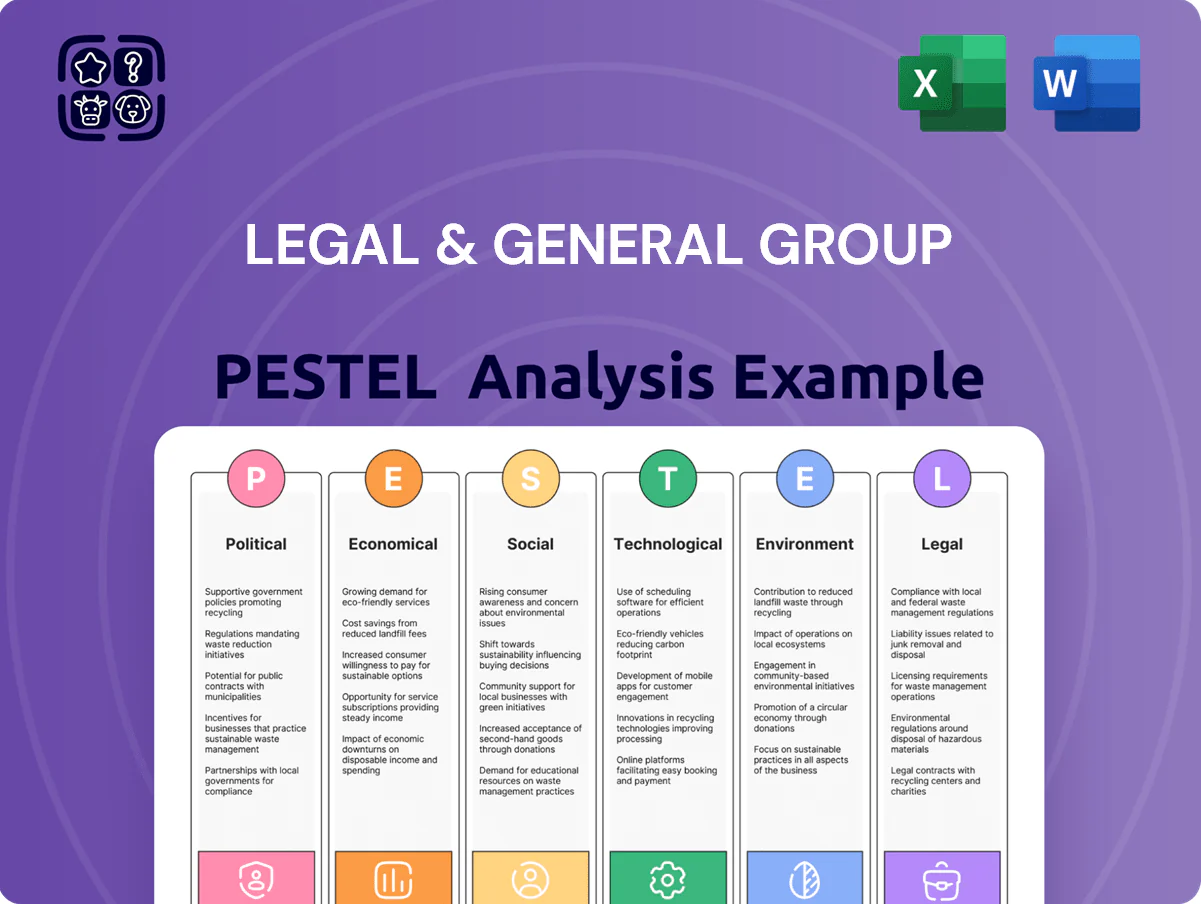

Legal & General Group PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of Legal & General Group—concise insights on political, economic, social, technological, legal, and environmental forces shaping its future; ideal for investors and strategists. Purchase the full report for actionable intelligence, editable charts, and scenario-ready recommendations to strengthen your investment thesis or corporate strategy.

Political factors

Post-Election Fiscal Policy Stability

Post-election fiscal policy through late 2025 emphasizes 50+ billion pounds in long-term infrastructure funding and targeted pension reforms aiming to boost private capital deployment; Legal & General stands to gain as a major institutional allocator supporting UK renewal projects.

Pension Review and Mansion House Reforms

Ongoing political pressure to consolidate pension schemes and increase investment in UK high-growth firms—exemplified by the 2024 Mansion House reforms targeting £1.5tn in DC assets—reshapes Legal & General Group’s strategic direction.

The government’s push for scale in the DC market directly affects L&G’s asset management and workplace savings divisions, which managed c.£1.2tn AUMA in 2025, increasing demand for pooled solutions.

Navigating these regulatory-driven shifts is essential for L&G to maintain UK market leadership amid policy aims to boost pension investments into domestic growth sectors by tens of billions annually.

Geopolitical Volatility and Global Trade

With sizable US operations and growing Asian exposure, Legal & General remains vulnerable to shifting trade alliances; US-UK trade tensions and US-China tariffs contributed to global trade volatility, impacting asset returns—LGIM reported 2024 net inflows of £35bn, exposing balance-sheet sensitivity to cross-border flows.

Political instability in markets like Hong Kong and parts of Southeast Asia has driven currency swings; 2023-24 FX volatility rose ~18%, increasing risk premiums on international fixed income and equities held by the group.

Legal & General employs strategic hedging and geographic diversification—LGIM’s multi-asset strategies use currency hedges and regional allocation limits, reducing portfolio tracking error and lowering political tail-risk exposure.

Social Housing and Urban Regeneration Policy

The group’s ~£82bn UK property portfolio and significant affordable housing pipeline are highly sensitive to local and national planning policies; a shift in housing targets or new rent controls could lower asset valuations and expected yields on long-duration investments.

Political prioritisation of social housing influences development approval timelines and funding; Legal & General’s strategy emphasizes maintaining close coordination with councils to protect returns and de-risk projects.

- £82bn UK property exposure (2024)

- Affordable housing pipeline growth linked to planning regimes

- Rent control or target changes → lower yields/valuations

- Strong local authority relationships critical for de-risking

International Regulatory Alignment

As a global financial group, Legal & General must navigate evolving international standards and cross-border data flow rules affecting its £1.2tn AUM and operations in 10+ jurisdictions, with compliance costs rising amid regulatory fragmentation.

Divergence between UK and EU financial rules—post-Brexit equivalence gaps and differing ESG disclosure regimes—requires continuous monitoring to safeguard efficiency across its insurance, pensions and asset management units.

Political moves on a global minimum tax (Pillar Two) and related corporate tax shifts influence Legal & General’s international structure and effective tax rate, impacting cross-border capital allocation and client solutions.

- £1.2tn AUM across 10+ jurisdictions

- Rising compliance costs from regulatory fragmentation

- Brexit-driven UK/EU divergence affects ESG and equivalence

- Pillar Two global tax minimums reshape tax planning

Policy Shock: Infrastructure, DC Reform & Tax Shift Rewire Legal & General’s Capital Risk

Political drivers—post-2024 infrastructure spending (£50bn+), Mansion House DC reforms targeting £1.5tn, Pillar Two tax, and UK/EU regulatory divergence—reshape Legal & General’s capital allocation, compliance costs and UK property/housing risk; group metrics: £1.2tn AUM (2025), £82bn UK property (2024), LGIM net inflows £35bn (2024), FX volatility +18% (2023–24).

| Metric | Value |

|---|---|

| AUM (2025) | £1.2tn |

| UK property (2024) | £82bn |

| LGIM net inflows (2024) | £35bn |

| Post-2024 infra funding | £50bn+ |

| DC reform target | £1.5tn |

| FX vol change (2023–24) | +18% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Legal & General Group, with data-backed trends and industry-specific examples to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary of Legal & General that can be dropped into presentations or shared across teams to quickly align on regulatory, economic, social, technological, environmental, and legal risks and opportunities.

Economic factors

Interest Rate Environment and Yield Curves

By end-2025, Bank of England base rate stabilization near 5.25% materially eased annuity pricing pressure for Legal & General, allowing quoted pricing increases and improving new business margins; higher sustained rates lifted investment yields on the group’s £300bn+ balance sheet. Active management of the gilt portfolio remains essential as duration mismatches can erode capital; L&G reported a solvency II ratio ~220% in 2024, sensitive to curve shifts. The yield curve shape—recently flatter between 2-10y—directly impacts L&G’s liability discounting and profitability, with steeper long-end supporting reserve reductions and margin expansion.

Inflationary Pressures on Operational Costs

While UK CPI eased to 3.9% in Dec 2025 from a 2022 peak, residual wage growth near 5% and service inflation at 4.2% continue to pressure Legal & General’s operational margins.

The group must balance competitive insurance pricing against rising claims and administration costs—UK household insurance claims rose ~7% YoY in 2024, increasing payout strain.

Managing the internal cost base via efficiency programmes is critical: L&G reported a £120m cost saving target for 2024–25 to offset input inflation and protect margins.

Global Equity Market Performance

The performance of Legal & General Investment Management is closely tied to global equity markets; a 10% fall in major indices could cut fee revenue materially given L&G IM's £1.2tn AUM (2025 Q4). Fluctuations in valuations drive management fees and AUM, with equities comprising a significant share of net inflows. US and Euro area GDP growth—0.8% q/q US (2025 Q4 annualised) and 0.4% q/q Eurozone—remain primary drivers of investor sentiment and capital flows.

Real Estate Market Valuations

As a major institutional landlord, Legal & General Group is exposed to commercial and residential valuation shifts, with UK investment property value down about 10% in 2023 versus 2022 and prime office yields widening to ~5.5% by mid-2024, affecting rental income and asset-backed returns.

The move to hybrid work and online retail reduced central London office and high-street footfall, prompting LGIM and L&G to increase allocations to life sciences and logistics, where vacancy in UK logistics fell to ~3.1% in 2024 and rents rose ~6% YoY.

Strategic pivots mitigate valuation risk: by end-2024 LGIM Real Assets reported >10% allocation to life sciences/logistics, improving portfolio resilience amid cap rate pressure and securing higher income growth versus traditional office assets.

- UK investment property values ≈ -10% (2023 v 2022)

- Prime office yields ~5.5% mid-2024

- UK logistics vacancy ~3.1% (2024); rents +6% YoY

- LGIM Real Assets >10% in life sciences/logistics by end-2024

Currency Exchange Rate Fluctuations

Legal & General Group's US exposure means GBP/USD swings drive translation risk; in 2025, with GBP at ~1.27 vs USD, a 5% move alters reported US-dollar income materially, as prior years showed FX translation variances exceeding £200m.

Currency shifts affect solvency ratios and capital allocation; treasury hedging reduced net translation volatility by ~60% in 2024, but continued UK-US economic divergence keeps FX management central to earnings stability.

- US earnings exposed to GBP/USD; 2025 rate ~1.27

- 5% FX move can change reported results by ~£200m+

- 2024 hedging cut translation volatility ~60%

- UK vs US economic divergence remains key treasury risk

Higher rates lift L&G yields and annuities; gilt duration and property drag solvency

Higher base rates (~5.25% end‑2025) boosted annuity pricing and investment yields across L&G’s £300bn+ balance sheet; gilt duration risk keeps solvency (~220% in 2024) sensitive. Property values down ~10% (2023 v 2022) and prime office yields ~5.5% weigh on returns, while LGIM AUM £1.2tn (Q4 2025) ties fee income to equity markets; GBP/USD ~1.27 in 2025 creates notable translation risk.

| Metric | Value |

|---|---|

| Base rate | ~5.25% (end‑2025) |

| Solvency II | ~220% (2024) |

| AUM | £1.2tn (Q4 2025) |

| Property value change | -10% (2023 v 2022) |

| GBP/USD | ~1.27 (2025) |

What You See Is What You Get

Legal & General Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains the complete PESTLE analysis for Legal & General Group with professional structure and actionable insights. This is a real screenshot of the product you’re buying—delivered exactly as shown, no surprises, and immediately downloadable after payment. What you’re previewing here is the actual file—no placeholders or teasers—fully edited and ready for use in reports, presentations, or strategic planning.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of Legal & General Group—concise insights on political, economic, social, technological, legal, and environmental forces shaping its future; ideal for investors and strategists. Purchase the full report for actionable intelligence, editable charts, and scenario-ready recommendations to strengthen your investment thesis or corporate strategy.

Political factors

Post-Election Fiscal Policy Stability

Post-election fiscal policy through late 2025 emphasizes 50+ billion pounds in long-term infrastructure funding and targeted pension reforms aiming to boost private capital deployment; Legal & General stands to gain as a major institutional allocator supporting UK renewal projects.

Pension Review and Mansion House Reforms

Ongoing political pressure to consolidate pension schemes and increase investment in UK high-growth firms—exemplified by the 2024 Mansion House reforms targeting £1.5tn in DC assets—reshapes Legal & General Group’s strategic direction.

The government’s push for scale in the DC market directly affects L&G’s asset management and workplace savings divisions, which managed c.£1.2tn AUMA in 2025, increasing demand for pooled solutions.

Navigating these regulatory-driven shifts is essential for L&G to maintain UK market leadership amid policy aims to boost pension investments into domestic growth sectors by tens of billions annually.

Geopolitical Volatility and Global Trade

With sizable US operations and growing Asian exposure, Legal & General remains vulnerable to shifting trade alliances; US-UK trade tensions and US-China tariffs contributed to global trade volatility, impacting asset returns—LGIM reported 2024 net inflows of £35bn, exposing balance-sheet sensitivity to cross-border flows.

Political instability in markets like Hong Kong and parts of Southeast Asia has driven currency swings; 2023-24 FX volatility rose ~18%, increasing risk premiums on international fixed income and equities held by the group.

Legal & General employs strategic hedging and geographic diversification—LGIM’s multi-asset strategies use currency hedges and regional allocation limits, reducing portfolio tracking error and lowering political tail-risk exposure.

Social Housing and Urban Regeneration Policy

The group’s ~£82bn UK property portfolio and significant affordable housing pipeline are highly sensitive to local and national planning policies; a shift in housing targets or new rent controls could lower asset valuations and expected yields on long-duration investments.

Political prioritisation of social housing influences development approval timelines and funding; Legal & General’s strategy emphasizes maintaining close coordination with councils to protect returns and de-risk projects.

- £82bn UK property exposure (2024)

- Affordable housing pipeline growth linked to planning regimes

- Rent control or target changes → lower yields/valuations

- Strong local authority relationships critical for de-risking

International Regulatory Alignment

As a global financial group, Legal & General must navigate evolving international standards and cross-border data flow rules affecting its £1.2tn AUM and operations in 10+ jurisdictions, with compliance costs rising amid regulatory fragmentation.

Divergence between UK and EU financial rules—post-Brexit equivalence gaps and differing ESG disclosure regimes—requires continuous monitoring to safeguard efficiency across its insurance, pensions and asset management units.

Political moves on a global minimum tax (Pillar Two) and related corporate tax shifts influence Legal & General’s international structure and effective tax rate, impacting cross-border capital allocation and client solutions.

- £1.2tn AUM across 10+ jurisdictions

- Rising compliance costs from regulatory fragmentation

- Brexit-driven UK/EU divergence affects ESG and equivalence

- Pillar Two global tax minimums reshape tax planning

Policy Shock: Infrastructure, DC Reform & Tax Shift Rewire Legal & General’s Capital Risk

Political drivers—post-2024 infrastructure spending (£50bn+), Mansion House DC reforms targeting £1.5tn, Pillar Two tax, and UK/EU regulatory divergence—reshape Legal & General’s capital allocation, compliance costs and UK property/housing risk; group metrics: £1.2tn AUM (2025), £82bn UK property (2024), LGIM net inflows £35bn (2024), FX volatility +18% (2023–24).

| Metric | Value |

|---|---|

| AUM (2025) | £1.2tn |

| UK property (2024) | £82bn |

| LGIM net inflows (2024) | £35bn |

| Post-2024 infra funding | £50bn+ |

| DC reform target | £1.5tn |

| FX vol change (2023–24) | +18% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Legal & General Group, with data-backed trends and industry-specific examples to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary of Legal & General that can be dropped into presentations or shared across teams to quickly align on regulatory, economic, social, technological, environmental, and legal risks and opportunities.

Economic factors

Interest Rate Environment and Yield Curves

By end-2025, Bank of England base rate stabilization near 5.25% materially eased annuity pricing pressure for Legal & General, allowing quoted pricing increases and improving new business margins; higher sustained rates lifted investment yields on the group’s £300bn+ balance sheet. Active management of the gilt portfolio remains essential as duration mismatches can erode capital; L&G reported a solvency II ratio ~220% in 2024, sensitive to curve shifts. The yield curve shape—recently flatter between 2-10y—directly impacts L&G’s liability discounting and profitability, with steeper long-end supporting reserve reductions and margin expansion.

Inflationary Pressures on Operational Costs

While UK CPI eased to 3.9% in Dec 2025 from a 2022 peak, residual wage growth near 5% and service inflation at 4.2% continue to pressure Legal & General’s operational margins.

The group must balance competitive insurance pricing against rising claims and administration costs—UK household insurance claims rose ~7% YoY in 2024, increasing payout strain.

Managing the internal cost base via efficiency programmes is critical: L&G reported a £120m cost saving target for 2024–25 to offset input inflation and protect margins.

Global Equity Market Performance

The performance of Legal & General Investment Management is closely tied to global equity markets; a 10% fall in major indices could cut fee revenue materially given L&G IM's £1.2tn AUM (2025 Q4). Fluctuations in valuations drive management fees and AUM, with equities comprising a significant share of net inflows. US and Euro area GDP growth—0.8% q/q US (2025 Q4 annualised) and 0.4% q/q Eurozone—remain primary drivers of investor sentiment and capital flows.

Real Estate Market Valuations

As a major institutional landlord, Legal & General Group is exposed to commercial and residential valuation shifts, with UK investment property value down about 10% in 2023 versus 2022 and prime office yields widening to ~5.5% by mid-2024, affecting rental income and asset-backed returns.

The move to hybrid work and online retail reduced central London office and high-street footfall, prompting LGIM and L&G to increase allocations to life sciences and logistics, where vacancy in UK logistics fell to ~3.1% in 2024 and rents rose ~6% YoY.

Strategic pivots mitigate valuation risk: by end-2024 LGIM Real Assets reported >10% allocation to life sciences/logistics, improving portfolio resilience amid cap rate pressure and securing higher income growth versus traditional office assets.

- UK investment property values ≈ -10% (2023 v 2022)

- Prime office yields ~5.5% mid-2024

- UK logistics vacancy ~3.1% (2024); rents +6% YoY

- LGIM Real Assets >10% in life sciences/logistics by end-2024

Currency Exchange Rate Fluctuations

Legal & General Group's US exposure means GBP/USD swings drive translation risk; in 2025, with GBP at ~1.27 vs USD, a 5% move alters reported US-dollar income materially, as prior years showed FX translation variances exceeding £200m.

Currency shifts affect solvency ratios and capital allocation; treasury hedging reduced net translation volatility by ~60% in 2024, but continued UK-US economic divergence keeps FX management central to earnings stability.

- US earnings exposed to GBP/USD; 2025 rate ~1.27

- 5% FX move can change reported results by ~£200m+

- 2024 hedging cut translation volatility ~60%

- UK vs US economic divergence remains key treasury risk

Higher rates lift L&G yields and annuities; gilt duration and property drag solvency

Higher base rates (~5.25% end‑2025) boosted annuity pricing and investment yields across L&G’s £300bn+ balance sheet; gilt duration risk keeps solvency (~220% in 2024) sensitive. Property values down ~10% (2023 v 2022) and prime office yields ~5.5% weigh on returns, while LGIM AUM £1.2tn (Q4 2025) ties fee income to equity markets; GBP/USD ~1.27 in 2025 creates notable translation risk.

| Metric | Value |

|---|---|

| Base rate | ~5.25% (end‑2025) |

| Solvency II | ~220% (2024) |

| AUM | £1.2tn (Q4 2025) |

| Property value change | -10% (2023 v 2022) |

| GBP/USD | ~1.27 (2025) |

What You See Is What You Get

Legal & General Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains the complete PESTLE analysis for Legal & General Group with professional structure and actionable insights. This is a real screenshot of the product you’re buying—delivered exactly as shown, no surprises, and immediately downloadable after payment. What you’re previewing here is the actual file—no placeholders or teasers—fully edited and ready for use in reports, presentations, or strategic planning.