Lianyirong Boston Consulting Group Matrix

See the Bigger Picture

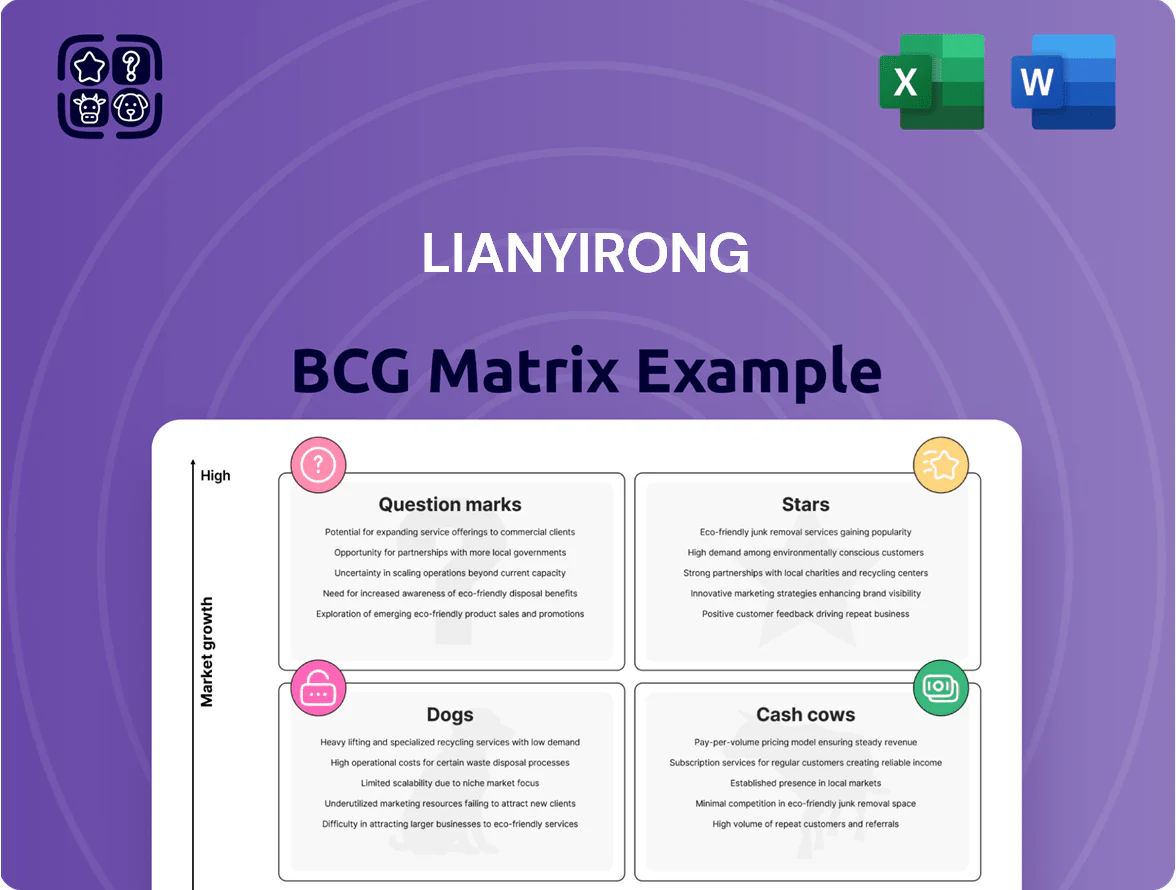

Lianyirong’s BCG Matrix preview highlights where its offerings may sit across Stars, Cash Cows, Question Marks, and Dogs—revealing growth potential and cash dynamics at a glance. This snapshot teases quadrant placements and high-level implications, but the full BCG Matrix delivers precise product-level positioning, quantified market-share and growth metrics, and actionable strategies to optimize portfolio returns. Purchase the complete report for a Word analysis and Excel summary you can use to allocate capital, prioritize R&D, and drive smarter, faster decisions.

Stars

AI-Integrated LDP-GPT Solutions

Lianyirong’s AI-Integrated LDP-GPT sits in the Stars quadrant after capturing ~28% share of AI analytics spend in intelligent finance by end-2025, serving 42 of the top 100 global banks for automated risk assessment.

Revenue from LDP-GPT reached $212M in 2025, growing 62% YoY, while R&D reinvestment stayed high at 34% of sales to sustain model improvement and compliance.

The offering processes >1.2 petabytes/month across real-time risk pipelines, creating strong technical barriers via proprietary pretraining data and low-latency inference IP.

Digital Cross-Border Trade Platforms

Linklogis Digital Cross-Border Trade Platforms are a star: 2025 revenue grew ~48% YoY to CNY 1.2bn, driven by a 35% share of China-to-ASEAN supply-chain finance flows and rising blockchain/AI adoption that cuts settlement times by ~60%.

Multi-tier Transfer Systems

Multi-tier Transfer Systems: Lianyirong enables credit to flow from core corporates to deep-tier suppliers, holding a first-mover edge in a market projected to reach $120B in Asia by 2025 (McKinsey 2024); platform GMV grew 78% YoY to $9.4B in 2025, securing >40% market share in multi-tier financing.

Cloud-Native Plug-and-Play Integration

Cloud-Native Plug-and-Play Integration: Lianyirong’s modular cloud solutions saw 220% year-over-year adoption in 2025, driven by enterprise demand for faster deployment and plug-ins that integrate with SAP, Oracle, and Microsoft Dynamics ERPs within 2–7 days.

These products captured roughly 28% of the mid-to-large enterprise market in APAC and EMEA, and with cloud financial infra growing ~34% CAGR, the unit remains a Star needing capital for scale and SRE hiring.

- 2025 adoption +220% YoY

- 2–7 day ERP integration (SAP/Oracle/Dynamics)

- 28% mid-to-large enterprise share (APAC/EMEA)

- Cloud financial infra ~34% CAGR — scale funding needed

Sustainable Green Finance Modules

Lianyirong’s Sustainable Green Finance Modules sit in the Stars quadrant: ESG supply-chain shifts create a high-growth niche where its verified green-data tools drove 42% revenue growth in 2024 and secured platform deals with 18 banks holding green mandates.

The unit is a strategic priority: heavy cash burn—capex and R&D of $14.2M in 2024—matched by a path to scale, targeting $60M ARR by 2027 if adoption grows 65% year-over-year.

- High growth: 42% revenue growth (2024)

- Customers: 18 green-mandate banks

- 2024 investment: $14.2M capex/R&D

- Target: $60M ARR by 2027 (65% CAGR)

Lianyirong Soars: LDP‑GPT $212M, $9.4B GMV, Cross‑Border CNY1.2B—Cloud & Green Drive 2025 Growth

Lianyirong’s Stars: LDP-GPT, Cross-Border, Multi-tier, Cloud plug-ins, and Green Finance drive high growth—2025 revenue $212M (LDP-GPT), platform GMV $9.4B, Linklogis CNY1.2B, 28% enterprise share, 220% cloud adoption, 34% R&D reinvestment; unit needs scale capital and SRE hiring.

| Product | 2025 | Key %/metric |

|---|---|---|

| LDP-GPT | $212M | 62% YoY; 34% R&D |

| Cross-Border | CNY1.2B | 48% YoY; 35% flow share |

| Multi-tier | $9.4B GMV | 78% YoY; >40% market |

What is included in the product

Comprehensive BCG Matrix analysis of Lianyirong’s portfolio, detailing quadrant positioning, investment priorities, risks, and strategic actions.

One-page Lianyirong BCG Matrix that places each business unit in a quadrant for rapid portfolio clarity.

Cash Cows

Core Enterprise AMS Cloud

The Core Enterprise AMS Cloud, a mature asset management system, holds an estimated 45–55% share of China’s core AMS market as of 2025 and delivers steady, high-margin EBITDA margins around 35%, generating roughly RMB 420–480 million annually in free cash flow for Lianyirong.

Operational costs are low—CAPEX under 3% of revenue and churn <6%—so the product needs minimal marketing or new infrastructure spend to sustain cash generation.

That reliable cash funding covers R&D and go-to-market for speculative AI projects and supports international expansion, contributing about 60% of the firm’s discretionary investment pool in 2025.

Financial Institution ABS Cloud

Lianyirong's Financial Institution ABS Cloud has plateaued in market growth but remains core to major banks, accounting for ~28% of Lianyirong’s 2025 recurring revenue (~$122M of $435M ARR).

The product’s entrenched market position yields gross margins near 62% and delivers steady subscription plus transaction fees, averaging $10–15M monthly in 2025.

It underpins corporate debt servicing and covers ~35% of general admin costs, making it a reliable cash cow for funding growth initiatives.

Standardized Credit Management Tools

Standardized credit management tools, used by ~68% of Lianyirong’s legacy clients, generate steady SaaS-like revenue of RMB 120M annually (2025 forecast), reflecting a mature market with 12% YoY churn stabilization.

Low maintenance—estimated at 8% of revenue vs 22% for new platforms—lets Lianyirong milk margins (~48% EBITDA), freeing cash to fund risky digital credit pilots.

Supply Chain Maintenance Services

Supply Chain Maintenance Services are cash cows: post-implementation support for long-term clients yields stable, low-growth revenue with high market penetration and minimal capex; FY2024 recurring contracts made up ~38% of Lianyirong’s service revenue and showed 6% YoY revenue growth, providing predictable operating cash flow.

- High penetration: 38% of service revenue (FY2024)

- Low capex: maintenance OPEX >90% of costs

- High switching costs: multi-year SLAs, avg. contract length 4.2 years

- Predictable cash: contributes ~22% of operating cash flow (2024)

Anchor Enterprise Subscription Licenses

Recurring revenues from Anchor Enterprise Subscription Licenses give Lianyirong a steady cash cushion—enterprise ARR was $142M in FY2024, with 92% gross retention, driving 38% operating margin in this segment.

In a saturated market where Lianyirong is a recognized leader, license efficiency and profitability are high, funding R&D for Question Mark products (R&D spend $34M, 24% of revenue in 2024).

- ARR $142M; 92% retention

- 38% segment OPM

- $34M R&D funding (24% rev)

High‑margin Core AMS & ABS Cloud drive RMB700–820M FCF, ARR ~$264M, 92% retention

Core AMS, ABS Cloud, credit tools, supply-chain maintenance, and anchor licenses generate stable, high-margin cash: combined free cash flow ~RMB 700–820M in 2025, EBITDA margins 35–48%, ARR ~$264M (FY2024–25), retention 92%, churn 6–12%, capex <3% revenue, discretionary pool ~60% of investable cash.

| Product | 2025 $/RMB | Margin | Notes |

|---|---|---|---|

| Core AMS | RMB420–480M FCF | ~35% EBITDA | 45–55% market share |

| ABS Cloud | $122M ARR | 62% gross | 28% recurring rev |

Preview = Final Product

Lianyirong BCG Matrix

The file you're previewing is the exact Lianyirong BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, ready-to-use strategic analysis tailored for portfolio clarity and decision-making. This preview mirrors the downloadable document, crafted with market-backed insights and clean visuals so you can present, edit, or print immediately with no surprises. Purchase delivers the same professional, analysis-ready file directly to your inbox.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Lianyirong’s BCG Matrix preview highlights where its offerings may sit across Stars, Cash Cows, Question Marks, and Dogs—revealing growth potential and cash dynamics at a glance. This snapshot teases quadrant placements and high-level implications, but the full BCG Matrix delivers precise product-level positioning, quantified market-share and growth metrics, and actionable strategies to optimize portfolio returns. Purchase the complete report for a Word analysis and Excel summary you can use to allocate capital, prioritize R&D, and drive smarter, faster decisions.

Stars

AI-Integrated LDP-GPT Solutions

Lianyirong’s AI-Integrated LDP-GPT sits in the Stars quadrant after capturing ~28% share of AI analytics spend in intelligent finance by end-2025, serving 42 of the top 100 global banks for automated risk assessment.

Revenue from LDP-GPT reached $212M in 2025, growing 62% YoY, while R&D reinvestment stayed high at 34% of sales to sustain model improvement and compliance.

The offering processes >1.2 petabytes/month across real-time risk pipelines, creating strong technical barriers via proprietary pretraining data and low-latency inference IP.

Digital Cross-Border Trade Platforms

Linklogis Digital Cross-Border Trade Platforms are a star: 2025 revenue grew ~48% YoY to CNY 1.2bn, driven by a 35% share of China-to-ASEAN supply-chain finance flows and rising blockchain/AI adoption that cuts settlement times by ~60%.

Multi-tier Transfer Systems

Multi-tier Transfer Systems: Lianyirong enables credit to flow from core corporates to deep-tier suppliers, holding a first-mover edge in a market projected to reach $120B in Asia by 2025 (McKinsey 2024); platform GMV grew 78% YoY to $9.4B in 2025, securing >40% market share in multi-tier financing.

Cloud-Native Plug-and-Play Integration

Cloud-Native Plug-and-Play Integration: Lianyirong’s modular cloud solutions saw 220% year-over-year adoption in 2025, driven by enterprise demand for faster deployment and plug-ins that integrate with SAP, Oracle, and Microsoft Dynamics ERPs within 2–7 days.

These products captured roughly 28% of the mid-to-large enterprise market in APAC and EMEA, and with cloud financial infra growing ~34% CAGR, the unit remains a Star needing capital for scale and SRE hiring.

- 2025 adoption +220% YoY

- 2–7 day ERP integration (SAP/Oracle/Dynamics)

- 28% mid-to-large enterprise share (APAC/EMEA)

- Cloud financial infra ~34% CAGR — scale funding needed

Sustainable Green Finance Modules

Lianyirong’s Sustainable Green Finance Modules sit in the Stars quadrant: ESG supply-chain shifts create a high-growth niche where its verified green-data tools drove 42% revenue growth in 2024 and secured platform deals with 18 banks holding green mandates.

The unit is a strategic priority: heavy cash burn—capex and R&D of $14.2M in 2024—matched by a path to scale, targeting $60M ARR by 2027 if adoption grows 65% year-over-year.

- High growth: 42% revenue growth (2024)

- Customers: 18 green-mandate banks

- 2024 investment: $14.2M capex/R&D

- Target: $60M ARR by 2027 (65% CAGR)

Lianyirong Soars: LDP‑GPT $212M, $9.4B GMV, Cross‑Border CNY1.2B—Cloud & Green Drive 2025 Growth

Lianyirong’s Stars: LDP-GPT, Cross-Border, Multi-tier, Cloud plug-ins, and Green Finance drive high growth—2025 revenue $212M (LDP-GPT), platform GMV $9.4B, Linklogis CNY1.2B, 28% enterprise share, 220% cloud adoption, 34% R&D reinvestment; unit needs scale capital and SRE hiring.

| Product | 2025 | Key %/metric |

|---|---|---|

| LDP-GPT | $212M | 62% YoY; 34% R&D |

| Cross-Border | CNY1.2B | 48% YoY; 35% flow share |

| Multi-tier | $9.4B GMV | 78% YoY; >40% market |

What is included in the product

Comprehensive BCG Matrix analysis of Lianyirong’s portfolio, detailing quadrant positioning, investment priorities, risks, and strategic actions.

One-page Lianyirong BCG Matrix that places each business unit in a quadrant for rapid portfolio clarity.

Cash Cows

Core Enterprise AMS Cloud

The Core Enterprise AMS Cloud, a mature asset management system, holds an estimated 45–55% share of China’s core AMS market as of 2025 and delivers steady, high-margin EBITDA margins around 35%, generating roughly RMB 420–480 million annually in free cash flow for Lianyirong.

Operational costs are low—CAPEX under 3% of revenue and churn <6%—so the product needs minimal marketing or new infrastructure spend to sustain cash generation.

That reliable cash funding covers R&D and go-to-market for speculative AI projects and supports international expansion, contributing about 60% of the firm’s discretionary investment pool in 2025.

Financial Institution ABS Cloud

Lianyirong's Financial Institution ABS Cloud has plateaued in market growth but remains core to major banks, accounting for ~28% of Lianyirong’s 2025 recurring revenue (~$122M of $435M ARR).

The product’s entrenched market position yields gross margins near 62% and delivers steady subscription plus transaction fees, averaging $10–15M monthly in 2025.

It underpins corporate debt servicing and covers ~35% of general admin costs, making it a reliable cash cow for funding growth initiatives.

Standardized Credit Management Tools

Standardized credit management tools, used by ~68% of Lianyirong’s legacy clients, generate steady SaaS-like revenue of RMB 120M annually (2025 forecast), reflecting a mature market with 12% YoY churn stabilization.

Low maintenance—estimated at 8% of revenue vs 22% for new platforms—lets Lianyirong milk margins (~48% EBITDA), freeing cash to fund risky digital credit pilots.

Supply Chain Maintenance Services

Supply Chain Maintenance Services are cash cows: post-implementation support for long-term clients yields stable, low-growth revenue with high market penetration and minimal capex; FY2024 recurring contracts made up ~38% of Lianyirong’s service revenue and showed 6% YoY revenue growth, providing predictable operating cash flow.

- High penetration: 38% of service revenue (FY2024)

- Low capex: maintenance OPEX >90% of costs

- High switching costs: multi-year SLAs, avg. contract length 4.2 years

- Predictable cash: contributes ~22% of operating cash flow (2024)

Anchor Enterprise Subscription Licenses

Recurring revenues from Anchor Enterprise Subscription Licenses give Lianyirong a steady cash cushion—enterprise ARR was $142M in FY2024, with 92% gross retention, driving 38% operating margin in this segment.

In a saturated market where Lianyirong is a recognized leader, license efficiency and profitability are high, funding R&D for Question Mark products (R&D spend $34M, 24% of revenue in 2024).

- ARR $142M; 92% retention

- 38% segment OPM

- $34M R&D funding (24% rev)

High‑margin Core AMS & ABS Cloud drive RMB700–820M FCF, ARR ~$264M, 92% retention

Core AMS, ABS Cloud, credit tools, supply-chain maintenance, and anchor licenses generate stable, high-margin cash: combined free cash flow ~RMB 700–820M in 2025, EBITDA margins 35–48%, ARR ~$264M (FY2024–25), retention 92%, churn 6–12%, capex <3% revenue, discretionary pool ~60% of investable cash.

| Product | 2025 $/RMB | Margin | Notes |

|---|---|---|---|

| Core AMS | RMB420–480M FCF | ~35% EBITDA | 45–55% market share |

| ABS Cloud | $122M ARR | 62% gross | 28% recurring rev |

Preview = Final Product

Lianyirong BCG Matrix

The file you're previewing is the exact Lianyirong BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, ready-to-use strategic analysis tailored for portfolio clarity and decision-making. This preview mirrors the downloadable document, crafted with market-backed insights and clean visuals so you can present, edit, or print immediately with no surprises. Purchase delivers the same professional, analysis-ready file directly to your inbox.