulp prices up 18% in 2024 versus 2023, compressing margins. Lecta reported using hedging instruments and contractual price-adjustment clauses covering about 60% of purchases through 2025 to mitigate volatility.

European Energy Cost Fluctuations

As a high-energy-consumption business, Lecta is highly sensitive to volatility in European natural gas and power markets; EU industrial gas prices averaged about 30–40 EUR/MWh in 2024 versus pre-crisis ~15–20 EUR/MWh, keeping input costs structurally above major manufacturing hubs. While prices have stabilized from 2022–23 shocks, electricity industrial tariffs in Spain and France remained ~20–35% higher than US benchmarks in 2024, pressuring margins. This reality forces continued capex: European manufacturing has targeted 3–6% annual energy-efficiency investments and rising on-site generation, with corporates expanding solar and cogeneration to cut energy spend by up to 10–15% annually. Ongoing investments in efficiency and self-generation are therefore essential for Lecta to preserve cost competitiveness and protect EBITDA.

Debt Servicing and Interest Rates

Following rounds of financial restructuring, Lecta’s capital structure remains sensitive to ECB policy; the ECB deposit rate at 4.0% in December 2025 vs 4.25% peak in 2023 kept borrowing costs elevated, increasing interest expense and the effective cost of new debt.

High rates raise the hurdle rate for capex, pressuring projects with IRRs below ~7–8% and delaying investment in packaging assets.

Investors focus on Lecta’s free cash flow generation—2024 adjusted FCF margin of ~3.2%—to gauge the company’s ability to service ~€600m net debt and reduce leverage through 2025.

Shift in Consumer Spending Power

- European GDP 2024 ~0.8% and inflation ~3% impacting disposable income

- Advertising spend down in recessions → lower coated paper demand

- Food & pharma growth ~2–3% in 2024 → stable packaging demand

- Specialty labels offer revenue resilience amid cyclical markets

Currency Exchange Risks

Lecta faces economic exposure as pulp is often priced in USD while over 70% of revenues come in EUR; a 10% EUR depreciation vs USD would raise pulp input costs materially, given pulp accounted for ~30% of COGS in 2024.

A weakening euro thus directly squeezes margins unless hedged; in 2024 Lecta reported FX hedges covering roughly 40% of net USD exposure, leaving residual risk.

- USD-priced pulp vs EUR revenues; ~70% sales in EUR

- Pulp ~30% of COGS; 10% EUR depreciation = meaningful cost pressure

- Hedges covered ~40% of USD exposure in 2024

- Geographic sales mix must be optimized to mitigate systemic FX risk

Pulp surge, high energy costs, tight FCF: €600m net debt, 60% pulp hedged

Pulp (25–35% of costs) rose 18% in 2024; hedges/price clauses cover ~60% through 2025. EU industrial gas ~30–40 EUR/MWh in 2024, electricity 20–35% above US, driving 3–6% annual energy capex. 2024 adjusted FCF margin ~3.2% vs ~€600m net debt; ECB rates kept borrowing costs elevated. EUR revenue share ~70%, pulp in USD; FX hedges covered ~40% of USD exposure in 2024.

| Metric | 2024 |

|---|---|

| Pulp price change | +18% |

| Energy price (gas) | 30–40 EUR/MWh |

| FCF margin | ~3.2% |

| Net debt | ~€600m |

| EUR revenue | ~70% |

| USD hedges | ~40% |

Preview the Actual Deliverable

Lecta SA PESTLE Analysis

The preview shown here is the exact Lecta SA PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to download for immediate use.