LG Display Business Model Canvas

LG Display: Compact Business Model Canvas for Investors & Strategists

Unlock the strategic blueprint behind LG Display with our concise Business Model Canvas—see how value propositions, key partners, and revenue streams combine to secure market leadership and innovation advantages; ideal for investors, consultants, and founders seeking actionable insights.

Partnerships

Strategic Alliances with LG Electronics and Group Affiliates

LG Display leverages a captive market with LG Electronics—supplying large OLED panels for TV and premium appliances—which accounted for about 28% of its 2024 panel shipments, enabling synchronized roadmaps and faster commercial launches.

Collaboration with LG Chem secures specialty chemicals and OLED organics, cutting input volatility; in 2024 the materials partnership supported a 12% yield improvement in Gen8 OLED lines, reducing per-panel defect costs.

Major Global Tech OEM Partnerships

LG Display is a critical supplier to top OEMs like Apple, supplying OLED/LPTO panels for high-end iPhones and iPads under multi-year contracts that in 2024 accounted for roughly 28% of panel revenue and supported ~$1.2bn in annual capex amortization.

These agreements require deep engineering co-development to meet flagship specs and secure high-volume orders—critical because a single 8.5G/6G fab line costs $2–3bn and needs sustained volumes to reach breakeven within 5–7 years.

Automotive Industry Collaborations

LG Display partners with premium automakers including Mercedes-Benz and Cadillac to integrate Plastic OLED (P-OLED) and Tandem OLED into curved dashboards and infotainment, targeting automotive revenue that rose to about $2.1 billion in 2024 and accounted for roughly 9% of company sales. These collaborations aim at high-margin digital cockpit orders—LGD projects automotive OLED capacity to reach ~1.2 million units/year by 2026, making autos a fast-growing pillar of its business model.

Upstream Material and Equipment Suppliers

Collaborations with suppliers like Idemitsu Kosan and Universal Display Corporation secure patented OLED emitters and equipment, helping LG Display improve material efficiency and brightness while avoiding tech obsolescence; in 2025 UDC reported ~$600m licensing revenue, underscoring critical IP value.

Securing these chains reduced production delays—LG Display’s 2024 capex was KRW 2.3trn, focused on OLED lines—to keep pace with demand and cut bottleneck risk.

- Access to UDC emitters: ~$600m licensing (2025)

- LGD capex: KRW 2.3trn (2024)

- Reduces tech obsolescence, improves brightness/material use

Joint Ventures and Academic Research Alliances

LG Display runs joint ventures and academic research alliances—partnering with universities and specialists—to develop micro-LED, stretchable displays, and advanced thin-film encapsulation, sharing high-risk R&D costs and accessing wider scientific talent pools.

- 2024 R&D spend: KRW 1.2 trillion; JV funding reduced LGD share ~20%

- Micro-LED pilots with universities since 2022; goal: 2026 commercial modules

- Stretchable display papers co-authored with 5 top labs (2023–25)

LG Display’s partner ecosystem fuels KRW2.3trn capex, $2.1bn auto sales, and faster OLED wins

LG Display’s key partners—LG Electronics, LG Chem, Apple, automakers (Mercedes, Cadillac), Idemitsu, Universal Display (UDC), and universities—secure demand, materials, IP, and R&D sharing; together they supported KRW 2.3trn capex (2024), KRW 1.2trn R&D (2024), ~$2.1bn auto revenue (2024), and UDC ~$600m licensing (2025), reducing yield defects and time-to-market.

| Partner | Role | Key 2024–25 Figure |

|---|---|---|

| LG Electronics | Captive demand | ~28% shipments |

| Apple | OEM contracts | ~28% panel revenue |

| Automakers | Auto OLED | $2.1bn revenue |

| UDC | Emitters/IP | $600m licensing (2025) |

| Suppliers/JVs | Materials/R&D | KRW1.2trn R&D; capex KRW2.3trn |

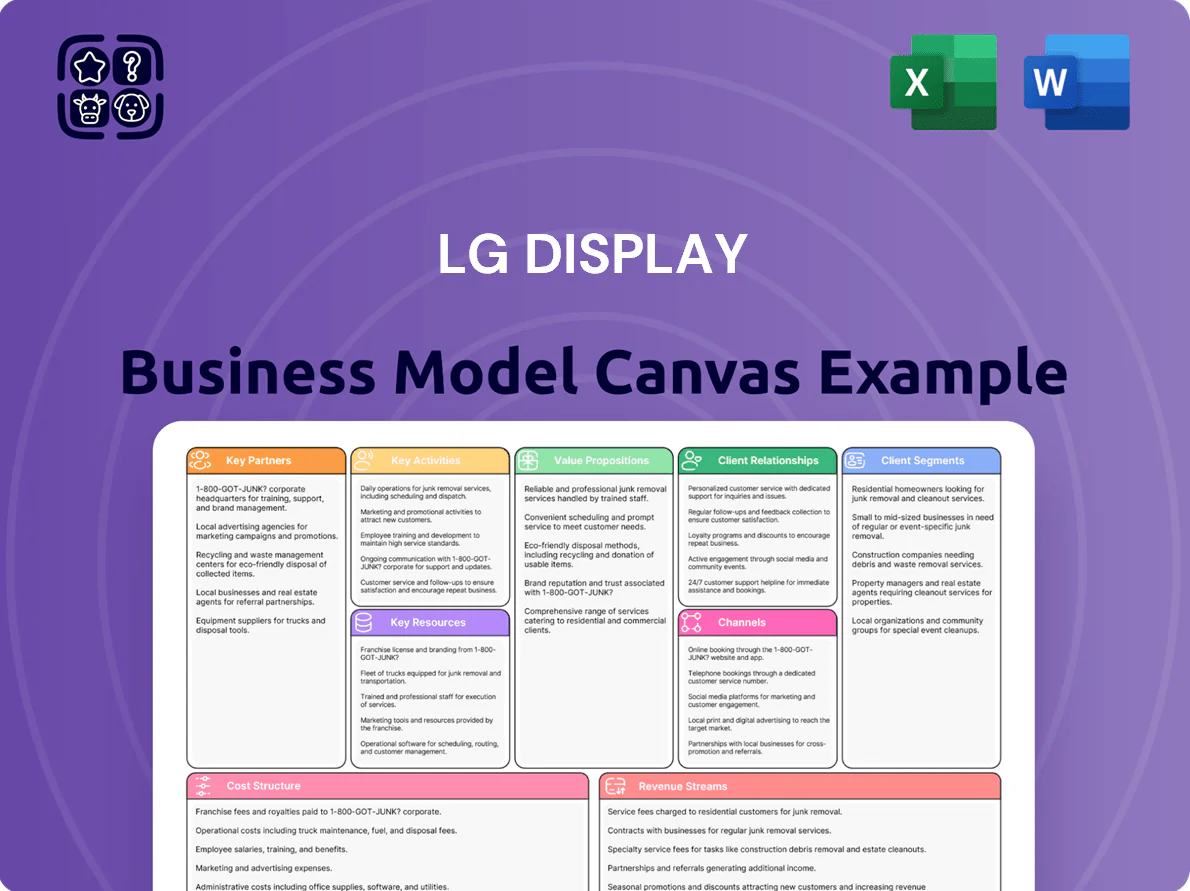

What is included in the product

A concise Business Model Canvas for LG Display mapping nine blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—reflecting its global OLED/LED display manufacturing, R&D-driven innovation, supply-chain partnerships, and diversified end-markets to support investor presentations and strategic analysis.

High-level view of LG Display’s business model with editable cells to quickly pinpoint value drivers, cost structures, and partner dependencies for faster strategic decisions.

Activities

Advanced R&D in OLED and Next-Gen Technologies

LG Display runs intensive lab R&D to boost OLED efficiency, lifespan and peak brightness, targeting a 15–20% EQE (external quantum efficiency) gain and 30% longer lifespan for commercial panels by 2027 based on current roadmaps; this reduces total cost of ownership versus LCDs. Engineers prioritize Tandem OLED stacks—stacking 2+ emissive layers—to meet IT and automotive reliability standards (aiming for 100,000+ hours) and defend market share as OLED revenue reached $6.2B in 2024.

High-Precision Mass Production and Fab Management

Operating massive fabs in South Korea and China, LG Display runs 8.6- and 10.5-generation lines that require tight control of vacuum deposition and encapsulation to hit yields; in 2024 the company reported capital expenditure of KRW 1.7 trillion for fab upgrades and achieved panel yield improvements that cut glass substrate waste by ~3.2% year-over-year. Efficient facility management sustains output of hundreds of millions of units while preserving global quality standards.

Yield Optimization and Quality Control

Maintaining high yields drives LG Displays profitability; a 1% yield improvement can raise gross margin by ~0.5–1.0 percentage points given 2024 panel ASPs and cost structure. The company uses AOI (automated optical inspection), inline electrical testing, and microscopic defect analytics to catch faults early, while engineering teams target daily yield gains for complex foldable and transparent OLEDs where current mass-production yields still trail rigid panels by 10–25%.

Strategic Supply Chain and Logistics Coordination

LG Display coordinates global flows of glass substrates, driver ICs and modules across hundreds of suppliers, targeting just-in-time delivery to its fabs to support 2024 capacity of ~18.5 million square meters of OLED/large-panel area; logistics aim to keep WIP inventory below industry norms to protect margins (FY2024 gross margin 7.1%).

It runs temperature-controlled, white-glove distribution to OEMs across Asia, Europe and North America, moving fragile panels with damage rates under 0.5% and reducing lead times by ~12% vs 2022 through route optimization and regional hubs.

- Just-in-time supply from hundreds of suppliers

- 2024 capacity ~18.5M m2 (OLED/large panels)

- FY2024 gross margin 7.1%

- Damage rates <0.5%

- Lead times cut ~12% since 2022

B2B Marketing and Client Relationship Management

LG Display targets B2B buyers by highlighting technical specs and reliability, not consumer branding; in 2024 the company cited a 12% year-over-year rise in commercial panel shipments as win evidence for enterprise contracts.

They attend MWC and Display Week and run private demos; sales engineers collaborate with client R&D to customize panels, reducing integration defects—LGD reported a 3.5% defect-rate drop in OEM integrations in 2024.

- Focus: technical specs, reliability

- Channels: Display Week, MWC, private demos

- Sales: joint engineering with clients

- 2024: +12% commercial shipments

- 2024: -3.5% integration defects

LG Display ramps OLED R&D, boosts capacity & margins with improved yield and shipments

LG Display runs advanced R&D (tandem OLED, EQE +15–20% by 2027), operates 8.6/10.5G fabs with 2024 capex KRW 1.7T and ~18.5M m2 capacity, targets JIT supply (WIP low), achieved FY2024 gross margin 7.1%, damage <0.5%, lead times −12% vs 2022, commercial shipments +12% in 2024, integration defects −3.5%.

| Metric | 2024/Target |

|---|---|

| CapEx | KRW 1.7T |

| Capacity | 18.5M m2 |

| Gross margin | 7.1% |

| Damage rate | <0.5% |

| Lead time | −12% vs 2022 |

| Commercial shipments | +12% YoY |

| Integration defects | −3.5% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the exact LG Display Business Model Canvas you will receive after purchase; it's not a mockup or excerpt but a direct snapshot of the final deliverable.

Upon completing your order, you'll get this same complete, professionally formatted file ready for editing and presenting in Word and Excel—no hidden pages or altered content.

We provide full transparency: what you see is what you'll download instantly after purchase, fully usable for analysis, strategy, or reporting.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

LG Display: Compact Business Model Canvas for Investors & Strategists

Unlock the strategic blueprint behind LG Display with our concise Business Model Canvas—see how value propositions, key partners, and revenue streams combine to secure market leadership and innovation advantages; ideal for investors, consultants, and founders seeking actionable insights.

Partnerships

Strategic Alliances with LG Electronics and Group Affiliates

LG Display leverages a captive market with LG Electronics—supplying large OLED panels for TV and premium appliances—which accounted for about 28% of its 2024 panel shipments, enabling synchronized roadmaps and faster commercial launches.

Collaboration with LG Chem secures specialty chemicals and OLED organics, cutting input volatility; in 2024 the materials partnership supported a 12% yield improvement in Gen8 OLED lines, reducing per-panel defect costs.

Major Global Tech OEM Partnerships

LG Display is a critical supplier to top OEMs like Apple, supplying OLED/LPTO panels for high-end iPhones and iPads under multi-year contracts that in 2024 accounted for roughly 28% of panel revenue and supported ~$1.2bn in annual capex amortization.

These agreements require deep engineering co-development to meet flagship specs and secure high-volume orders—critical because a single 8.5G/6G fab line costs $2–3bn and needs sustained volumes to reach breakeven within 5–7 years.

Automotive Industry Collaborations

LG Display partners with premium automakers including Mercedes-Benz and Cadillac to integrate Plastic OLED (P-OLED) and Tandem OLED into curved dashboards and infotainment, targeting automotive revenue that rose to about $2.1 billion in 2024 and accounted for roughly 9% of company sales. These collaborations aim at high-margin digital cockpit orders—LGD projects automotive OLED capacity to reach ~1.2 million units/year by 2026, making autos a fast-growing pillar of its business model.

Upstream Material and Equipment Suppliers

Collaborations with suppliers like Idemitsu Kosan and Universal Display Corporation secure patented OLED emitters and equipment, helping LG Display improve material efficiency and brightness while avoiding tech obsolescence; in 2025 UDC reported ~$600m licensing revenue, underscoring critical IP value.

Securing these chains reduced production delays—LG Display’s 2024 capex was KRW 2.3trn, focused on OLED lines—to keep pace with demand and cut bottleneck risk.

- Access to UDC emitters: ~$600m licensing (2025)

- LGD capex: KRW 2.3trn (2024)

- Reduces tech obsolescence, improves brightness/material use

Joint Ventures and Academic Research Alliances

LG Display runs joint ventures and academic research alliances—partnering with universities and specialists—to develop micro-LED, stretchable displays, and advanced thin-film encapsulation, sharing high-risk R&D costs and accessing wider scientific talent pools.

- 2024 R&D spend: KRW 1.2 trillion; JV funding reduced LGD share ~20%

- Micro-LED pilots with universities since 2022; goal: 2026 commercial modules

- Stretchable display papers co-authored with 5 top labs (2023–25)

LG Display’s partner ecosystem fuels KRW2.3trn capex, $2.1bn auto sales, and faster OLED wins

LG Display’s key partners—LG Electronics, LG Chem, Apple, automakers (Mercedes, Cadillac), Idemitsu, Universal Display (UDC), and universities—secure demand, materials, IP, and R&D sharing; together they supported KRW 2.3trn capex (2024), KRW 1.2trn R&D (2024), ~$2.1bn auto revenue (2024), and UDC ~$600m licensing (2025), reducing yield defects and time-to-market.

| Partner | Role | Key 2024–25 Figure |

|---|---|---|

| LG Electronics | Captive demand | ~28% shipments |

| Apple | OEM contracts | ~28% panel revenue |

| Automakers | Auto OLED | $2.1bn revenue |

| UDC | Emitters/IP | $600m licensing (2025) |

| Suppliers/JVs | Materials/R&D | KRW1.2trn R&D; capex KRW2.3trn |

What is included in the product

A concise Business Model Canvas for LG Display mapping nine blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—reflecting its global OLED/LED display manufacturing, R&D-driven innovation, supply-chain partnerships, and diversified end-markets to support investor presentations and strategic analysis.

High-level view of LG Display’s business model with editable cells to quickly pinpoint value drivers, cost structures, and partner dependencies for faster strategic decisions.

Activities

Advanced R&D in OLED and Next-Gen Technologies

LG Display runs intensive lab R&D to boost OLED efficiency, lifespan and peak brightness, targeting a 15–20% EQE (external quantum efficiency) gain and 30% longer lifespan for commercial panels by 2027 based on current roadmaps; this reduces total cost of ownership versus LCDs. Engineers prioritize Tandem OLED stacks—stacking 2+ emissive layers—to meet IT and automotive reliability standards (aiming for 100,000+ hours) and defend market share as OLED revenue reached $6.2B in 2024.

High-Precision Mass Production and Fab Management

Operating massive fabs in South Korea and China, LG Display runs 8.6- and 10.5-generation lines that require tight control of vacuum deposition and encapsulation to hit yields; in 2024 the company reported capital expenditure of KRW 1.7 trillion for fab upgrades and achieved panel yield improvements that cut glass substrate waste by ~3.2% year-over-year. Efficient facility management sustains output of hundreds of millions of units while preserving global quality standards.

Yield Optimization and Quality Control

Maintaining high yields drives LG Displays profitability; a 1% yield improvement can raise gross margin by ~0.5–1.0 percentage points given 2024 panel ASPs and cost structure. The company uses AOI (automated optical inspection), inline electrical testing, and microscopic defect analytics to catch faults early, while engineering teams target daily yield gains for complex foldable and transparent OLEDs where current mass-production yields still trail rigid panels by 10–25%.

Strategic Supply Chain and Logistics Coordination

LG Display coordinates global flows of glass substrates, driver ICs and modules across hundreds of suppliers, targeting just-in-time delivery to its fabs to support 2024 capacity of ~18.5 million square meters of OLED/large-panel area; logistics aim to keep WIP inventory below industry norms to protect margins (FY2024 gross margin 7.1%).

It runs temperature-controlled, white-glove distribution to OEMs across Asia, Europe and North America, moving fragile panels with damage rates under 0.5% and reducing lead times by ~12% vs 2022 through route optimization and regional hubs.

- Just-in-time supply from hundreds of suppliers

- 2024 capacity ~18.5M m2 (OLED/large panels)

- FY2024 gross margin 7.1%

- Damage rates <0.5%

- Lead times cut ~12% since 2022

B2B Marketing and Client Relationship Management

LG Display targets B2B buyers by highlighting technical specs and reliability, not consumer branding; in 2024 the company cited a 12% year-over-year rise in commercial panel shipments as win evidence for enterprise contracts.

They attend MWC and Display Week and run private demos; sales engineers collaborate with client R&D to customize panels, reducing integration defects—LGD reported a 3.5% defect-rate drop in OEM integrations in 2024.

- Focus: technical specs, reliability

- Channels: Display Week, MWC, private demos

- Sales: joint engineering with clients

- 2024: +12% commercial shipments

- 2024: -3.5% integration defects

LG Display ramps OLED R&D, boosts capacity & margins with improved yield and shipments

LG Display runs advanced R&D (tandem OLED, EQE +15–20% by 2027), operates 8.6/10.5G fabs with 2024 capex KRW 1.7T and ~18.5M m2 capacity, targets JIT supply (WIP low), achieved FY2024 gross margin 7.1%, damage <0.5%, lead times −12% vs 2022, commercial shipments +12% in 2024, integration defects −3.5%.

| Metric | 2024/Target |

|---|---|

| CapEx | KRW 1.7T |

| Capacity | 18.5M m2 |

| Gross margin | 7.1% |

| Damage rate | <0.5% |

| Lead time | −12% vs 2022 |

| Commercial shipments | +12% YoY |

| Integration defects | −3.5% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the exact LG Display Business Model Canvas you will receive after purchase; it's not a mockup or excerpt but a direct snapshot of the final deliverable.

Upon completing your order, you'll get this same complete, professionally formatted file ready for editing and presenting in Word and Excel—no hidden pages or altered content.

We provide full transparency: what you see is what you'll download instantly after purchase, fully usable for analysis, strategy, or reporting.