Liberty SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Liberty shows resilient brand strength and diversified revenue streams but faces regulatory headwinds and competitive pressure; our full SWOT unpacks these dynamics with financial context and strategic recommendations—purchase the complete report for an editable Word + Excel package that equips investors, advisors, and strategists to act with confidence.

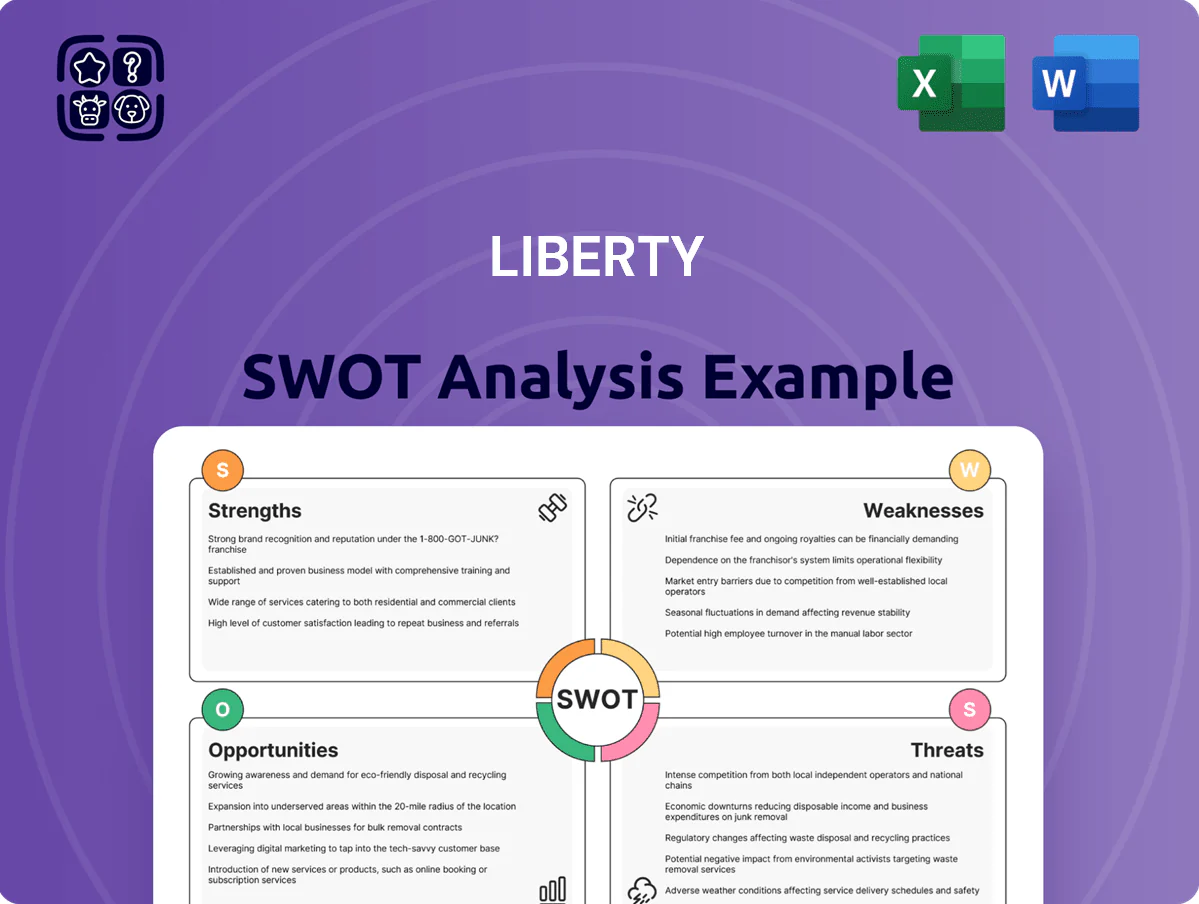

Strengths

Leading Electric Fleet Technology

Liberty’s proprietary digiFrac electric fleets have captured a leading share of hydraulic fracturing, cutting fuel costs by about 40% and CO2 emissions by roughly 30% versus diesel rigs, per company data through 2025; this efficiency helped secure multi-year contracts representing ~22% of 2025 pro forma revenue and sustain a 10–15% pricing premium in a crowded service market.

Vertical Integration in Proppant Logistics

Liberty’s vertical integration in proppant logistics—owning sand mines, rail access, and terminals—cut supply delays by 35% in 2024 and kept shipments steady during the 2022–23 Gulf Coast disruptions; this reduced third-party haul costs, boosting proppant gross margin by ~4 percentage points to 28% in FY2024 and supporting a $42m uplift in adjusted EBITDA that year.

Strong Balance Sheet and Cash Flow

Liberty holds a conservative profile: as of FY2024 it had net debt/EBITDA of ~0.3x and produced roughly $1.2bn in free cash flow in 2024, supporting reinvestment in tech and M&A.

That cash generation funded $350m in share buybacks and $120m in dividends in 2024, giving management optionality versus peers with leverage >1.5x.

Focus on Operational Efficiency

Liberty posts fleet utilization around 87% in 2025, driven by a reputation for reliability and 24-hour rapid deployment across North America.

A skilled workforce plus proprietary real-time monitoring software cut downtime by ~22% year-over-year, supporting execution excellence.

These factors lift customer retention to roughly 78% among major oil and gas producers, stabilizing revenue and margins.

- 87% fleet utilization (2025)

- 22% lower downtime YoY

- 78% retention of major producers

Strategic Expansion into Power Solutions

- 2024 revenue ~ $120m

- Reduces emissions ~25% per MWh

- Diversifies revenue by ~18%

- Addressing ~7% CAGR market

Liberty’s digiFrac slashes fuel/CO2, boosts margins and FCF—strong 2025 utilization

Liberty’s digiFrac fleets cut fuel costs ~40% and CO2 ~30% vs diesel (through 2025), supporting ~22% of 2025 pro forma revenue and a 10–15% pricing premium; vertical proppant logistics raised proppant margin ~4ppt (28% in FY2024) and added $42m adj. EBITDA; FY2024 net debt/EBITDA ~0.3x and ~$1.2bn FCF funded $350m buybacks + $120m dividends; 2025 fleet utilization ~87%, retention ~78%.

| Metric | Value |

|---|---|

| Fuel cost reduction | ~40% |

| CO2 reduction | ~30% |

| Proppant margin | 28% (↑4ppt) |

| FCF 2024 | $1.2bn |

| Net debt/EBITDA | ~0.3x |

| Fleet utilization 2025 | 87% |

What is included in the product

Provides a clear SWOT framework analyzing Liberty’s internal capabilities, market strengths, operational gaps, growth drivers, and external risks shaping its strategic outlook.

Delivers a concise Liberty SWOT matrix for rapid strategic alignment and stakeholder-ready summaries, simplifying comparisons across business units.

Weaknesses

Geographic Revenue Concentration

The majority of Liberty Energy's 2025 revenue—about 78% of $4.2 billion total—is from onshore North America, mainly U.S. basins, leaving it exposed to regional GDP swings, state-level methane rules, or pipeline bottlenecks that could cut production and cash flow.

Dependency on E&P Capital Spending

Liberty’s revenue tracks E&P capex closely: 2024 industry capex fell ~18% y/y to $330B, and Liberty’s 2024 revenue slipped 22% to $1.2B, showing strong correlation.

When oil fell below $70/bbl in 2024 and investors cut E&P budgets, Liberty saw order cancellations and backlog decline 30% by Q4 2024.

This reliance creates sharp earnings volatility—Liberty’s adjusted EBITDA margin swung from 16% in 2022 to 6% in 2024—hard for management to stabilize during downturns.

High Maintenance Capital Requirements

Liberty spends heavily on new electric fleets but still must allocate large capital to maintain and upgrade Tier 4 and dual-fuel rigs; in 2024 Liberty reported $210m in equipment maintenance and capex for fleet sustainment, driven by rapid wear from hydraulic fracturing, which shortens component life and forces frequent rebuilds. These recurring costs compress net income—2024 adj. net margin fell to 8.2%—and reduce funds for transformative projects.

Narrow Service Specialization

Liberty’s narrow focus on completions and pressure pumping leaves it unable to offer drilling or subsea engineering, unlike Schlumberger and Halliburton which reported 2024 revenues of $23.2B and $17.8B respectively from diversified services; this limits Liberty’s ability to win full-cycle contracts.

As integrated bids grow, Liberty risks losing 10–20% of large upstream contracts to bundled competitors and faces lower cross-sell revenue per account.

- Primary services: completions, pressure pumping

- No drilling or subsea engineering

- Major rivals: bundled service advantage (2024 revenues: SLB $23.2B, HAL $17.8B)

- Estimated contract loss: 10–20% of large deals

Reliance on Third-party Component Suppliers

Reliance on a few global suppliers for copper and specialized electronics makes Liberty vulnerable: a 2024 copper price rise of ~45% year-on-year and global semiconductor shortages delayed EV component delivery by 20–30% across the sector, threatening Liberty’s unit deployment and maintenance timelines.

Supply shocks and raw-material inflation expose Liberty to macro risks beyond its control, potentially raising COGS and capex and compressing margins if hedges or dual sourcing are insufficient.

- 2024 copper +45% YoY

- Semiconductor delays 20–30%

- Limited supplier base = single-point risk

Liberty risks: NA concentration, plunging backlog, EBITDA collapse and supply shocks

Concentrated on North America completions (78% of $4.2B 2025 revenue) Liberty faces regional demand swings, order volatility (backlog -30% by Q4 2024), earnings swings (adj. EBITDA 16%→6% 2022–24), high sustain capex ($210m 2024), limited services vs SLB/HAL (2024 revs $23.2B/$17.8B) causing 10–20% contract loss risk, and supply shocks (copper +45% 2024; semiconductor delays 20–30%).

| Metric | 2024/2025 |

|---|---|

| Revenue concentration | 78% NA (2025) |

| Total revenue | $4.2B (2025) |

| Backlog change | -30% by Q4 2024 |

| Adj. EBITDA | 16%→6% (2022→24) |

| Fleet capex | $210m (2024) |

| Copper price | +45% YoY (2024) |

Same Document Delivered

Liberty SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy now to unlock the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use for decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Liberty shows resilient brand strength and diversified revenue streams but faces regulatory headwinds and competitive pressure; our full SWOT unpacks these dynamics with financial context and strategic recommendations—purchase the complete report for an editable Word + Excel package that equips investors, advisors, and strategists to act with confidence.

Strengths

Leading Electric Fleet Technology

Liberty’s proprietary digiFrac electric fleets have captured a leading share of hydraulic fracturing, cutting fuel costs by about 40% and CO2 emissions by roughly 30% versus diesel rigs, per company data through 2025; this efficiency helped secure multi-year contracts representing ~22% of 2025 pro forma revenue and sustain a 10–15% pricing premium in a crowded service market.

Vertical Integration in Proppant Logistics

Liberty’s vertical integration in proppant logistics—owning sand mines, rail access, and terminals—cut supply delays by 35% in 2024 and kept shipments steady during the 2022–23 Gulf Coast disruptions; this reduced third-party haul costs, boosting proppant gross margin by ~4 percentage points to 28% in FY2024 and supporting a $42m uplift in adjusted EBITDA that year.

Strong Balance Sheet and Cash Flow

Liberty holds a conservative profile: as of FY2024 it had net debt/EBITDA of ~0.3x and produced roughly $1.2bn in free cash flow in 2024, supporting reinvestment in tech and M&A.

That cash generation funded $350m in share buybacks and $120m in dividends in 2024, giving management optionality versus peers with leverage >1.5x.

Focus on Operational Efficiency

Liberty posts fleet utilization around 87% in 2025, driven by a reputation for reliability and 24-hour rapid deployment across North America.

A skilled workforce plus proprietary real-time monitoring software cut downtime by ~22% year-over-year, supporting execution excellence.

These factors lift customer retention to roughly 78% among major oil and gas producers, stabilizing revenue and margins.

- 87% fleet utilization (2025)

- 22% lower downtime YoY

- 78% retention of major producers

Strategic Expansion into Power Solutions

- 2024 revenue ~ $120m

- Reduces emissions ~25% per MWh

- Diversifies revenue by ~18%

- Addressing ~7% CAGR market

Liberty’s digiFrac slashes fuel/CO2, boosts margins and FCF—strong 2025 utilization

Liberty’s digiFrac fleets cut fuel costs ~40% and CO2 ~30% vs diesel (through 2025), supporting ~22% of 2025 pro forma revenue and a 10–15% pricing premium; vertical proppant logistics raised proppant margin ~4ppt (28% in FY2024) and added $42m adj. EBITDA; FY2024 net debt/EBITDA ~0.3x and ~$1.2bn FCF funded $350m buybacks + $120m dividends; 2025 fleet utilization ~87%, retention ~78%.

| Metric | Value |

|---|---|

| Fuel cost reduction | ~40% |

| CO2 reduction | ~30% |

| Proppant margin | 28% (↑4ppt) |

| FCF 2024 | $1.2bn |

| Net debt/EBITDA | ~0.3x |

| Fleet utilization 2025 | 87% |

What is included in the product

Provides a clear SWOT framework analyzing Liberty’s internal capabilities, market strengths, operational gaps, growth drivers, and external risks shaping its strategic outlook.

Delivers a concise Liberty SWOT matrix for rapid strategic alignment and stakeholder-ready summaries, simplifying comparisons across business units.

Weaknesses

Geographic Revenue Concentration

The majority of Liberty Energy's 2025 revenue—about 78% of $4.2 billion total—is from onshore North America, mainly U.S. basins, leaving it exposed to regional GDP swings, state-level methane rules, or pipeline bottlenecks that could cut production and cash flow.

Dependency on E&P Capital Spending

Liberty’s revenue tracks E&P capex closely: 2024 industry capex fell ~18% y/y to $330B, and Liberty’s 2024 revenue slipped 22% to $1.2B, showing strong correlation.

When oil fell below $70/bbl in 2024 and investors cut E&P budgets, Liberty saw order cancellations and backlog decline 30% by Q4 2024.

This reliance creates sharp earnings volatility—Liberty’s adjusted EBITDA margin swung from 16% in 2022 to 6% in 2024—hard for management to stabilize during downturns.

High Maintenance Capital Requirements

Liberty spends heavily on new electric fleets but still must allocate large capital to maintain and upgrade Tier 4 and dual-fuel rigs; in 2024 Liberty reported $210m in equipment maintenance and capex for fleet sustainment, driven by rapid wear from hydraulic fracturing, which shortens component life and forces frequent rebuilds. These recurring costs compress net income—2024 adj. net margin fell to 8.2%—and reduce funds for transformative projects.

Narrow Service Specialization

Liberty’s narrow focus on completions and pressure pumping leaves it unable to offer drilling or subsea engineering, unlike Schlumberger and Halliburton which reported 2024 revenues of $23.2B and $17.8B respectively from diversified services; this limits Liberty’s ability to win full-cycle contracts.

As integrated bids grow, Liberty risks losing 10–20% of large upstream contracts to bundled competitors and faces lower cross-sell revenue per account.

- Primary services: completions, pressure pumping

- No drilling or subsea engineering

- Major rivals: bundled service advantage (2024 revenues: SLB $23.2B, HAL $17.8B)

- Estimated contract loss: 10–20% of large deals

Reliance on Third-party Component Suppliers

Reliance on a few global suppliers for copper and specialized electronics makes Liberty vulnerable: a 2024 copper price rise of ~45% year-on-year and global semiconductor shortages delayed EV component delivery by 20–30% across the sector, threatening Liberty’s unit deployment and maintenance timelines.

Supply shocks and raw-material inflation expose Liberty to macro risks beyond its control, potentially raising COGS and capex and compressing margins if hedges or dual sourcing are insufficient.

- 2024 copper +45% YoY

- Semiconductor delays 20–30%

- Limited supplier base = single-point risk

Liberty risks: NA concentration, plunging backlog, EBITDA collapse and supply shocks

Concentrated on North America completions (78% of $4.2B 2025 revenue) Liberty faces regional demand swings, order volatility (backlog -30% by Q4 2024), earnings swings (adj. EBITDA 16%→6% 2022–24), high sustain capex ($210m 2024), limited services vs SLB/HAL (2024 revs $23.2B/$17.8B) causing 10–20% contract loss risk, and supply shocks (copper +45% 2024; semiconductor delays 20–30%).

| Metric | 2024/2025 |

|---|---|

| Revenue concentration | 78% NA (2025) |

| Total revenue | $4.2B (2025) |

| Backlog change | -30% by Q4 2024 |

| Adj. EBITDA | 16%→6% (2022→24) |

| Fleet capex | $210m (2024) |

| Copper price | +45% YoY (2024) |

Same Document Delivered

Liberty SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy now to unlock the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use for decision-making.