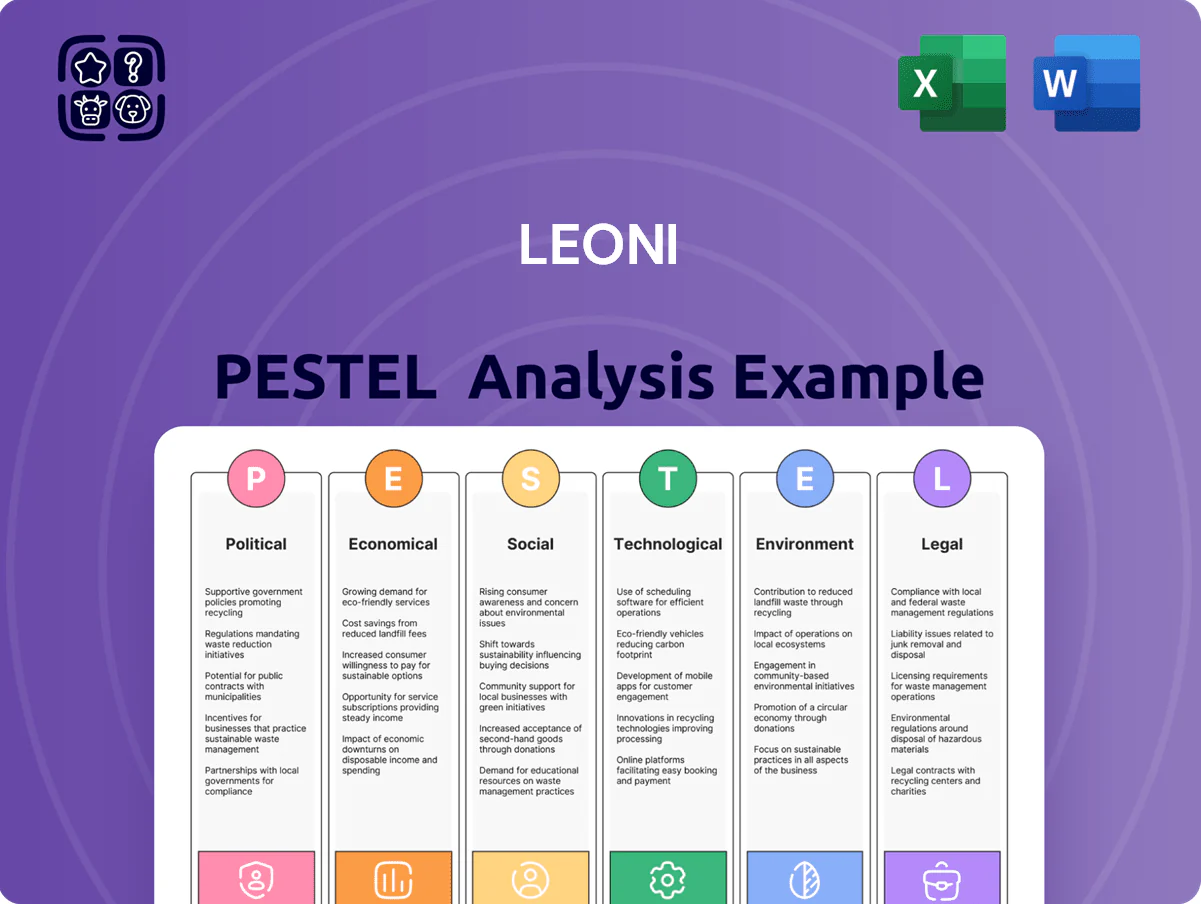

LEONI PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, supply-chain dynamics, and rapid electrification are reshaping LEONI’s prospects—our concise PESTLE highlights the external forces that matter and where risks and opportunities lie; buy the full analysis for a complete, ready-to-use report to inform investment decisions and strategic plans.

Political factors

Geopolitical Supply Chain Stability

Geopolitical tensions in Eastern Europe and US-China trade friction force LEONI to prioritize supply chain resilience; in 2024 the company reported 55% of revenues tied to automotive OEMs, heightening sensitivity to disruptions.

With production sites across Europe, North Africa, and Asia, even short border closures can delay deliveries and cost millions—LEONI faced a €120m supply-chain impact in FY2023, underscoring the need for flexible logistics.

Management must sustain diversified manufacturing hubs and dynamic routing; maintaining buffer inventories and dual-sourcing helped reduce lead-time volatility by 18% in 2024.

Trade Protectionism and Tariffs

Tariffs on EVs and components between blocs like the EU, US and China—which imposed tariffs rising to 25% on certain auto parts in 2024—raise LEONI's input costs and can cut gross margins by several percentage points on exported harnesses.

Rising national subsidies for domestic EV supply chains (EU Net-Zero Industry Act allocations €50+bn, US CHIPS/IRA incentives) increase local content rules, forcing LEONI to meet country-specific thresholds to qualify for customers' incentives.

This political mix compels LEONI to reassess plant placement for high-value assembly—shifting capacity to low-tariff jurisdictions or near OEMs to avoid punitive duties and protect 2024–25 revenue streams.

European Industrial Policy

The European Green Deal and 2023 Net-Zero Industry Act push demand for high-voltage EV cables, benefiting LEONI, whose automotive segment generated 2.1 billion EUR in 2024; policy timelines create compliance costs and milestones tied to CO2 targets and battery supply rules.

Labor Relations and Union Power

Political climates in Germany and North Africa shape LEONI’s labor costs via strict German co-determination laws and rising North African wage pressures; Germany’s manufacturing wage growth was ~3.5% in 2024 while Tunisia/Morocco saw 4–6% increases. LEONI monitors collective bargaining and minimum wage shifts to control personnel expenses and maintains dialogue with policymakers to support competitiveness and job stability.

- Germany: 3.5% manufacturing wage growth (2024)

- North Africa: 4–6% wage increases (2024)

- Active engagement with policymakers to manage labor risk

Global Standardization Efforts

Political cooperation in bodies like the IEA and IEC to standardize EV charging and data protocols reduces fragmentation, allowing LEONI to target a consolidated market; IEC SC23 reports 12% fewer connector variants since 2022, aiding component commonality.

As governments in the EU and UK push unified standards (EU mandate proposal 2024), LEONI can streamline R&D and cut development cycles, potentially lowering R&D intensity from ~6% revenue toward 5%.

However, US–EU–China divergence persists: in 2025 China accounted for 40% of global EV production, forcing LEONI to retain multi-standard lines, raising manufacturing overheads and capex by an estimated 3–5%.

- Standardization lowers product fragmentation and R&D scope

- EU policy moves enable focused portfolio and potential R&D cost reduction

- US/EU/China divergence forces costly multi-standard production, adding ~3–5% capex/overhead

LEONI faces reshoring, wage pressure and 3–5% higher capex as auto exposure amplifies risk

Geopolitical tensions, tariffs and local-content rules in 2024–25 force LEONI to diversify production, increasing logistics and capex by ~3–5%; automotive (55% revenue) and €2.1bn 2024 segment exposure heighten sensitivity. Wage inflation (Germany +3.5%, North Africa +4–6% in 2024) and subsidy-driven reshoring (EU €50bn+, US IRA) reshape plant siting and margin pressure. Standards alignment (IEC: −12% connector variants) can cut R&D intensity toward 5% from ~6%.

| Metric | 2024/25 |

|---|---|

| Automotive revenue share | 55% |

| Automotive revenue | €2.1bn |

| Supply‑chain hit FY2023 | €120m |

| Wage growth Germany | 3.5% |

| Wage growth N.Africa | 4–6% |

| Capex/overhead from multi‑standard | +3–5% |

| IEC connector variants change | −12% |

What is included in the product

Explores how macro-environmental factors specifically affect LEONI across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to inform strategy and risk management.

Summarizes LEONI's PESTLE insights in a compact, shareable format for quick reference in meetings or decks, with clear PESTLE segmentation to streamline risk discussions and strategic alignment across teams.

Economic factors

Raw Material Price Volatility

Raw material price volatility, especially copper, remains a key cost driver for LEONI—copper and conductive materials accounted for roughly 25–30% of COGS in 2024, making margins sensitive to commodity swings.

Between 2023–2025 copper averaged around 9,000–10,000 USD/tonne with peaks from energy-transition demand causing potential margin compression if not hedged or passed through.

LEONI employs advanced procurement, hedging and contractual price adjustment clauses; in 2024 these measures helped limit input-cost exposure to under 5% of EBIT volatility versus unhedged scenarios.

Restructuring and Financial Health

Following 2023–2024 restructuring and privatization, LEONI focuses on deleveraging and liquidity: net debt fell to about EUR 1.1bn by Q3 2025 from EUR 1.6bn in 2022, prioritizing covenant compliance and working capital efficiency.

With ECB rates near 3.75% in 2025, interest expense sensitivity affects funding for capex—LEONI’s planned 2025–26 capex of ~EUR 200–250m depends on affordable borrowing and refinancing.

Analysts track operating cash flow stability; trailing 12-month free cash flow turned positive in H1 2025 (~EUR 40m), a key metric for restoring market and credit insurer confidence.

Automotive Market Cycles

LEONI’s revenue remains highly sensitive to automotive cycles; global light-vehicle production fell about 2% to ~79.6 million units in 2024, pressuring cable-system demand and OEM orders.

Economic downturns and weaker consumer spending compress margins as plant utilization dipped—LEONI reported adjusted capacity utilization near 72% in FY 2024.

To reduce exposure, LEONI is expanding into commercial vehicle and industrial segments, which accounted for roughly 28% of sales in 2024, aiming to stabilize revenue against passenger-car volatility.

Inflationary Cost Pressures

Persistent inflation in energy (+18% year-on-year in 2024 EU industrial power costs) and logistics (global container rates +12% in 2024) pressures LEONI’s margins, forcing tight cost-saving programs and operational-excellence drives to protect EBITDA.

Management targets non-raw input reductions via productivity gains, headcount and process optimization, and intensified supplier price negotiations to preserve competitive pricing for complex wiring systems.

- Energy costs +18% YoY (EU industrial, 2024)

- Global container rates +12% (2024)

- Focus: productivity, supplier renegotiation, cost programs

Currency Exchange Risk

As a global supplier, LEONI faces material currency translation and transaction exposure: in 2025 roughly 40% of revenues were outside the Eurozone, making EUR/USD and EUR/CNY swings key drivers of reported EBIT volatility.

The company uses forwards, options and netting and aims to align cost base with revenue currency; in 2024 hedge coverage reportedly exceeded 60% of short-term FX exposure to smooth P&L effects.

- ~40% revenues outside Eurozone (2025)

- EUR/USD and EUR/CNY volatility materially affects reported earnings

- Hedge instruments: forwards, options, netting; >60% short-term coverage (2024)

- Currency-matching of costs and revenues to preserve export competitiveness

Margin risk from copper, energy & logistics; net debt cut to ~€1.1bn, FCF improving

Raw-materials (copper ~25–30% of COGS) and energy/logistics inflation (+18% EU industrial power, +12% container rates in 2024) drive margin risk; copper averaged USD9–10k/t (2023–25). Net debt reduced to ~EUR1.1bn by Q3 2025; FCF ~EUR40m H1 2025. ~40% revenues non‑EUR; FX hedges >60% (2024).

| Metric | Value |

|---|---|

| Copper | USD9–10k/t (2023–25) |

| Copper share COGS | 25–30% |

| Energy rise (EU) | +18% (2024) |

| Container rates | +12% (2024) |

| Net debt | ~EUR1.1bn (Q3 2025) |

| FCF | ~EUR40m (H1 2025) |

| Non‑EUR revenue | ~40% (2025) |

| FX hedge coverage | >60% (2024) |

Same Document Delivered

LEONI PESTLE Analysis

The preview shown here is the exact LEONI PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, supply-chain dynamics, and rapid electrification are reshaping LEONI’s prospects—our concise PESTLE highlights the external forces that matter and where risks and opportunities lie; buy the full analysis for a complete, ready-to-use report to inform investment decisions and strategic plans.

Political factors

Geopolitical Supply Chain Stability

Geopolitical tensions in Eastern Europe and US-China trade friction force LEONI to prioritize supply chain resilience; in 2024 the company reported 55% of revenues tied to automotive OEMs, heightening sensitivity to disruptions.

With production sites across Europe, North Africa, and Asia, even short border closures can delay deliveries and cost millions—LEONI faced a €120m supply-chain impact in FY2023, underscoring the need for flexible logistics.

Management must sustain diversified manufacturing hubs and dynamic routing; maintaining buffer inventories and dual-sourcing helped reduce lead-time volatility by 18% in 2024.

Trade Protectionism and Tariffs

Tariffs on EVs and components between blocs like the EU, US and China—which imposed tariffs rising to 25% on certain auto parts in 2024—raise LEONI's input costs and can cut gross margins by several percentage points on exported harnesses.

Rising national subsidies for domestic EV supply chains (EU Net-Zero Industry Act allocations €50+bn, US CHIPS/IRA incentives) increase local content rules, forcing LEONI to meet country-specific thresholds to qualify for customers' incentives.

This political mix compels LEONI to reassess plant placement for high-value assembly—shifting capacity to low-tariff jurisdictions or near OEMs to avoid punitive duties and protect 2024–25 revenue streams.

European Industrial Policy

The European Green Deal and 2023 Net-Zero Industry Act push demand for high-voltage EV cables, benefiting LEONI, whose automotive segment generated 2.1 billion EUR in 2024; policy timelines create compliance costs and milestones tied to CO2 targets and battery supply rules.

Labor Relations and Union Power

Political climates in Germany and North Africa shape LEONI’s labor costs via strict German co-determination laws and rising North African wage pressures; Germany’s manufacturing wage growth was ~3.5% in 2024 while Tunisia/Morocco saw 4–6% increases. LEONI monitors collective bargaining and minimum wage shifts to control personnel expenses and maintains dialogue with policymakers to support competitiveness and job stability.

- Germany: 3.5% manufacturing wage growth (2024)

- North Africa: 4–6% wage increases (2024)

- Active engagement with policymakers to manage labor risk

Global Standardization Efforts

Political cooperation in bodies like the IEA and IEC to standardize EV charging and data protocols reduces fragmentation, allowing LEONI to target a consolidated market; IEC SC23 reports 12% fewer connector variants since 2022, aiding component commonality.

As governments in the EU and UK push unified standards (EU mandate proposal 2024), LEONI can streamline R&D and cut development cycles, potentially lowering R&D intensity from ~6% revenue toward 5%.

However, US–EU–China divergence persists: in 2025 China accounted for 40% of global EV production, forcing LEONI to retain multi-standard lines, raising manufacturing overheads and capex by an estimated 3–5%.

- Standardization lowers product fragmentation and R&D scope

- EU policy moves enable focused portfolio and potential R&D cost reduction

- US/EU/China divergence forces costly multi-standard production, adding ~3–5% capex/overhead

LEONI faces reshoring, wage pressure and 3–5% higher capex as auto exposure amplifies risk

Geopolitical tensions, tariffs and local-content rules in 2024–25 force LEONI to diversify production, increasing logistics and capex by ~3–5%; automotive (55% revenue) and €2.1bn 2024 segment exposure heighten sensitivity. Wage inflation (Germany +3.5%, North Africa +4–6% in 2024) and subsidy-driven reshoring (EU €50bn+, US IRA) reshape plant siting and margin pressure. Standards alignment (IEC: −12% connector variants) can cut R&D intensity toward 5% from ~6%.

| Metric | 2024/25 |

|---|---|

| Automotive revenue share | 55% |

| Automotive revenue | €2.1bn |

| Supply‑chain hit FY2023 | €120m |

| Wage growth Germany | 3.5% |

| Wage growth N.Africa | 4–6% |

| Capex/overhead from multi‑standard | +3–5% |

| IEC connector variants change | −12% |

What is included in the product

Explores how macro-environmental factors specifically affect LEONI across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to inform strategy and risk management.

Summarizes LEONI's PESTLE insights in a compact, shareable format for quick reference in meetings or decks, with clear PESTLE segmentation to streamline risk discussions and strategic alignment across teams.

Economic factors

Raw Material Price Volatility

Raw material price volatility, especially copper, remains a key cost driver for LEONI—copper and conductive materials accounted for roughly 25–30% of COGS in 2024, making margins sensitive to commodity swings.

Between 2023–2025 copper averaged around 9,000–10,000 USD/tonne with peaks from energy-transition demand causing potential margin compression if not hedged or passed through.

LEONI employs advanced procurement, hedging and contractual price adjustment clauses; in 2024 these measures helped limit input-cost exposure to under 5% of EBIT volatility versus unhedged scenarios.

Restructuring and Financial Health

Following 2023–2024 restructuring and privatization, LEONI focuses on deleveraging and liquidity: net debt fell to about EUR 1.1bn by Q3 2025 from EUR 1.6bn in 2022, prioritizing covenant compliance and working capital efficiency.

With ECB rates near 3.75% in 2025, interest expense sensitivity affects funding for capex—LEONI’s planned 2025–26 capex of ~EUR 200–250m depends on affordable borrowing and refinancing.

Analysts track operating cash flow stability; trailing 12-month free cash flow turned positive in H1 2025 (~EUR 40m), a key metric for restoring market and credit insurer confidence.

Automotive Market Cycles

LEONI’s revenue remains highly sensitive to automotive cycles; global light-vehicle production fell about 2% to ~79.6 million units in 2024, pressuring cable-system demand and OEM orders.

Economic downturns and weaker consumer spending compress margins as plant utilization dipped—LEONI reported adjusted capacity utilization near 72% in FY 2024.

To reduce exposure, LEONI is expanding into commercial vehicle and industrial segments, which accounted for roughly 28% of sales in 2024, aiming to stabilize revenue against passenger-car volatility.

Inflationary Cost Pressures

Persistent inflation in energy (+18% year-on-year in 2024 EU industrial power costs) and logistics (global container rates +12% in 2024) pressures LEONI’s margins, forcing tight cost-saving programs and operational-excellence drives to protect EBITDA.

Management targets non-raw input reductions via productivity gains, headcount and process optimization, and intensified supplier price negotiations to preserve competitive pricing for complex wiring systems.

- Energy costs +18% YoY (EU industrial, 2024)

- Global container rates +12% (2024)

- Focus: productivity, supplier renegotiation, cost programs

Currency Exchange Risk

As a global supplier, LEONI faces material currency translation and transaction exposure: in 2025 roughly 40% of revenues were outside the Eurozone, making EUR/USD and EUR/CNY swings key drivers of reported EBIT volatility.

The company uses forwards, options and netting and aims to align cost base with revenue currency; in 2024 hedge coverage reportedly exceeded 60% of short-term FX exposure to smooth P&L effects.

- ~40% revenues outside Eurozone (2025)

- EUR/USD and EUR/CNY volatility materially affects reported earnings

- Hedge instruments: forwards, options, netting; >60% short-term coverage (2024)

- Currency-matching of costs and revenues to preserve export competitiveness

Margin risk from copper, energy & logistics; net debt cut to ~€1.1bn, FCF improving

Raw-materials (copper ~25–30% of COGS) and energy/logistics inflation (+18% EU industrial power, +12% container rates in 2024) drive margin risk; copper averaged USD9–10k/t (2023–25). Net debt reduced to ~EUR1.1bn by Q3 2025; FCF ~EUR40m H1 2025. ~40% revenues non‑EUR; FX hedges >60% (2024).

| Metric | Value |

|---|---|

| Copper | USD9–10k/t (2023–25) |

| Copper share COGS | 25–30% |

| Energy rise (EU) | +18% (2024) |

| Container rates | +12% (2024) |

| Net debt | ~EUR1.1bn (Q3 2025) |

| FCF | ~EUR40m (H1 2025) |

| Non‑EUR revenue | ~40% (2025) |

| FX hedge coverage | >60% (2024) |

Same Document Delivered

LEONI PESTLE Analysis

The preview shown here is the exact LEONI PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or surprises.