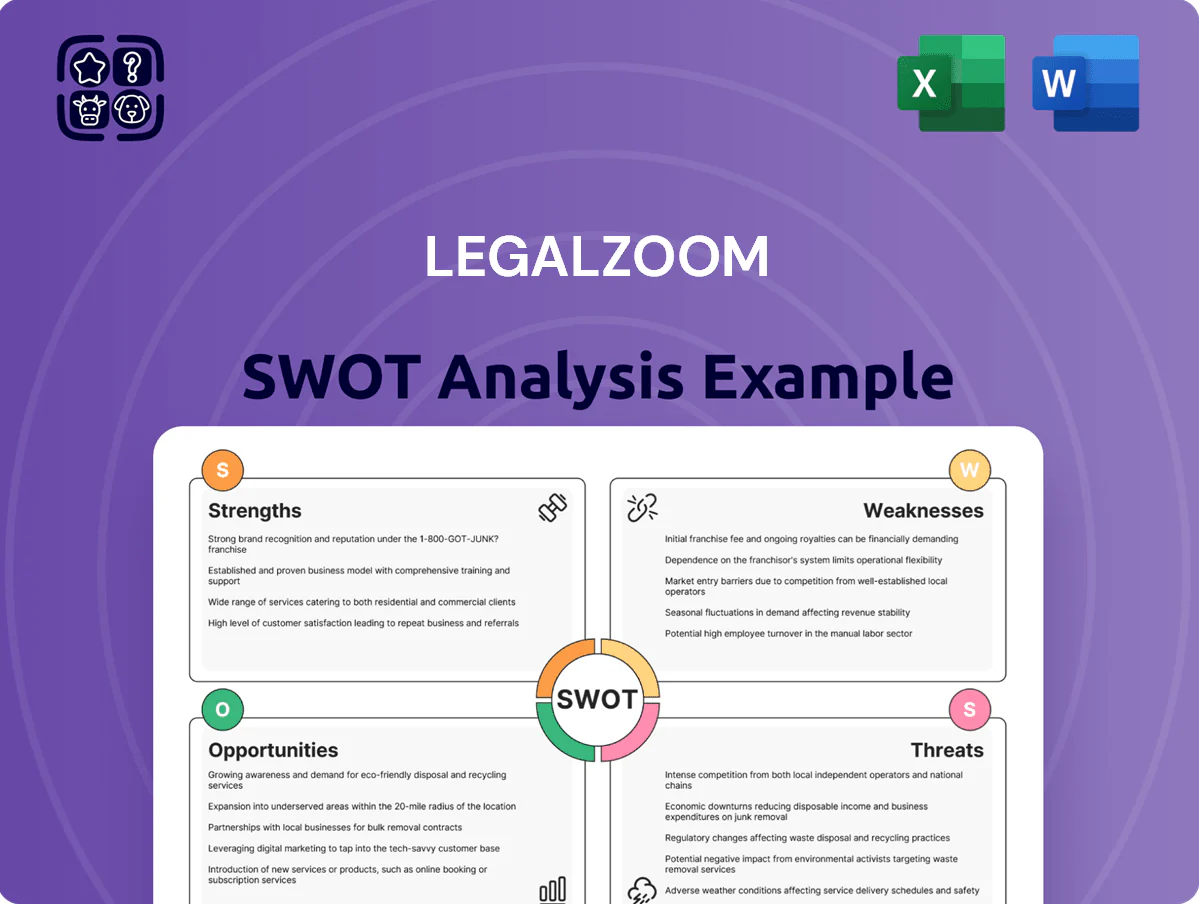

LegalZoom SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

LegalZoom’s SWOT highlights a strong brand and scalable digital platform but flags competition, regulatory nuances, and margin pressures; our full analysis unpacks these drivers with financial context and strategic implications. Discover actionable recommendations, editable tools, and investor-ready visuals—purchase the complete SWOT to plan, pitch, or invest with confidence.

Strengths

Dominant Brand Recognition

LegalZoom is the most recognized online legal services brand for small businesses and entrepreneurs, with brand awareness cited at ~70% among US small-business owners in 2024 surveys, lowering trust friction for services like incorporation and trademarking.

Diversified Subscription Revenue

Extensive Attorney Network

By 2024 LegalZoom maintained a vetted network of thousands of independent attorneys across all 50 US states and key international markets, letting it pair automated documents with live counsel and closing the advice gap for users.

The hybrid model delivers consultations at a fraction of traditional firm costs—typical session fees under the service average 40–60% below small‑firm rates—boosting conversion and retention.

This attorney network forms a durable moat: purely software providers struggle to match LegalZoom’s regulatory footprint and partner depth at scale.

Comprehensive Small Business Ecosystem

LegalZoom expanded from filings to tax prep, bookkeeping, and IP protection, creating a comprehensive small-business ecosystem that served over 4 million customers by end-2024.

This one-stop approach boosts lifetime value and cross-sell: services attach rates rose to ~28% in 2024, lowering churn vs niche providers.

Integrated services increase stickiness and reduce customer acquisition cost by enabling repeat renewals and bundled pricing.

- 4M+ customers (2024)

- 28% attach rate (2024)

- Lower CAC via bundles

Scalable Technology Infrastructure

- High-throughput automation: ~95% accuracy

- Strong margins: ~60% on standard products (2024)

- Repeat buyers: >30% retention

- Support load down ~20% YoY

LegalZoom: Market‑leading SMB legal platform — 4M+ customers, 45% subscription, 72% retention

LegalZoom is the leading online legal brand with ~70% awareness among US small-business owners (2024), 4M+ customers, a subscription shift to ~45% of revenue and 72% annual subscriber retention, ~28% attach rate, ~60% gross margins on standardized products, and ~95% document automation accuracy—driving high LTV and lower CAC.

| Metric | 2024 |

|---|---|

| Brand awareness | ~70% |

| Customers | 4M+ |

| Subscription revenue | ~45% |

| Subscriber retention | 72% |

| Attach rate | 28% |

| Gross margin (standard) | ~60% |

| Automation accuracy | ~95% |

What is included in the product

Provides a concise SWOT analysis of LegalZoom, highlighting its core strengths and weaknesses while mapping external opportunities and threats that shape its competitive and strategic outlook.

Delivers a clear SWOT snapshot tailored to LegalZoom, enabling fast strategic alignment and concise stakeholder briefings.

Weaknesses

High Customer Acquisition Costs

LegalZoom spends heavily on digital ads—search and social—to drive new business formations, with marketing costs per new customer estimated at roughly $150–$220 in 2024 per company disclosures and industry tracker estimates.

As ad auctions tighten, higher cost-per-clicks can push customer acquisition cost (CAC) above lifetime value margins and erode net margins (LegalZoom reported 2024 adjusted EBITDA loss pressure tied to sales & marketing increases).

Relying on external traffic makes revenue sensitive to platform algorithm shifts or sudden ad price spikes, increasing forecast volatility and forcing higher spend to sustain growth.

Sensitivity to Macroeconomic Cycles

A large share of LegalZoom’s revenue comes from new business filings, which fell during the 2022–2023 U.S. slowdown—new business applications declined about 6% in 2023 vs. 2021 peak, per Census data—showing sensitivity to macro cycles.

Higher interest rates and tighter VC funding since 2022 reduced startup formation, cutting demand for formation and financing-related legal services, increasing quarter-to-quarter revenue volatility for LegalZoom.

Regulatory and Compliance Burdens

Operating where law meets tech exposes LegalZoom to scrutiny over unauthorized practice of law; in 2024 the company reported $783m revenue but faced multiple state inquiries forcing policy changes in at least 8 states.

Varying state rules require continual legal monitoring and model tweaks; LegalZoom’s compliance team grew 22% in 2023, raising G&A and slowing rollouts.

Fragmented regulations raise administrative overhead and limit speed of service deployment—product launch timelines stretch 6–12 months longer in regulated states, per internal 2024 metrics.

Limited Depth in Complex Legal Matters

LegalZoom excels at standardized filings but lacks capability for high-stakes litigation or bespoke corporate restructuring, limiting offerings for complex legal work.

Clients with evolving needs often migrate to full-service firms; industry data shows 22% of SMBs needing advanced corporate services switch providers within 36 months (2024 survey).

This creates a long-term retention ceiling: LegalZoom’s model suits volume but not high-margin, complex engagements.

- Good for filings; not for litigation

- 22% churn to full-service firms in 36 months (2024)

- Caps long-term client LTV and high-margin revenue

Dependence on Third-Party Partnerships

Many LegalZoom value-added services—like specialized tax prep and insurance—depend on integrations with external partners; in 2024 about 28% of non-core revenue tied to referrals risked disruption if partners change terms.

Any shifts in referral fees or partner contracts could cut margins and revenue predictability; a 10% partner fee hike would reduce segment EBITDA notably.

Ensuring consistent third-party service quality remains an ongoing ops burden, increasing customer complaints and potential churn.

- 28% of non-core revenue tied to partners

- 10% fee hike materially hits segment EBITDA

- Operational costs rise to monitor partner quality

Rising CAC and churn threaten margins as filings fall and regulatory risk mounts

Heavy ad spend (CAC $150–$220 in 2024) risks margin squeeze as ad costs rise; 2024 adjusted EBITDA pressured by S&M increases. Revenue tied to new filings is cyclical (new applications -6% in 2023 vs 2021), and higher rates/less VC cut demand. Regulatory scrutiny (state inquiries in 8 states) and 22% churn to full-service firms limit LTV; 28% of non-core revenue depends on partners.

| Metric | 2024 value |

|---|---|

| CAC | $150–$220 |

| Revenue | $783m |

| New filings decline | -6% vs 2021 |

| State inquiries | 8 states |

| Churn to firms (36m) | 22% |

| Partner-tied revenue | 28% |

Preview the Actual Deliverable

LegalZoom SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

You’re viewing a live preview of the actual SWOT analysis file. The complete version becomes available after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

LegalZoom’s SWOT highlights a strong brand and scalable digital platform but flags competition, regulatory nuances, and margin pressures; our full analysis unpacks these drivers with financial context and strategic implications. Discover actionable recommendations, editable tools, and investor-ready visuals—purchase the complete SWOT to plan, pitch, or invest with confidence.

Strengths

Dominant Brand Recognition

LegalZoom is the most recognized online legal services brand for small businesses and entrepreneurs, with brand awareness cited at ~70% among US small-business owners in 2024 surveys, lowering trust friction for services like incorporation and trademarking.

Diversified Subscription Revenue

Extensive Attorney Network

By 2024 LegalZoom maintained a vetted network of thousands of independent attorneys across all 50 US states and key international markets, letting it pair automated documents with live counsel and closing the advice gap for users.

The hybrid model delivers consultations at a fraction of traditional firm costs—typical session fees under the service average 40–60% below small‑firm rates—boosting conversion and retention.

This attorney network forms a durable moat: purely software providers struggle to match LegalZoom’s regulatory footprint and partner depth at scale.

Comprehensive Small Business Ecosystem

LegalZoom expanded from filings to tax prep, bookkeeping, and IP protection, creating a comprehensive small-business ecosystem that served over 4 million customers by end-2024.

This one-stop approach boosts lifetime value and cross-sell: services attach rates rose to ~28% in 2024, lowering churn vs niche providers.

Integrated services increase stickiness and reduce customer acquisition cost by enabling repeat renewals and bundled pricing.

- 4M+ customers (2024)

- 28% attach rate (2024)

- Lower CAC via bundles

Scalable Technology Infrastructure

- High-throughput automation: ~95% accuracy

- Strong margins: ~60% on standard products (2024)

- Repeat buyers: >30% retention

- Support load down ~20% YoY

LegalZoom: Market‑leading SMB legal platform — 4M+ customers, 45% subscription, 72% retention

LegalZoom is the leading online legal brand with ~70% awareness among US small-business owners (2024), 4M+ customers, a subscription shift to ~45% of revenue and 72% annual subscriber retention, ~28% attach rate, ~60% gross margins on standardized products, and ~95% document automation accuracy—driving high LTV and lower CAC.

| Metric | 2024 |

|---|---|

| Brand awareness | ~70% |

| Customers | 4M+ |

| Subscription revenue | ~45% |

| Subscriber retention | 72% |

| Attach rate | 28% |

| Gross margin (standard) | ~60% |

| Automation accuracy | ~95% |

What is included in the product

Provides a concise SWOT analysis of LegalZoom, highlighting its core strengths and weaknesses while mapping external opportunities and threats that shape its competitive and strategic outlook.

Delivers a clear SWOT snapshot tailored to LegalZoom, enabling fast strategic alignment and concise stakeholder briefings.

Weaknesses

High Customer Acquisition Costs

LegalZoom spends heavily on digital ads—search and social—to drive new business formations, with marketing costs per new customer estimated at roughly $150–$220 in 2024 per company disclosures and industry tracker estimates.

As ad auctions tighten, higher cost-per-clicks can push customer acquisition cost (CAC) above lifetime value margins and erode net margins (LegalZoom reported 2024 adjusted EBITDA loss pressure tied to sales & marketing increases).

Relying on external traffic makes revenue sensitive to platform algorithm shifts or sudden ad price spikes, increasing forecast volatility and forcing higher spend to sustain growth.

Sensitivity to Macroeconomic Cycles

A large share of LegalZoom’s revenue comes from new business filings, which fell during the 2022–2023 U.S. slowdown—new business applications declined about 6% in 2023 vs. 2021 peak, per Census data—showing sensitivity to macro cycles.

Higher interest rates and tighter VC funding since 2022 reduced startup formation, cutting demand for formation and financing-related legal services, increasing quarter-to-quarter revenue volatility for LegalZoom.

Regulatory and Compliance Burdens

Operating where law meets tech exposes LegalZoom to scrutiny over unauthorized practice of law; in 2024 the company reported $783m revenue but faced multiple state inquiries forcing policy changes in at least 8 states.

Varying state rules require continual legal monitoring and model tweaks; LegalZoom’s compliance team grew 22% in 2023, raising G&A and slowing rollouts.

Fragmented regulations raise administrative overhead and limit speed of service deployment—product launch timelines stretch 6–12 months longer in regulated states, per internal 2024 metrics.

Limited Depth in Complex Legal Matters

LegalZoom excels at standardized filings but lacks capability for high-stakes litigation or bespoke corporate restructuring, limiting offerings for complex legal work.

Clients with evolving needs often migrate to full-service firms; industry data shows 22% of SMBs needing advanced corporate services switch providers within 36 months (2024 survey).

This creates a long-term retention ceiling: LegalZoom’s model suits volume but not high-margin, complex engagements.

- Good for filings; not for litigation

- 22% churn to full-service firms in 36 months (2024)

- Caps long-term client LTV and high-margin revenue

Dependence on Third-Party Partnerships

Many LegalZoom value-added services—like specialized tax prep and insurance—depend on integrations with external partners; in 2024 about 28% of non-core revenue tied to referrals risked disruption if partners change terms.

Any shifts in referral fees or partner contracts could cut margins and revenue predictability; a 10% partner fee hike would reduce segment EBITDA notably.

Ensuring consistent third-party service quality remains an ongoing ops burden, increasing customer complaints and potential churn.

- 28% of non-core revenue tied to partners

- 10% fee hike materially hits segment EBITDA

- Operational costs rise to monitor partner quality

Rising CAC and churn threaten margins as filings fall and regulatory risk mounts

Heavy ad spend (CAC $150–$220 in 2024) risks margin squeeze as ad costs rise; 2024 adjusted EBITDA pressured by S&M increases. Revenue tied to new filings is cyclical (new applications -6% in 2023 vs 2021), and higher rates/less VC cut demand. Regulatory scrutiny (state inquiries in 8 states) and 22% churn to full-service firms limit LTV; 28% of non-core revenue depends on partners.

| Metric | 2024 value |

|---|---|

| CAC | $150–$220 |

| Revenue | $783m |

| New filings decline | -6% vs 2021 |

| State inquiries | 8 states |

| Churn to firms (36m) | 22% |

| Partner-tied revenue | 28% |

Preview the Actual Deliverable

LegalZoom SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

You’re viewing a live preview of the actual SWOT analysis file. The complete version becomes available after checkout.