Legend Holding Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

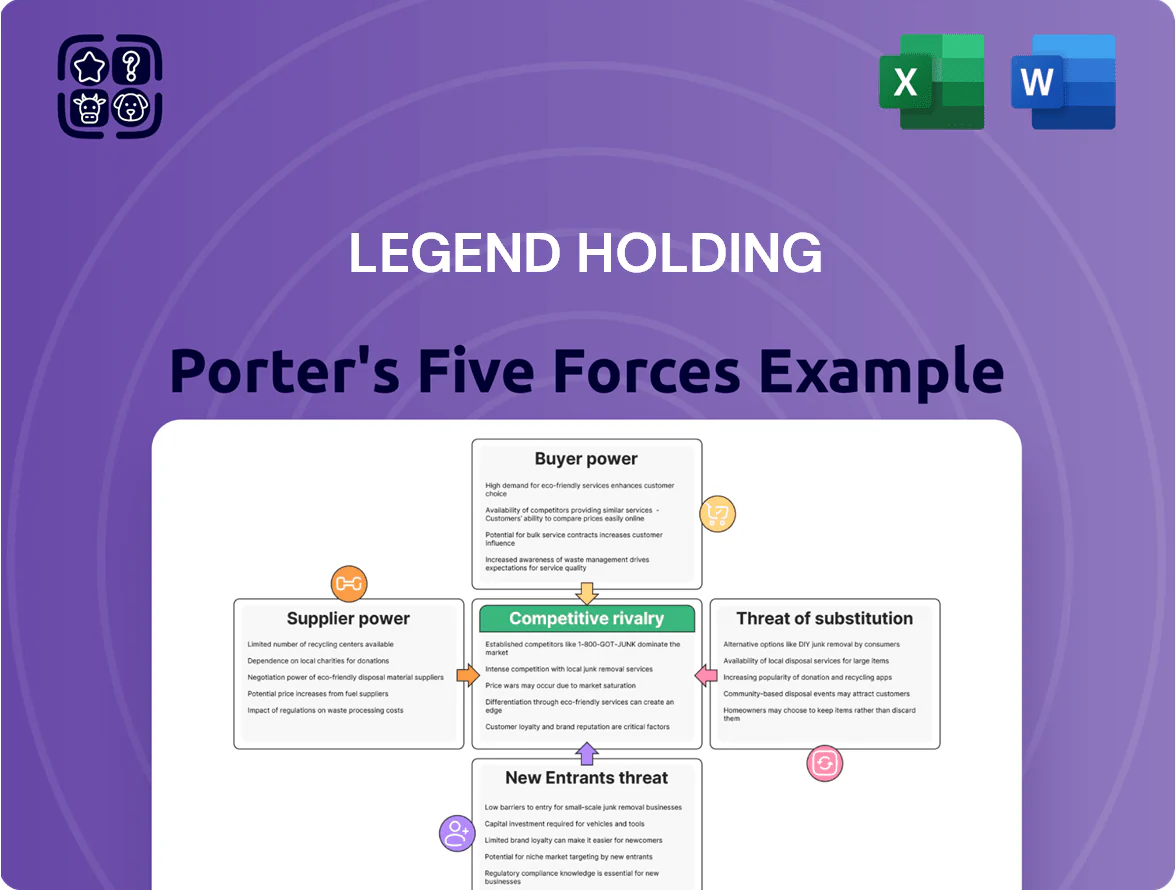

Legend Holding faces moderate supplier power and rising competitive intensity from agile entrants, while buyer leverage and substitutes vary across its diversified segments, creating a complex strategic landscape.

This snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Legend Holding’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of semiconductor and component providers

The IT segment, led by Lenovo within Legend Holdings, depends on a few global suppliers for CPUs and GPUs; Nvidia and Intel supply over 70% of high-performance AI chips used in enterprise PCs and servers as of 2025.

By end-2025 supply chains diversified regionally, but AI chip technical complexity keeps Nvidia and Intel with strong leverage over pricing and lead times.

This supplier concentration lets them set premium prices—Nvidia raised datacenter GPU ASPs ~15% in 2024—squeezing Legend’s margins in its largest revenue sector.

Volatility in agricultural raw material sourcing

Legend Holdings' agriculture and food investments face rising supplier power as climate-driven yield shocks lift raw-ingredient prices; global cereal production fell 1.3% in 2024, tightening supply chains and raising input costs for food processors.

Primary producers can demand higher margins—farmgate prices for key crops rose ~12% YoY in 2024—forcing Legend to hedge via long-term contracts and vertical integration to protect margins across its food subsidiaries.

Access to institutional capital and credit markets

As an investment holding company, Legend depends on banks and debt markets to fund acquisitions and expansion, with 2025 term debt spreads averaging about 320 bps over swaps for mid‑rating corporates, raising borrowing costs materially.

Central bank policy drove policy rates to roughly 5.25% in late 2025, so lenders dictate covenants, maturities, and pricing based on Legend’s consolidated credit profile rather than weaker subsidiaries.

In this high‑rate climate lenders hold bargaining power: syndicated loans and bonds demand tighter covenants and higher collateral, often increasing effective cost of capital by 1.5–3 percentage points versus pre‑2022 levels.

Specialized labor and technical expertise

Advanced manufacturing and financial services at Legend Holdings demand AI, biotech, and wealth-management experts; global competition pushed median AI engineer salaries up 18% in 2024 to about $150,000, boosting supplier (labor) leverage.

High churn and scarce researchers give staff strong bargaining power over pay, equity, and remote terms; Legend must spend more on retention—industry data show training and hiring costs can reach 20% of annual payroll.

- Specialized roles = high pay pressure (AI median ~$150k, 2024)

- Churn raises hiring/training cost ~20% of payroll

- Retention needs ongoing investment in comp, equity, and R&D access

Intellectual property and software licensing

High supplier power, rising costs: AI chip concentration, wages, rates squeeze margins

Supplier power is high: AI chip concentration (Nvidia+Intel >70% of high‑perf AI chips, 2025) and SaaS spend (~$430B, 2024) drive margins; farmgate prices +12% YoY (2024) and cereal output −1.3% (2024) raise input costs; mid‑corp debt spreads ~320bps (2025) and policy rates ~5.25% tighten financing; AI engineer median pay ~$150k (2024) increases labor costs.

| Metric | Value |

|---|---|

| AI chip share | >70% (Nvidia+Intel, 2025) |

| Enterprise SW spend | $430B (2024) |

| Farmgate price change | +12% YoY (2024) |

| Cereal output | −1.3% (2024) |

| Debt spread | ~320bps (2025) |

| Policy rate | ~5.25% (late 2025) |

| AI engineer pay | $150k median (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Legend Holding that uncovers competitive drivers, buyer and supplier power, entry barriers, and substitution threats to assess pricing leverage and strategic risks.

A concise one-sheet Porter's Five Forces for Legend Holding—visualize competitive pressure with an editable radar chart, swap in your own data, and drop straight into pitch decks or dashboards for faster, board-ready decisions.

Customers Bargaining Power

Enterprise procurement for IT infrastructure

Large corporate and government buyers of Lenovo-scale IT infrastructure wield strong leverage, often securing 10–25% average volume discounts on deals above $5M and asking for custom configs and extended warranties; in 2024 Lenovo reported 18% of revenue from large enterprise contracts.

Price sensitivity in innovative consumption

In consumption and services, consumers face low switching costs and high info access, and 72% of Chinese shoppers surveyed in 2024 compared prices online before purchase, raising price sensitivity for Legend Holdings (SEHK:03396).

Brand fatigue is common and alternatives are a click away—Legend must keep service NPS high and pricing competitive to avoid churn; a 1% price premium can cut conversion by ~3% in digital retail channels.

That pressure forces continued investment in customer service and dynamic pricing; in 2024 Legend’s portfolio companies reported average gross margins of ~18%, constraining room for price cuts.

Sophistication of financial services clients

Clients in Legend Holding’s financial arm—notably institutional investors and HNWIs—are highly informed and demand superior risk-adjusted returns, with 2024 data showing 68% of institutions rebalancing annually and 42% switching managers after underperformance over 3 years. These customers can readily move assets: global ETF flows hit $1.2 trillion in 2024, lowering switching frictions and raising churn risk if benchmarks lag. Fee sensitivity is acute—median hedge fund fees fell to 1.25/15 in 2024—so perceived excessive pricing prompts outflows. The 2025 market’s transparency, driven by expanded reporting and real-time analytics, increases pressure on Legend to show clear, differentiated value.

Retail buyer influence in the food sector

Retail buyer influence in food is rising as 72% of Chinese consumers (2024 Nielsen) prioritize health and 65% prioritize sustainability, pressuring suppliers for traceability and eco-claims.

Buyers can boycott or switch brands quickly—global plant-based sales rose 28% in 2023—so noncompliant products face rapid share loss.

Legend Holdings must upgrade supply-chain traceability, certify sustainability, and relabel products to retain margins and market share.

- 72% Chinese consumers: health-focused (2024 Nielsen)

- 65% prioritize sustainability (2024 Nielsen)

- Plant-based sales +28% in 2023 (Euromonitor)

- Action: traceability, certifications, relabeling

Consolidation of distribution channels

Major e-commerce platforms and retail chains act as powerful intermediaries for Legend Holdings’ subsidiaries, controlling shelf placement, ads, and margin splits—especially in consumer electronics and food.

By 2025, three global marketplaces account for ~55–65% of online sales in key markets, forcing Legend to accept unfavorable terms to retain broad access; in 2024 logistics/marketing fees rose 2–4% EBITDA impact for peers.

- Platform concentration: ~55–65% market share (top 3)

- Areas hit: consumer electronics, food

- Costs: 2–4% EBITDA pressure (2024 peers)

- Leverage: low vs. dominant distributors

Enterprise discounts & platform concentration squeeze margins as consumers hunt prices

Customers hold strong leverage: large enterprise deals get 10–25% discounts (>$5M); 18% revenue from enterprise (2024). Consumers show high price sensitivity—72% compare online (2024); 1% price premium cuts conversion ~3%. Financial clients rebalance/switch often (68%/42% in 2024); fee pressure—median hedge fees 1.25/15 (2024). Platforms concentrate 55–65% online sales (top3).

| Metric | Value (Year) |

|---|---|

| Enterprise discount | 10–25% (2024) |

| Enterprise rev | 18% (2024) |

| Online price checks | 72% China (2024) |

| Hedge fees median | 1.25/15 (2024) |

| Top3 platforms | 55–65% share (2025 est.) |

Full Version Awaits

Legend Holding Porter's Five Forces Analysis

This preview shows the exact Legend Holding Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, complete, and ready for use with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Legend Holding faces moderate supplier power and rising competitive intensity from agile entrants, while buyer leverage and substitutes vary across its diversified segments, creating a complex strategic landscape.

This snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Legend Holding’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of semiconductor and component providers

The IT segment, led by Lenovo within Legend Holdings, depends on a few global suppliers for CPUs and GPUs; Nvidia and Intel supply over 70% of high-performance AI chips used in enterprise PCs and servers as of 2025.

By end-2025 supply chains diversified regionally, but AI chip technical complexity keeps Nvidia and Intel with strong leverage over pricing and lead times.

This supplier concentration lets them set premium prices—Nvidia raised datacenter GPU ASPs ~15% in 2024—squeezing Legend’s margins in its largest revenue sector.

Volatility in agricultural raw material sourcing

Legend Holdings' agriculture and food investments face rising supplier power as climate-driven yield shocks lift raw-ingredient prices; global cereal production fell 1.3% in 2024, tightening supply chains and raising input costs for food processors.

Primary producers can demand higher margins—farmgate prices for key crops rose ~12% YoY in 2024—forcing Legend to hedge via long-term contracts and vertical integration to protect margins across its food subsidiaries.

Access to institutional capital and credit markets

As an investment holding company, Legend depends on banks and debt markets to fund acquisitions and expansion, with 2025 term debt spreads averaging about 320 bps over swaps for mid‑rating corporates, raising borrowing costs materially.

Central bank policy drove policy rates to roughly 5.25% in late 2025, so lenders dictate covenants, maturities, and pricing based on Legend’s consolidated credit profile rather than weaker subsidiaries.

In this high‑rate climate lenders hold bargaining power: syndicated loans and bonds demand tighter covenants and higher collateral, often increasing effective cost of capital by 1.5–3 percentage points versus pre‑2022 levels.

Specialized labor and technical expertise

Advanced manufacturing and financial services at Legend Holdings demand AI, biotech, and wealth-management experts; global competition pushed median AI engineer salaries up 18% in 2024 to about $150,000, boosting supplier (labor) leverage.

High churn and scarce researchers give staff strong bargaining power over pay, equity, and remote terms; Legend must spend more on retention—industry data show training and hiring costs can reach 20% of annual payroll.

- Specialized roles = high pay pressure (AI median ~$150k, 2024)

- Churn raises hiring/training cost ~20% of payroll

- Retention needs ongoing investment in comp, equity, and R&D access

Intellectual property and software licensing

High supplier power, rising costs: AI chip concentration, wages, rates squeeze margins

Supplier power is high: AI chip concentration (Nvidia+Intel >70% of high‑perf AI chips, 2025) and SaaS spend (~$430B, 2024) drive margins; farmgate prices +12% YoY (2024) and cereal output −1.3% (2024) raise input costs; mid‑corp debt spreads ~320bps (2025) and policy rates ~5.25% tighten financing; AI engineer median pay ~$150k (2024) increases labor costs.

| Metric | Value |

|---|---|

| AI chip share | >70% (Nvidia+Intel, 2025) |

| Enterprise SW spend | $430B (2024) |

| Farmgate price change | +12% YoY (2024) |

| Cereal output | −1.3% (2024) |

| Debt spread | ~320bps (2025) |

| Policy rate | ~5.25% (late 2025) |

| AI engineer pay | $150k median (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Legend Holding that uncovers competitive drivers, buyer and supplier power, entry barriers, and substitution threats to assess pricing leverage and strategic risks.

A concise one-sheet Porter's Five Forces for Legend Holding—visualize competitive pressure with an editable radar chart, swap in your own data, and drop straight into pitch decks or dashboards for faster, board-ready decisions.

Customers Bargaining Power

Enterprise procurement for IT infrastructure

Large corporate and government buyers of Lenovo-scale IT infrastructure wield strong leverage, often securing 10–25% average volume discounts on deals above $5M and asking for custom configs and extended warranties; in 2024 Lenovo reported 18% of revenue from large enterprise contracts.

Price sensitivity in innovative consumption

In consumption and services, consumers face low switching costs and high info access, and 72% of Chinese shoppers surveyed in 2024 compared prices online before purchase, raising price sensitivity for Legend Holdings (SEHK:03396).

Brand fatigue is common and alternatives are a click away—Legend must keep service NPS high and pricing competitive to avoid churn; a 1% price premium can cut conversion by ~3% in digital retail channels.

That pressure forces continued investment in customer service and dynamic pricing; in 2024 Legend’s portfolio companies reported average gross margins of ~18%, constraining room for price cuts.

Sophistication of financial services clients

Clients in Legend Holding’s financial arm—notably institutional investors and HNWIs—are highly informed and demand superior risk-adjusted returns, with 2024 data showing 68% of institutions rebalancing annually and 42% switching managers after underperformance over 3 years. These customers can readily move assets: global ETF flows hit $1.2 trillion in 2024, lowering switching frictions and raising churn risk if benchmarks lag. Fee sensitivity is acute—median hedge fund fees fell to 1.25/15 in 2024—so perceived excessive pricing prompts outflows. The 2025 market’s transparency, driven by expanded reporting and real-time analytics, increases pressure on Legend to show clear, differentiated value.

Retail buyer influence in the food sector

Retail buyer influence in food is rising as 72% of Chinese consumers (2024 Nielsen) prioritize health and 65% prioritize sustainability, pressuring suppliers for traceability and eco-claims.

Buyers can boycott or switch brands quickly—global plant-based sales rose 28% in 2023—so noncompliant products face rapid share loss.

Legend Holdings must upgrade supply-chain traceability, certify sustainability, and relabel products to retain margins and market share.

- 72% Chinese consumers: health-focused (2024 Nielsen)

- 65% prioritize sustainability (2024 Nielsen)

- Plant-based sales +28% in 2023 (Euromonitor)

- Action: traceability, certifications, relabeling

Consolidation of distribution channels

Major e-commerce platforms and retail chains act as powerful intermediaries for Legend Holdings’ subsidiaries, controlling shelf placement, ads, and margin splits—especially in consumer electronics and food.

By 2025, three global marketplaces account for ~55–65% of online sales in key markets, forcing Legend to accept unfavorable terms to retain broad access; in 2024 logistics/marketing fees rose 2–4% EBITDA impact for peers.

- Platform concentration: ~55–65% market share (top 3)

- Areas hit: consumer electronics, food

- Costs: 2–4% EBITDA pressure (2024 peers)

- Leverage: low vs. dominant distributors

Enterprise discounts & platform concentration squeeze margins as consumers hunt prices

Customers hold strong leverage: large enterprise deals get 10–25% discounts (>$5M); 18% revenue from enterprise (2024). Consumers show high price sensitivity—72% compare online (2024); 1% price premium cuts conversion ~3%. Financial clients rebalance/switch often (68%/42% in 2024); fee pressure—median hedge fees 1.25/15 (2024). Platforms concentrate 55–65% online sales (top3).

| Metric | Value (Year) |

|---|---|

| Enterprise discount | 10–25% (2024) |

| Enterprise rev | 18% (2024) |

| Online price checks | 72% China (2024) |

| Hedge fees median | 1.25/15 (2024) |

| Top3 platforms | 55–65% share (2025 est.) |

Full Version Awaits

Legend Holding Porter's Five Forces Analysis

This preview shows the exact Legend Holding Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, complete, and ready for use with no placeholders or mockups.