Legend Biotech Porter's Five Forces Analysis

Don't Miss the Bigger Picture

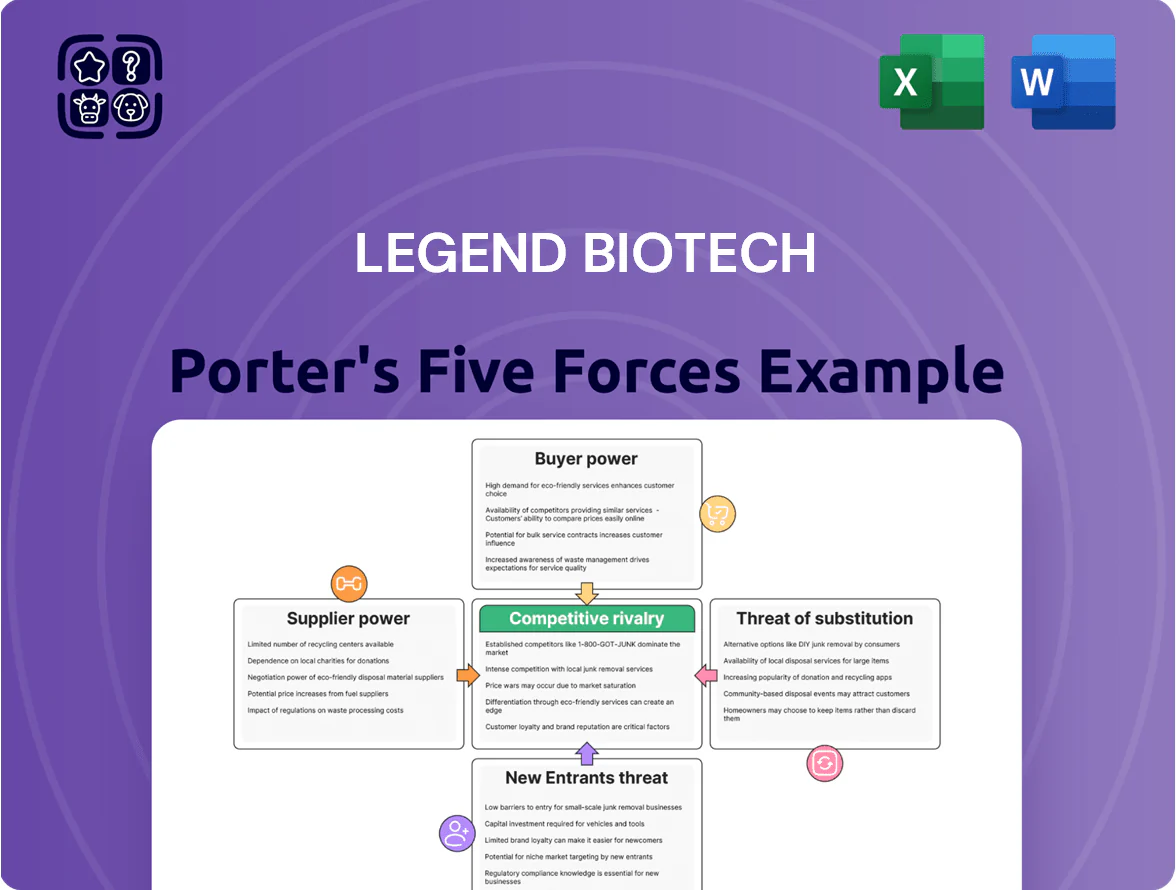

Legend Biotech faces high competitive rivalry and moderate supplier power, while patent-backed therapies reduce immediate substitute threats but raise barriers for entrants; this snapshot highlights key tensions between clinical differentiation and commercialization risk. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, strategic implications, and data-backed recommendations tailored to investment and corporate strategy.

Suppliers Bargaining Power

Specialized Raw Material Dependency

Legend Biotech’s CAR-T production depends on specialized viral vectors and culture media from few suppliers; disruptions can delay manufacturing and raise costs. In 2024 supply constraints pushed viral vector prices up ~20% and caused batch delays of 2–6 weeks for some firms, giving suppliers leverage on pricing and contract terms. Proprietary inputs limit switching options and increase supplier bargaining power.

Limited Plasmid and Vector Manufacturing Capacity

Global shortage of GMP-grade viral vectors—estimated demand outstripping supply by ~30% in 2024—raises supplier leverage; Legend Biotech (NASDAQ: LEGN) scaled internal plasmid/vector lines but still buys key genetic components and single-use equipment from CDMOs, giving those suppliers pricing and timing power. Major CDMOs (Thermo Fisher, Catalent) reported 15–25% margin premiums on biotech contracts in 2024, pressuring smaller firms and forcing Legend to hedge via long-term supply deals.

High Switching Costs for Validated Inputs

Regulators like FDA and EMA demand validated, consistent manufacturing for cell therapies, so switching a primary reagent supplier forces extensive re-validation and comparability studies costing months and often $1–5M per change; this raises time-to-market risk and compliance burden.

Specialized Equipment and Technology Providers

Specialized automated and closed-loop cell therapy systems are concentrated among a few providers (Lonza, Miltenyi Biotec), and Legend Biotech depends on their proprietary hardware and software for sterile, precise processing.

Because alternatives are scarce and integration costs are high, suppliers hold strong bargaining power—Lonza reported 2024 revenues of €4.7bn, showing scale advantage and pricing leverage.

- Few suppliers: Lonza, Miltenyi

- High switching cost: integration, validation

- Proprietary IP → pricing power

- 2024 Lonza revenue €4.7bn indicates market scale

Concentration of Specialized Labor

The global pool of skilled cell-therapy specialists is tiny—estimated shortages reached 30% in bioprocessing roles by 2024—so Legend Biotech faces intense competition for talent that raises labor costs and benefits obligations.

As CAR-T and allogeneic programs scale, global hiring pressure gives technicians and scientists bargaining power, forcing higher wages, signing bonuses, and relocation packages to protect proprietary platforms.

Legend must deploy global recruiting, training pipelines, and retention pay; failure risks capacity bottlenecks and delayed product launches that can cut near-term revenue growth.

- ~30% bioprocessing talent gap (2024)

- Higher comp raises COGS and R&D spend

- Global hiring + training needed to secure platforms

Supplier squeeze: viral-vector shortfall, 15–25% CDMO hikes, $1–5M switching costs

Suppliers hold strong leverage: limited GMP viral-vector/CDMO and closed-system vendors (Lonza, Miltenyi) raised prices ~15–25% in 2024; viral-vector shortage ~30% gap; switching costs $1–5M and months for re-validation; bioprocess talent gap ~30% inflates labor COGS.

| Metric | 2024 value |

|---|---|

| Viral-vector supply gap | ~30% |

| CDMO price premium | 15–25% |

| Switching cost | $1–5M / months |

| Talent gap | ~30% |

What is included in the product

Tailored Porter's Five Forces analysis for Legend Biotech, outlining competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and pinpointing disruptive risks and strategic levers affecting pricing, profitability, and market positioning.

Compact Porter's Five Forces snapshot for Legend Biotech—quickly pinpoint bargaining power, rivalry, and regulatory threats to accelerate strategic decisions.

Customers Bargaining Power

Consolidated Payer Influence

In the US and EU, large government payers and insurers—Medicare, Medicaid, NHS England, and top private insurers—control reimbursement and can negotiate steep discounts; in 2024 Medicare drug spending was $157B, showing scale. These payers push for strong phase III/real-world evidence to justify cell-therapy prices often >$400,000 per course, and can exclude therapies from formularies, creating acute buyer power.

Concentration of Specialized Treatment Centers

CERTIFIED CAR-T centers are few: in the US ~250 sites were authorized for CAR-T as of Dec 2024, concentrating purchasing power in hospitals and academic medical centers that can handle cell processing. These centers set formularies and scheduling priorities, meaning institutional preferences and credentialing can shift volume between competitors; for Carvykti (approved Nov 2022) this concentration likely affects uptake and site-level market share. In 2024, top 50 centers performed ~40% of CAR-T procedures, amplifying buyer influence.

Value-Based Pricing Pressure

Availability of Alternative Clinical Trials

Patients and physicians can choose competing clinical trials over commercial therapies, giving buyers leverage; in oncology trials enrollment rose ~12% since 2020, expanding experimental access.

Trials often offer cutting-edge drugs at low/no cost, so commercial products must show clear superior efficacy—CAR-T therapies face pressure with median OS and response-rate comparisons driving switching.

Availability of trials acts as buyer power by lowering price sensitivity and shortening adoption windows; Legend must demonstrate differentiated outcomes and real-world value to retain customers.

- Clinical-trial enrollment +12% since 2020

- Trials reduce out‑of‑pocket cost, increasing trial uptake

- Comparative efficacy (OS/response rates) determines switch

Government Price Negotiations

Legislation like the 2022 Inflation Reduction Act lets Medicare negotiate prices for select high-cost drugs starting 2026, boosting government bargaining power versus manufacturers such as Legend Biotech.

As Legend’s CAR-T therapies approach Medicare’s expenditure thresholds—estimated program targets covering drugs with annual US spend in the billions—they face federal price caps, mandatory rebates, and phased-in negotiated maximums, cutting potential revenue.

This regulatory shift strengthens government buyers over time; CMS negotiation could lower net prices by an estimated 20–40% for targeted products based on 2023 Medicare drug spend precedents.

- IRA enables Medicare negotiation from 2026

- Targets: high-spend drugs (annual US spend ~billions)

- Estimated price reductions 20–40% (2023-based)

- Impacts: caps, rebates, phased negotiation

Buyers’ leverage could force 20–40% CAR‑T price cuts and outcome‑risk for Legend

Buyers (govt payers, insurers, ~250 US CAR-T centers) have strong leverage: Medicare/insurer negotiation, outcome-based deals (8–12% of advanced therapy contracts in 2024), concentrated sites (top 50 = ~40% procedures), and IRA negotiation (from 2026) can cut net prices ~20–40%, forcing Legend to fund real‑world evidence and accept payment-at-risk.

| Metric | Value (2024) |

|---|---|

| Authorized US CAR‑T sites | ~250 |

| Top‑50 share of procedures | ~40% |

| Outcome‑based deals | 8–12% |

| Estimated Medicare price cut | 20–40% |

Preview the Actual Deliverable

Legend Biotech Porter's Five Forces Analysis

This preview shows the exact Legend Biotech Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Legend Biotech faces high competitive rivalry and moderate supplier power, while patent-backed therapies reduce immediate substitute threats but raise barriers for entrants; this snapshot highlights key tensions between clinical differentiation and commercialization risk. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, strategic implications, and data-backed recommendations tailored to investment and corporate strategy.

Suppliers Bargaining Power

Specialized Raw Material Dependency

Legend Biotech’s CAR-T production depends on specialized viral vectors and culture media from few suppliers; disruptions can delay manufacturing and raise costs. In 2024 supply constraints pushed viral vector prices up ~20% and caused batch delays of 2–6 weeks for some firms, giving suppliers leverage on pricing and contract terms. Proprietary inputs limit switching options and increase supplier bargaining power.

Limited Plasmid and Vector Manufacturing Capacity

Global shortage of GMP-grade viral vectors—estimated demand outstripping supply by ~30% in 2024—raises supplier leverage; Legend Biotech (NASDAQ: LEGN) scaled internal plasmid/vector lines but still buys key genetic components and single-use equipment from CDMOs, giving those suppliers pricing and timing power. Major CDMOs (Thermo Fisher, Catalent) reported 15–25% margin premiums on biotech contracts in 2024, pressuring smaller firms and forcing Legend to hedge via long-term supply deals.

High Switching Costs for Validated Inputs

Regulators like FDA and EMA demand validated, consistent manufacturing for cell therapies, so switching a primary reagent supplier forces extensive re-validation and comparability studies costing months and often $1–5M per change; this raises time-to-market risk and compliance burden.

Specialized Equipment and Technology Providers

Specialized automated and closed-loop cell therapy systems are concentrated among a few providers (Lonza, Miltenyi Biotec), and Legend Biotech depends on their proprietary hardware and software for sterile, precise processing.

Because alternatives are scarce and integration costs are high, suppliers hold strong bargaining power—Lonza reported 2024 revenues of €4.7bn, showing scale advantage and pricing leverage.

- Few suppliers: Lonza, Miltenyi

- High switching cost: integration, validation

- Proprietary IP → pricing power

- 2024 Lonza revenue €4.7bn indicates market scale

Concentration of Specialized Labor

The global pool of skilled cell-therapy specialists is tiny—estimated shortages reached 30% in bioprocessing roles by 2024—so Legend Biotech faces intense competition for talent that raises labor costs and benefits obligations.

As CAR-T and allogeneic programs scale, global hiring pressure gives technicians and scientists bargaining power, forcing higher wages, signing bonuses, and relocation packages to protect proprietary platforms.

Legend must deploy global recruiting, training pipelines, and retention pay; failure risks capacity bottlenecks and delayed product launches that can cut near-term revenue growth.

- ~30% bioprocessing talent gap (2024)

- Higher comp raises COGS and R&D spend

- Global hiring + training needed to secure platforms

Supplier squeeze: viral-vector shortfall, 15–25% CDMO hikes, $1–5M switching costs

Suppliers hold strong leverage: limited GMP viral-vector/CDMO and closed-system vendors (Lonza, Miltenyi) raised prices ~15–25% in 2024; viral-vector shortage ~30% gap; switching costs $1–5M and months for re-validation; bioprocess talent gap ~30% inflates labor COGS.

| Metric | 2024 value |

|---|---|

| Viral-vector supply gap | ~30% |

| CDMO price premium | 15–25% |

| Switching cost | $1–5M / months |

| Talent gap | ~30% |

What is included in the product

Tailored Porter's Five Forces analysis for Legend Biotech, outlining competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and pinpointing disruptive risks and strategic levers affecting pricing, profitability, and market positioning.

Compact Porter's Five Forces snapshot for Legend Biotech—quickly pinpoint bargaining power, rivalry, and regulatory threats to accelerate strategic decisions.

Customers Bargaining Power

Consolidated Payer Influence

In the US and EU, large government payers and insurers—Medicare, Medicaid, NHS England, and top private insurers—control reimbursement and can negotiate steep discounts; in 2024 Medicare drug spending was $157B, showing scale. These payers push for strong phase III/real-world evidence to justify cell-therapy prices often >$400,000 per course, and can exclude therapies from formularies, creating acute buyer power.

Concentration of Specialized Treatment Centers

CERTIFIED CAR-T centers are few: in the US ~250 sites were authorized for CAR-T as of Dec 2024, concentrating purchasing power in hospitals and academic medical centers that can handle cell processing. These centers set formularies and scheduling priorities, meaning institutional preferences and credentialing can shift volume between competitors; for Carvykti (approved Nov 2022) this concentration likely affects uptake and site-level market share. In 2024, top 50 centers performed ~40% of CAR-T procedures, amplifying buyer influence.

Value-Based Pricing Pressure

Availability of Alternative Clinical Trials

Patients and physicians can choose competing clinical trials over commercial therapies, giving buyers leverage; in oncology trials enrollment rose ~12% since 2020, expanding experimental access.

Trials often offer cutting-edge drugs at low/no cost, so commercial products must show clear superior efficacy—CAR-T therapies face pressure with median OS and response-rate comparisons driving switching.

Availability of trials acts as buyer power by lowering price sensitivity and shortening adoption windows; Legend must demonstrate differentiated outcomes and real-world value to retain customers.

- Clinical-trial enrollment +12% since 2020

- Trials reduce out‑of‑pocket cost, increasing trial uptake

- Comparative efficacy (OS/response rates) determines switch

Government Price Negotiations

Legislation like the 2022 Inflation Reduction Act lets Medicare negotiate prices for select high-cost drugs starting 2026, boosting government bargaining power versus manufacturers such as Legend Biotech.

As Legend’s CAR-T therapies approach Medicare’s expenditure thresholds—estimated program targets covering drugs with annual US spend in the billions—they face federal price caps, mandatory rebates, and phased-in negotiated maximums, cutting potential revenue.

This regulatory shift strengthens government buyers over time; CMS negotiation could lower net prices by an estimated 20–40% for targeted products based on 2023 Medicare drug spend precedents.

- IRA enables Medicare negotiation from 2026

- Targets: high-spend drugs (annual US spend ~billions)

- Estimated price reductions 20–40% (2023-based)

- Impacts: caps, rebates, phased negotiation

Buyers’ leverage could force 20–40% CAR‑T price cuts and outcome‑risk for Legend

Buyers (govt payers, insurers, ~250 US CAR-T centers) have strong leverage: Medicare/insurer negotiation, outcome-based deals (8–12% of advanced therapy contracts in 2024), concentrated sites (top 50 = ~40% procedures), and IRA negotiation (from 2026) can cut net prices ~20–40%, forcing Legend to fund real‑world evidence and accept payment-at-risk.

| Metric | Value (2024) |

|---|---|

| Authorized US CAR‑T sites | ~250 |

| Top‑50 share of procedures | ~40% |

| Outcome‑based deals | 8–12% |

| Estimated Medicare price cut | 20–40% |

Preview the Actual Deliverable

Legend Biotech Porter's Five Forces Analysis

This preview shows the exact Legend Biotech Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.