Lepu Medical Technology (Beijing) Co. Porter's Five Forces Analysis

Don't Miss the Bigger Picture

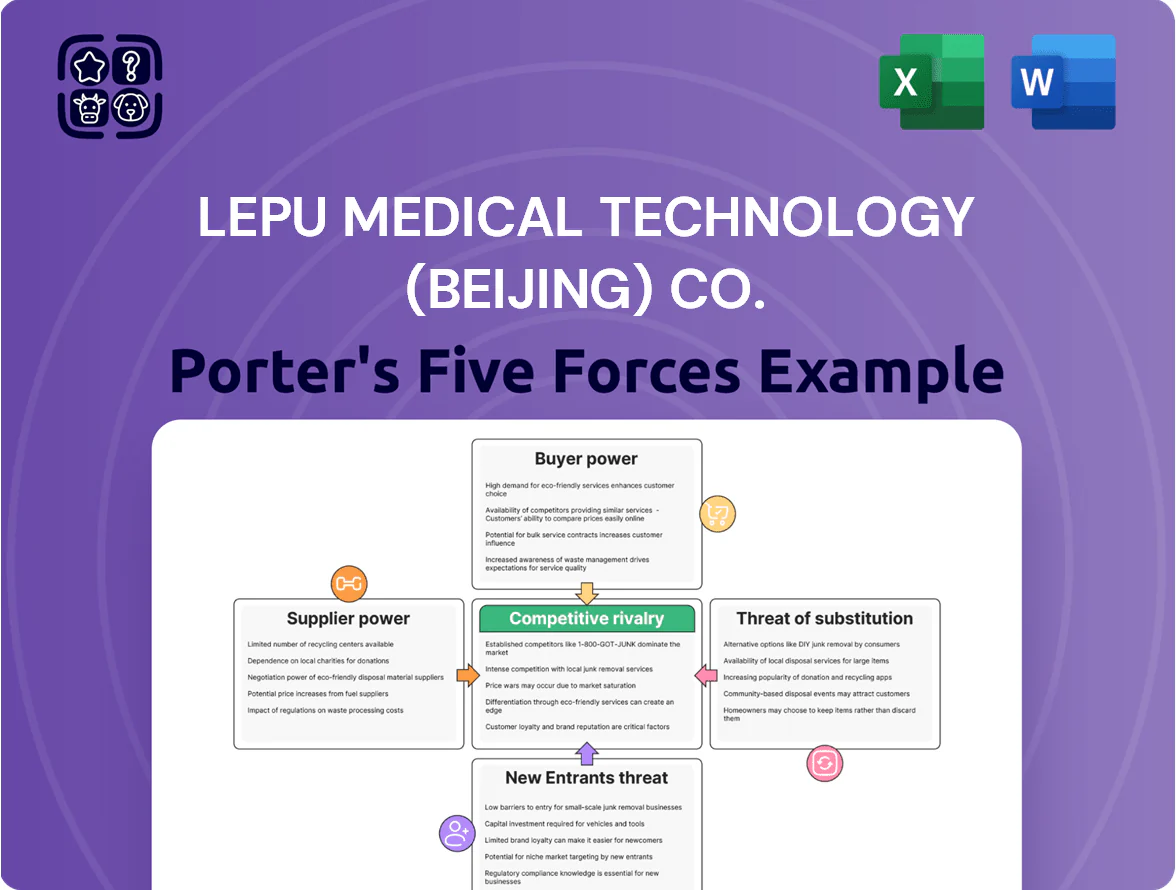

Lepu Medical faces moderate supplier power and intense rivalry from established device makers, while regulatory barriers and differentiated tech limit new entrants and substitution risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lepu Medical Technology (Beijing) Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Requirements

The production of Lepu Medical’s cardiovascular stents and pacemakers needs high-purity medical-grade metals and specialized polymers that meet strict biocompatibility and ISO 13485/CE/FDA-related standards; only about 10–15 global suppliers meet these specs, giving suppliers moderate bargaining power.

Lepu limits risk via multi-year contracts and supplier diversification across China, Europe, and South Korea; as of FY2024 Lepu sourced ~40% of key alloys domestically and kept strategic inventories covering 3–4 months of production.

Vertical Integration Capabilities

Lepu Medical has pushed vertical integration, producing core components and reagents in-house—by 2024 its internal production covered about 60% of stent inputs and 45% of in‑vitro diagnostic reagents, cutting third‑party spend and COGS volatility. This capability reduced supplier dependency and limited exposure to vendor price hikes, helping gross margin stability (2024 gross margin 35.2%). During 2020–2023 logistics shocks, internal output sustained production with inventory days falling to 78 in 2024, improving reliability.

High Switching Costs for Regulated Inputs

Switching suppliers in medical devices is costly: re-validation and regulatory filings can take 6–24+ months and cost $0.5–5M per product change, so Lepu must prove safety to regulators for any critical-component swap.

That delay raises supplier power, but large buyers like Lepu (2024 revenue RMB 5.8B) keep suppliers tied to long-term contracts, so suppliers are incentivized to preserve stable relationships.

Technological Proprietary Components

Lepu Medical depends on specialized semiconductor and sensor makers for pacemakers and digital monitors; these parts are often proprietary so Lepu has few substitutes if a supplier stops, raising supply risk.

Because these tech suppliers serve niche markets with high R&D barriers, they command higher pricing power than commodity vendors; in 2024 global medical sensor shortages pushed lead times from 12 to 28 weeks for some parts.

- High dependency on proprietary chips

- Limited alternate suppliers = higher risk

- 2024 lead times rose 12→28 weeks for some sensors

Impact of Global Commodity Fluctuations

The cost of petroleum-based plastics and precious metals (gold, platinum) used in Lepu Medical Technology surgical devices is driven by global markets; gold rose ~8% in 2024 and petrochemical feedstock Brent-linked PVC input volatility reached +/-15% y/y, making Lepu a price taker despite scale, pressuring gross margins (2024 gross margin 34.2%).

To blunt spikes, Lepu uses strategic stockpiling and advanced procurement planning—inventory days rose to 96 in FY2024 from 82 in FY2022—reducing quarterly margin swings by an estimated 120–180 basis points per event.

- Lepu gross margin 34.2% (2024)

- Inventory days 96 (FY2024)

- Commodity volatility: petrochemical +/-15% y/y

- Estimated margin relief 120–180 bps per spike

Moderate supplier power; Lepu boosts resilience with 60% in‑house stents, 34–35% GM

Suppliers hold moderate power: few global medical‑grade metal/polymer and proprietary sensor suppliers (10–15), long validation (6–24+ months, $0.5–5M) raises switching costs, but Lepu reduced exposure via 60% in‑house stent input, 45% IVD reagents, multi‑year contracts, 3–4 months strategic stock, 2024 revenue RMB 5.8B and gross margin ~34–35%.

| Metric | 2024 |

|---|---|

| Key suppliers | 10–15 |

| In‑house stent inputs | 60% |

| IVD reagents in‑house | 45% |

| Inventory | 3–4 months (96 days) |

| Revenue | RMB 5.8B |

| Gross margin | 34–35% |

What is included in the product

Tailored Porter's Five Forces for Lepu Medical Technology (Beijing) Co.: uncovers competitive intensity, buyer/supplier power, threat of substitutes and new entrants, and identifies disruptive trends and regulatory barriers shaping its profitability and strategic positioning.

A concise Porter's Five Forces snapshot for Lepu Medical Technology (Beijing) that highlights regulatory and supplier pressures, competitive intensity from established device makers, moderate buyer power, and barriers for new entrants—ready to paste into decks or executive summaries.

Customers Bargaining Power

Centralized Government Procurement Power

The Chinese government wields strong bargaining power via Volume-Based Procurement (VBP), which in 2024 covered stents and other high-value consumables and cut prices by 30–70% in pilot rounds; Lepu Medical faced contract wins with single-digit margins after a 2021–24 VBP expansion.

Hospital Concentration and Group Purchasing

Large public hospital networks and private chains in China accounted for roughly 45% of national procurement spend in 2024, letting them demand bundled offerings from Lepu Medical Technology (Beijing) Co., including training, maintenance, and integrated digital systems rather than standalone devices.

As hospital groups scale, their pooled purchasing power increases price negotiation leverage and they routinely pit manufacturers against each other, pressuring Lepu on margins and after-sales service terms.

Price Transparency and Digital Platforms

Price transparency from digital procurement platforms and expanded public disclosure in China has compressed margins for Lepu Medical Technology (Beijing) Co.; 2024 hospital tender data show median device price spreads fell ~18% vs 2019, limiting Lepu’s ability to command premiums on legacy devices.

Buyers can now benchmark Lepu against dozens of domestic rivals and multinational firms in minutes, driving commoditization and higher price sensitivity—Lepu’s fiscal 2024 gross margin of 39.2% reflects this pressure.

Low Switching Costs for Standardized Products

Patient Influence in Private Healthcare

In China’s private healthcare market, growing patient and physician brand awareness—survey: 62% of urban patients in 2024 recognize medtech brands—gives individuals more say in non-reimbursable device choice, pushing Lepu to invest in brand equity and peer-reviewed clinical data.

Still, payers and hospitals control ~70–80% of device procurement via insurance formularies and tenders, so ultimate bargaining power remains with institutional buyers; Lepu must balance direct-to-consumer reputation with tender competitiveness.

- 62% urban patient brand recognition (2024 survey)

- Payers/hospitals control ~70–80% device procurement

- Action: fund clinical trials, KOL programs, patient-facing marketing

VBP cuts slash stent prices 30–70% — Lepu margins squeezed as hospitals control procurement

Buyers hold high bargaining power: 2024 VBP cut stent/consumable prices 30–70%, Lepu faced single-digit margins; hospital networks = ~45% procurement spend; median tender price spreads down ~18% vs 2019; Lepu FY2024 gross margin 39.2%; consumables revenue CN¥1.2–1.5b exposed; patient brand awareness 62% but hospitals/payers control ~70–80% purchases.

| Metric | 2024 |

|---|---|

| VBP price cuts | 30–70% |

| Hospital share | ~45% |

| Price spread vs 2019 | -18% |

| Gross margin | 39.2% |

| Consumables rev | CN¥1.2–1.5b |

| Patient brand awareness | 62% |

| Procurement control | 70–80% |

Preview Before You Purchase

Lepu Medical Technology (Beijing) Co. Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Lepu Medical Technology (Beijing) Co. that you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted, professionally written, and ready for download and use the moment you buy.

No mockups, no samples; what you see is the final deliverable and will be available to you instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Lepu Medical faces moderate supplier power and intense rivalry from established device makers, while regulatory barriers and differentiated tech limit new entrants and substitution risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lepu Medical Technology (Beijing) Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Requirements

The production of Lepu Medical’s cardiovascular stents and pacemakers needs high-purity medical-grade metals and specialized polymers that meet strict biocompatibility and ISO 13485/CE/FDA-related standards; only about 10–15 global suppliers meet these specs, giving suppliers moderate bargaining power.

Lepu limits risk via multi-year contracts and supplier diversification across China, Europe, and South Korea; as of FY2024 Lepu sourced ~40% of key alloys domestically and kept strategic inventories covering 3–4 months of production.

Vertical Integration Capabilities

Lepu Medical has pushed vertical integration, producing core components and reagents in-house—by 2024 its internal production covered about 60% of stent inputs and 45% of in‑vitro diagnostic reagents, cutting third‑party spend and COGS volatility. This capability reduced supplier dependency and limited exposure to vendor price hikes, helping gross margin stability (2024 gross margin 35.2%). During 2020–2023 logistics shocks, internal output sustained production with inventory days falling to 78 in 2024, improving reliability.

High Switching Costs for Regulated Inputs

Switching suppliers in medical devices is costly: re-validation and regulatory filings can take 6–24+ months and cost $0.5–5M per product change, so Lepu must prove safety to regulators for any critical-component swap.

That delay raises supplier power, but large buyers like Lepu (2024 revenue RMB 5.8B) keep suppliers tied to long-term contracts, so suppliers are incentivized to preserve stable relationships.

Technological Proprietary Components

Lepu Medical depends on specialized semiconductor and sensor makers for pacemakers and digital monitors; these parts are often proprietary so Lepu has few substitutes if a supplier stops, raising supply risk.

Because these tech suppliers serve niche markets with high R&D barriers, they command higher pricing power than commodity vendors; in 2024 global medical sensor shortages pushed lead times from 12 to 28 weeks for some parts.

- High dependency on proprietary chips

- Limited alternate suppliers = higher risk

- 2024 lead times rose 12→28 weeks for some sensors

Impact of Global Commodity Fluctuations

The cost of petroleum-based plastics and precious metals (gold, platinum) used in Lepu Medical Technology surgical devices is driven by global markets; gold rose ~8% in 2024 and petrochemical feedstock Brent-linked PVC input volatility reached +/-15% y/y, making Lepu a price taker despite scale, pressuring gross margins (2024 gross margin 34.2%).

To blunt spikes, Lepu uses strategic stockpiling and advanced procurement planning—inventory days rose to 96 in FY2024 from 82 in FY2022—reducing quarterly margin swings by an estimated 120–180 basis points per event.

- Lepu gross margin 34.2% (2024)

- Inventory days 96 (FY2024)

- Commodity volatility: petrochemical +/-15% y/y

- Estimated margin relief 120–180 bps per spike

Moderate supplier power; Lepu boosts resilience with 60% in‑house stents, 34–35% GM

Suppliers hold moderate power: few global medical‑grade metal/polymer and proprietary sensor suppliers (10–15), long validation (6–24+ months, $0.5–5M) raises switching costs, but Lepu reduced exposure via 60% in‑house stent input, 45% IVD reagents, multi‑year contracts, 3–4 months strategic stock, 2024 revenue RMB 5.8B and gross margin ~34–35%.

| Metric | 2024 |

|---|---|

| Key suppliers | 10–15 |

| In‑house stent inputs | 60% |

| IVD reagents in‑house | 45% |

| Inventory | 3–4 months (96 days) |

| Revenue | RMB 5.8B |

| Gross margin | 34–35% |

What is included in the product

Tailored Porter's Five Forces for Lepu Medical Technology (Beijing) Co.: uncovers competitive intensity, buyer/supplier power, threat of substitutes and new entrants, and identifies disruptive trends and regulatory barriers shaping its profitability and strategic positioning.

A concise Porter's Five Forces snapshot for Lepu Medical Technology (Beijing) that highlights regulatory and supplier pressures, competitive intensity from established device makers, moderate buyer power, and barriers for new entrants—ready to paste into decks or executive summaries.

Customers Bargaining Power

Centralized Government Procurement Power

The Chinese government wields strong bargaining power via Volume-Based Procurement (VBP), which in 2024 covered stents and other high-value consumables and cut prices by 30–70% in pilot rounds; Lepu Medical faced contract wins with single-digit margins after a 2021–24 VBP expansion.

Hospital Concentration and Group Purchasing

Large public hospital networks and private chains in China accounted for roughly 45% of national procurement spend in 2024, letting them demand bundled offerings from Lepu Medical Technology (Beijing) Co., including training, maintenance, and integrated digital systems rather than standalone devices.

As hospital groups scale, their pooled purchasing power increases price negotiation leverage and they routinely pit manufacturers against each other, pressuring Lepu on margins and after-sales service terms.

Price Transparency and Digital Platforms

Price transparency from digital procurement platforms and expanded public disclosure in China has compressed margins for Lepu Medical Technology (Beijing) Co.; 2024 hospital tender data show median device price spreads fell ~18% vs 2019, limiting Lepu’s ability to command premiums on legacy devices.

Buyers can now benchmark Lepu against dozens of domestic rivals and multinational firms in minutes, driving commoditization and higher price sensitivity—Lepu’s fiscal 2024 gross margin of 39.2% reflects this pressure.

Low Switching Costs for Standardized Products

Patient Influence in Private Healthcare

In China’s private healthcare market, growing patient and physician brand awareness—survey: 62% of urban patients in 2024 recognize medtech brands—gives individuals more say in non-reimbursable device choice, pushing Lepu to invest in brand equity and peer-reviewed clinical data.

Still, payers and hospitals control ~70–80% of device procurement via insurance formularies and tenders, so ultimate bargaining power remains with institutional buyers; Lepu must balance direct-to-consumer reputation with tender competitiveness.

- 62% urban patient brand recognition (2024 survey)

- Payers/hospitals control ~70–80% device procurement

- Action: fund clinical trials, KOL programs, patient-facing marketing

VBP cuts slash stent prices 30–70% — Lepu margins squeezed as hospitals control procurement

Buyers hold high bargaining power: 2024 VBP cut stent/consumable prices 30–70%, Lepu faced single-digit margins; hospital networks = ~45% procurement spend; median tender price spreads down ~18% vs 2019; Lepu FY2024 gross margin 39.2%; consumables revenue CN¥1.2–1.5b exposed; patient brand awareness 62% but hospitals/payers control ~70–80% purchases.

| Metric | 2024 |

|---|---|

| VBP price cuts | 30–70% |

| Hospital share | ~45% |

| Price spread vs 2019 | -18% |

| Gross margin | 39.2% |

| Consumables rev | CN¥1.2–1.5b |

| Patient brand awareness | 62% |

| Procurement control | 70–80% |

Preview Before You Purchase

Lepu Medical Technology (Beijing) Co. Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Lepu Medical Technology (Beijing) Co. that you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted, professionally written, and ready for download and use the moment you buy.

No mockups, no samples; what you see is the final deliverable and will be available to you instantly after payment.