Life Insurance Corp. of India PESTLE Analysis

Your Competitive Advantage Starts with This Report

Uncover how political shifts, economic trends, social demographics, and technological advances are shaping Life Insurance Corp. of India's prospects with our concise PESTLE snapshot—perfect for investors and strategists seeking actionable external insights; buy the full analysis for a detailed, ready-to-use report you can download instantly.

Political factors

Government Ownership and Strategic Influence

The Indian government holds a 54.86% stake in LIC after its 2022 IPO, aligning LIC’s strategic objectives with national priorities and ensuring sovereign trust; this ownership often directs LIC to support public infrastructure and state enterprises, and political mandates can shape investment allocation. Dividend decisions are regularly influenced by government fiscal needs—LIC paid a dividend of Rs 3,606 crore in FY2024 amid budgetary pressures.

Insurance for All by 2047 Mandate

The government’s Insurance for All by 2047 mandate pushes LIC to scale rural outreach via Bima Vistaar, increasing rural policy issuance—rural premiums grew ~12% in FY2024 to ₹45,000 crore—requiring reallocation of agents, tech and CSR spend toward low-margin social products. State-led targets make social coverage a KPI for LIC leadership; meeting them influences regulator and political goodwill, affecting LIC’s long-term market share (LIC held ~68% individual life market share in 2024).

FDI Policy and Global Competition

Political decisions to raise FDI limits in insurance to 74% (from 49% in 2021) have intensified competition for LIC, inviting global players with deep pockets. As India’s insurance premium market grew 12.4% in FY2024 to about INR 11.1 trillion, private entrants deploy advanced tech and niche products targeting urban segments. LIC’s ability to defend its 60%+ market share hinges on rapid digital adoption, product innovation, and capital raises to match foreign-backed rivals.

Public Sector Divestment Strategy

As a listed entity, LIC is central to the government’s disinvestment roadmap; the 2022 IPO reduced government holding to 51% and subsequent stake sale plans have driven episodic volatility in LIC share price (FY2024 trading range ~₹500–₹650).

Political timing and scale of offerings—often aligned with fiscal targets—shape investor sentiment and force LIC to balance public service mandates with shareholder returns; planned follow-on sales in 2024–25 target further reduction of government stake.

Geopolitical Stability and Asset Valuation

India's sustained political stability through 2025 supports LIC's Rs 46 trillion investment book, enhancing confidence in long-duration holdings across infrastructure, banking and energy sectors.

Many assets are sensitive to trade and security policies; for example, 18% of LIC's equity exposure is in sectors tied to national security and imports, making valuations vulnerable to geopolitical shocks.

Significant regional tensions could pressure sovereign and corporate bond spreads, risking mark-to-market losses that would affect LIC's solvency ratios and capital adequacy.

- Rs 46 trillion total investments (2025)

- ~18% exposure in security/trade-sensitive sectors

- Geopolitical shocks may widen bond spreads and hit solvency

LIC: Govt 51% Control, ₹46tn Assets, 68% Share — Volatility as FDI, Dividends Rise

Govt 51% stake post-2022 IPO ties LIC to fiscal priorities; dividend and stake-sales (planned 2024–25) drive volatility—FY2024 share range ~₹500–₹650. Govt Insurance for All to 2047 raised rural premiums ~12% in FY2024 (₹45,000 crore) and kept LIC individual market share ~68% (2024). FDI rise to 74% intensifies competition as India premium market reached ₹11.1 tn in FY2024; LIC investments ~₹46 tn (2025).

| Metric | Value |

|---|---|

| Govt stake | 51% |

| LIC investments | ₹46 tn (2025) |

| Market share | ~68% (2024) |

| India premiums | ₹11.1 tn (FY2024) |

What is included in the product

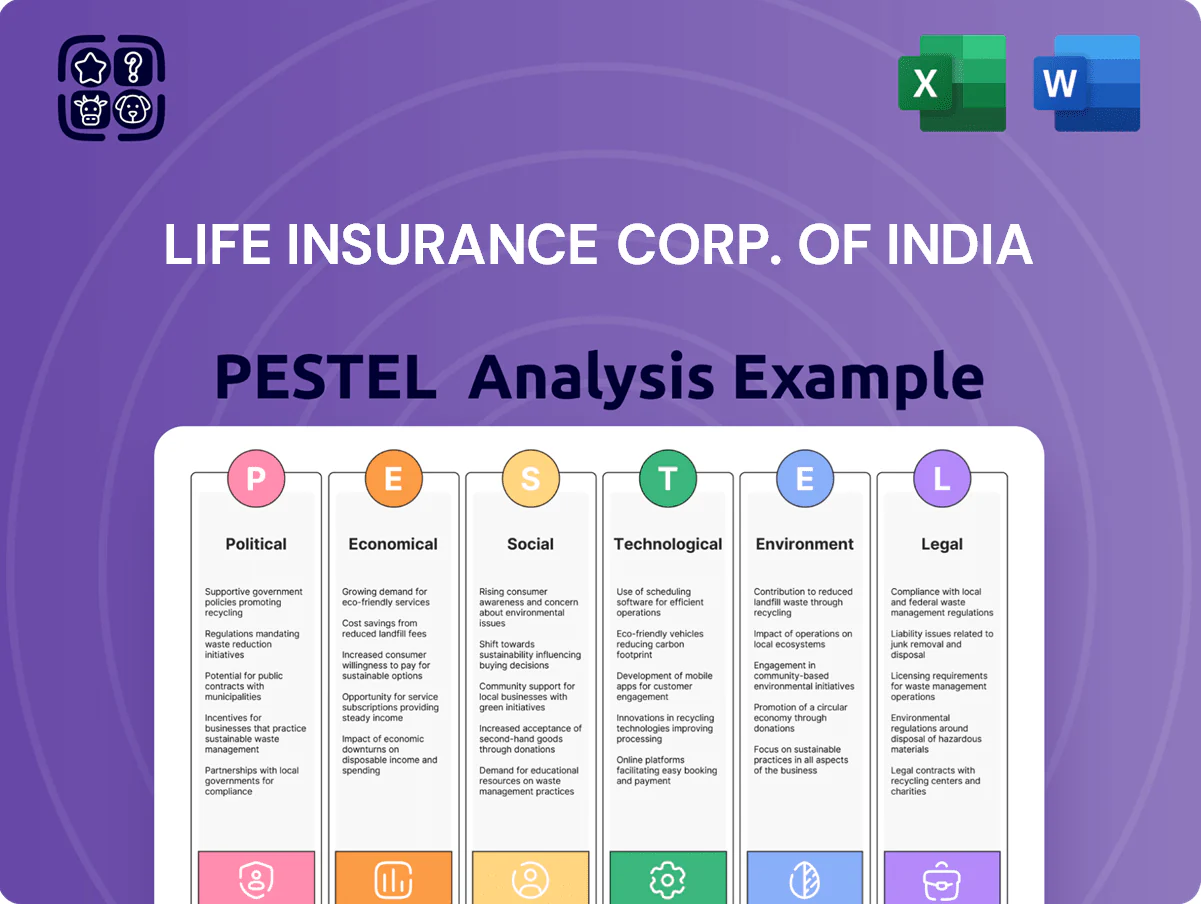

Explores how external macro-environmental factors uniquely affect the Life Insurance Corp. of India across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed, region-specific insights and forward-looking implications to help executives, consultants, and investors identify risks and opportunities for strategic planning and capital allocation.

A concise PESTLE summary for Life Insurance Corp. of India that’s visually segmented and editable, enabling quick risk assessment and slide-ready copy for meetings, team alignment, or client reports.

Economic factors

Interest Rate Environment and Yields

Fluctuations in the Reserve Bank of India’s repo rate (raised from 6.50% in May 2022 to 6.75% by Dec 2023 and standing at 6.50%–6.75% through 2024–25 policy shifts) directly affect returns on LIC’s ~₹46 trillion fixed-income portfolio (FY24). Volatile rates strain LIC’s ability to honor guaranteed returns on traditional policies while protecting margins. Rising yields can trigger mark-to-market losses; falling rates compress spreads needed for long-term solvency.

GDP Growth and Household Savings

India’s 2024 GDP growth estimate of about 6.8% supports rising household disposable income, boosting capacity for insurance and long-term savings.

Higher growth is driving a shift from gold and real estate toward financial assets; financial savings rate rose to ~8.6% of GDP in 2023–24, aiding demand for life cover.

LIC’s premium growth tracks middle-class expansion—urban households grew to ~462 million in 2024—fuelling higher annual new business premium and persistence rates.

Equity Market Volatility

As India’s largest institutional investor, Life Insurance Corp. of India holds over Rs 16 trillion in equities (FY2024), making its balance sheet highly sensitive to NSE and BSE movements.

Bull markets lifted LIC’s embedded value and solvency—market gains contributed to a reported Rs 1.2 trillion uptick in investment income in FY2024—supporting higher terminal bonuses.

Prolonged downturns compress unrealized gains and pressure solvency margins, forcing LIC to reallocate to lower-risk assets and adjust bonus declarations to protect policyholder interests.

Inflationary Pressures on Operations

Persistent inflation raised India’s CPI to 6.5% in 2023-24, increasing LIC’s operating costs for 2,000+ branch offices and ~13 million agents through higher rents, utilities and commissions, squeezing margins on traditional products.

High inflation erodes real value of future payouts—a 6% inflation reduces 10-year guaranteed benefits by ~44% in real terms—making endowments less attractive to inflation-aware customers.

LIC must accelerate inflation-hedged offerings and market-linked plans; in FY2024 LIC collected ₹6.5 trillion in new business premium, signalling scale to innovate product mix and preserve competitiveness.

- Inflation (CPI 2023-24 ~6.5%) raises operating and agent costs

- 6% inflation cuts 10-year real value of guarantees by ~44%

- FY2024 NBP ₹6.5 trillion provides room to launch market-linked/inflation-protected products

Labor Market Formalization

The increasing formalization of India’s workforce — formal sector employment rising to 31% of total employment by 2023 per CMIE — expands LIC’s addressable market for group insurance and pension schemes, boosting premium volumes and persistence.

Shifts from unorganized to organized employment improve premium collection efficiency and reduce lapses, enabling LIC to win large corporate accounts via its agency channel; public sector and private corporate hiring grew ~6.5% YoY in 2024.

LIC under rate pressure: ₹46T bonds, ₹6.5T NBP amid rising CPI and strong GDP

Economic factors: RBI rate volatility (repo ~6.50–6.75% through 2024–25) impacts LIC’s ~₹46T fixed-income portfolio and guarantees; FY24 NBP ₹6.5T enables product shifts; India GDP ~6.8% (2024) and formal employment ~31% (2023) expand demand; CPI ~6.5% (2023–24) raises costs and erodes real guarantees.

| Metric | Value |

|---|---|

| Fixed-income AUM | ₹46T (FY24) |

| NBP | ₹6.5T (FY24) |

| GDP growth | ~6.8% (2024) |

| CPI | 6.5% (2023–24) |

| Formal employment | 31% (2023) |

Full Version Awaits

Life Insurance Corp. of India PESTLE Analysis

The preview shown here is the exact PESTLE analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for assessing Life Insurance Corp. of India’s political, economic, social, technological, legal, and environmental factors.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Uncover how political shifts, economic trends, social demographics, and technological advances are shaping Life Insurance Corp. of India's prospects with our concise PESTLE snapshot—perfect for investors and strategists seeking actionable external insights; buy the full analysis for a detailed, ready-to-use report you can download instantly.

Political factors

Government Ownership and Strategic Influence

The Indian government holds a 54.86% stake in LIC after its 2022 IPO, aligning LIC’s strategic objectives with national priorities and ensuring sovereign trust; this ownership often directs LIC to support public infrastructure and state enterprises, and political mandates can shape investment allocation. Dividend decisions are regularly influenced by government fiscal needs—LIC paid a dividend of Rs 3,606 crore in FY2024 amid budgetary pressures.

Insurance for All by 2047 Mandate

The government’s Insurance for All by 2047 mandate pushes LIC to scale rural outreach via Bima Vistaar, increasing rural policy issuance—rural premiums grew ~12% in FY2024 to ₹45,000 crore—requiring reallocation of agents, tech and CSR spend toward low-margin social products. State-led targets make social coverage a KPI for LIC leadership; meeting them influences regulator and political goodwill, affecting LIC’s long-term market share (LIC held ~68% individual life market share in 2024).

FDI Policy and Global Competition

Political decisions to raise FDI limits in insurance to 74% (from 49% in 2021) have intensified competition for LIC, inviting global players with deep pockets. As India’s insurance premium market grew 12.4% in FY2024 to about INR 11.1 trillion, private entrants deploy advanced tech and niche products targeting urban segments. LIC’s ability to defend its 60%+ market share hinges on rapid digital adoption, product innovation, and capital raises to match foreign-backed rivals.

Public Sector Divestment Strategy

As a listed entity, LIC is central to the government’s disinvestment roadmap; the 2022 IPO reduced government holding to 51% and subsequent stake sale plans have driven episodic volatility in LIC share price (FY2024 trading range ~₹500–₹650).

Political timing and scale of offerings—often aligned with fiscal targets—shape investor sentiment and force LIC to balance public service mandates with shareholder returns; planned follow-on sales in 2024–25 target further reduction of government stake.

Geopolitical Stability and Asset Valuation

India's sustained political stability through 2025 supports LIC's Rs 46 trillion investment book, enhancing confidence in long-duration holdings across infrastructure, banking and energy sectors.

Many assets are sensitive to trade and security policies; for example, 18% of LIC's equity exposure is in sectors tied to national security and imports, making valuations vulnerable to geopolitical shocks.

Significant regional tensions could pressure sovereign and corporate bond spreads, risking mark-to-market losses that would affect LIC's solvency ratios and capital adequacy.

- Rs 46 trillion total investments (2025)

- ~18% exposure in security/trade-sensitive sectors

- Geopolitical shocks may widen bond spreads and hit solvency

LIC: Govt 51% Control, ₹46tn Assets, 68% Share — Volatility as FDI, Dividends Rise

Govt 51% stake post-2022 IPO ties LIC to fiscal priorities; dividend and stake-sales (planned 2024–25) drive volatility—FY2024 share range ~₹500–₹650. Govt Insurance for All to 2047 raised rural premiums ~12% in FY2024 (₹45,000 crore) and kept LIC individual market share ~68% (2024). FDI rise to 74% intensifies competition as India premium market reached ₹11.1 tn in FY2024; LIC investments ~₹46 tn (2025).

| Metric | Value |

|---|---|

| Govt stake | 51% |

| LIC investments | ₹46 tn (2025) |

| Market share | ~68% (2024) |

| India premiums | ₹11.1 tn (FY2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Life Insurance Corp. of India across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed, region-specific insights and forward-looking implications to help executives, consultants, and investors identify risks and opportunities for strategic planning and capital allocation.

A concise PESTLE summary for Life Insurance Corp. of India that’s visually segmented and editable, enabling quick risk assessment and slide-ready copy for meetings, team alignment, or client reports.

Economic factors

Interest Rate Environment and Yields

Fluctuations in the Reserve Bank of India’s repo rate (raised from 6.50% in May 2022 to 6.75% by Dec 2023 and standing at 6.50%–6.75% through 2024–25 policy shifts) directly affect returns on LIC’s ~₹46 trillion fixed-income portfolio (FY24). Volatile rates strain LIC’s ability to honor guaranteed returns on traditional policies while protecting margins. Rising yields can trigger mark-to-market losses; falling rates compress spreads needed for long-term solvency.

GDP Growth and Household Savings

India’s 2024 GDP growth estimate of about 6.8% supports rising household disposable income, boosting capacity for insurance and long-term savings.

Higher growth is driving a shift from gold and real estate toward financial assets; financial savings rate rose to ~8.6% of GDP in 2023–24, aiding demand for life cover.

LIC’s premium growth tracks middle-class expansion—urban households grew to ~462 million in 2024—fuelling higher annual new business premium and persistence rates.

Equity Market Volatility

As India’s largest institutional investor, Life Insurance Corp. of India holds over Rs 16 trillion in equities (FY2024), making its balance sheet highly sensitive to NSE and BSE movements.

Bull markets lifted LIC’s embedded value and solvency—market gains contributed to a reported Rs 1.2 trillion uptick in investment income in FY2024—supporting higher terminal bonuses.

Prolonged downturns compress unrealized gains and pressure solvency margins, forcing LIC to reallocate to lower-risk assets and adjust bonus declarations to protect policyholder interests.

Inflationary Pressures on Operations

Persistent inflation raised India’s CPI to 6.5% in 2023-24, increasing LIC’s operating costs for 2,000+ branch offices and ~13 million agents through higher rents, utilities and commissions, squeezing margins on traditional products.

High inflation erodes real value of future payouts—a 6% inflation reduces 10-year guaranteed benefits by ~44% in real terms—making endowments less attractive to inflation-aware customers.

LIC must accelerate inflation-hedged offerings and market-linked plans; in FY2024 LIC collected ₹6.5 trillion in new business premium, signalling scale to innovate product mix and preserve competitiveness.

- Inflation (CPI 2023-24 ~6.5%) raises operating and agent costs

- 6% inflation cuts 10-year real value of guarantees by ~44%

- FY2024 NBP ₹6.5 trillion provides room to launch market-linked/inflation-protected products

Labor Market Formalization

The increasing formalization of India’s workforce — formal sector employment rising to 31% of total employment by 2023 per CMIE — expands LIC’s addressable market for group insurance and pension schemes, boosting premium volumes and persistence.

Shifts from unorganized to organized employment improve premium collection efficiency and reduce lapses, enabling LIC to win large corporate accounts via its agency channel; public sector and private corporate hiring grew ~6.5% YoY in 2024.

LIC under rate pressure: ₹46T bonds, ₹6.5T NBP amid rising CPI and strong GDP

Economic factors: RBI rate volatility (repo ~6.50–6.75% through 2024–25) impacts LIC’s ~₹46T fixed-income portfolio and guarantees; FY24 NBP ₹6.5T enables product shifts; India GDP ~6.8% (2024) and formal employment ~31% (2023) expand demand; CPI ~6.5% (2023–24) raises costs and erodes real guarantees.

| Metric | Value |

|---|---|

| Fixed-income AUM | ₹46T (FY24) |

| NBP | ₹6.5T (FY24) |

| GDP growth | ~6.8% (2024) |

| CPI | 6.5% (2023–24) |

| Formal employment | 31% (2023) |

Full Version Awaits

Life Insurance Corp. of India PESTLE Analysis

The preview shown here is the exact PESTLE analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for assessing Life Insurance Corp. of India’s political, economic, social, technological, legal, and environmental factors.