Lennar PESTLE Analysis

Skip the Research. Get the Strategy.

Understand how political shifts, housing demand cycles, and rising material costs are shaping Lennar’s strategy—our concise PESTLE highlights the external pressures and opportunities that matter most to investors and strategists. Dive deeper with the full PESTLE for actionable insights, modeled scenarios, and ready-to-use slides to support decision-making. Purchase now to get the complete, editable analysis instantly.

Political factors

Federal Housing Policy and Tax Incentives

Federal housing initiatives shape Lennar’s sales and planning: 2024 affordability programs and proposed first-time buyer credits elevated entry-level demand, supporting Lennar’s $22.4B 2024 home closings (FY).

Retention of the mortgage interest deduction sustains buyer purchasing power—mortgage deductibility affects a pool of ~65% of homeowners—critical for Lennar’s starter-home segment.

Shifts in federal emphasis between suburban expansion and urban density influence deployment of Lennar’s ~150,000 entitled lots and $8–10B land bank capital, redirecting build projects and land acquisitions.

Trade Policy and Material Tariffs

Lennar is highly sensitive to trade policy as tariffs on lumber, steel and aluminum can rapidly raise costs; US lumber tariffs rose intermittently through 2024–2025 with softwood duties on some Canadian imports adding up to roughly 9–17% tariffs at times, pushing builder input inflation beyond the industry’s 2024 material cost increase of about 6–8% year-over-year.

Government Sponsored Enterprise Reform

The stability and liquidity of the secondary mortgage market, underpinned by Fannie Mae and Freddie Mac which held about $5.1 trillion in mortgage-backed securities at end-2024, are critical for Lennar’s financial services; disruption could raise financing costs and tighten credit for buyers. Moves to privatize or tighten underwriting could reduce loan availability, affecting Lennar’s closings—Lennar reported $13.2 billion in mortgage origination volume in 2024. Changes to FHA and VA loan limits, which in 2025 have conforming limits up to $766,550 in high-cost areas, directly alter the eligible buyer pool for Lennar’s entry-level communities and could shift demand patterns.

Local Zoning and Land Use Regulations

Local municipal political climates directly affect Lennar’s ability to entitle land and commence construction; in 2024 zoning delays added an estimated 6–12 months on average in high-growth Sun Belt markets, raising holding costs by up to 8% per project.

Rising NIMBY sentiment has driven restrictive zoning and downzoning in parts of California and the Northeast, contributing to longer approval cycles and 5–10% higher development costs for affected projects in 2024–25.

By contrast, pro-growth local governments—notably in Texas and Florida—streamlined permitting in 2024, cutting approval times by roughly 20–30% and giving Lennar a competitive advantage in delivering inventory faster.

- Municipal zoning delays: +6–12 months; holding costs +8%

- NIMBY impact: development costs +5–10%

- Pro-growth regions: approval time −20–30%

Infrastructure Spending and Connectivity

Federal and state investments—like the Bipartisan Infrastructure Law’s $110B for roads and bridges and $65B for public transit (2021–2026 allocations)—directly affect the feasibility of Lennar’s peripheral suburban land by lowering travel times and increasing demand for housing near new access points.

Improved highway access and transit expansions can rapidly revalue distant parcels into residential hubs; studies show proximity to new transit can boost home prices 5–20% within 3–5 years.

Political commitment to grid modernization—$65B in grid and resiliency funding—reduces utility hookup delays and construction costs, enabling faster community build-out and lower operational risk for Lennar developments.

- Infrastructure funding scale: billions from federal/state programs

- Transit proximity price uplift: ~5–20% (3–5 years)

- Grid modernization funding: ~$65B improves hookup timelines

Lennar sails $22.4B closings amid tariff-driven inflation and zoning delays

Federal affordability programs and stable mortgage deductibility supported Lennar’s $22.4B home closings and $13.2B mortgage origination in 2024, while tariff-driven material inflation (6–8% in 2024; lumber duties intermittently 9–17%) and zoning delays (6–12 months; +8% holding costs) materially affect margins; pro-growth states cut approvals 20–30%, aiding faster deliveries.

| Metric | 2024/25 Value |

|---|---|

| Home closings | $22.4B |

| Mortgage originations | $13.2B |

| Material cost inflation | 6–8% |

| Lumber tariffs | 9–17% |

| Zoning delays | 6–12 months |

| Approval time reduction (pro-growth) | −20–30% |

What is included in the product

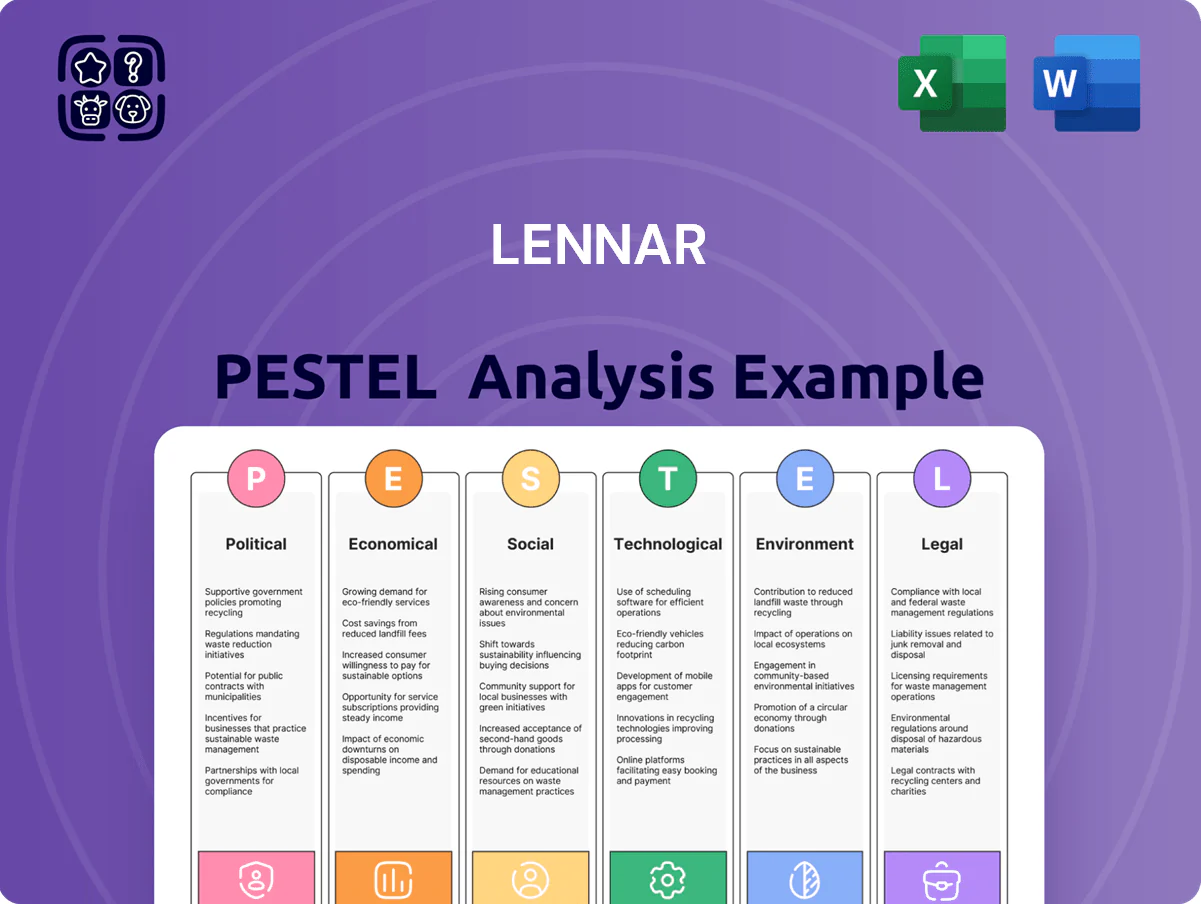

Explores how external macro-environmental factors uniquely affect Lennar across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify threats and opportunities for executives, investors, and strategists.

A concise, shareable Lennar PESTLE summary that’s visually segmented by category for quick interpretation and easily dropped into presentations or strategy packs to streamline risk discussions and team alignment.

Economic factors

Interest Rate Environment and Mortgage Affordability

The Federal Reserve’s policy remains the key economic driver for Lennar, with the fed funds rate peaking at 5.25–5.50% in 2023–24 and still elevated into 2025, directly raising mortgage costs and squeezing buyer affordability.

Higher rates pushed Lennar to increase mortgage rate buy-downs via Lennar Mortgage and Eagle Home Mortgage, adding hundreds to thousands in per‑unit incentives and pressuring gross margins.

As of late 2025, any stabilization or cut in rates is viewed as the main catalyst to sustain new home orders, given median 30‑yr mortgage rates near 6.7% in 2025 versus ~3% a few years earlier.

Labor Market Dynamics and Skilled Trade Shortages

Inflationary Pressures on Construction Inputs

Consumer Sentiment and Wealth Effects

Rising US equity markets and a 2024 median household net worth increase supported demand for Lennar’s luxury and move-up homes, as asset appreciation boosts buyer willingness to take on long-term mortgages and pay for premium upgrades.

By contrast, 2024–2025 cooling in services payroll growth and tighter credit drove higher cancellations and shifted some buyers toward Lennar’s entry-level and affordable product lines.

- 2024 S&P 500 up ~20% from 2022 trough, raising household wealth

- Mortgage rates ~6–7% in 2024—dampening affordability

- Higher cancellations correlated with slower payroll gains in late 2024

Regional Economic Disparities

Lennar’s heavy concentration in Sunbelt states—Florida, Texas and Arizona—ties revenue to these regions’ economic health; Sunbelt markets accounted for roughly 60% of Lennar’s homebuilding deliveries in 2024.

Corporate relocations and strong job growth (Sunbelt metro payrolls grew ~2.5–3.5% YoY in 2024) have supported new-home demand and pricing resilience.

Localized downturns—energy shocks, state tax changes, or high mortgage rates—would disproportionately hit Lennar vs. geographically diversified peers, amplifying revenue volatility.

- ~60% of deliveries in Sunbelt (2024)

- Sunbelt payroll growth ~2.5–3.5% YoY (2024)

- Higher regional revenue concentration increases downside risk

High rates, rising construction costs squeeze housing affordability as Sunbelt leads deliveries

Fed rates peaked 5.25–5.50% (2023–24); 30‑yr mortgage ~6.7% (2025) hurting affordability; construction wages +6% YoY (2024) and subcontractor costs +8% (2024–25) raise unit costs; Sunbelt = ~60% deliveries (2024), payrolls +2.5–3.5% YoY (2024); 2024 gross margin 22.4%; CPI 3.4% YoY Apr 2025; housing demand sensitive to rate cuts.

| Metric | Value |

|---|---|

| 30‑yr mortgage | ~6.7% (2025) |

| Fed funds peak | 5.25–5.50% (2023–24) |

| Gross margin | 22.4% (2024) |

| Sunbelt deliveries | ~60% (2024) |

| Construction wages | +6% YoY (2024) |

Full Version Awaits

Lennar PESTLE Analysis

The preview shown here is the exact Lennar PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Understand how political shifts, housing demand cycles, and rising material costs are shaping Lennar’s strategy—our concise PESTLE highlights the external pressures and opportunities that matter most to investors and strategists. Dive deeper with the full PESTLE for actionable insights, modeled scenarios, and ready-to-use slides to support decision-making. Purchase now to get the complete, editable analysis instantly.

Political factors

Federal Housing Policy and Tax Incentives

Federal housing initiatives shape Lennar’s sales and planning: 2024 affordability programs and proposed first-time buyer credits elevated entry-level demand, supporting Lennar’s $22.4B 2024 home closings (FY).

Retention of the mortgage interest deduction sustains buyer purchasing power—mortgage deductibility affects a pool of ~65% of homeowners—critical for Lennar’s starter-home segment.

Shifts in federal emphasis between suburban expansion and urban density influence deployment of Lennar’s ~150,000 entitled lots and $8–10B land bank capital, redirecting build projects and land acquisitions.

Trade Policy and Material Tariffs

Lennar is highly sensitive to trade policy as tariffs on lumber, steel and aluminum can rapidly raise costs; US lumber tariffs rose intermittently through 2024–2025 with softwood duties on some Canadian imports adding up to roughly 9–17% tariffs at times, pushing builder input inflation beyond the industry’s 2024 material cost increase of about 6–8% year-over-year.

Government Sponsored Enterprise Reform

The stability and liquidity of the secondary mortgage market, underpinned by Fannie Mae and Freddie Mac which held about $5.1 trillion in mortgage-backed securities at end-2024, are critical for Lennar’s financial services; disruption could raise financing costs and tighten credit for buyers. Moves to privatize or tighten underwriting could reduce loan availability, affecting Lennar’s closings—Lennar reported $13.2 billion in mortgage origination volume in 2024. Changes to FHA and VA loan limits, which in 2025 have conforming limits up to $766,550 in high-cost areas, directly alter the eligible buyer pool for Lennar’s entry-level communities and could shift demand patterns.

Local Zoning and Land Use Regulations

Local municipal political climates directly affect Lennar’s ability to entitle land and commence construction; in 2024 zoning delays added an estimated 6–12 months on average in high-growth Sun Belt markets, raising holding costs by up to 8% per project.

Rising NIMBY sentiment has driven restrictive zoning and downzoning in parts of California and the Northeast, contributing to longer approval cycles and 5–10% higher development costs for affected projects in 2024–25.

By contrast, pro-growth local governments—notably in Texas and Florida—streamlined permitting in 2024, cutting approval times by roughly 20–30% and giving Lennar a competitive advantage in delivering inventory faster.

- Municipal zoning delays: +6–12 months; holding costs +8%

- NIMBY impact: development costs +5–10%

- Pro-growth regions: approval time −20–30%

Infrastructure Spending and Connectivity

Federal and state investments—like the Bipartisan Infrastructure Law’s $110B for roads and bridges and $65B for public transit (2021–2026 allocations)—directly affect the feasibility of Lennar’s peripheral suburban land by lowering travel times and increasing demand for housing near new access points.

Improved highway access and transit expansions can rapidly revalue distant parcels into residential hubs; studies show proximity to new transit can boost home prices 5–20% within 3–5 years.

Political commitment to grid modernization—$65B in grid and resiliency funding—reduces utility hookup delays and construction costs, enabling faster community build-out and lower operational risk for Lennar developments.

- Infrastructure funding scale: billions from federal/state programs

- Transit proximity price uplift: ~5–20% (3–5 years)

- Grid modernization funding: ~$65B improves hookup timelines

Lennar sails $22.4B closings amid tariff-driven inflation and zoning delays

Federal affordability programs and stable mortgage deductibility supported Lennar’s $22.4B home closings and $13.2B mortgage origination in 2024, while tariff-driven material inflation (6–8% in 2024; lumber duties intermittently 9–17%) and zoning delays (6–12 months; +8% holding costs) materially affect margins; pro-growth states cut approvals 20–30%, aiding faster deliveries.

| Metric | 2024/25 Value |

|---|---|

| Home closings | $22.4B |

| Mortgage originations | $13.2B |

| Material cost inflation | 6–8% |

| Lumber tariffs | 9–17% |

| Zoning delays | 6–12 months |

| Approval time reduction (pro-growth) | −20–30% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Lennar across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify threats and opportunities for executives, investors, and strategists.

A concise, shareable Lennar PESTLE summary that’s visually segmented by category for quick interpretation and easily dropped into presentations or strategy packs to streamline risk discussions and team alignment.

Economic factors

Interest Rate Environment and Mortgage Affordability

The Federal Reserve’s policy remains the key economic driver for Lennar, with the fed funds rate peaking at 5.25–5.50% in 2023–24 and still elevated into 2025, directly raising mortgage costs and squeezing buyer affordability.

Higher rates pushed Lennar to increase mortgage rate buy-downs via Lennar Mortgage and Eagle Home Mortgage, adding hundreds to thousands in per‑unit incentives and pressuring gross margins.

As of late 2025, any stabilization or cut in rates is viewed as the main catalyst to sustain new home orders, given median 30‑yr mortgage rates near 6.7% in 2025 versus ~3% a few years earlier.

Labor Market Dynamics and Skilled Trade Shortages

Inflationary Pressures on Construction Inputs

Consumer Sentiment and Wealth Effects

Rising US equity markets and a 2024 median household net worth increase supported demand for Lennar’s luxury and move-up homes, as asset appreciation boosts buyer willingness to take on long-term mortgages and pay for premium upgrades.

By contrast, 2024–2025 cooling in services payroll growth and tighter credit drove higher cancellations and shifted some buyers toward Lennar’s entry-level and affordable product lines.

- 2024 S&P 500 up ~20% from 2022 trough, raising household wealth

- Mortgage rates ~6–7% in 2024—dampening affordability

- Higher cancellations correlated with slower payroll gains in late 2024

Regional Economic Disparities

Lennar’s heavy concentration in Sunbelt states—Florida, Texas and Arizona—ties revenue to these regions’ economic health; Sunbelt markets accounted for roughly 60% of Lennar’s homebuilding deliveries in 2024.

Corporate relocations and strong job growth (Sunbelt metro payrolls grew ~2.5–3.5% YoY in 2024) have supported new-home demand and pricing resilience.

Localized downturns—energy shocks, state tax changes, or high mortgage rates—would disproportionately hit Lennar vs. geographically diversified peers, amplifying revenue volatility.

- ~60% of deliveries in Sunbelt (2024)

- Sunbelt payroll growth ~2.5–3.5% YoY (2024)

- Higher regional revenue concentration increases downside risk

High rates, rising construction costs squeeze housing affordability as Sunbelt leads deliveries

Fed rates peaked 5.25–5.50% (2023–24); 30‑yr mortgage ~6.7% (2025) hurting affordability; construction wages +6% YoY (2024) and subcontractor costs +8% (2024–25) raise unit costs; Sunbelt = ~60% deliveries (2024), payrolls +2.5–3.5% YoY (2024); 2024 gross margin 22.4%; CPI 3.4% YoY Apr 2025; housing demand sensitive to rate cuts.

| Metric | Value |

|---|---|

| 30‑yr mortgage | ~6.7% (2025) |

| Fed funds peak | 5.25–5.50% (2023–24) |

| Gross margin | 22.4% (2024) |

| Sunbelt deliveries | ~60% (2024) |

| Construction wages | +6% YoY (2024) |

Full Version Awaits

Lennar PESTLE Analysis

The preview shown here is the exact Lennar PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.