Lindsay Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

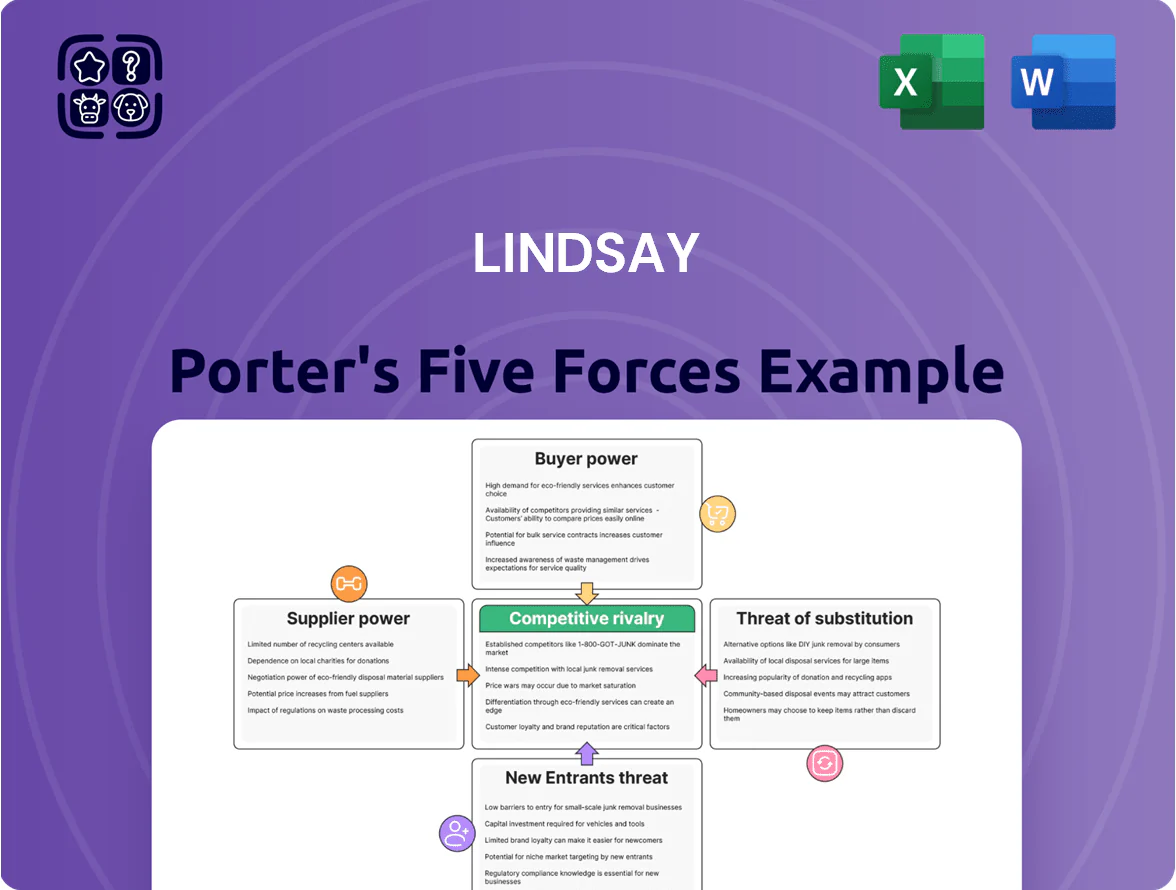

Lindsay’s Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, substitute threats, and entry barriers—offering a concise view of its strategic position and market pressures. This brief intro only scratches the surface; unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights tailored to guide investment and strategic decisions.

Suppliers Bargaining Power

Raw material price volatility

The production of irrigation systems and road-safety products depends on steel, zinc, and aluminum; Latham Industries reported a 28% year-on-year steel price spike in 2023 and LME zinc rose 45% in 2022–23, squeezing margins for makers like Lindsay Porter. Global demand cycles and tariffs (US Section 232, EU safeguards since 2018) drive price swings, and Lindsay cannot force prices down versus major metal producers during supply tightness.

Specialized technology component reliance

As Lindsay adds IoT and autonomous features to FieldNET and Road Zipper, dependence on semiconductors and sensors grows; global chip shortages in 2021–23 showed suppliers can delay delivery—average lead times rose 20–30%—and top sensor makers hold >60% market share in key segments.

Energy and logistics costs

Energy and freight form 12–18% of cost of goods sold for heavy infrastructure makers; in 2024 US diesel averaged $4.05/gal and industrial electricity $0.11/kWh, so a 10% transport or energy price rise (as in 2022–23) can cut Lindsay’s gross margin by ~1.2–1.8 percentage points. Large trucking and fuel suppliers thus hold bargaining power because Lindsay can only partially pass hikes to customers in a price-sensitive irrigation and roadway market.

Supplier concentration in specific regions

- 60–80% of critical parts from 2–4 suppliers

- Regions: US Midwest, Northern Mexico

- 35% of farms saw >14-day delays (2024)

- Downtime cost +12% per disruption

Availability of skilled labor

The manufacturing process needs specialized welding and engineering talent that is increasingly scarce in developed markets; OECD data show skilled-trades shortages rose ~12% from 2019–2023, pushing wages up 6–10% in 2024 in metal fabrication sectors.

Strong unions and tight local labor pools force higher concessions or signing bonuses, and the labor force thus behaves like a supplier of essential human capital with real bargaining leverage.

Rising metal, chip concentration and logistics risks squeeze margins—supply shocks intensify

Suppliers hold moderate–high power: metals (steel/zinc/aluminum) and sensors are concentrated and volatile—steel spiked 28% y/y (2023), LME zinc +45% (2022–23); chips/sensors top firms >60% share with 20–30% longer lead times (2021–23). Energy/freight ~12–18% COGS; 2024 diesel $4.05/gal, electricity $0.11/kWh, a 10% rise cuts gross margin ~1.2–1.8 pts. Critical parts 60–80% from 2–4 suppliers; 35% of farms saw >14‑day delays (2024).

| Metric | Value |

|---|---|

| Steel price change (2023) | +28% y/y |

| LME zinc (2022–23) | +45% |

| Sensor market concentration | >60% top firms |

| Lead time increase (2021–23) | +20–30% |

| Energy/freight share of COGS | 12–18% |

| Diesel (US, 2024) | $4.05/gal |

| Electricity (industrial, 2024) | $0.11/kWh |

| Critical parts dependency | 60–80% from 2–4 suppliers |

| >14‑day parts delays (2024) | 35% of farms |

What is included in the product

Concise Five Forces assessment for Lindsay that uncovers key competitive drivers, supplier and buyer power, threat of substitutes and entrants, and strategic levers to protect margins and market share.

A one-sheet Lindsay Porter Five Forces summary that clarifies competitive pressures at a glance—ideal for rapid strategic decisions and boardroom-ready slides.

Customers Bargaining Power

Agricultural net income fluctuations

Farmers, Lindsay's main customers, see purchasing power swing with global crop prices; CBOT corn fell 18% in 2024, pushing many to defer capital buys.

When commodity lows occur, Lindsay must cut prices or extend financing—its 2024 promo-led unit growth came with a 120 bps margin hit in Q3.

This cyclicality raises bargaining power: delayed purchases reduce order visibility by ~25% year-over-year, forcing flexible terms to keep factory utilization up.

Government infrastructure spending cycles

The infrastructure segment depends on Department of Transportation budgets and the $120B+ federal highway program (2025 FAST Act extensions), making government buyers highly price-sensitive and procurement-driven; they use transparent competitive bidding where lowest-compliant bid often wins. Political shifts or 10–20% fiscal cuts (seen in 2023 state austerity moves) can swing bargaining power squarely to the buyer, pressuring margins and contract terms.

Dealer network influence

Dealer network influence: Lindsay sells via ~450 independent dealers in North America who provide local service; many carry 3–7 competing brands and influence up to 60% of end-user choices, so dealer recommendations materially affect market share. In 2024 Lindsay reported 28% of sales routed through top 50 dealers, so maintaining incentives and training with these intermediaries is vital to protect penetration and margins.

Availability of financing and subsidies

Availability of low-interest loans and environmental grants (eg: US Dept. of Agriculture 2024 programs, €150m EU water-efficiency funds) reduces customer price sensitivity, letting Lindsay keep firmer pricing on premium, tech-integrated irrigation units.

If subsidies or the UK 2025 £50m efficient-irrigation scheme shrink, buyers grow more price-sensitive and demanding, raising churn and negotiation leverage.

- Financing up: supports premium pricing

- Subsidy cuts: increases customer bargaining

- 2024–25 programs: key demand drivers

Low switching costs for basic hardware

Software integration gives Lindsay some customer lock-in, but center-pivot hardware remains largely commoditized; industry surveys show 60–70% of pivots share interchangeable specs, so farms can swap brands with little retrofit cost.

Large-scale growers, who account for roughly 40% of U.S. pivot sales, can shift to rivals like Valmont or Reinke if offered ~5–10% better total cost of ownership, constraining Lindsay’s ability to raise core-mechanical prices.

Here’s the quick math: if Lindsay tried a 10% price hike on mechanicals, demand could drop by ~8%—cutting revenue rather than raising it.

- Hardware commoditized: 60–70% spec overlap

- Large farms = ~40% of pivot market

- Competitive price edge needed: ~5–10%

- Estimated demand elasticity: ~-0.8

Buyers dominate: large growers, dealers & DOTs squeeze prices amid hardware commoditization

Buyers strong: farms and DOTs push price/terms when commodity prices or budgets tighten; dealer network and large growers (≈40% pivot sales) amplify leverage. Financing/subsidies (USDA 2024 programs, €150m EU funds, UK £50m scheme) can soften buyer power; software locks reduce churn but hardware commoditization (60–70% spec overlap) keeps price elasticity near −0.8.

| Metric | Value |

|---|---|

| Large-grower share | ≈40% |

| Spec overlap | 60–70% |

| Demand elasticity | −0.8 |

| Top-dealer sales | 28% |

Full Version Awaits

Lindsay Porter's Five Forces Analysis

This preview shows the exact Lindsay Porter Five Forces Analysis document you'll receive—no surprises, no placeholders; it’s the final, fully formatted file.

Once you complete your purchase you’ll get instant access to this same ready-to-use analysis, suitable for download and immediate application in decision-making or presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Lindsay’s Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, substitute threats, and entry barriers—offering a concise view of its strategic position and market pressures. This brief intro only scratches the surface; unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights tailored to guide investment and strategic decisions.

Suppliers Bargaining Power

Raw material price volatility

The production of irrigation systems and road-safety products depends on steel, zinc, and aluminum; Latham Industries reported a 28% year-on-year steel price spike in 2023 and LME zinc rose 45% in 2022–23, squeezing margins for makers like Lindsay Porter. Global demand cycles and tariffs (US Section 232, EU safeguards since 2018) drive price swings, and Lindsay cannot force prices down versus major metal producers during supply tightness.

Specialized technology component reliance

As Lindsay adds IoT and autonomous features to FieldNET and Road Zipper, dependence on semiconductors and sensors grows; global chip shortages in 2021–23 showed suppliers can delay delivery—average lead times rose 20–30%—and top sensor makers hold >60% market share in key segments.

Energy and logistics costs

Energy and freight form 12–18% of cost of goods sold for heavy infrastructure makers; in 2024 US diesel averaged $4.05/gal and industrial electricity $0.11/kWh, so a 10% transport or energy price rise (as in 2022–23) can cut Lindsay’s gross margin by ~1.2–1.8 percentage points. Large trucking and fuel suppliers thus hold bargaining power because Lindsay can only partially pass hikes to customers in a price-sensitive irrigation and roadway market.

Supplier concentration in specific regions

- 60–80% of critical parts from 2–4 suppliers

- Regions: US Midwest, Northern Mexico

- 35% of farms saw >14-day delays (2024)

- Downtime cost +12% per disruption

Availability of skilled labor

The manufacturing process needs specialized welding and engineering talent that is increasingly scarce in developed markets; OECD data show skilled-trades shortages rose ~12% from 2019–2023, pushing wages up 6–10% in 2024 in metal fabrication sectors.

Strong unions and tight local labor pools force higher concessions or signing bonuses, and the labor force thus behaves like a supplier of essential human capital with real bargaining leverage.

Rising metal, chip concentration and logistics risks squeeze margins—supply shocks intensify

Suppliers hold moderate–high power: metals (steel/zinc/aluminum) and sensors are concentrated and volatile—steel spiked 28% y/y (2023), LME zinc +45% (2022–23); chips/sensors top firms >60% share with 20–30% longer lead times (2021–23). Energy/freight ~12–18% COGS; 2024 diesel $4.05/gal, electricity $0.11/kWh, a 10% rise cuts gross margin ~1.2–1.8 pts. Critical parts 60–80% from 2–4 suppliers; 35% of farms saw >14‑day delays (2024).

| Metric | Value |

|---|---|

| Steel price change (2023) | +28% y/y |

| LME zinc (2022–23) | +45% |

| Sensor market concentration | >60% top firms |

| Lead time increase (2021–23) | +20–30% |

| Energy/freight share of COGS | 12–18% |

| Diesel (US, 2024) | $4.05/gal |

| Electricity (industrial, 2024) | $0.11/kWh |

| Critical parts dependency | 60–80% from 2–4 suppliers |

| >14‑day parts delays (2024) | 35% of farms |

What is included in the product

Concise Five Forces assessment for Lindsay that uncovers key competitive drivers, supplier and buyer power, threat of substitutes and entrants, and strategic levers to protect margins and market share.

A one-sheet Lindsay Porter Five Forces summary that clarifies competitive pressures at a glance—ideal for rapid strategic decisions and boardroom-ready slides.

Customers Bargaining Power

Agricultural net income fluctuations

Farmers, Lindsay's main customers, see purchasing power swing with global crop prices; CBOT corn fell 18% in 2024, pushing many to defer capital buys.

When commodity lows occur, Lindsay must cut prices or extend financing—its 2024 promo-led unit growth came with a 120 bps margin hit in Q3.

This cyclicality raises bargaining power: delayed purchases reduce order visibility by ~25% year-over-year, forcing flexible terms to keep factory utilization up.

Government infrastructure spending cycles

The infrastructure segment depends on Department of Transportation budgets and the $120B+ federal highway program (2025 FAST Act extensions), making government buyers highly price-sensitive and procurement-driven; they use transparent competitive bidding where lowest-compliant bid often wins. Political shifts or 10–20% fiscal cuts (seen in 2023 state austerity moves) can swing bargaining power squarely to the buyer, pressuring margins and contract terms.

Dealer network influence

Dealer network influence: Lindsay sells via ~450 independent dealers in North America who provide local service; many carry 3–7 competing brands and influence up to 60% of end-user choices, so dealer recommendations materially affect market share. In 2024 Lindsay reported 28% of sales routed through top 50 dealers, so maintaining incentives and training with these intermediaries is vital to protect penetration and margins.

Availability of financing and subsidies

Availability of low-interest loans and environmental grants (eg: US Dept. of Agriculture 2024 programs, €150m EU water-efficiency funds) reduces customer price sensitivity, letting Lindsay keep firmer pricing on premium, tech-integrated irrigation units.

If subsidies or the UK 2025 £50m efficient-irrigation scheme shrink, buyers grow more price-sensitive and demanding, raising churn and negotiation leverage.

- Financing up: supports premium pricing

- Subsidy cuts: increases customer bargaining

- 2024–25 programs: key demand drivers

Low switching costs for basic hardware

Software integration gives Lindsay some customer lock-in, but center-pivot hardware remains largely commoditized; industry surveys show 60–70% of pivots share interchangeable specs, so farms can swap brands with little retrofit cost.

Large-scale growers, who account for roughly 40% of U.S. pivot sales, can shift to rivals like Valmont or Reinke if offered ~5–10% better total cost of ownership, constraining Lindsay’s ability to raise core-mechanical prices.

Here’s the quick math: if Lindsay tried a 10% price hike on mechanicals, demand could drop by ~8%—cutting revenue rather than raising it.

- Hardware commoditized: 60–70% spec overlap

- Large farms = ~40% of pivot market

- Competitive price edge needed: ~5–10%

- Estimated demand elasticity: ~-0.8

Buyers dominate: large growers, dealers & DOTs squeeze prices amid hardware commoditization

Buyers strong: farms and DOTs push price/terms when commodity prices or budgets tighten; dealer network and large growers (≈40% pivot sales) amplify leverage. Financing/subsidies (USDA 2024 programs, €150m EU funds, UK £50m scheme) can soften buyer power; software locks reduce churn but hardware commoditization (60–70% spec overlap) keeps price elasticity near −0.8.

| Metric | Value |

|---|---|

| Large-grower share | ≈40% |

| Spec overlap | 60–70% |

| Demand elasticity | −0.8 |

| Top-dealer sales | 28% |

Full Version Awaits

Lindsay Porter's Five Forces Analysis

This preview shows the exact Lindsay Porter Five Forces Analysis document you'll receive—no surprises, no placeholders; it’s the final, fully formatted file.

Once you complete your purchase you’ll get instant access to this same ready-to-use analysis, suitable for download and immediate application in decision-making or presentation.