Lennar Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

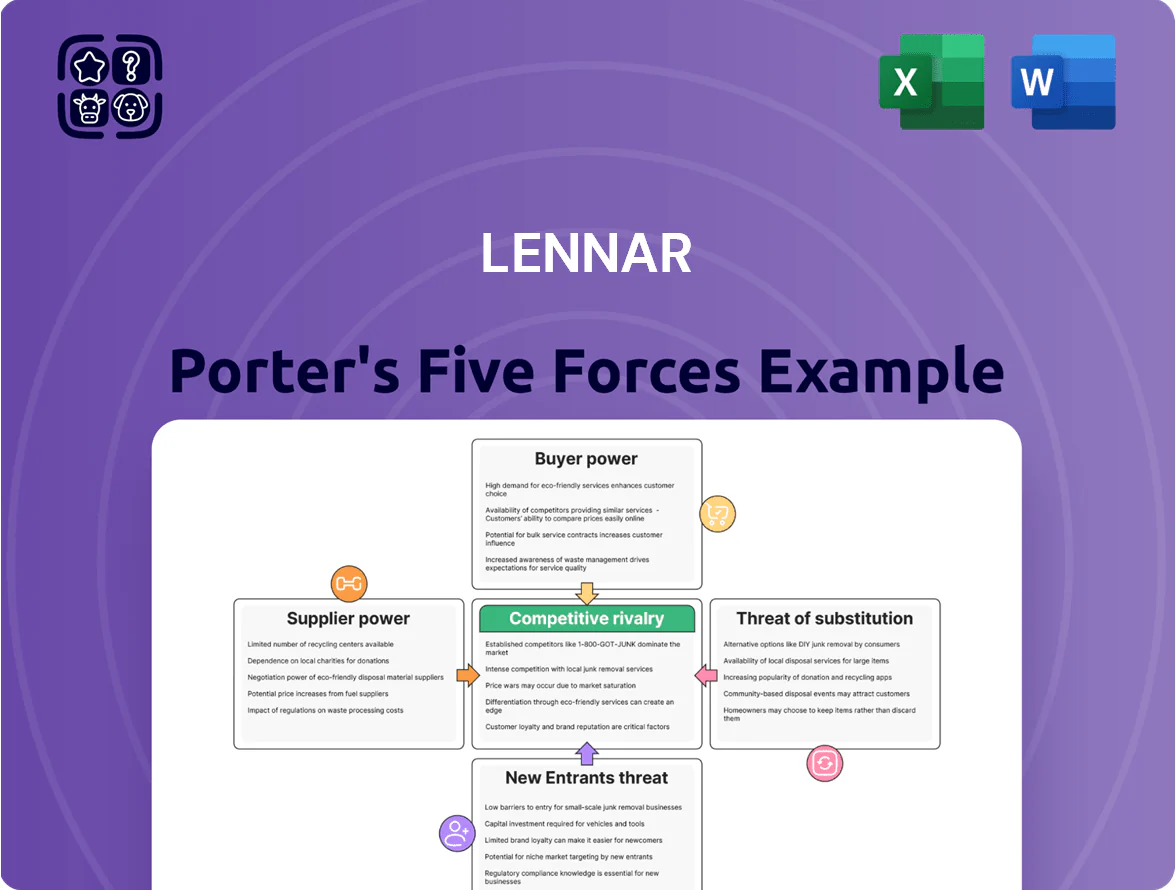

Lennar faces a mix of strong buyer power, moderate supplier leverage, and high rivalry as homebuilders compete on price, land access, and product differentiation, while regulatory hurdles and cyclical demand shape entry threats and substitutes.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lennar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in Raw Material Costs

Lennar depends on lumber, steel and concrete, commodities with volatile global prices; lumber futures rose ~40% in 2020–2021 and remained 12% higher year-over-year in 2024, pressuring input costs.

Scale gives Lennar bargaining power and volume discounts—2024 homebuilding revenue was $37.6B—yet sudden material spikes can compress gross margins if costs aren’t passed to buyers.

Management uses strategic sourcing, long‑term contracts and hedges to reduce exposure, but supplier-driven price hikes remain a recurring margin risk.

Shortage of Skilled Subcontractor Labor

The homebuilding sector faces a chronic shortage of skilled trades—electricians, plumbers, framers—driving subcontractor leverage during booms; the US had a 2024 shortage of roughly 300,000 construction-skilled workers per Associated Builders and Contractors.

Lennar relies on third-party subs rather than direct hires, so subs can demand higher rates; Lennar mitigates this by offering steady volume but still saw labor cost inflation add about 2–3 percentage points to gross margin pressure in 2023–2024.

Concentration of Key Product Vendors

For specialized items like appliances, HVAC, and smart-home kits Lennar relies on a handful of national vendors, creating supplier concentration that can trigger bottlenecks if a key supplier has production or logistics failures; for example, in 2023 US appliance lead times spiked 30% and Lennar reported supplier-related delays on ~4% of closings in FY2024. Lennar mitigates risk via long-term strategic alliances that secure priority allocation for its high-volume orders over smaller builders.

Land Seller Leverage in Prime Markets

Land in high-growth U.S. corridors is scarce, so sellers hold strong leverage; Lennar reported land purchase costs rising ~18% year-over-year in 2024, pressuring margins.

Lennar uses options and a strategic land bank—land owned for future development—to lock pipelines while deferring full capital outlay; at FY2024 it held roughly $9.5B in land and land development inventory.

As prime areas saturate, acquisition costs climb and compress project IRRs, forcing longer hold periods or higher home prices to preserve profitability.

- Land scarcity raises seller leverage

- 2024 land costs +18% YoY

- Lennar land inventory ~$9.5B (FY2024)

- Rising costs compress IRR, may increase home prices

Impact of Global Logistics and Tariffs

Suppliers of imported finished goods face shipping delays and trade-policy shifts; global container rates rose 38% in 2023 vs 2022, pressuring lead times and costs.

Tariffs—like U.S. levies that raised lumber and appliance import costs by up to 12–15% in recent cycles—often get passed to homebuilders as per-supplier markups.

Lennar tracks these geopolitical risks daily, adjusts procurement, and diversified 2024 sourcing to cut tariff exposure and keep component flow steady.

- 2023 container rates +38%

- Tariff-driven cost jumps ~12–15%

- Lennar increased sourcing diversity in 2024

Lennar's scale cushions costs, but rising lumber and labor gaps squeeze margins

Lennar has purchasing scale (2024 revenue $37.6B) and $9.5B land inventory, which give negotiating leverage, but volatile commodity prices (lumber +12% YoY in 2024 after a ~40% spike in 2020–21), labor shortages (~300,000 skilled workers gap in 2024) and concentrated suppliers raise supplier power and compress margins.

| Metric | 2024/2023 |

|---|---|

| Homebuilding rev | $37.6B (2024) |

| Land inventory | $9.5B (FY2024) |

| Lumber price change | +12% YoY (2024) |

| Skilled worker gap | ~300,000 (2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Lennar, evaluating supplier and buyer power, substitutes, rivalry intensity, and barriers that protect or threaten its market position.

A concise Porter's Five Forces one-sheet for Lennar—quickly assess supplier, buyer, entrant, substitute, and rivalry pressures to guide strategic and investment decisions.

Customers Bargaining Power

Sensitivity to Mortgage Interest Rates

Homebuyers are highly rate-sensitive: a 1 percentage-point mortgage rate rise cuts borrowing power by about 10% for the same payment, boosting customer bargaining power as buyers press for price cuts or seller-paid incentives.

When rates climbed from 3.0% in 2021 to ~6.9% peak in late 2022, Lennar saw demand pressure and increased concessions.

Lennar combats this with in-house mortgage LendLease-style services and rate buy-downs—in 2024 it reported mortgage incentives on roughly 30% of closings to keep sales moving.

Availability of Resale Home Inventory

The supply of resale homes directly benchmarks Lennar’s pricing power; when resale inventory rises, buyers push harder on new-build prices. In 2025 resale listings fell ~18% year-over-year nationally, per Redfin, tightening competition and letting Lennar raise community pricing in top metros. Higher resale supply in select Sun Belt pockets still forces localized concessions, so Lennar’s leverage varies by market.

Digital Transparency and Price Comparison

Modern buyers use platforms like Zillow and Redfin to compare floor plans, amenities, and pricing instantly, raising customer bargaining power; 78% of homebuyers reported online research shaped their choices in 2024, so Lennar must price competitively within micro-markets. Lennar counters with its Everything Is Included program, which cited a 9% higher closing rate in 2023 for homes marketed with bundled features, clarifying value versus piecemeal options.

Demand for Incentives and Customization

Buyers in Lennar’s move-up and luxury segments push for high-end finishes and personalization; in 2024 roughly 28% of Lennar’s orders were higher-margin Signature Series or upgrade-inclined, raising pressure for variety.

Lennar balances standardized high-quality builds and modular upgrade packages to protect construction efficiency while offering design-center credits and closing-cost assistance—in 2024 incentives averaged about $12,000 per home on promoted communities.

Economic Confidence and Job Market Stability

The job market and GDP growth drive buyer confidence for Lennar; US real GDP grew 2.4% in 2024 and unemployment averaged 3.9%, supporting demand for big-ticket homes.

When confidence falls, buyers delay purchases, forcing discounts or incentives—Lennar offered roughly 3–5% price concessions in soft markets 2023–2024.

Lennar’s mix—entry-level homes made up about 40% of 2024 deliveries—reduces sensitivity to high-end buyer pullback.

- US unemployment 2024: 3.9%

- US GDP growth 2024: 2.4%

- Lennar entry-level share 2024: ~40%

- Typical concessions in soft periods: 3–5%

Buyers Hold Leverage: Rates, Transparency Drive Incentives—Avg $12K; Resales Down

Buyers have strong leverage: rate sensitivity (1 ppt rise cuts borrowing ~10%) and online price transparency boost concessions; Lennar used mortgage incentives on ~30% of 2024 closings and averaged ~$12,000 incentives to sustain demand. Resale inventory down ~18% y/y in 2025 eased pricing in many metros, but local resale surges force concessions; entry-level share (~40% of 2024 deliveries) cushions downturns.

| Metric | Value |

|---|---|

| Mortgage sensitivity | 1 ppt → ~10% borrowing |

| Closings w/ incentives 2024 | ~30% |

| Avg incentive 2024 | $12,000 |

| Resale listings change 2025 | -18% y/y (Redfin) |

| Entry-level share 2024 | ~40% |

Same Document Delivered

Lennar Porter's Five Forces Analysis

This preview shows the exact Lennar Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the file is fully formatted and ready for use.

You're looking at the actual deliverable: the complete, professionally written document that will be available for instant download once you complete your purchase.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Lennar faces a mix of strong buyer power, moderate supplier leverage, and high rivalry as homebuilders compete on price, land access, and product differentiation, while regulatory hurdles and cyclical demand shape entry threats and substitutes.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lennar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in Raw Material Costs

Lennar depends on lumber, steel and concrete, commodities with volatile global prices; lumber futures rose ~40% in 2020–2021 and remained 12% higher year-over-year in 2024, pressuring input costs.

Scale gives Lennar bargaining power and volume discounts—2024 homebuilding revenue was $37.6B—yet sudden material spikes can compress gross margins if costs aren’t passed to buyers.

Management uses strategic sourcing, long‑term contracts and hedges to reduce exposure, but supplier-driven price hikes remain a recurring margin risk.

Shortage of Skilled Subcontractor Labor

The homebuilding sector faces a chronic shortage of skilled trades—electricians, plumbers, framers—driving subcontractor leverage during booms; the US had a 2024 shortage of roughly 300,000 construction-skilled workers per Associated Builders and Contractors.

Lennar relies on third-party subs rather than direct hires, so subs can demand higher rates; Lennar mitigates this by offering steady volume but still saw labor cost inflation add about 2–3 percentage points to gross margin pressure in 2023–2024.

Concentration of Key Product Vendors

For specialized items like appliances, HVAC, and smart-home kits Lennar relies on a handful of national vendors, creating supplier concentration that can trigger bottlenecks if a key supplier has production or logistics failures; for example, in 2023 US appliance lead times spiked 30% and Lennar reported supplier-related delays on ~4% of closings in FY2024. Lennar mitigates risk via long-term strategic alliances that secure priority allocation for its high-volume orders over smaller builders.

Land Seller Leverage in Prime Markets

Land in high-growth U.S. corridors is scarce, so sellers hold strong leverage; Lennar reported land purchase costs rising ~18% year-over-year in 2024, pressuring margins.

Lennar uses options and a strategic land bank—land owned for future development—to lock pipelines while deferring full capital outlay; at FY2024 it held roughly $9.5B in land and land development inventory.

As prime areas saturate, acquisition costs climb and compress project IRRs, forcing longer hold periods or higher home prices to preserve profitability.

- Land scarcity raises seller leverage

- 2024 land costs +18% YoY

- Lennar land inventory ~$9.5B (FY2024)

- Rising costs compress IRR, may increase home prices

Impact of Global Logistics and Tariffs

Suppliers of imported finished goods face shipping delays and trade-policy shifts; global container rates rose 38% in 2023 vs 2022, pressuring lead times and costs.

Tariffs—like U.S. levies that raised lumber and appliance import costs by up to 12–15% in recent cycles—often get passed to homebuilders as per-supplier markups.

Lennar tracks these geopolitical risks daily, adjusts procurement, and diversified 2024 sourcing to cut tariff exposure and keep component flow steady.

- 2023 container rates +38%

- Tariff-driven cost jumps ~12–15%

- Lennar increased sourcing diversity in 2024

Lennar's scale cushions costs, but rising lumber and labor gaps squeeze margins

Lennar has purchasing scale (2024 revenue $37.6B) and $9.5B land inventory, which give negotiating leverage, but volatile commodity prices (lumber +12% YoY in 2024 after a ~40% spike in 2020–21), labor shortages (~300,000 skilled workers gap in 2024) and concentrated suppliers raise supplier power and compress margins.

| Metric | 2024/2023 |

|---|---|

| Homebuilding rev | $37.6B (2024) |

| Land inventory | $9.5B (FY2024) |

| Lumber price change | +12% YoY (2024) |

| Skilled worker gap | ~300,000 (2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Lennar, evaluating supplier and buyer power, substitutes, rivalry intensity, and barriers that protect or threaten its market position.

A concise Porter's Five Forces one-sheet for Lennar—quickly assess supplier, buyer, entrant, substitute, and rivalry pressures to guide strategic and investment decisions.

Customers Bargaining Power

Sensitivity to Mortgage Interest Rates

Homebuyers are highly rate-sensitive: a 1 percentage-point mortgage rate rise cuts borrowing power by about 10% for the same payment, boosting customer bargaining power as buyers press for price cuts or seller-paid incentives.

When rates climbed from 3.0% in 2021 to ~6.9% peak in late 2022, Lennar saw demand pressure and increased concessions.

Lennar combats this with in-house mortgage LendLease-style services and rate buy-downs—in 2024 it reported mortgage incentives on roughly 30% of closings to keep sales moving.

Availability of Resale Home Inventory

The supply of resale homes directly benchmarks Lennar’s pricing power; when resale inventory rises, buyers push harder on new-build prices. In 2025 resale listings fell ~18% year-over-year nationally, per Redfin, tightening competition and letting Lennar raise community pricing in top metros. Higher resale supply in select Sun Belt pockets still forces localized concessions, so Lennar’s leverage varies by market.

Digital Transparency and Price Comparison

Modern buyers use platforms like Zillow and Redfin to compare floor plans, amenities, and pricing instantly, raising customer bargaining power; 78% of homebuyers reported online research shaped their choices in 2024, so Lennar must price competitively within micro-markets. Lennar counters with its Everything Is Included program, which cited a 9% higher closing rate in 2023 for homes marketed with bundled features, clarifying value versus piecemeal options.

Demand for Incentives and Customization

Buyers in Lennar’s move-up and luxury segments push for high-end finishes and personalization; in 2024 roughly 28% of Lennar’s orders were higher-margin Signature Series or upgrade-inclined, raising pressure for variety.

Lennar balances standardized high-quality builds and modular upgrade packages to protect construction efficiency while offering design-center credits and closing-cost assistance—in 2024 incentives averaged about $12,000 per home on promoted communities.

Economic Confidence and Job Market Stability

The job market and GDP growth drive buyer confidence for Lennar; US real GDP grew 2.4% in 2024 and unemployment averaged 3.9%, supporting demand for big-ticket homes.

When confidence falls, buyers delay purchases, forcing discounts or incentives—Lennar offered roughly 3–5% price concessions in soft markets 2023–2024.

Lennar’s mix—entry-level homes made up about 40% of 2024 deliveries—reduces sensitivity to high-end buyer pullback.

- US unemployment 2024: 3.9%

- US GDP growth 2024: 2.4%

- Lennar entry-level share 2024: ~40%

- Typical concessions in soft periods: 3–5%

Buyers Hold Leverage: Rates, Transparency Drive Incentives—Avg $12K; Resales Down

Buyers have strong leverage: rate sensitivity (1 ppt rise cuts borrowing ~10%) and online price transparency boost concessions; Lennar used mortgage incentives on ~30% of 2024 closings and averaged ~$12,000 incentives to sustain demand. Resale inventory down ~18% y/y in 2025 eased pricing in many metros, but local resale surges force concessions; entry-level share (~40% of 2024 deliveries) cushions downturns.

| Metric | Value |

|---|---|

| Mortgage sensitivity | 1 ppt → ~10% borrowing |

| Closings w/ incentives 2024 | ~30% |

| Avg incentive 2024 | $12,000 |

| Resale listings change 2025 | -18% y/y (Redfin) |

| Entry-level share 2024 | ~40% |

Same Document Delivered

Lennar Porter's Five Forces Analysis

This preview shows the exact Lennar Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the file is fully formatted and ready for use.

You're looking at the actual deliverable: the complete, professionally written document that will be available for instant download once you complete your purchase.