Levi Strauss & Co. Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

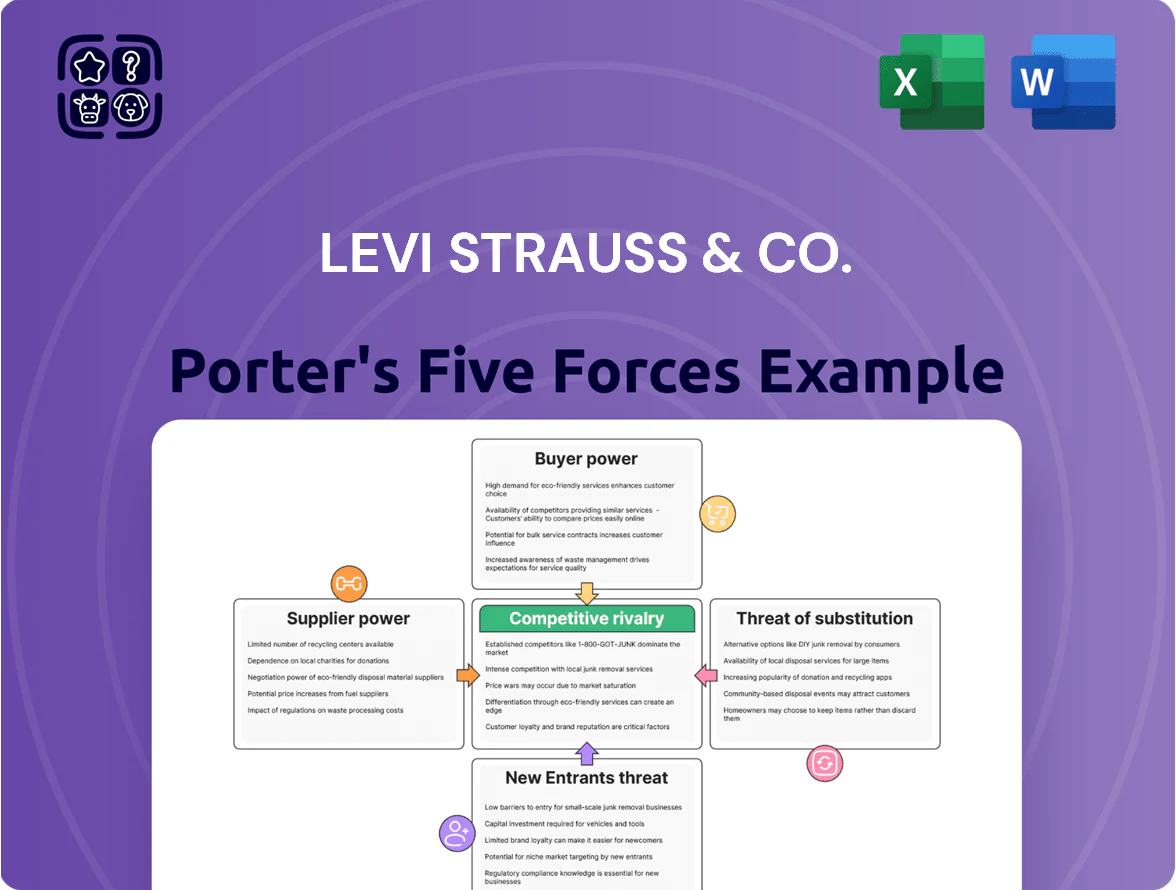

Levi Strauss & Co. faces intense rivalry from global apparel brands and fast-fashion entrants, while brand strength and scale temper supplier and buyer pressures in denim and lifestyle segments.

Emerging substitutes, shifting consumer trends, and digital retailing raise strategic risks but also create opportunities for premium positioning and direct-to-consumer growth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Levi Strauss & Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Global Supply Base

Levi Strauss & Co. taps a fragmented global supply base of ~850 third-party factories across Asia and Latin America, diluting supplier leverage by spreading orders; in 2024 roughly 60% of production came from Asia and 25% from Latin America, lowering dependence on any single vendor.

Commodity Price Volatility

Commodity price volatility for cotton and synthetics drives Levi Strauss & Co. input costs; cotton futures rose ~24% in 2024 after weather shocks, pushing raw-material inflation that increased gross margin pressure in FY2024 when COGS rose 7.1% year-over-year.

Strict Sustainability and Ethical Compliance

Levi Strauss & Co. enforces strict environmental and social standards via its Terms of Engagement, reducing eligible suppliers but giving Levi leverage as a high-value client—its 2024 revenues of $6.0 billion make retention attractive. Suppliers report capital expenditures rising up to 20% to meet compliance, creating a lock-in as switching costs rise. This dynamic strengthens supplier bargaining power in quality but weakens it on price and contract terms, favoring Levi in negotiations.

Strategic Manufacturing Partnerships

A portion of Levi Strauss & Co. production is concentrated among a few strategic partners that run large-scale, multi-region operations and thus hold slightly higher bargaining power due to technical expertise and rapid scaling capacity.

Levi’s 2024 revenue was $6.5 billion, and large partners depend on its high order volumes—roughly 100–150 million garments annually—keeping supplier pricing competitive despite their leverage.

- Few partners: concentrated production across regions

- Higher supplier power: technical know-how, fast scaling

- Counterbalance: Levi’s ~$6.5B revenue and 100–150M garments/year orders

- Result: suppliers incentivized to offer competitive pricing

Impact of Nearshoring and Vertical Integration

- Regional output +12% (2024 run-rate)

- Transit times −20% (median, 2024)

- Lower freight leverage, fewer single-source suppliers

- More in-house finishing reduces input-price volatility

Levi’s supplier power: buyer leverage amid rising cotton costs and critical technical partners

Levi’s supplier power is low-to-moderate: ~850 third-party factories (60% Asia, 25% Latin America) plus nearshoring raised regional output +12% (2024), revenue $6.5B and 100–150M garments/year give Levi buyer leverage, but cotton futures +24% (2024) and a few large technical partners raise supplier influence on quality and lead-time.

| Metric | 2024 |

|---|---|

| Factories | ~850 |

| Revenue | $6.5B |

| Garments/year | 100–150M |

| Asia share | 60% |

| LatAm share | 25% |

| Regional output change | +12% |

| Cotton futures | +24% |

What is included in the product

Tailored exclusively for Levi Strauss & Co., this Porter's Five Forces overview uncovers key drivers of competition, customer and supplier power, entry barriers, and substitute threats to assess pricing power and profitability in the apparel and denim market.

A concise Levi Strauss & Co. Porter's Five Forces snapshot—quickly assess competitive rivalry, supplier/buyer power, threat of substitutes and entrants to guide merchandising, pricing and market-entry decisions.

Customers Bargaining Power

Concentration of Wholesale Retailers

Low Switching Costs for End Consumers

Individual consumers face virtually zero financial cost switching from Levi's to rivals for denim or casual wear, so buyer power rises and Levi must sustain product quality and relevance; US apparel switch rates reached 28% annual churn in 2024 (NPD Group). Levi counters with loyalty and storytelling—its 2024 Silver Tab loyalty program grew members 18% to ~3.6 million—and marketing spend of $640 million in FY2024 to create emotional switching costs.

Expansion of Direct-to-Consumer Channels

Price Sensitivity and Economic Trends

Macroeconomic shocks like 2023–2024 US inflation (peaked 6.5% YoY in 2023) and real wage softness cut disposable income, making Levi Strauss & Co. (LEVI) customers more price-sensitive and prone to trade down or wait for promotions.

Levi balances premium positioning with value lines—Denizen and outlet channels—helping protect 2024 net revenue (US apparel market down ~1.5%) by retaining value-conscious buyers.

- Inflation peak 6.5% (2023)

- US real wages flat‑to‑down 2023–24

- Denizen/value lines soften downside

- Promotions rise in downturns

Information Transparency and Digital Comparison

- Instant price/review access raises buyer power

- 2024 DTC revenue $2.6B, +15% YoY

- Avg rating ~4.5/5 on major marketplaces

- Omnichannel focus reduces churn, protects margins

Moderate–High Customer Power: Wholesale Strength vs. Levi’s DTC, Loyalty & Margins

| Metric | 2024 |

|---|---|

| Wholesale net rev | $1.9B |

| Global brand rev | $3.9B |

| DTC revenue | $2.6B (30%) |

| Inventory turns | 3.5x |

| Loyalty members | ~3.6M |

| Marketing spend | $640M |

| Retail gross margin | ~60% |

| Wholesale gross margin | ~40% |

Same Document Delivered

Levi Strauss & Co. Porter's Five Forces Analysis

This preview shows the exact Levi Strauss & Co. Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted and ready for download and use the moment you buy. You're looking at the actual deliverable, complete and professionally written. No mockups or samples—what you see is what you'll get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Levi Strauss & Co. faces intense rivalry from global apparel brands and fast-fashion entrants, while brand strength and scale temper supplier and buyer pressures in denim and lifestyle segments.

Emerging substitutes, shifting consumer trends, and digital retailing raise strategic risks but also create opportunities for premium positioning and direct-to-consumer growth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Levi Strauss & Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Global Supply Base

Levi Strauss & Co. taps a fragmented global supply base of ~850 third-party factories across Asia and Latin America, diluting supplier leverage by spreading orders; in 2024 roughly 60% of production came from Asia and 25% from Latin America, lowering dependence on any single vendor.

Commodity Price Volatility

Commodity price volatility for cotton and synthetics drives Levi Strauss & Co. input costs; cotton futures rose ~24% in 2024 after weather shocks, pushing raw-material inflation that increased gross margin pressure in FY2024 when COGS rose 7.1% year-over-year.

Strict Sustainability and Ethical Compliance

Levi Strauss & Co. enforces strict environmental and social standards via its Terms of Engagement, reducing eligible suppliers but giving Levi leverage as a high-value client—its 2024 revenues of $6.0 billion make retention attractive. Suppliers report capital expenditures rising up to 20% to meet compliance, creating a lock-in as switching costs rise. This dynamic strengthens supplier bargaining power in quality but weakens it on price and contract terms, favoring Levi in negotiations.

Strategic Manufacturing Partnerships

A portion of Levi Strauss & Co. production is concentrated among a few strategic partners that run large-scale, multi-region operations and thus hold slightly higher bargaining power due to technical expertise and rapid scaling capacity.

Levi’s 2024 revenue was $6.5 billion, and large partners depend on its high order volumes—roughly 100–150 million garments annually—keeping supplier pricing competitive despite their leverage.

- Few partners: concentrated production across regions

- Higher supplier power: technical know-how, fast scaling

- Counterbalance: Levi’s ~$6.5B revenue and 100–150M garments/year orders

- Result: suppliers incentivized to offer competitive pricing

Impact of Nearshoring and Vertical Integration

- Regional output +12% (2024 run-rate)

- Transit times −20% (median, 2024)

- Lower freight leverage, fewer single-source suppliers

- More in-house finishing reduces input-price volatility

Levi’s supplier power: buyer leverage amid rising cotton costs and critical technical partners

Levi’s supplier power is low-to-moderate: ~850 third-party factories (60% Asia, 25% Latin America) plus nearshoring raised regional output +12% (2024), revenue $6.5B and 100–150M garments/year give Levi buyer leverage, but cotton futures +24% (2024) and a few large technical partners raise supplier influence on quality and lead-time.

| Metric | 2024 |

|---|---|

| Factories | ~850 |

| Revenue | $6.5B |

| Garments/year | 100–150M |

| Asia share | 60% |

| LatAm share | 25% |

| Regional output change | +12% |

| Cotton futures | +24% |

What is included in the product

Tailored exclusively for Levi Strauss & Co., this Porter's Five Forces overview uncovers key drivers of competition, customer and supplier power, entry barriers, and substitute threats to assess pricing power and profitability in the apparel and denim market.

A concise Levi Strauss & Co. Porter's Five Forces snapshot—quickly assess competitive rivalry, supplier/buyer power, threat of substitutes and entrants to guide merchandising, pricing and market-entry decisions.

Customers Bargaining Power

Concentration of Wholesale Retailers

Low Switching Costs for End Consumers

Individual consumers face virtually zero financial cost switching from Levi's to rivals for denim or casual wear, so buyer power rises and Levi must sustain product quality and relevance; US apparel switch rates reached 28% annual churn in 2024 (NPD Group). Levi counters with loyalty and storytelling—its 2024 Silver Tab loyalty program grew members 18% to ~3.6 million—and marketing spend of $640 million in FY2024 to create emotional switching costs.

Expansion of Direct-to-Consumer Channels

Price Sensitivity and Economic Trends

Macroeconomic shocks like 2023–2024 US inflation (peaked 6.5% YoY in 2023) and real wage softness cut disposable income, making Levi Strauss & Co. (LEVI) customers more price-sensitive and prone to trade down or wait for promotions.

Levi balances premium positioning with value lines—Denizen and outlet channels—helping protect 2024 net revenue (US apparel market down ~1.5%) by retaining value-conscious buyers.

- Inflation peak 6.5% (2023)

- US real wages flat‑to‑down 2023–24

- Denizen/value lines soften downside

- Promotions rise in downturns

Information Transparency and Digital Comparison

- Instant price/review access raises buyer power

- 2024 DTC revenue $2.6B, +15% YoY

- Avg rating ~4.5/5 on major marketplaces

- Omnichannel focus reduces churn, protects margins

Moderate–High Customer Power: Wholesale Strength vs. Levi’s DTC, Loyalty & Margins

| Metric | 2024 |

|---|---|

| Wholesale net rev | $1.9B |

| Global brand rev | $3.9B |

| DTC revenue | $2.6B (30%) |

| Inventory turns | 3.5x |

| Loyalty members | ~3.6M |

| Marketing spend | $640M |

| Retail gross margin | ~60% |

| Wholesale gross margin | ~40% |

Same Document Delivered

Levi Strauss & Co. Porter's Five Forces Analysis

This preview shows the exact Levi Strauss & Co. Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted and ready for download and use the moment you buy. You're looking at the actual deliverable, complete and professionally written. No mockups or samples—what you see is what you'll get.