Lippert PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

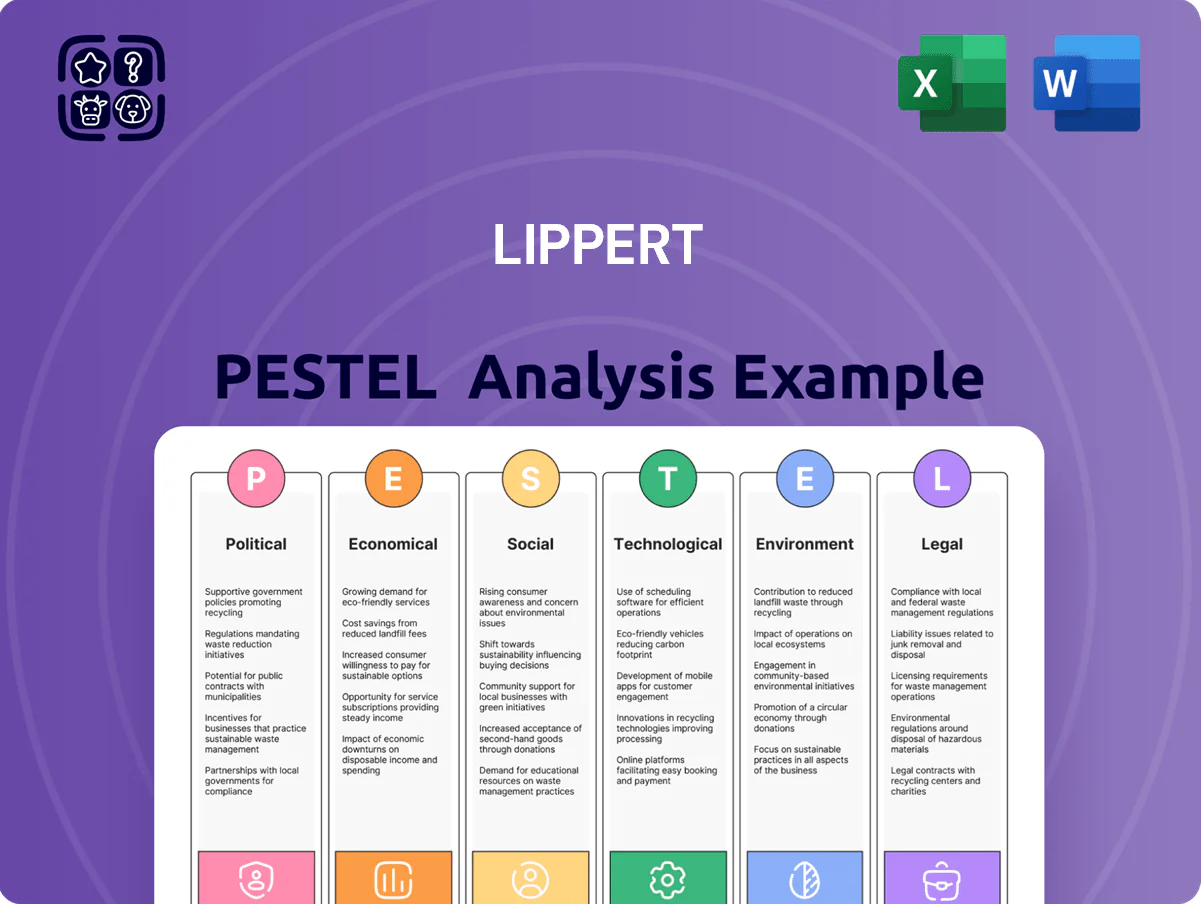

Unlock strategic clarity with our Lippert PESTLE Analysis—concise, expert-led insights into political, economic, social, technological, legal, and environmental forces shaping the company’s future; ideal for investors and strategists. Purchase the full report to access deep-dive findings, risk forecasts, and ready-to-use recommendations you can apply immediately.

Political factors

Global Trade and Tariff Policies

Lippert’s heavy reliance on international supply chains for steel and aluminum—about 45% of procurement sourced from Mexico and Asia as of Q3 2025—heightens exposure to shifting trade agreements and tariff adjustments.

A 10 percentage-point rise in US import duties on steel/aluminum could raise component costs by an estimated 6–9%, squeezing 2025 gross margins that averaged ~18% year-to-date.

Protectionist moves or renegotiated pacts with key manufacturing hubs would force price pass-throughs or margin compression across OEM RV and marine contracts.

Management must proactively hedge materials, diversify suppliers, and engage in policy monitoring to sustain competitive pricing for major clients like Thor Industries and Brunswick.

Government Support for Outdoor Infrastructure

Federal and state investments in national parks and public camping infrastructure, including $1.9 billion allocated under the Great American Outdoors Act through 2025, directly boost demand for Lippert components used in RV chassis and suspension systems.

By end-2025, expanded funding and state matching grants increased campground capacity by an estimated 12%, supporting higher RV utilization rates and aftermarket sales.

Political support for outdoor recreation creates a favorable environment for long-term growth in the outdoor lifestyle market, benefiting suppliers of chassis, suspension, and related systems through sustained OEM and replacement part demand.

Regulatory Focus on Electrification

Political mandates to cut CO2 have accelerated EV adoption in RVs and light commercial vehicles, with US federal targets aiming for 50% of new vehicle sales to be electric by 2030 and EU CO2 standards tightening 2024–2025; this shifts demand toward lightweight, electrification-compatible components that Lippert supplies.

Federal EV tax credits and programs like the US Inflation Reduction Act, which allocates over $370 billion for clean energy through 2031, and EU subsidies boost OEM investment in efficient parts, directly benefiting Lippert’s aluminum and composite product lines.

Aligning with these incentives is essential: OEMs increasingly require suppliers to meet EV weight and thermal management specs to secure contracts, and Lippert’s ability to adapt will influence its share of an EV-related aftermarket projected to grow at double-digit CAGR through 2028.

Geopolitical Stability in European Markets

With a significant footprint in Europe, Lippert faces exposure to Eurozone political stability; in 2024 EU manufacturing PMI averaged 48.7, signaling contraction that can affect demand and plant utilization.

Regional conflicts or shifts in EU manufacturing rules—such as 2025 proposed tightening of CO2 and supply-chain due diligence—could disrupt schedules at overseas facilities and raise compliance costs.

Political moves toward reshoring in Germany and France, where incentives grew 18% in 2024, force Lippert to adapt its footprint to secure supply for caravan OEMs and avoid tariff or logistics shocks.

- EU manufacturing PMI 2024: 48.7

- 2024 incentives for reshoring in DE/FR up 18%

- 2025 proposed EU CO2 and supply-chain rules increase compliance risk

Lobbying and Industry Advocacy

Lippert engages with political entities via groups like the RV Industry Association to influence safety and manufacturing standards, aiming to prevent regulations that could raise costs across the $22.5B U.S. RV supply chain (2024) and the $60B marine market (2023–24).

Effective advocacy seeks balance between consumer safety and manufacturer margins, protecting Lippert’s 2024 revenue drivers amid industry-wide material cost pressures (steel up ~15% YoY in 2023–24).

- Active engagement through RVIA

- Protects margins across $22.5B RV supply chain

- Seeks balanced safety rules for $60B marine market

- Mitigates material-cost headwinds (steel +~15% YoY)

Lippert faces tariff-driven cost risks but gains from US/EV stimulus and reshoring pressures

Political risks for Lippert include tariff exposure from 45%+ sourcing in Mexico/Asia, potential 6–9% material-cost hit from higher US steel/aluminum duties, benefit from $1.9B Great American Outdoors Act boosting RV demand, EV policy incentives (IRA $370B+) shifting demand to lightweight/electrification parts, and EU regulatory/reshoring pressures raising compliance and capacity costs.

| Metric | Value |

|---|---|

| Procurement from MX/AS | 45%+ |

| Potential cost rise if tariffs +10pp | 6–9% |

| Great American Outdoors Act through 2025 | $1.9B |

| IRA clean energy funding | $370B+ |

| EU manufacturing PMI 2024 | 48.7 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Lippert across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight region- and industry-specific threats and opportunities.

A concise, visually segmented PESTLE summary tailored to Lippert that’s easy to drop into presentations or share across teams, helping quickly surface external risks and opportunities during planning sessions.

Economic factors

Interest Rate Environment and Financing

As of late 2025, elevated borrowing costs remain a key constraint on RV and boat purchases: US 30-year mortgage-equivalent rates around 6.8% and average new vehicle loan rates near 9% push up monthly payments, reducing demand and pressuring Lippert’s OEM order volumes.

High rates trimmed RV wholesale shipments ~18% YoY in 2024–2025, tightening dealer backlogs and slowing chassis and furniture orders to Lippert.

A pivot toward lower rates—every 100 bps drop can raise demand materially—would spur dealer restocking and lift Lippert revenue from chassis, suspension and interior components.

Raw Material Price Volatility

Steel, aluminum and glass prices swung in 2024–25—hot-rolled coil averaged about $820/ton in 2024 vs $740/ton in 2023, aluminum LME at ~$2,250/ton and flat glass up ~12% y/y—amplifying input cost risk for Lippert. Lippert’s gross margin moves materially with these commodities, necessitating hedging and contract price passes; management targets stabilizing inputs by end-2025 to protect margins across RV, OEM and industrial segments.

Consumer Discretionary Spending Trends

Lippert’s revenue closely tracks US disposable personal income, which rose 3.4% YoY in 2024; declines in disposable income historically cut OEM RV part demand by ~8–12%. During downturns consumers shift to aftermarket repairs—Lippert’s aftermarket sales grew 7% in 2024 as OEM fell 4%. The firm watches the Conference Board consumer confidence (122.1 in Dec 2024) to forecast OEM vs replacement part demand.

Labor Market Dynamics and Automation

- Manufacturing wage inflation ~4.1% (2024)

- US manufacturing vacancies ≈350,000 (2024)

- Lippert increased 2024–25 capex on automation within plant modernization

Housing Market Influence on Building Products

Lippert’s push into residential building products ties revenue to housing cycles; US new home starts fell 8.4% year-over-year in 2025, pressuring windows and doors demand.

Renovation activity buoyed segment in 2024–25 as existing-home sales slowed; exterior product pricing rose ~3.2% in 2024, supporting margins.

Mortgage rates ~6.8% in early 2025 and low national inventory (≈2.9 months supply) are key indicators affecting order books.

- Exposure to new home starts and renovation trends

- Mortgage rates (~6.8% in 2025) influence buyer activity

- Housing inventory ~2.9 months affects replacement vs new-build demand

- Price inflation (~3.2% in 2024) supported margins

Higher rates, commodity inflation hit OEM RVs; aftermarket and automation gain

Higher financing costs (mortgage ~6.8%, auto loans ~9% in 2025) and commodity inflation (HRC ~$820/ton, aluminum ~$2,250/ton) depressed OEM RV orders (~18% drop 2024–25) while boosting aftermarket (+7% in 2024); wage inflation (~4.1% 2024) and 350k manufacturing vacancies spurred automation capex; housing weakness (new starts -8.4% 2025) pressures building-products demand.

| Metric | Value |

|---|---|

| Mortgage rate | ~6.8% (2025) |

| Auto loan rate | ~9% (2025) |

| RV wholesale change | -18% YoY (2024–25) |

| HRC | $820/ton (2024) |

| Aluminum LME | $2,250/ton (2024) |

| Wage inflation | ~4.1% (2024) |

| Manufacturing vacancies | ~350,000 (2024) |

| New home starts | -8.4% (2025) |

Full Version Awaits

Lippert PESTLE Analysis

The preview shown here is the exact Lippert PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our Lippert PESTLE Analysis—concise, expert-led insights into political, economic, social, technological, legal, and environmental forces shaping the company’s future; ideal for investors and strategists. Purchase the full report to access deep-dive findings, risk forecasts, and ready-to-use recommendations you can apply immediately.

Political factors

Global Trade and Tariff Policies

Lippert’s heavy reliance on international supply chains for steel and aluminum—about 45% of procurement sourced from Mexico and Asia as of Q3 2025—heightens exposure to shifting trade agreements and tariff adjustments.

A 10 percentage-point rise in US import duties on steel/aluminum could raise component costs by an estimated 6–9%, squeezing 2025 gross margins that averaged ~18% year-to-date.

Protectionist moves or renegotiated pacts with key manufacturing hubs would force price pass-throughs or margin compression across OEM RV and marine contracts.

Management must proactively hedge materials, diversify suppliers, and engage in policy monitoring to sustain competitive pricing for major clients like Thor Industries and Brunswick.

Government Support for Outdoor Infrastructure

Federal and state investments in national parks and public camping infrastructure, including $1.9 billion allocated under the Great American Outdoors Act through 2025, directly boost demand for Lippert components used in RV chassis and suspension systems.

By end-2025, expanded funding and state matching grants increased campground capacity by an estimated 12%, supporting higher RV utilization rates and aftermarket sales.

Political support for outdoor recreation creates a favorable environment for long-term growth in the outdoor lifestyle market, benefiting suppliers of chassis, suspension, and related systems through sustained OEM and replacement part demand.

Regulatory Focus on Electrification

Political mandates to cut CO2 have accelerated EV adoption in RVs and light commercial vehicles, with US federal targets aiming for 50% of new vehicle sales to be electric by 2030 and EU CO2 standards tightening 2024–2025; this shifts demand toward lightweight, electrification-compatible components that Lippert supplies.

Federal EV tax credits and programs like the US Inflation Reduction Act, which allocates over $370 billion for clean energy through 2031, and EU subsidies boost OEM investment in efficient parts, directly benefiting Lippert’s aluminum and composite product lines.

Aligning with these incentives is essential: OEMs increasingly require suppliers to meet EV weight and thermal management specs to secure contracts, and Lippert’s ability to adapt will influence its share of an EV-related aftermarket projected to grow at double-digit CAGR through 2028.

Geopolitical Stability in European Markets

With a significant footprint in Europe, Lippert faces exposure to Eurozone political stability; in 2024 EU manufacturing PMI averaged 48.7, signaling contraction that can affect demand and plant utilization.

Regional conflicts or shifts in EU manufacturing rules—such as 2025 proposed tightening of CO2 and supply-chain due diligence—could disrupt schedules at overseas facilities and raise compliance costs.

Political moves toward reshoring in Germany and France, where incentives grew 18% in 2024, force Lippert to adapt its footprint to secure supply for caravan OEMs and avoid tariff or logistics shocks.

- EU manufacturing PMI 2024: 48.7

- 2024 incentives for reshoring in DE/FR up 18%

- 2025 proposed EU CO2 and supply-chain rules increase compliance risk

Lobbying and Industry Advocacy

Lippert engages with political entities via groups like the RV Industry Association to influence safety and manufacturing standards, aiming to prevent regulations that could raise costs across the $22.5B U.S. RV supply chain (2024) and the $60B marine market (2023–24).

Effective advocacy seeks balance between consumer safety and manufacturer margins, protecting Lippert’s 2024 revenue drivers amid industry-wide material cost pressures (steel up ~15% YoY in 2023–24).

- Active engagement through RVIA

- Protects margins across $22.5B RV supply chain

- Seeks balanced safety rules for $60B marine market

- Mitigates material-cost headwinds (steel +~15% YoY)

Lippert faces tariff-driven cost risks but gains from US/EV stimulus and reshoring pressures

Political risks for Lippert include tariff exposure from 45%+ sourcing in Mexico/Asia, potential 6–9% material-cost hit from higher US steel/aluminum duties, benefit from $1.9B Great American Outdoors Act boosting RV demand, EV policy incentives (IRA $370B+) shifting demand to lightweight/electrification parts, and EU regulatory/reshoring pressures raising compliance and capacity costs.

| Metric | Value |

|---|---|

| Procurement from MX/AS | 45%+ |

| Potential cost rise if tariffs +10pp | 6–9% |

| Great American Outdoors Act through 2025 | $1.9B |

| IRA clean energy funding | $370B+ |

| EU manufacturing PMI 2024 | 48.7 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Lippert across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight region- and industry-specific threats and opportunities.

A concise, visually segmented PESTLE summary tailored to Lippert that’s easy to drop into presentations or share across teams, helping quickly surface external risks and opportunities during planning sessions.

Economic factors

Interest Rate Environment and Financing

As of late 2025, elevated borrowing costs remain a key constraint on RV and boat purchases: US 30-year mortgage-equivalent rates around 6.8% and average new vehicle loan rates near 9% push up monthly payments, reducing demand and pressuring Lippert’s OEM order volumes.

High rates trimmed RV wholesale shipments ~18% YoY in 2024–2025, tightening dealer backlogs and slowing chassis and furniture orders to Lippert.

A pivot toward lower rates—every 100 bps drop can raise demand materially—would spur dealer restocking and lift Lippert revenue from chassis, suspension and interior components.

Raw Material Price Volatility

Steel, aluminum and glass prices swung in 2024–25—hot-rolled coil averaged about $820/ton in 2024 vs $740/ton in 2023, aluminum LME at ~$2,250/ton and flat glass up ~12% y/y—amplifying input cost risk for Lippert. Lippert’s gross margin moves materially with these commodities, necessitating hedging and contract price passes; management targets stabilizing inputs by end-2025 to protect margins across RV, OEM and industrial segments.

Consumer Discretionary Spending Trends

Lippert’s revenue closely tracks US disposable personal income, which rose 3.4% YoY in 2024; declines in disposable income historically cut OEM RV part demand by ~8–12%. During downturns consumers shift to aftermarket repairs—Lippert’s aftermarket sales grew 7% in 2024 as OEM fell 4%. The firm watches the Conference Board consumer confidence (122.1 in Dec 2024) to forecast OEM vs replacement part demand.

Labor Market Dynamics and Automation

- Manufacturing wage inflation ~4.1% (2024)

- US manufacturing vacancies ≈350,000 (2024)

- Lippert increased 2024–25 capex on automation within plant modernization

Housing Market Influence on Building Products

Lippert’s push into residential building products ties revenue to housing cycles; US new home starts fell 8.4% year-over-year in 2025, pressuring windows and doors demand.

Renovation activity buoyed segment in 2024–25 as existing-home sales slowed; exterior product pricing rose ~3.2% in 2024, supporting margins.

Mortgage rates ~6.8% in early 2025 and low national inventory (≈2.9 months supply) are key indicators affecting order books.

- Exposure to new home starts and renovation trends

- Mortgage rates (~6.8% in 2025) influence buyer activity

- Housing inventory ~2.9 months affects replacement vs new-build demand

- Price inflation (~3.2% in 2024) supported margins

Higher rates, commodity inflation hit OEM RVs; aftermarket and automation gain

Higher financing costs (mortgage ~6.8%, auto loans ~9% in 2025) and commodity inflation (HRC ~$820/ton, aluminum ~$2,250/ton) depressed OEM RV orders (~18% drop 2024–25) while boosting aftermarket (+7% in 2024); wage inflation (~4.1% 2024) and 350k manufacturing vacancies spurred automation capex; housing weakness (new starts -8.4% 2025) pressures building-products demand.

| Metric | Value |

|---|---|

| Mortgage rate | ~6.8% (2025) |

| Auto loan rate | ~9% (2025) |

| RV wholesale change | -18% YoY (2024–25) |

| HRC | $820/ton (2024) |

| Aluminum LME | $2,250/ton (2024) |

| Wage inflation | ~4.1% (2024) |

| Manufacturing vacancies | ~350,000 (2024) |

| New home starts | -8.4% (2025) |

Full Version Awaits

Lippert PESTLE Analysis

The preview shown here is the exact Lippert PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.