Bank Leumi PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain strategic clarity with our PESTLE Analysis of Bank Leumi—unpack how political shifts, economic cycles, regulatory changes, social trends, technological disruption, and environmental pressures shape its outlook; ideal for investors and strategists seeking actionable intelligence. Purchase the full report to access detailed insights, editable charts, and practical recommendations for confident decision-making.

Political factors

Regional Geopolitical Stability

The ongoing security situation in the Middle East remains a key risk driver for Israeli banks; by Q4 2025 investor risk premia lifted yields on 10-year Israeli government bonds to about 3.9%, raising Bank Leumi’s wholesale funding costs and pressuring net interest margins.

Government Fiscal Policy

Israel's 2025 budget projects defense spending at roughly NIS 123 billion (about 3.4% of GDP) and expanded social programs, contributing to a projected deficit near 4.0% of GDP and public debt around 66% of GDP, tightening market liquidity and pressuring yields.

Higher fiscal deficits have lifted 10-year Israeli government bond yields to about 3.8% in late 2025, raising funding costs and influencing Bank Leumi's interest margin management.

Bank Leumi must model potential financial-sector levies or corporate tax adjustments—recent government discussions in 2024–2025 included proposals to raise tax revenues by NIS 10–15 billion—to assess impacts on profitability and capital planning.

International Diplomatic Relations

Leumi’s extensive international operations and correspondent-banking network—supporting roughly 15% of its NIS 220 billion total assets in 2024—are sensitive to Israel’s global standing, with diplomatic ties to the US and EU enabling smoother cross-border payments and access to $USD and EUR capital markets. Strong US/EU relations reduce compliance frictions and lower funding costs; sudden changes in trade agreements or sanctions (e.g., post-2023 measures) force immediate legal, AML, and operational adjustments to maintain uninterrupted global service.

Internal Political Landscape

Domestic political stability and legislative continuity underpin predictability for Bank Leumi, which reported NIS 17.8 billion in net income for 2024 H1, making policy-driven risk management vital.

Judicial reforms or coalition shifts have historically triggered shekel volatility—USD/ILS moved from 3.80 to 3.65 in 2024—raising market and credit-risk exposure for large banks.

As a systemic bank, Bank Leumi must remain neutral yet proactive, maintaining capital buffers (CET1 ~12.5% in 2024) and contingency plans to stabilize operations amid local political shifts.

- Political stability supports predictable lending and investment decisions

- Judicial/government changes correlate with FX and market volatility (USD/ILS swings in 2024)

- Bank Leumi acts as economic stabilizer—maintains CET1 ~12.5% and robust liquidity

State-Led Infrastructure Investment

Government initiatives targeting energy independence, transportation, and housing create sizable project-financing pipelines for Bank Leumi’s corporate arm, with Israel budgeting NIS 120–150 billion for national infrastructure through 2026 and renewables targets raising project finance demand.

Leumi increasingly serves as lead financier in public-private partnerships toward 2026 modernization goals, originating multi-year loans and bond syndications that can represent 5–8% of its corporate loan book.

These long-term contracts yield stable fee and interest income but require strict compliance and adaptive risk pricing as regulatory frameworks evolve, with recent regulatory revisions accelerating PPP oversight and repayment guarantees.

- NIS 120–150 billion national infrastructure budget through 2026

- Leumi exposure in PPPs ≈ 5–8% of corporate loan book

- Stable long-term revenue vs. regulatory and policy risk

Rising yields, fiscal strain and tax shifts squeeze margins as infrastructure boosts PPP risk

Political risks—regional security, higher fiscal deficits (≈4.0% GDP) and rising 10y yields (~3.8–3.9% in late 2025)—increase funding costs and NIM pressure; proposed 2024–25 tax measures (NIS 10–15bn) and regulatory shifts require capital planning (CET1 ~12.5% in 2024); infrastructure spending (NIS 120–150bn through 2026) supports PPP lending (5–8% of corporate book) but adds policy/compliance risk.

| Metric | Value |

|---|---|

| 10y Israel yield | 3.8–3.9% |

| Fiscal deficit | ≈4.0% GDP |

| Public debt | ≈66% GDP |

| CET1 (2024) | ≈12.5% |

| Infrastructure budget | NIS 120–150bn |

| PPP exposure | 5–8% corporate loans |

What is included in the product

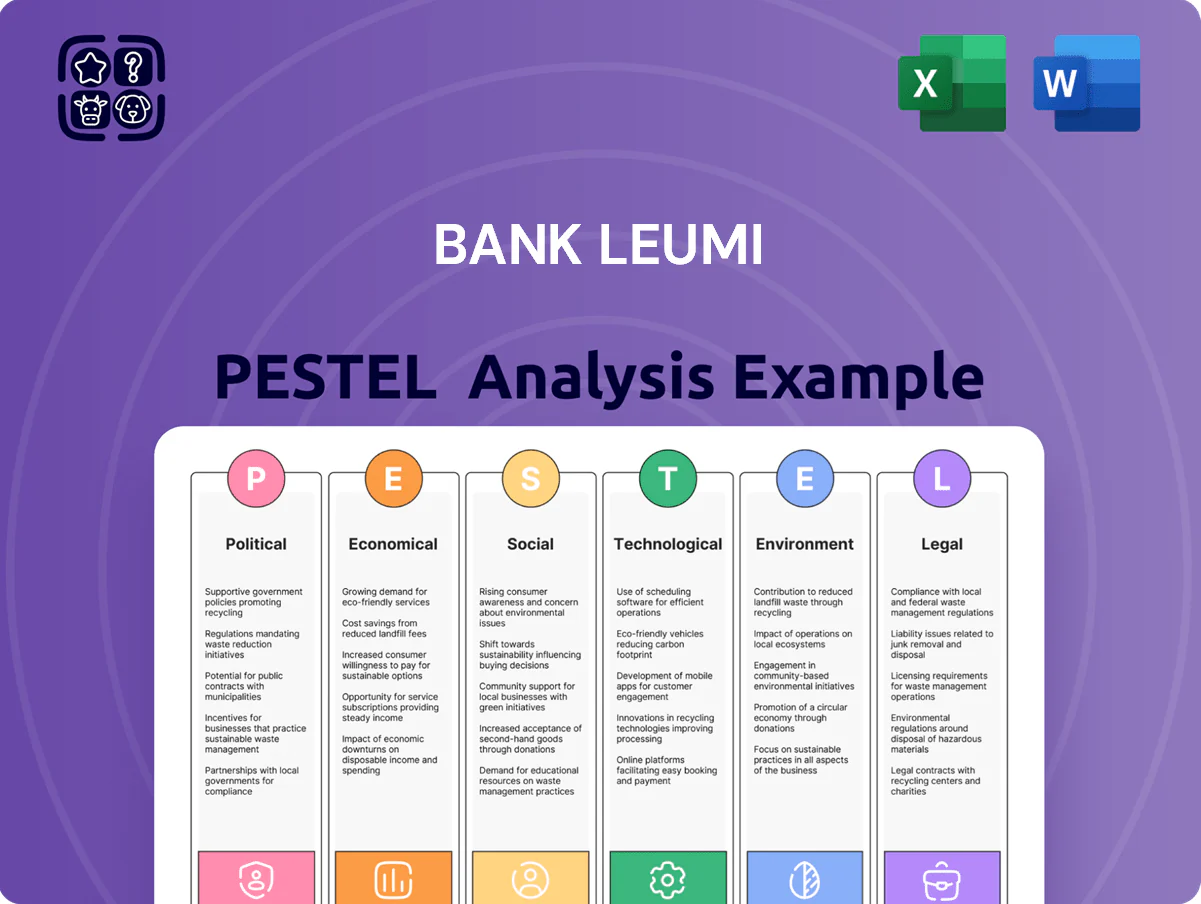

Explores how macro-environmental factors uniquely affect Bank Leumi across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking implications to identify threats, opportunities, and strategic responses for executives, investors, and advisors.

Visually segmented by PESTLE categories for Bank Leumi, this concise summary enables quick interpretation in meetings, easy insertion into presentations, and effortless sharing across teams to streamline risk discussions and strategic alignment.

Economic factors

Interest Rate Environment

Decisions by the Bank of Israel on the benchmark rate drive Leumi’s net interest margin; after peak rates in 2023–2024 (10.25%), inflation eased toward end-2025 and the BoI moved to a neutral stance, compressing NIM pressure. Leumi reported NIM of about 2.1% in 2025, prompting optimization of deposit yields and loan pricing to protect ROE while remaining competitively priced; balancing margin and market share is a core executive challenge.

Inflationary Trends

Persistent inflation erodes real value of Bank Leumi’s assets and retail purchasing power; Israel’s CPI rose 3.3% in 2024 y/y, increasing pressure on margins and deposit real returns.

Indexed mortgages and CPI-linked products offer partial protection, but high inflation raised SME default rates to 2.1% in 2024, heightening credit risk for leveraged borrowers.

Bank Leumi deploys dynamic hedges and CPI swaps—hedge book expanded 18% in 2024—to stabilize net interest income and cushion CPI volatility on the balance sheet.

Real Estate Market Dynamics

Bank Leumi holds roughly 28% of its loan book in mortgages and construction financing, so shifts in Israel's housing market—where prices rose 6.5% y/y in 2024 in high-demand areas—directly impact credit growth and NPL risk.

Currency Exchange Volatility

Fluctuations in the Israeli shekel versus the US dollar and euro directly affect Bank Leumi’s valuation of FX-denominated assets and liabilities; in 2024 the shekel moved roughly 3–6% vs the dollar, amplifying translation swings in quarterly results.

For international corporate clients, exchange-rate stability is crucial for trade finance and cross-border investments Leumi manages, with FX volatility raising hedging costs and margin risks.

Leumi’s treasury must actively hedge and use dynamic net‑open‑position limits to avoid material translation losses; as of Q4 2024 the bank reported FX exposure reductions of about 20% year‑on‑year.

- Shekel USD/EUR swings (2024): ~3–6% vs USD; ~2–5% vs EUR

- Hedging and net‑open‑position limits used to cut FX exposure ~20% YoY (Q4 2024)

- Higher hedging costs impact trade finance margins for corporates

Labor Market and GDP Growth

The Israeli economy expanded 3.4% in 2023 with unemployment at 3.8% (Q4 2023), directly supporting retail and commercial credit demand for Bank Leumi; high-tech exports and VC activity—tech GDP share ~15%—fuel private banking asset growth.

A slowdown (IMF 2024 growth forecast 2.5%) would force tighter lending standards, higher provisioning and a greater focus on capital preservation.

- GDP 2023: 3.4%

- Unemployment Q4 2023: 3.8%

- High-tech ~15% of GDP

- IMF 2024 forecast: 2.5%

Inflation eases, NIMs squeeze to ~2.1% as housing and hedging drive risks

Rate moves (BoI peak 10.25% 2023–24) compressed NIM to ~2.1% in 2025; CPI eased to ~2.8% end‑2025, reducing immediate margin pressure. Inflation raised SME defaults to ~2.1% in 2024 and pushed hedging (hedge book +18% 2024) and provisioning higher. Mortgages/construction ~28% of loans; housing prices +6.5% y/y 2024; shekel swung ~3–6% vs USD in 2024, FX exposure cut ~20% YoY (Q4 2024).

| Metric | Value |

|---|---|

| NIM 2025 | ~2.1% |

| CPI 2024 | 3.3% |

| SME default 2024 | 2.1% |

| Mortgages & construction | ~28% loans |

| Housing prices 2024 | +6.5% y/y |

| Shekel vs USD 2024 | ~3–6% |

| Hedge book 2024 | +18% |

| FX exposure reduction Q4 2024 | ~20% YoY |

Same Document Delivered

Bank Leumi PESTLE Analysis

The preview shown here is the exact Bank Leumi PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain strategic clarity with our PESTLE Analysis of Bank Leumi—unpack how political shifts, economic cycles, regulatory changes, social trends, technological disruption, and environmental pressures shape its outlook; ideal for investors and strategists seeking actionable intelligence. Purchase the full report to access detailed insights, editable charts, and practical recommendations for confident decision-making.

Political factors

Regional Geopolitical Stability

The ongoing security situation in the Middle East remains a key risk driver for Israeli banks; by Q4 2025 investor risk premia lifted yields on 10-year Israeli government bonds to about 3.9%, raising Bank Leumi’s wholesale funding costs and pressuring net interest margins.

Government Fiscal Policy

Israel's 2025 budget projects defense spending at roughly NIS 123 billion (about 3.4% of GDP) and expanded social programs, contributing to a projected deficit near 4.0% of GDP and public debt around 66% of GDP, tightening market liquidity and pressuring yields.

Higher fiscal deficits have lifted 10-year Israeli government bond yields to about 3.8% in late 2025, raising funding costs and influencing Bank Leumi's interest margin management.

Bank Leumi must model potential financial-sector levies or corporate tax adjustments—recent government discussions in 2024–2025 included proposals to raise tax revenues by NIS 10–15 billion—to assess impacts on profitability and capital planning.

International Diplomatic Relations

Leumi’s extensive international operations and correspondent-banking network—supporting roughly 15% of its NIS 220 billion total assets in 2024—are sensitive to Israel’s global standing, with diplomatic ties to the US and EU enabling smoother cross-border payments and access to $USD and EUR capital markets. Strong US/EU relations reduce compliance frictions and lower funding costs; sudden changes in trade agreements or sanctions (e.g., post-2023 measures) force immediate legal, AML, and operational adjustments to maintain uninterrupted global service.

Internal Political Landscape

Domestic political stability and legislative continuity underpin predictability for Bank Leumi, which reported NIS 17.8 billion in net income for 2024 H1, making policy-driven risk management vital.

Judicial reforms or coalition shifts have historically triggered shekel volatility—USD/ILS moved from 3.80 to 3.65 in 2024—raising market and credit-risk exposure for large banks.

As a systemic bank, Bank Leumi must remain neutral yet proactive, maintaining capital buffers (CET1 ~12.5% in 2024) and contingency plans to stabilize operations amid local political shifts.

- Political stability supports predictable lending and investment decisions

- Judicial/government changes correlate with FX and market volatility (USD/ILS swings in 2024)

- Bank Leumi acts as economic stabilizer—maintains CET1 ~12.5% and robust liquidity

State-Led Infrastructure Investment

Government initiatives targeting energy independence, transportation, and housing create sizable project-financing pipelines for Bank Leumi’s corporate arm, with Israel budgeting NIS 120–150 billion for national infrastructure through 2026 and renewables targets raising project finance demand.

Leumi increasingly serves as lead financier in public-private partnerships toward 2026 modernization goals, originating multi-year loans and bond syndications that can represent 5–8% of its corporate loan book.

These long-term contracts yield stable fee and interest income but require strict compliance and adaptive risk pricing as regulatory frameworks evolve, with recent regulatory revisions accelerating PPP oversight and repayment guarantees.

- NIS 120–150 billion national infrastructure budget through 2026

- Leumi exposure in PPPs ≈ 5–8% of corporate loan book

- Stable long-term revenue vs. regulatory and policy risk

Rising yields, fiscal strain and tax shifts squeeze margins as infrastructure boosts PPP risk

Political risks—regional security, higher fiscal deficits (≈4.0% GDP) and rising 10y yields (~3.8–3.9% in late 2025)—increase funding costs and NIM pressure; proposed 2024–25 tax measures (NIS 10–15bn) and regulatory shifts require capital planning (CET1 ~12.5% in 2024); infrastructure spending (NIS 120–150bn through 2026) supports PPP lending (5–8% of corporate book) but adds policy/compliance risk.

| Metric | Value |

|---|---|

| 10y Israel yield | 3.8–3.9% |

| Fiscal deficit | ≈4.0% GDP |

| Public debt | ≈66% GDP |

| CET1 (2024) | ≈12.5% |

| Infrastructure budget | NIS 120–150bn |

| PPP exposure | 5–8% corporate loans |

What is included in the product

Explores how macro-environmental factors uniquely affect Bank Leumi across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking implications to identify threats, opportunities, and strategic responses for executives, investors, and advisors.

Visually segmented by PESTLE categories for Bank Leumi, this concise summary enables quick interpretation in meetings, easy insertion into presentations, and effortless sharing across teams to streamline risk discussions and strategic alignment.

Economic factors

Interest Rate Environment

Decisions by the Bank of Israel on the benchmark rate drive Leumi’s net interest margin; after peak rates in 2023–2024 (10.25%), inflation eased toward end-2025 and the BoI moved to a neutral stance, compressing NIM pressure. Leumi reported NIM of about 2.1% in 2025, prompting optimization of deposit yields and loan pricing to protect ROE while remaining competitively priced; balancing margin and market share is a core executive challenge.

Inflationary Trends

Persistent inflation erodes real value of Bank Leumi’s assets and retail purchasing power; Israel’s CPI rose 3.3% in 2024 y/y, increasing pressure on margins and deposit real returns.

Indexed mortgages and CPI-linked products offer partial protection, but high inflation raised SME default rates to 2.1% in 2024, heightening credit risk for leveraged borrowers.

Bank Leumi deploys dynamic hedges and CPI swaps—hedge book expanded 18% in 2024—to stabilize net interest income and cushion CPI volatility on the balance sheet.

Real Estate Market Dynamics

Bank Leumi holds roughly 28% of its loan book in mortgages and construction financing, so shifts in Israel's housing market—where prices rose 6.5% y/y in 2024 in high-demand areas—directly impact credit growth and NPL risk.

Currency Exchange Volatility

Fluctuations in the Israeli shekel versus the US dollar and euro directly affect Bank Leumi’s valuation of FX-denominated assets and liabilities; in 2024 the shekel moved roughly 3–6% vs the dollar, amplifying translation swings in quarterly results.

For international corporate clients, exchange-rate stability is crucial for trade finance and cross-border investments Leumi manages, with FX volatility raising hedging costs and margin risks.

Leumi’s treasury must actively hedge and use dynamic net‑open‑position limits to avoid material translation losses; as of Q4 2024 the bank reported FX exposure reductions of about 20% year‑on‑year.

- Shekel USD/EUR swings (2024): ~3–6% vs USD; ~2–5% vs EUR

- Hedging and net‑open‑position limits used to cut FX exposure ~20% YoY (Q4 2024)

- Higher hedging costs impact trade finance margins for corporates

Labor Market and GDP Growth

The Israeli economy expanded 3.4% in 2023 with unemployment at 3.8% (Q4 2023), directly supporting retail and commercial credit demand for Bank Leumi; high-tech exports and VC activity—tech GDP share ~15%—fuel private banking asset growth.

A slowdown (IMF 2024 growth forecast 2.5%) would force tighter lending standards, higher provisioning and a greater focus on capital preservation.

- GDP 2023: 3.4%

- Unemployment Q4 2023: 3.8%

- High-tech ~15% of GDP

- IMF 2024 forecast: 2.5%

Inflation eases, NIMs squeeze to ~2.1% as housing and hedging drive risks

Rate moves (BoI peak 10.25% 2023–24) compressed NIM to ~2.1% in 2025; CPI eased to ~2.8% end‑2025, reducing immediate margin pressure. Inflation raised SME defaults to ~2.1% in 2024 and pushed hedging (hedge book +18% 2024) and provisioning higher. Mortgages/construction ~28% of loans; housing prices +6.5% y/y 2024; shekel swung ~3–6% vs USD in 2024, FX exposure cut ~20% YoY (Q4 2024).

| Metric | Value |

|---|---|

| NIM 2025 | ~2.1% |

| CPI 2024 | 3.3% |

| SME default 2024 | 2.1% |

| Mortgages & construction | ~28% loans |

| Housing prices 2024 | +6.5% y/y |

| Shekel vs USD 2024 | ~3–6% |

| Hedge book 2024 | +18% |

| FX exposure reduction Q4 2024 | ~20% YoY |

Same Document Delivered

Bank Leumi PESTLE Analysis

The preview shown here is the exact Bank Leumi PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.