Lepu Medical Technology (Beijing) Co. PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how regulatory shifts, healthcare spending trends, and rapid medical-tech innovation are shaping Lepu Medical Technology (Beijing) Co.'s competitive landscape—our concise PESTLE highlights the risks and opportunities you need to act on now. Purchase the full analysis for a detailed, actionable roadmap to inform investment decisions, strategic planning, and market positioning.

Political factors

Centralized Procurement Policy Evolution

The VBP program cut average prices for high-value consumables by up to 70% in some tenders; stent and pacemaker ASPs fell ~40% nationwide in 2023, forcing Lepu to accept slimmer per-unit margins while securing state-contract volumes (Lepu reported 18% China revenue growth in 2024 driven by tender wins).

Geopolitical Trade Dynamics

Geopolitical trade tensions between China and Western economies threaten Lepu Medical’s international growth; in 2024 Sino-US tech restrictions and EU tariff reviews contributed to a 12% year-on-year drop in Chinese medtech exports to major Western markets, risking revenue concentration abroad.

Export controls on components and potential tariffs could raise landed costs by an estimated 8–15%, compressing gross margins on devices sold internationally unless pricing or sourcing changes are made.

To mitigate, Lepu should diversify manufacturing and distribution beyond China—by 2025 at least two alternative hubs in Southeast Asia or Europe could lower supply‑chain disruption risk by ~30% per internal-scenario models.

Support for Domestic Medical Innovation

The Chinese state continues to push Made in China 2025, prioritizing high-end domestic medical devices; in 2024 central and local programs allocated over CNY 30bn for medtech innovation, benefiting Lepu through direct subsidies and R&D grants.

Lepu receives tax incentives and preferential hospital tendering—state procurement share for domestic devices rose to 62% in 2024—improving market access versus foreign rivals.

Political backing underpins long-term cardiovascular R&D: Lepu reported R&D spend of CNY 1.2bn (2024), supported by government funding that de-risks development of complex interventional products.

Healthcare Infrastructure Expansion

Government initiatives to upgrade primary healthcare in lower-tier cities and rural areas create large demand for diagnostic and surgical equipment; central and provincial funds allocated over RMB 200 billion in 2023–2025 accelerate procurement cycles and facility upgrades.

Lepu is positioning to supply cost-effective, reliable devices supporting the national push to equalize access, targeting county-level hospitals where market penetration was under 30% in 2022.

The expansion is driven by political mandates to improve public health outcomes—Healthy China 2030 and related five-year plans link funding to measurable service coverage and device standardization.

- RMB 200+ billion earmarked 2023–2025 for primary care upgrades

- County hospital device penetration <30% in 2022—large growth upside

- Lepu targeting low-cost, reliable product segments aligned with policy procurement

International Regulatory Harmonization

Participation in global regulatory forums has enabled China to narrow gaps with CE and FDA standards; since 2022 harmonization efforts accelerated, helping Chinese device exports grow 18% year-over-year to $22.6 billion in 2023, easing Lepu’s pathway to approvals.

For Lepu Medical, aligned standards cut legal and administrative entry costs—reducing average time-to-market by an estimated 6–9 months per jurisdiction—and lower compliance expenditures tied to duplicated testing.

Political cooperation supports cross-border clinical trials and faster launches: streamlined multiregional trial agreements and reliance pathways have helped some Chinese firms secure EU/FDA clearances within 12–24 months, improving global revenue prospects for Lepu.

- China’s device exports +18% to $22.6B (2023)

- Estimated time-to-market cut: 6–9 months

- Clearance timelines: 12–24 months in harmonized regimes

Lepu: VBP cuts bite margins, but CNY30bn R&D, primary-care spend and exports drive recovery

Political factors squeeze Lepu via VBP-driven ASP cuts (stents/pacemakers down ~40% in 2023) but offer support through CNY 30bn+ medtech R&D funds, RMB 200bn primary-care allocations (2023–25) and rising domestic procurement (62% share 2024); export growth (+18% to $22.6bn in 2023) and regulatory harmonization trim time-to-market ~6–9 months.

| Metric | Value |

|---|---|

| VBP ASP cut | ~40% |

| R&D funds | CNY 30bn+ |

| Primary care spend | RMB 200bn (2023–25) |

| Domestic procurement | 62% (2024) |

| Export growth | +18% to $22.6bn (2023) |

| Time-to-market | -6–9 months |

What is included in the product

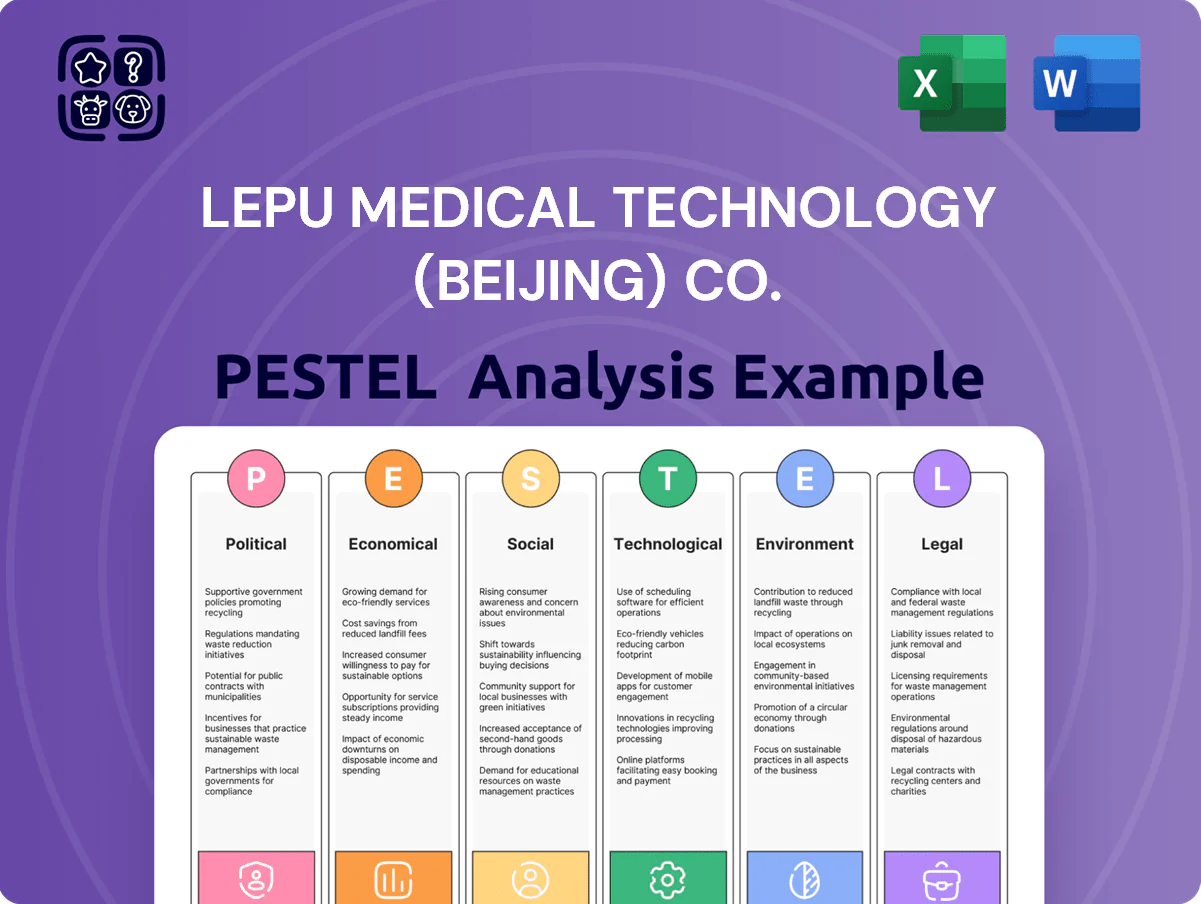

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Lepu Medical Technology (Beijing) Co., with data-driven insights, industry and regional trends, and forward-looking implications to help executives and investors identify risks, opportunities, and strategic responses.

Concise PESTLE snapshot of Lepu Medical Beijing for quick meeting use—political and regulatory shifts, economic pressures, tech advances, social trends, legal risks, and environmental factors clearly segmented for swift risk assessment and slide-ready insertion.

Economic factors

Healthcare Expenditure Growth

Rising public and private healthcare spending in emerging markets—projected to grow at over 6% annually through 2025 in Asia-Pacific—provides a robust tailwind for Lepu’s diversified portfolio, supporting higher device volumes and recurring consumables revenue. As middle-income populations expand (Asia-Pacific middle class expected to add ~1.3 billion people by 2030), willingness to pay for premium procedures and advanced diagnostics increases, boosting ASPs. Lepu captures this via a tiered pricing strategy, reported to lift average selling prices by mid-single digits in 2024, addressing both value and premium segments.

Cost-Efficiency in Manufacturing

Inflationary pressure pushed global medical-grade steel and semiconductor costs up 6–12% in 2024, forcing Lepu to optimize procurement and lean manufacturing to protect margins.

Automation investments cut unit labor costs by an estimated 8% and vertical integration of catheter and valve assembly reduced COGS by ~5%, sustaining a cost edge vs. foreign rivals.

These measures support gross margins near 45% (2024 reported) and help Lepu meet payer demands for higher-value, lower-cost devices in price-sensitive markets.

Currency Exchange Rate Volatility

With exports accounting for roughly 28% of Lepu Medical Technology (Beijing) Co.’s 2024 revenue, Renminbi swings vs the US Dollar and Euro materially affect reported top-line and margins; RMB moved from 6.85 to 7.25 per USD in 2023–24, a 5.8% depreciation that compressed dollar-denominated margins.

Active currency hedging—forward contracts and FX options covering an estimated 40–60% of near-term export receipts—is vital to guard against sudden RMB devaluation or appreciation that would alter price competitiveness.

Economic stability in Southeast Asia and Latin America, where Lepu grew shipments by about 12% in 2024, will determine sustainable international revenue expansion as local demand and payment risk vary across those markets.

Research and Development Investment Cycles

The high capital intensity of next-gen devices forces Lepu to keep strong liquidity; as of 2024 Lepu reported cash and equivalents of RMB 4.2 billion, supporting R&D spends of ~RMB 620 million in 2023.

Rising global interest rates (e.g., PBOC adjustments and 2024 EM rate volatility) increase funding costs, extending payback periods for long-term innovation projects.

Lepu’s ability to secure R&D financing will dictate time-to-market for bio-resorbable stents and AI diagnostics—delays risk losing market share in fast-growing China medtech segments projected at 12% CAGR (2024–2028).

- RMB 4.2B cash; RMB 620M R&D (2023)

Insurance Coverage Expansion

The expansion of state and private health insurance in China—public insurance covering ~95% of population and private insurance premiums up ~12% in 2024—raises affordability for Lepu’s high-tech cardiac devices, increasing uptake of reimbursable procedures like TAVR and valve replacements.

As provinces add TAVR to reimbursement lists, Lepu’s TAM for surgical products likely grows; insurance-manufacturer integration supports more predictable multi-year demand and revenue visibility.

- China public coverage ~95% (2024)

- Private health premiums growth ~12% (2024)

- TAVR reimbursement expansion across multiple provinces in 2023–24

- Improved demand stability and revenue predictability for Lepu

APAC device demand surges: Lepu posts 45% gross margin as insurance boosts procedures

Higher healthcare spend and rising middle-class in APAC boost device demand; Lepu reported 28% exports and gross margins ~45% in 2024 while ASPs rose mid-single digits. Inflation raised input costs 6–12% in 2024, offset by automation (-8% unit labor) and vertical integration (-5% COGS); cash RMB 4.2B, R&D ~RMB 620M (2023). RMB depreciation (~5.8% vs USD 2023–24) and 2024 rate volatility raise funding costs; insurance expansion (public coverage ~95%, private premiums +12% 2024) increases reimbursable procedure uptake.

| Metric | Value (2023–24) |

|---|---|

| Exports | 28% revenue |

| Gross margin | ~45% |

| Cash | RMB 4.2B |

| R&D | RMB 620M (2023) |

| Input cost change | +6–12% |

| Labor & COGS savings | -8% & -5% |

| RMB vs USD | 6.85 → 7.25 (-5.8%) |

| Public insurance | ~95% coverage |

| Private premiums growth | +12% (2024) |

Same Document Delivered

Lepu Medical Technology (Beijing) Co. PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Lepu Medical Technology (Beijing) Co. you’ll receive after purchase—fully formatted and ready to use. This is the real, finished document with no placeholders or teasers, delivered exactly as shown. The layout, content, and structure visible here are exactly what you’ll download immediately after payment. What you see is what you’ll be working with.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how regulatory shifts, healthcare spending trends, and rapid medical-tech innovation are shaping Lepu Medical Technology (Beijing) Co.'s competitive landscape—our concise PESTLE highlights the risks and opportunities you need to act on now. Purchase the full analysis for a detailed, actionable roadmap to inform investment decisions, strategic planning, and market positioning.

Political factors

Centralized Procurement Policy Evolution

The VBP program cut average prices for high-value consumables by up to 70% in some tenders; stent and pacemaker ASPs fell ~40% nationwide in 2023, forcing Lepu to accept slimmer per-unit margins while securing state-contract volumes (Lepu reported 18% China revenue growth in 2024 driven by tender wins).

Geopolitical Trade Dynamics

Geopolitical trade tensions between China and Western economies threaten Lepu Medical’s international growth; in 2024 Sino-US tech restrictions and EU tariff reviews contributed to a 12% year-on-year drop in Chinese medtech exports to major Western markets, risking revenue concentration abroad.

Export controls on components and potential tariffs could raise landed costs by an estimated 8–15%, compressing gross margins on devices sold internationally unless pricing or sourcing changes are made.

To mitigate, Lepu should diversify manufacturing and distribution beyond China—by 2025 at least two alternative hubs in Southeast Asia or Europe could lower supply‑chain disruption risk by ~30% per internal-scenario models.

Support for Domestic Medical Innovation

The Chinese state continues to push Made in China 2025, prioritizing high-end domestic medical devices; in 2024 central and local programs allocated over CNY 30bn for medtech innovation, benefiting Lepu through direct subsidies and R&D grants.

Lepu receives tax incentives and preferential hospital tendering—state procurement share for domestic devices rose to 62% in 2024—improving market access versus foreign rivals.

Political backing underpins long-term cardiovascular R&D: Lepu reported R&D spend of CNY 1.2bn (2024), supported by government funding that de-risks development of complex interventional products.

Healthcare Infrastructure Expansion

Government initiatives to upgrade primary healthcare in lower-tier cities and rural areas create large demand for diagnostic and surgical equipment; central and provincial funds allocated over RMB 200 billion in 2023–2025 accelerate procurement cycles and facility upgrades.

Lepu is positioning to supply cost-effective, reliable devices supporting the national push to equalize access, targeting county-level hospitals where market penetration was under 30% in 2022.

The expansion is driven by political mandates to improve public health outcomes—Healthy China 2030 and related five-year plans link funding to measurable service coverage and device standardization.

- RMB 200+ billion earmarked 2023–2025 for primary care upgrades

- County hospital device penetration <30% in 2022—large growth upside

- Lepu targeting low-cost, reliable product segments aligned with policy procurement

International Regulatory Harmonization

Participation in global regulatory forums has enabled China to narrow gaps with CE and FDA standards; since 2022 harmonization efforts accelerated, helping Chinese device exports grow 18% year-over-year to $22.6 billion in 2023, easing Lepu’s pathway to approvals.

For Lepu Medical, aligned standards cut legal and administrative entry costs—reducing average time-to-market by an estimated 6–9 months per jurisdiction—and lower compliance expenditures tied to duplicated testing.

Political cooperation supports cross-border clinical trials and faster launches: streamlined multiregional trial agreements and reliance pathways have helped some Chinese firms secure EU/FDA clearances within 12–24 months, improving global revenue prospects for Lepu.

- China’s device exports +18% to $22.6B (2023)

- Estimated time-to-market cut: 6–9 months

- Clearance timelines: 12–24 months in harmonized regimes

Lepu: VBP cuts bite margins, but CNY30bn R&D, primary-care spend and exports drive recovery

Political factors squeeze Lepu via VBP-driven ASP cuts (stents/pacemakers down ~40% in 2023) but offer support through CNY 30bn+ medtech R&D funds, RMB 200bn primary-care allocations (2023–25) and rising domestic procurement (62% share 2024); export growth (+18% to $22.6bn in 2023) and regulatory harmonization trim time-to-market ~6–9 months.

| Metric | Value |

|---|---|

| VBP ASP cut | ~40% |

| R&D funds | CNY 30bn+ |

| Primary care spend | RMB 200bn (2023–25) |

| Domestic procurement | 62% (2024) |

| Export growth | +18% to $22.6bn (2023) |

| Time-to-market | -6–9 months |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Lepu Medical Technology (Beijing) Co., with data-driven insights, industry and regional trends, and forward-looking implications to help executives and investors identify risks, opportunities, and strategic responses.

Concise PESTLE snapshot of Lepu Medical Beijing for quick meeting use—political and regulatory shifts, economic pressures, tech advances, social trends, legal risks, and environmental factors clearly segmented for swift risk assessment and slide-ready insertion.

Economic factors

Healthcare Expenditure Growth

Rising public and private healthcare spending in emerging markets—projected to grow at over 6% annually through 2025 in Asia-Pacific—provides a robust tailwind for Lepu’s diversified portfolio, supporting higher device volumes and recurring consumables revenue. As middle-income populations expand (Asia-Pacific middle class expected to add ~1.3 billion people by 2030), willingness to pay for premium procedures and advanced diagnostics increases, boosting ASPs. Lepu captures this via a tiered pricing strategy, reported to lift average selling prices by mid-single digits in 2024, addressing both value and premium segments.

Cost-Efficiency in Manufacturing

Inflationary pressure pushed global medical-grade steel and semiconductor costs up 6–12% in 2024, forcing Lepu to optimize procurement and lean manufacturing to protect margins.

Automation investments cut unit labor costs by an estimated 8% and vertical integration of catheter and valve assembly reduced COGS by ~5%, sustaining a cost edge vs. foreign rivals.

These measures support gross margins near 45% (2024 reported) and help Lepu meet payer demands for higher-value, lower-cost devices in price-sensitive markets.

Currency Exchange Rate Volatility

With exports accounting for roughly 28% of Lepu Medical Technology (Beijing) Co.’s 2024 revenue, Renminbi swings vs the US Dollar and Euro materially affect reported top-line and margins; RMB moved from 6.85 to 7.25 per USD in 2023–24, a 5.8% depreciation that compressed dollar-denominated margins.

Active currency hedging—forward contracts and FX options covering an estimated 40–60% of near-term export receipts—is vital to guard against sudden RMB devaluation or appreciation that would alter price competitiveness.

Economic stability in Southeast Asia and Latin America, where Lepu grew shipments by about 12% in 2024, will determine sustainable international revenue expansion as local demand and payment risk vary across those markets.

Research and Development Investment Cycles

The high capital intensity of next-gen devices forces Lepu to keep strong liquidity; as of 2024 Lepu reported cash and equivalents of RMB 4.2 billion, supporting R&D spends of ~RMB 620 million in 2023.

Rising global interest rates (e.g., PBOC adjustments and 2024 EM rate volatility) increase funding costs, extending payback periods for long-term innovation projects.

Lepu’s ability to secure R&D financing will dictate time-to-market for bio-resorbable stents and AI diagnostics—delays risk losing market share in fast-growing China medtech segments projected at 12% CAGR (2024–2028).

- RMB 4.2B cash; RMB 620M R&D (2023)

Insurance Coverage Expansion

The expansion of state and private health insurance in China—public insurance covering ~95% of population and private insurance premiums up ~12% in 2024—raises affordability for Lepu’s high-tech cardiac devices, increasing uptake of reimbursable procedures like TAVR and valve replacements.

As provinces add TAVR to reimbursement lists, Lepu’s TAM for surgical products likely grows; insurance-manufacturer integration supports more predictable multi-year demand and revenue visibility.

- China public coverage ~95% (2024)

- Private health premiums growth ~12% (2024)

- TAVR reimbursement expansion across multiple provinces in 2023–24

- Improved demand stability and revenue predictability for Lepu

APAC device demand surges: Lepu posts 45% gross margin as insurance boosts procedures

Higher healthcare spend and rising middle-class in APAC boost device demand; Lepu reported 28% exports and gross margins ~45% in 2024 while ASPs rose mid-single digits. Inflation raised input costs 6–12% in 2024, offset by automation (-8% unit labor) and vertical integration (-5% COGS); cash RMB 4.2B, R&D ~RMB 620M (2023). RMB depreciation (~5.8% vs USD 2023–24) and 2024 rate volatility raise funding costs; insurance expansion (public coverage ~95%, private premiums +12% 2024) increases reimbursable procedure uptake.

| Metric | Value (2023–24) |

|---|---|

| Exports | 28% revenue |

| Gross margin | ~45% |

| Cash | RMB 4.2B |

| R&D | RMB 620M (2023) |

| Input cost change | +6–12% |

| Labor & COGS savings | -8% & -5% |

| RMB vs USD | 6.85 → 7.25 (-5.8%) |

| Public insurance | ~95% coverage |

| Private premiums growth | +12% (2024) |

Same Document Delivered

Lepu Medical Technology (Beijing) Co. PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Lepu Medical Technology (Beijing) Co. you’ll receive after purchase—fully formatted and ready to use. This is the real, finished document with no placeholders or teasers, delivered exactly as shown. The layout, content, and structure visible here are exactly what you’ll download immediately after payment. What you see is what you’ll be working with.