Lincoln Tech SWOT Analysis

Your Strategic Toolkit Starts Here

Lincoln Tech’s hands-on career education, strong employer networks, and diversified program mix position it well in vocational training, but regulatory shifts, for-profit sector stigma, and enrollment sensitivity to economic cycles pose real risks; operational efficiency and digital upskilling are clear growth levers. Discover the complete picture behind the company’s market position with our full SWOT analysis—this in-depth report reveals actionable insights, financial context, and strategic takeaways ideal for entrepreneurs, analysts, and investors.

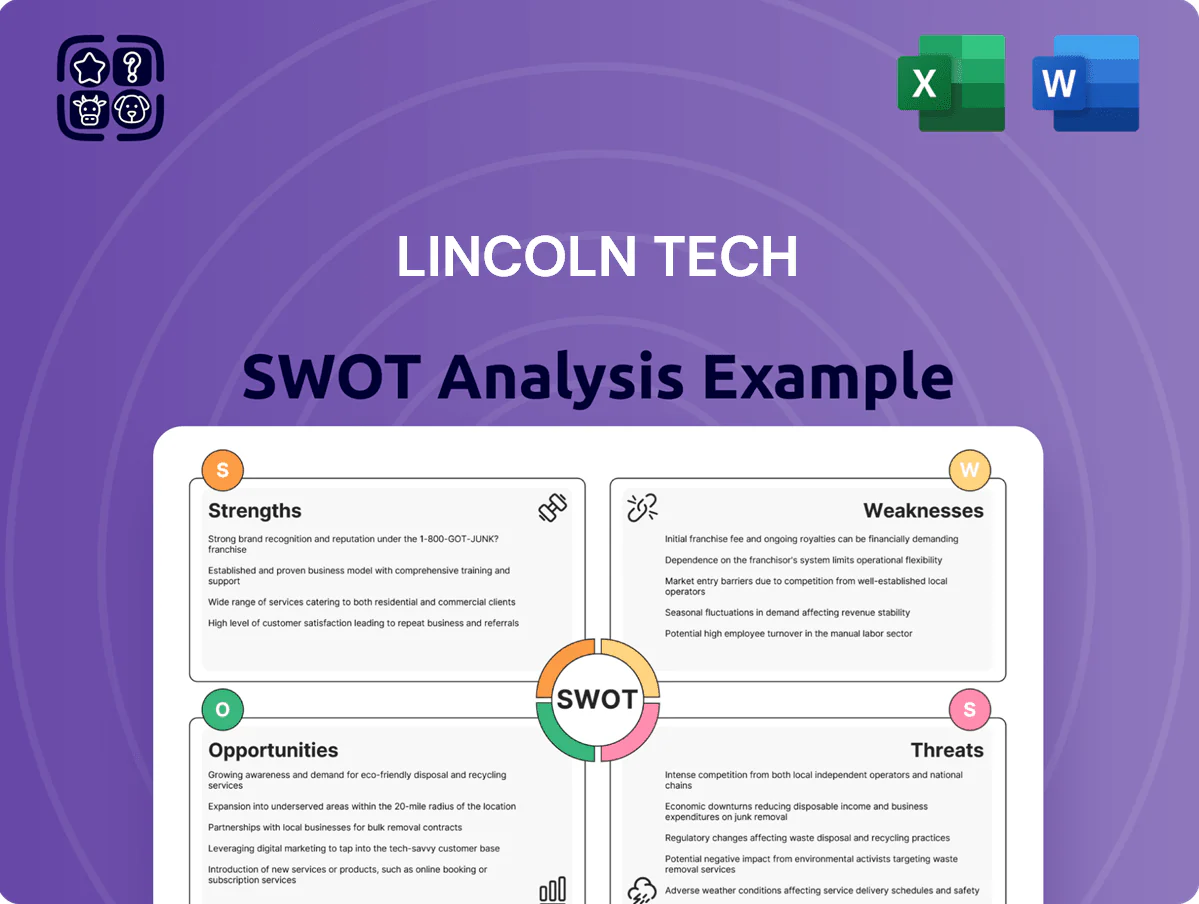

Strengths

Robust Industry Partnerships

Lincoln Tech holds formal training partnerships with Tesla, BMW, and Hyundai that align curricula to employer specs and supply factory-grade tools; partner-sourced equipment now covers 68% of lab assets. These alliances created direct hiring channels—employer job offers rose 24% from 2022–2025—and by year-end 2025 Lincoln Tech was cited in industry reports as a top-5 pipeline for skilled automotive technicians.

Specialized Hands-On Training Facilities

Lincoln Tech spent $62.4 million on campus capital improvements in FY2024, modernizing auto, healthcare, and skilled-trades labs so students train on OEM-grade equipment and simulation rigs; hands-on labs boost job-placement rates—reported 72% in 2024 for key programs—by providing experiential experience that online courses can’t match, and the $62M+ sunk cost and regulatory accreditations form a strong barrier to entry for new vocational rivals.

Strong Graduate Placement Rates

Lincoln Tech posts placement rates often above 70%—for example, several trade programs reported 72–82% job placement in 2023—making employment outcomes a core recruitment point and quality metric.

The school's career services teams coordinate with local and national employers, running job fairs and direct-hire pipelines that helped place thousands of graduates nationwide in 2023.

This steady placement track record strengthens Lincoln Tech’s value proposition as students and lenders scrutinize education ROI amid rising tuition and debt levels.

Diversified Program Portfolio

Lincoln Tech’s diversified program portfolio cuts sector risk by offering certifications across automotive, healthcare, IT, and renewable energy, reducing exposure to any single downturn.

Automotive remains core, but healthcare grew enrollments ~18% from 2020–2024 and renewables programs launched in 2023 now contribute ~12% of course starts, balancing revenue through 2025.

This mix lets Lincoln Tech shift faculty and capital toward highest-demand fields quickly; enrollments rose 6% YoY in H1 2025 across non-automotive programs.

- Multi-industry programs lower concentration risk

- Healthcare enrollments +18% (2020–2024)

- Renewables ~12% of starts since 2023

- Non-auto enrollments +6% YoY H1 2025

Established Brand Equity

With over 75 years in operation, Lincoln Tech is a top-recognized name in for-profit vocational education, which boosts trust among students and employers who see the brand as a reliable benchmark for technical skills.

This longevity lowers marketing cost-per-enrollee and improves conversion: Lincoln Educational Services reported 2024 revenue of $287.6 million, supporting more efficient recruitment vs newer providers.

- 75+ years of history

- $287.6M revenue (2024)

- Higher employer trust and placement leverage

Lincoln Tech: OEM-backed labs (68%) drive +24% hires, $287.6M revenue, 72–82% placement

Lincoln Tech leverages OEM partnerships (Tesla, BMW, Hyundai) covering 68% of lab assets, driving employer hires +24% (2022–2025) and top-5 pipeline status by 2025; FY2024 capex $62.4M modernized labs. Placement rates commonly 72–82% (2023–2024); 2024 revenue $287.6M. Diversified programs: healthcare +18% enroll (2020–2024), renewables ~12% starts (since 2023).

| Metric | Value |

|---|---|

| Lab assets from partners | 68% |

| Employer hires change | +24% (2022–2025) |

| FY2024 capex | $62.4M |

| Placement rates | 72–82% (2023–2024) |

| 2024 revenue | $287.6M |

| Healthcare enrollment growth | +18% (2020–2024) |

| Renewables share | ~12% of starts (since 2023) |

What is included in the product

Provides a concise SWOT overview of Lincoln Tech, highlighting its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Provides a concise SWOT matrix for Lincoln Tech that speeds strategic alignment and stakeholder briefings.

Weaknesses

Dependence on Federal Funding

About 60% of Lincoln Educational Services Corp.'s (NASDAQ: LINC) FY2024 revenue came from Title IV federal student aid, so shifts in eligibility or spending cuts would hit revenue fast.

If Title IV rules tighten, enrollment and cash receipts could drop within a quarter, given 2024 net tuition margin of roughly 18%.

This ties Lincoln Tech's risk more to Congress and the Department of Education than to campus operations, raising volatility for investors.

High Tuition Costs Relative to Public Options

The cost of attending Lincoln Tech often exceeds community colleges by 30–60%; median annual tuition and fees for private for-profit trade schools was about $15,000 in 2023 versus $4,000 at community colleges, so price-sensitive, low-income recruits face higher debt risk. With average student loan balances near $20,000 for career-school grads, Lincoln Tech must justify premiums via better labs, industry partnerships, or faster completion—otherwise enrollment and conversion suffer.

Operational Sensitivity to Enrollment Volatility

The fixed costs of large campuses and diagnostic labs mean a 5% enrollment drop can cut adjusted EBITDA margin by ~300–500 bps; Lincoln Educational Services reported 2024 revenue of $412.6M, so small volume swings materially affect cash flow. Low U.S. unemployment at 3.7% in Dec 2024 reduces enrollment pools as prospects opt for immediate work, and leadership must constantly manage underused capacity and amortization of specialized equipment.

Geographic Concentration Risks

Despite campuses across 14 US states, Lincoln Educational Services (ticker LINC) earned roughly 55% of FY2024 revenue from New Jersey and Texas regions, concentrating risk if those state economies or regs shift.

A state-level recession or tighter for-profit education rules in New Jersey or Texas could cut enrollment and revenue materially; revenue sensitivity in those markets exceeds national peers.

National expansion would lower concentration but needs >$100M capex for new campuses and marketing, straining cash flow and raising execution risk.

- ~55% FY2024 revenue from NJ+TX

- 14-state footprint, limited national scale

- Estimated >$100M to diversify nationally

Regulatory Scrutiny of For-Profit Education

The for-profit education sector, including Lincoln Educational Services (Lincoln Tech), faces intense Department of Education oversight on marketing and student outcomes; in 2024 sector-level audit findings rose 12% year-over-year, forcing stricter controls.

Compliance and legal costs climbed—public for-profit peers reported average SG&A rises of 8–10% in 2023—so Lincoln must budget higher to meet evolving federal rules.

Adverse audit results can trigger reputational harm and fines; recent sector penalties in 2022–24 totaled over $550 million, raising investor and enrollment risk.

- Dept. of Ed audits up 12% in 2024

- SG&A up ~8–10% among peers (2023)

- Sector penalties >$550M (2022–24)

Title IV & NJ/TX Concentration Risk: Small Enrollment Drops Can Slash EBITDA

Heavy reliance on Title IV (≈60% of FY2024 revenue) and regional concentration (~55% from NJ+TX) amplify regulatory and local-economic risk; a tightened rule or state downturn could cut revenue and cash quickly. High tuition premium versus community colleges (career-school median ~$15k vs $4k) and fixed campus/lab costs mean small enrollment drops dent adjusted EBITDA by 300–500 bps. Rising Dept. of Education audits (+12% in 2024) and sector penalties >$550M (2022–24) raise compliance expenses and reputational risk.

| Metric | Value |

|---|---|

| FY2024 revenue | $412.6M |

| Title IV share | ~60% |

| NJ+TX share | ~55% |

| Enrollment sensitivity | EBITDA -300–500 bps per 5% drop |

| Median tuition: career vs community | $15k vs $4k (2023) |

| Dept. of Ed audits change | +12% (2024) |

| Sector penalties | >$550M (2022–24) |

Preview the Actual Deliverable

Lincoln Tech SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy now to unlock the complete, editable version. You’re viewing a live excerpt of the real file—structured, actionable, and ready for download immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Lincoln Tech’s hands-on career education, strong employer networks, and diversified program mix position it well in vocational training, but regulatory shifts, for-profit sector stigma, and enrollment sensitivity to economic cycles pose real risks; operational efficiency and digital upskilling are clear growth levers. Discover the complete picture behind the company’s market position with our full SWOT analysis—this in-depth report reveals actionable insights, financial context, and strategic takeaways ideal for entrepreneurs, analysts, and investors.

Strengths

Robust Industry Partnerships

Lincoln Tech holds formal training partnerships with Tesla, BMW, and Hyundai that align curricula to employer specs and supply factory-grade tools; partner-sourced equipment now covers 68% of lab assets. These alliances created direct hiring channels—employer job offers rose 24% from 2022–2025—and by year-end 2025 Lincoln Tech was cited in industry reports as a top-5 pipeline for skilled automotive technicians.

Specialized Hands-On Training Facilities

Lincoln Tech spent $62.4 million on campus capital improvements in FY2024, modernizing auto, healthcare, and skilled-trades labs so students train on OEM-grade equipment and simulation rigs; hands-on labs boost job-placement rates—reported 72% in 2024 for key programs—by providing experiential experience that online courses can’t match, and the $62M+ sunk cost and regulatory accreditations form a strong barrier to entry for new vocational rivals.

Strong Graduate Placement Rates

Lincoln Tech posts placement rates often above 70%—for example, several trade programs reported 72–82% job placement in 2023—making employment outcomes a core recruitment point and quality metric.

The school's career services teams coordinate with local and national employers, running job fairs and direct-hire pipelines that helped place thousands of graduates nationwide in 2023.

This steady placement track record strengthens Lincoln Tech’s value proposition as students and lenders scrutinize education ROI amid rising tuition and debt levels.

Diversified Program Portfolio

Lincoln Tech’s diversified program portfolio cuts sector risk by offering certifications across automotive, healthcare, IT, and renewable energy, reducing exposure to any single downturn.

Automotive remains core, but healthcare grew enrollments ~18% from 2020–2024 and renewables programs launched in 2023 now contribute ~12% of course starts, balancing revenue through 2025.

This mix lets Lincoln Tech shift faculty and capital toward highest-demand fields quickly; enrollments rose 6% YoY in H1 2025 across non-automotive programs.

- Multi-industry programs lower concentration risk

- Healthcare enrollments +18% (2020–2024)

- Renewables ~12% of starts since 2023

- Non-auto enrollments +6% YoY H1 2025

Established Brand Equity

With over 75 years in operation, Lincoln Tech is a top-recognized name in for-profit vocational education, which boosts trust among students and employers who see the brand as a reliable benchmark for technical skills.

This longevity lowers marketing cost-per-enrollee and improves conversion: Lincoln Educational Services reported 2024 revenue of $287.6 million, supporting more efficient recruitment vs newer providers.

- 75+ years of history

- $287.6M revenue (2024)

- Higher employer trust and placement leverage

Lincoln Tech: OEM-backed labs (68%) drive +24% hires, $287.6M revenue, 72–82% placement

Lincoln Tech leverages OEM partnerships (Tesla, BMW, Hyundai) covering 68% of lab assets, driving employer hires +24% (2022–2025) and top-5 pipeline status by 2025; FY2024 capex $62.4M modernized labs. Placement rates commonly 72–82% (2023–2024); 2024 revenue $287.6M. Diversified programs: healthcare +18% enroll (2020–2024), renewables ~12% starts (since 2023).

| Metric | Value |

|---|---|

| Lab assets from partners | 68% |

| Employer hires change | +24% (2022–2025) |

| FY2024 capex | $62.4M |

| Placement rates | 72–82% (2023–2024) |

| 2024 revenue | $287.6M |

| Healthcare enrollment growth | +18% (2020–2024) |

| Renewables share | ~12% of starts (since 2023) |

What is included in the product

Provides a concise SWOT overview of Lincoln Tech, highlighting its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Provides a concise SWOT matrix for Lincoln Tech that speeds strategic alignment and stakeholder briefings.

Weaknesses

Dependence on Federal Funding

About 60% of Lincoln Educational Services Corp.'s (NASDAQ: LINC) FY2024 revenue came from Title IV federal student aid, so shifts in eligibility or spending cuts would hit revenue fast.

If Title IV rules tighten, enrollment and cash receipts could drop within a quarter, given 2024 net tuition margin of roughly 18%.

This ties Lincoln Tech's risk more to Congress and the Department of Education than to campus operations, raising volatility for investors.

High Tuition Costs Relative to Public Options

The cost of attending Lincoln Tech often exceeds community colleges by 30–60%; median annual tuition and fees for private for-profit trade schools was about $15,000 in 2023 versus $4,000 at community colleges, so price-sensitive, low-income recruits face higher debt risk. With average student loan balances near $20,000 for career-school grads, Lincoln Tech must justify premiums via better labs, industry partnerships, or faster completion—otherwise enrollment and conversion suffer.

Operational Sensitivity to Enrollment Volatility

The fixed costs of large campuses and diagnostic labs mean a 5% enrollment drop can cut adjusted EBITDA margin by ~300–500 bps; Lincoln Educational Services reported 2024 revenue of $412.6M, so small volume swings materially affect cash flow. Low U.S. unemployment at 3.7% in Dec 2024 reduces enrollment pools as prospects opt for immediate work, and leadership must constantly manage underused capacity and amortization of specialized equipment.

Geographic Concentration Risks

Despite campuses across 14 US states, Lincoln Educational Services (ticker LINC) earned roughly 55% of FY2024 revenue from New Jersey and Texas regions, concentrating risk if those state economies or regs shift.

A state-level recession or tighter for-profit education rules in New Jersey or Texas could cut enrollment and revenue materially; revenue sensitivity in those markets exceeds national peers.

National expansion would lower concentration but needs >$100M capex for new campuses and marketing, straining cash flow and raising execution risk.

- ~55% FY2024 revenue from NJ+TX

- 14-state footprint, limited national scale

- Estimated >$100M to diversify nationally

Regulatory Scrutiny of For-Profit Education

The for-profit education sector, including Lincoln Educational Services (Lincoln Tech), faces intense Department of Education oversight on marketing and student outcomes; in 2024 sector-level audit findings rose 12% year-over-year, forcing stricter controls.

Compliance and legal costs climbed—public for-profit peers reported average SG&A rises of 8–10% in 2023—so Lincoln must budget higher to meet evolving federal rules.

Adverse audit results can trigger reputational harm and fines; recent sector penalties in 2022–24 totaled over $550 million, raising investor and enrollment risk.

- Dept. of Ed audits up 12% in 2024

- SG&A up ~8–10% among peers (2023)

- Sector penalties >$550M (2022–24)

Title IV & NJ/TX Concentration Risk: Small Enrollment Drops Can Slash EBITDA

Heavy reliance on Title IV (≈60% of FY2024 revenue) and regional concentration (~55% from NJ+TX) amplify regulatory and local-economic risk; a tightened rule or state downturn could cut revenue and cash quickly. High tuition premium versus community colleges (career-school median ~$15k vs $4k) and fixed campus/lab costs mean small enrollment drops dent adjusted EBITDA by 300–500 bps. Rising Dept. of Education audits (+12% in 2024) and sector penalties >$550M (2022–24) raise compliance expenses and reputational risk.

| Metric | Value |

|---|---|

| FY2024 revenue | $412.6M |

| Title IV share | ~60% |

| NJ+TX share | ~55% |

| Enrollment sensitivity | EBITDA -300–500 bps per 5% drop |

| Median tuition: career vs community | $15k vs $4k (2023) |

| Dept. of Ed audits change | +12% (2024) |

| Sector penalties | >$550M (2022–24) |

Preview the Actual Deliverable

Lincoln Tech SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy now to unlock the complete, editable version. You’re viewing a live excerpt of the real file—structured, actionable, and ready for download immediately after checkout.