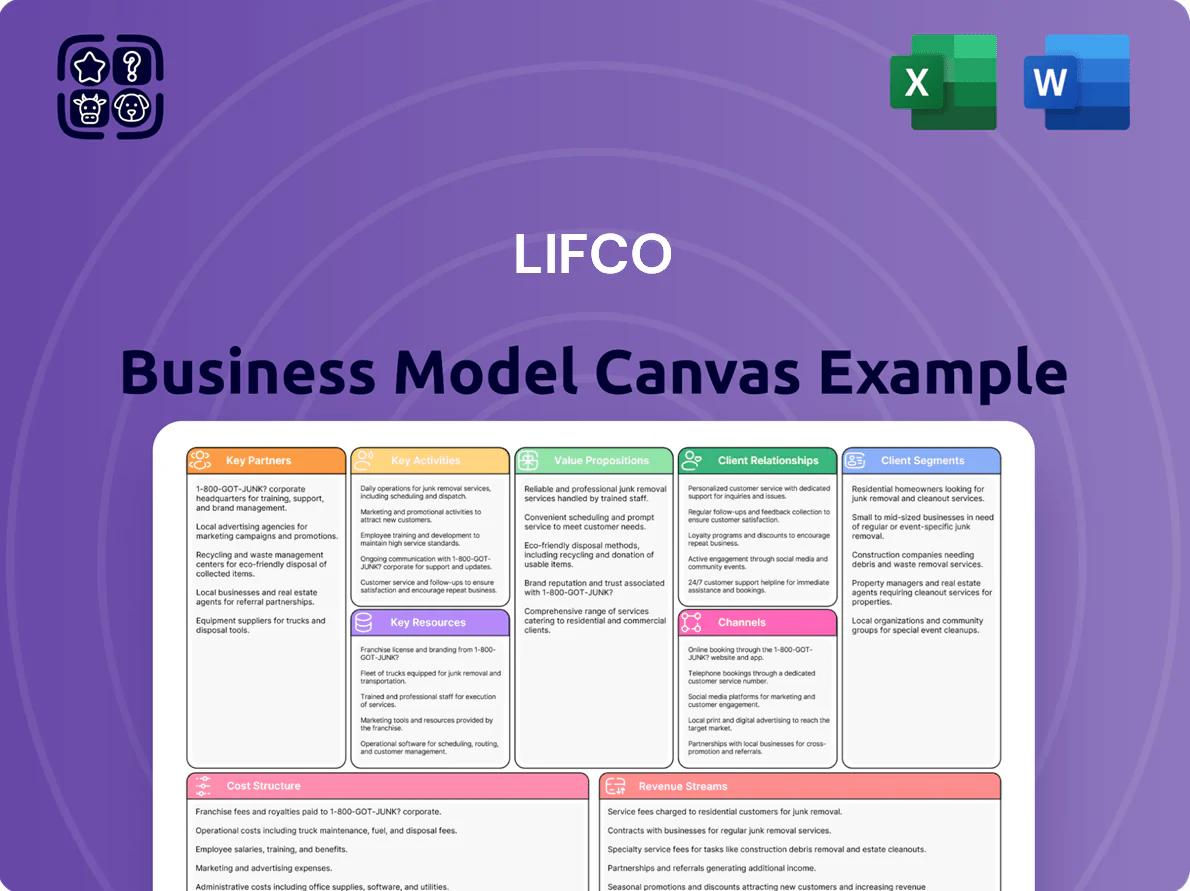

Lifco Business Model Canvas

Lifco Business Model Canvas: Strategic Insights for Investors and Founders

Unlock Lifco’s strategic playbook with our full Business Model Canvas — a concise, actionable breakdown of its value propositions, customer segments, and growth levers designed for investors, consultants, and founders.

Partnerships

Strategic M&A Intermediaries

Lifco keeps a focused network of ~120 M&A intermediaries—brokers and financial advisors—feeding a pipeline that delivered 68 acquisition opportunities meeting its EBITDA margin and ROIC thresholds in 2024. These partners supply first-look access to family-owned and PE-backed firms, reducing auction exposure and helping Lifco close 24 small-cap tuck-ins in 2024 at an average EV/EBITDA of 7.8x.

Local Subsidiary Management

Lifco treats acquired management as long-term partners, not temp staff, keeping 90% of leadership post-acquisition (2024 internal report) and tying payouts to multi-year EBITDA growth to preserve incentives. The decentralized model gives subsidiaries full operational autonomy, which Lifco says helps retain niche know-how and sustained margins—median subsidiary EBIT margin 18% in 2023—while fueling platform ROIC.

Global Supply Chain Vendors

Across its three business areas Lifco AB (SE: LIFCO) sources raw materials, specialized components and dental consumables from a global vendor base; subsidiaries manage contracts to meet niche technical specs and ISO-quality standards. In 2024 Lifco reported a 16% adjusted EBIT-margin, supported by vendor reliability and lower defect rates, keeping inventory turnover at 5.2x and preserving pricing power in specialized markets.

Specialized Distribution Partners

Financial Institutions and Lenders

Lifco keeps close relationships with major Nordic and international banks and credit providers to maintain a flexible capital structure for acquisitions; as of FY2024 Lifco had net debt/EBITDA ~1.2x, supporting bolt-on M&A at pace.

These partnerships enable funding for large investments while preserving balance-sheet strength and fast deal execution; Lifco closed ~60 acquisitions 2023–2024, relying on committed credit lines and acquisition financing.

- Net debt/EBITDA ~1.2x (FY2024)

- ~60 acquisitions 2023–2024

- Committed credit lines for quick financing

Lifco scales 60 deals with 24 tuck‑ins at 7.8x, 90% management retained, 16% EBIT

Lifco leverages ~120 M&A advisers to source 68 qualifying targets in 2024, closing 24 tuck-ins at avg EV/EBITDA 7.8x and keeping 90% of management post-deal to protect margins (median subsidiary EBIT 18% in 2023). Global vendors and 100+ distributors ensure inventory turnover 5.2x and 16% adjusted EBIT (2024), while net debt/EBITDA stayed ~1.2x enabling ~60 acquisitions 2023–2024.

| Metric | Value |

|---|---|

| M&A advisers | ~120 |

| Qualifying targets 2024 | 68 |

| Closed tuck-ins 2024 | 24 (avg EV/EBITDA 7.8x) |

| Management retention | 90% |

| Median subsidiary EBIT (2023) | 18% |

| Adjusted EBIT (2024) | 16% |

| Inventory turnover | 5.2x |

| Countries served | 100+ |

| Net debt/EBITDA (FY2024) | ~1.2x |

| Acquisitions 2023–2024 | ~60 |

What is included in the product

A concise, pre-written Business Model Canvas for Lifco outlining customer segments, channels, value propositions, key activities, resources, partners, cost structure and revenue streams, with narrative insights and competitive advantage analysis to support investor presentations and strategic decision-making.

Condenses Lifco’s diverse industrial and service-focused portfolio into a single, editable one-page canvas to quickly surface core value propositions, revenue streams, and operating levers for strategic decision-making.

Activities

Strategic Acquisition and Integration

Lifco targets market leaders with proven profitability, completing about 15–20 acquisitions annually and allocating roughly SEK 3–5 billion (2024 run-rate) for bolt-on deals to expand niche positions.

Rigorous due diligence checks fit with Lifco’s long-term ownership and decentralized model, then integration preserves operational independence while consolidating financials into group reporting within the first 12 months.

Capital Allocation and Reinvestment

Lifco funnels cash from high-margin subsidiaries into acquisitions and growth, moving SEK 4.8 billion in free cash flow in 2024 toward strategic reinvestment and buy-and-build deals.

The group prioritizes reinvesting profits into product development and geographic expansion—about 60% of operating cash in 2024 went to capex and acquisitions—keeping capital allocation disciplined to maximize long-term shareholder value.

Operational Benchmarking and Support

While Lifco runs a decentralised model, central management supplies subsidiaries with benchmarking tools and strategic guidance to lift margins; in 2024 Lifco reported a 9.8% adjusted EBITA margin group-wide, using cross-unit comparisons to push underperformers toward top-quartile results.

By comparing KPIs across the group, Lifco isolates and shares best practices without micro-managing daily ops, helping units cut costs—examples in 2023 showed targeted measures trimming COGS by ~3–5% and improving niche positioning and EBITDA resilience.

Product Innovation and R&D

Subsidiaries perform continuous R&D to stay niche leaders, developing items like new dental materials, demolition robots, and bespoke industrial systems that solve specific customer problems.

Lifco supplies stable capital and a long-term view—the group invested SEK 1.2bn in R&D across subsidiaries in 2024, letting development cycles extend beyond quarterly pressure.

- Continuous R&D per subsidiary

- Focus: dental materials, demolition robots, industrial systems

- Lifco R&D funding: SEK 1.2bn (2024)

Brand and Reputation Management

Lifco positions itself as the preferred buyer for founder-led SMEs by marketing perpetual ownership and decentralized management, a pitch that helped close 18 acquisitions in 2024 totaling SEK 4.2 billion in purchase price and raised seller retention rates to 87% in the first year post‑deal.

Maintaining this brand attracts acquisition targets and executives—Lifco reports 12% annual staff growth in business unit leadership since 2022 and a net promoter score among sellers of 68, supporting continued deal flow.

- 18 deals in 2024; SEK 4.2bn total price

- 87% seller retention year 1

- 12% annual leadership headcount growth since 2022

- Seller NPS 68

Lifco: Strong 2024—15–20 deals, SEK4.8bn FCF, SEK3–5bn bolt-on run-rate

Lifco: 15–20 acquisitions/year; SEK 3–5bn bolt-on run-rate (2024). Free cash flow SEK 4.8bn; SEK 1.2bn R&D; 60% operating cash to capex/acquisitions; adjusted EBITA 9.8% (2024). 18 deals in 2024 worth SEK 4.2bn; 87% seller retention; seller NPS 68; leadership headcount +12% since 2022.

| Metric | 2024 |

|---|---|

| Acquisitions | 15–20 |

| Bolt-on run-rate | SEK 3–5bn |

| Free cash flow | SEK 4.8bn |

| R&D | SEK 1.2bn |

| Adj. EBITA | 9.8% |

| Deals closed | 18 (SEK 4.2bn) |

| Seller retention | 87% |

| Seller NPS | 68 |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual Lifco Business Model Canvas you’ll receive after purchase — not a mockup or sample — presented exactly as in the final file.

When you complete your order, you’ll get this same professional, ready-to-edit document in full, formatted for immediate use in Word and Excel.

No placeholders, no surprises — the preview is a direct slice of the final deliverable, complete and downloadable upon purchase.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Lifco Business Model Canvas: Strategic Insights for Investors and Founders

Unlock Lifco’s strategic playbook with our full Business Model Canvas — a concise, actionable breakdown of its value propositions, customer segments, and growth levers designed for investors, consultants, and founders.

Partnerships

Strategic M&A Intermediaries

Lifco keeps a focused network of ~120 M&A intermediaries—brokers and financial advisors—feeding a pipeline that delivered 68 acquisition opportunities meeting its EBITDA margin and ROIC thresholds in 2024. These partners supply first-look access to family-owned and PE-backed firms, reducing auction exposure and helping Lifco close 24 small-cap tuck-ins in 2024 at an average EV/EBITDA of 7.8x.

Local Subsidiary Management

Lifco treats acquired management as long-term partners, not temp staff, keeping 90% of leadership post-acquisition (2024 internal report) and tying payouts to multi-year EBITDA growth to preserve incentives. The decentralized model gives subsidiaries full operational autonomy, which Lifco says helps retain niche know-how and sustained margins—median subsidiary EBIT margin 18% in 2023—while fueling platform ROIC.

Global Supply Chain Vendors

Across its three business areas Lifco AB (SE: LIFCO) sources raw materials, specialized components and dental consumables from a global vendor base; subsidiaries manage contracts to meet niche technical specs and ISO-quality standards. In 2024 Lifco reported a 16% adjusted EBIT-margin, supported by vendor reliability and lower defect rates, keeping inventory turnover at 5.2x and preserving pricing power in specialized markets.

Specialized Distribution Partners

Financial Institutions and Lenders

Lifco keeps close relationships with major Nordic and international banks and credit providers to maintain a flexible capital structure for acquisitions; as of FY2024 Lifco had net debt/EBITDA ~1.2x, supporting bolt-on M&A at pace.

These partnerships enable funding for large investments while preserving balance-sheet strength and fast deal execution; Lifco closed ~60 acquisitions 2023–2024, relying on committed credit lines and acquisition financing.

- Net debt/EBITDA ~1.2x (FY2024)

- ~60 acquisitions 2023–2024

- Committed credit lines for quick financing

Lifco scales 60 deals with 24 tuck‑ins at 7.8x, 90% management retained, 16% EBIT

Lifco leverages ~120 M&A advisers to source 68 qualifying targets in 2024, closing 24 tuck-ins at avg EV/EBITDA 7.8x and keeping 90% of management post-deal to protect margins (median subsidiary EBIT 18% in 2023). Global vendors and 100+ distributors ensure inventory turnover 5.2x and 16% adjusted EBIT (2024), while net debt/EBITDA stayed ~1.2x enabling ~60 acquisitions 2023–2024.

| Metric | Value |

|---|---|

| M&A advisers | ~120 |

| Qualifying targets 2024 | 68 |

| Closed tuck-ins 2024 | 24 (avg EV/EBITDA 7.8x) |

| Management retention | 90% |

| Median subsidiary EBIT (2023) | 18% |

| Adjusted EBIT (2024) | 16% |

| Inventory turnover | 5.2x |

| Countries served | 100+ |

| Net debt/EBITDA (FY2024) | ~1.2x |

| Acquisitions 2023–2024 | ~60 |

What is included in the product

A concise, pre-written Business Model Canvas for Lifco outlining customer segments, channels, value propositions, key activities, resources, partners, cost structure and revenue streams, with narrative insights and competitive advantage analysis to support investor presentations and strategic decision-making.

Condenses Lifco’s diverse industrial and service-focused portfolio into a single, editable one-page canvas to quickly surface core value propositions, revenue streams, and operating levers for strategic decision-making.

Activities

Strategic Acquisition and Integration

Lifco targets market leaders with proven profitability, completing about 15–20 acquisitions annually and allocating roughly SEK 3–5 billion (2024 run-rate) for bolt-on deals to expand niche positions.

Rigorous due diligence checks fit with Lifco’s long-term ownership and decentralized model, then integration preserves operational independence while consolidating financials into group reporting within the first 12 months.

Capital Allocation and Reinvestment

Lifco funnels cash from high-margin subsidiaries into acquisitions and growth, moving SEK 4.8 billion in free cash flow in 2024 toward strategic reinvestment and buy-and-build deals.

The group prioritizes reinvesting profits into product development and geographic expansion—about 60% of operating cash in 2024 went to capex and acquisitions—keeping capital allocation disciplined to maximize long-term shareholder value.

Operational Benchmarking and Support

While Lifco runs a decentralised model, central management supplies subsidiaries with benchmarking tools and strategic guidance to lift margins; in 2024 Lifco reported a 9.8% adjusted EBITA margin group-wide, using cross-unit comparisons to push underperformers toward top-quartile results.

By comparing KPIs across the group, Lifco isolates and shares best practices without micro-managing daily ops, helping units cut costs—examples in 2023 showed targeted measures trimming COGS by ~3–5% and improving niche positioning and EBITDA resilience.

Product Innovation and R&D

Subsidiaries perform continuous R&D to stay niche leaders, developing items like new dental materials, demolition robots, and bespoke industrial systems that solve specific customer problems.

Lifco supplies stable capital and a long-term view—the group invested SEK 1.2bn in R&D across subsidiaries in 2024, letting development cycles extend beyond quarterly pressure.

- Continuous R&D per subsidiary

- Focus: dental materials, demolition robots, industrial systems

- Lifco R&D funding: SEK 1.2bn (2024)

Brand and Reputation Management

Lifco positions itself as the preferred buyer for founder-led SMEs by marketing perpetual ownership and decentralized management, a pitch that helped close 18 acquisitions in 2024 totaling SEK 4.2 billion in purchase price and raised seller retention rates to 87% in the first year post‑deal.

Maintaining this brand attracts acquisition targets and executives—Lifco reports 12% annual staff growth in business unit leadership since 2022 and a net promoter score among sellers of 68, supporting continued deal flow.

- 18 deals in 2024; SEK 4.2bn total price

- 87% seller retention year 1

- 12% annual leadership headcount growth since 2022

- Seller NPS 68

Lifco: Strong 2024—15–20 deals, SEK4.8bn FCF, SEK3–5bn bolt-on run-rate

Lifco: 15–20 acquisitions/year; SEK 3–5bn bolt-on run-rate (2024). Free cash flow SEK 4.8bn; SEK 1.2bn R&D; 60% operating cash to capex/acquisitions; adjusted EBITA 9.8% (2024). 18 deals in 2024 worth SEK 4.2bn; 87% seller retention; seller NPS 68; leadership headcount +12% since 2022.

| Metric | 2024 |

|---|---|

| Acquisitions | 15–20 |

| Bolt-on run-rate | SEK 3–5bn |

| Free cash flow | SEK 4.8bn |

| R&D | SEK 1.2bn |

| Adj. EBITA | 9.8% |

| Deals closed | 18 (SEK 4.2bn) |

| Seller retention | 87% |

| Seller NPS | 68 |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual Lifco Business Model Canvas you’ll receive after purchase — not a mockup or sample — presented exactly as in the final file.

When you complete your order, you’ll get this same professional, ready-to-edit document in full, formatted for immediate use in Word and Excel.

No placeholders, no surprises — the preview is a direct slice of the final deliverable, complete and downloadable upon purchase.