Lithia Motors Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

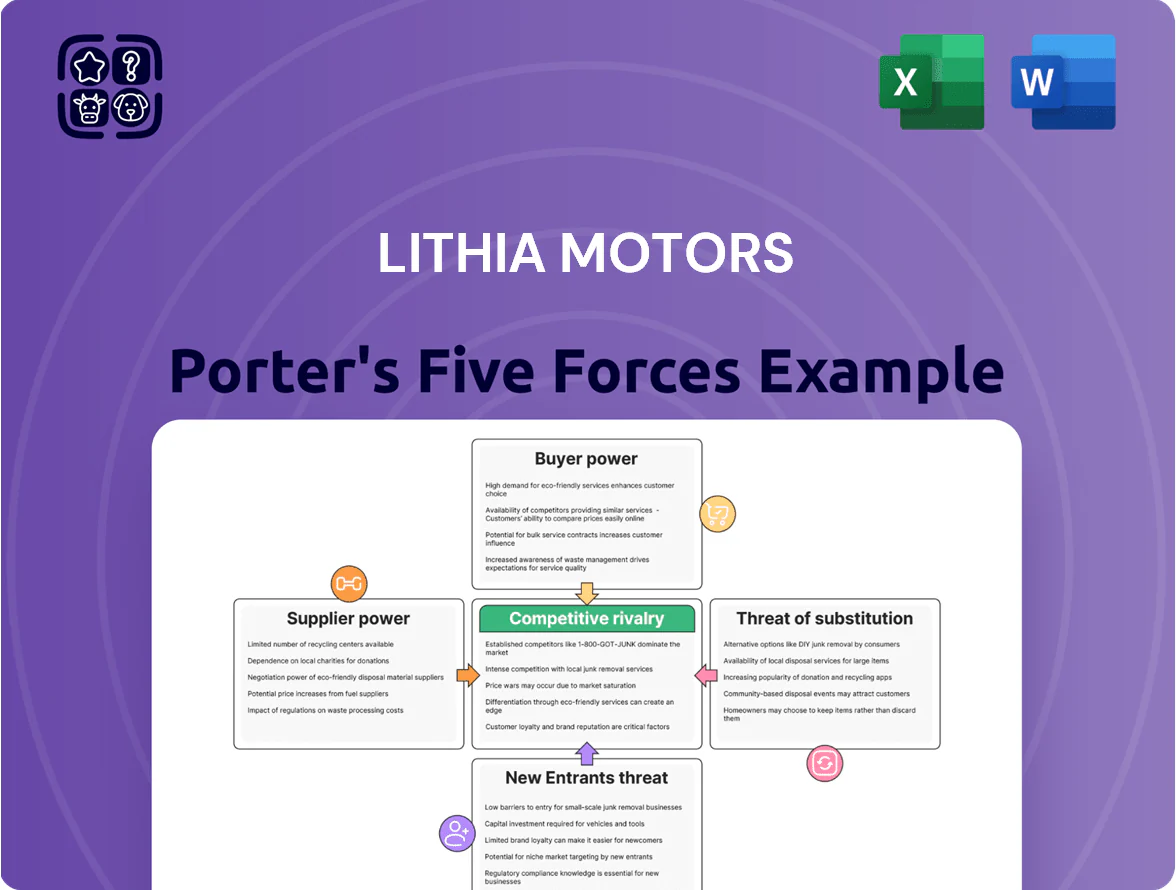

Lithia Motors operates in a fragmented, capital-intensive auto retail sector where dealer consolidation, strong OEM relationships, and digital retailing shape competitive intensity—buyers have growing price transparency, suppliers (OEMs) exert influence via allocation and incentives, and barriers to entry remain moderate due to scale advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lithia Motors’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

OEM Dependency and Franchise Agreements

Major OEMs such as Toyota Motor Corporation, Ford Motor Company, and Stellantis NV enforce strict franchise agreements that give them control over dealer networks; in 2024 these three accounted for roughly 35% of U.S. new-vehicle retail volumes, tightening Lithia Motors' sourcing leverage. OEMs set inventory mixes and often require dealers to accept low-turn models to get high-demand units, raising stocking costs and reducing margins. By end-2025 OEMs' control over EV battery supply chains—where a few suppliers and captive fabs supply ~70% of pack capacity—has amplified OEM bargaining power and constrained Lithia's procurement flexibility.

Inventory Allocation and Pricing Control

Manufacturers control allocation of high-margin models to regions or top dealers, which in 2024 shifted ~15–25% of luxury SUV allocations to premium networks, constraining Lithia’s mix and revenue per unit.

When OEMs raise MSRP or dealer invoice — up 3–7% on average in 2023–2024 for key brands — Lithia has little leverage to absorb those costs without cutting margins.

During 2020–2022 supply shocks OEMs prioritized select dealers; limited-stock windows reduced Lithia’s new-vehicle sales volume by an estimated 6–9% in peak months.

Mandated Facility Standards and Brand Identity

Suppliers force dealerships to spend on brand-mandated renovations and tech—Lithia faced over $400m in facility capex across 2023–2024 for showroom upgrades and dealer network investments, largely non-negotiable to keep authorized status for brands like Toyota and Honda.

Proprietary Parts and Warranty Reimbursement

- High dependence on OEM parts/tools

- Fixed-ops = 27% of Lithia revenue (2024)

- Warranty reimbursements cover ~60–80% of shop costs

- OEM-set labor times limit margin upside

Captive Finance Arm Influence

- Captive lenders ~30% market share (2024)

- Typical floorplan APR 6–9% (2024 data)

- Diversify funding to reduce manufacturer leverage

- Ensure liquidity to keep diverse fleet and fast turnover

OEMs Tighten Grip: Volume, EV Supply & Financing Squeeze Dealers

OEMs hold high supplier power: they controlled ~35% of U.S. new-vehicle volumes (2024), drove EV battery pack concentration (~70% capacity via few suppliers by end-2025), forced $400m+ capex (2023–24), and constrained margins via MSRP/invoice rises (3–7% in 2023–24) plus warranty reimbursements (covering ~60–80% of shop costs); captive lenders (~30% floorplan share, 6–9% APR) further tighten dealer leverage.

| Metric | Value |

|---|---|

| OEM share of U.S. volumes (2024) | ~35% |

| EV pack supply concentration (end-2025) | ~70% |

| Facility capex (2023–24) | $400m+ |

| MSRP/invoice increase (2023–24) | 3–7% |

| Warranty reimbursement coverage | 60–80% |

| Captive floorplan share (2024) | ~30% |

| Typical floorplan APR (2024) | 6–9% |

What is included in the product

Tailored exclusively for Lithia Motors, this Porter's Five Forces analysis uncovers competitive drivers, buyer and supplier power, threats from new entrants and substitutes, and emerging disruptors shaping pricing and profitability.

A concise Porter's Five Forces one-sheet for Lithia Motors—instantly highlights dealer consolidation, supplier leverage, entry threats from online disruptors, buyer bargaining via price comparison, and rivalry intensity to speed strategic decisions.

Customers Bargaining Power

Digital Price Transparency and Comparison Tools

Low Switching Costs Between Dealerships

Customers face almost zero financial penalty switching dealerships, since phone and online quotes and free transfers make moves simple; JD Power found 63% of buyers price-shop multiple dealers in 2024.

Many dealers stock identical brands/models, so price and service dominate—Lithia reported 2024 gross profit per retail unit of $5,200, pressuring margins when competing on price.

The low switching cost forces Lithia to invest in service, digital retail, and 75+ point inspections plus loyalty programs to retain buyers; retention drops raise risk of lost volume.

Omnichannel Purchasing Expectations

Modern buyers expect a seamless shift from online browsing to in-person signing, and Lithia’s Driveway platform—which enabled roughly 25% of Lithia’s US retail units to have digital-touch capabilities in 2024—meets that demand; dealerships without fully digital or hybrid experiences risk losing customers who can switch to competitors offering end-to-end online buying. This trend gives consumers leverage to choose transaction channel and timing, pressuring margins via price transparency and faster comparison shopping.

Financing and Insurance Independence

Buyers increasingly arrive with pre-approved loans from credit unions or online lenders—by 2024 about 32% of U.S. auto purchases used external financing—cutting Lithia Motors’ chance to earn F&I (finance and insurance) markups that once drove 20–25% of dealership gross profit.

That shift gives customers leverage to refuse dealer add-ons and pick cheaper third-party warranties, reducing per-vehicle F&I revenue and pressuring Lithia’s margins.

- ~32% external financing (2024, U.S. auto market)

Influence of Online Reviews and Reputation

Consumer sentiment on platforms like Google, Yelp and social media now shapes buying: a single negative review can be seen by thousands and reduce dealership visits; 2024 JD Power data shows online reviews influence 62% of US car buyers.

Lithia spends heavily on reputation: its 2024 SG&A rose 8% to $3.1B, reflecting customer-service and digital investments because buyers trust peer feedback over ads.

High customer power means consistent service quality is required to keep market share; Lithia’s 2024 same-store service revenue grew 4.5%, showing service focus prevents churn.

- 62% of buyers use online reviews (JD Power 2024)

- SG&A $3.1B in 2024, +8% YoY

- Same-store service revenue +4.5% in 2024

Lithia under margin pressure: shoppers price-shop, finance shifts and rising SG&A

| Metric | 2024 |

|---|---|

| New-vehicle gross profit/unit | −4.2% YoY |

| Price-shop buyers | 63% |

| External financing | ~32% |

| Online review influence | 62% |

| SG&A | $3.1B (+8%) |

What You See Is What You Get

Lithia Motors Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Lithia Motors you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written and fully formatted file you'll be able to download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Lithia Motors operates in a fragmented, capital-intensive auto retail sector where dealer consolidation, strong OEM relationships, and digital retailing shape competitive intensity—buyers have growing price transparency, suppliers (OEMs) exert influence via allocation and incentives, and barriers to entry remain moderate due to scale advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lithia Motors’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

OEM Dependency and Franchise Agreements

Major OEMs such as Toyota Motor Corporation, Ford Motor Company, and Stellantis NV enforce strict franchise agreements that give them control over dealer networks; in 2024 these three accounted for roughly 35% of U.S. new-vehicle retail volumes, tightening Lithia Motors' sourcing leverage. OEMs set inventory mixes and often require dealers to accept low-turn models to get high-demand units, raising stocking costs and reducing margins. By end-2025 OEMs' control over EV battery supply chains—where a few suppliers and captive fabs supply ~70% of pack capacity—has amplified OEM bargaining power and constrained Lithia's procurement flexibility.

Inventory Allocation and Pricing Control

Manufacturers control allocation of high-margin models to regions or top dealers, which in 2024 shifted ~15–25% of luxury SUV allocations to premium networks, constraining Lithia’s mix and revenue per unit.

When OEMs raise MSRP or dealer invoice — up 3–7% on average in 2023–2024 for key brands — Lithia has little leverage to absorb those costs without cutting margins.

During 2020–2022 supply shocks OEMs prioritized select dealers; limited-stock windows reduced Lithia’s new-vehicle sales volume by an estimated 6–9% in peak months.

Mandated Facility Standards and Brand Identity

Suppliers force dealerships to spend on brand-mandated renovations and tech—Lithia faced over $400m in facility capex across 2023–2024 for showroom upgrades and dealer network investments, largely non-negotiable to keep authorized status for brands like Toyota and Honda.

Proprietary Parts and Warranty Reimbursement

- High dependence on OEM parts/tools

- Fixed-ops = 27% of Lithia revenue (2024)

- Warranty reimbursements cover ~60–80% of shop costs

- OEM-set labor times limit margin upside

Captive Finance Arm Influence

- Captive lenders ~30% market share (2024)

- Typical floorplan APR 6–9% (2024 data)

- Diversify funding to reduce manufacturer leverage

- Ensure liquidity to keep diverse fleet and fast turnover

OEMs Tighten Grip: Volume, EV Supply & Financing Squeeze Dealers

OEMs hold high supplier power: they controlled ~35% of U.S. new-vehicle volumes (2024), drove EV battery pack concentration (~70% capacity via few suppliers by end-2025), forced $400m+ capex (2023–24), and constrained margins via MSRP/invoice rises (3–7% in 2023–24) plus warranty reimbursements (covering ~60–80% of shop costs); captive lenders (~30% floorplan share, 6–9% APR) further tighten dealer leverage.

| Metric | Value |

|---|---|

| OEM share of U.S. volumes (2024) | ~35% |

| EV pack supply concentration (end-2025) | ~70% |

| Facility capex (2023–24) | $400m+ |

| MSRP/invoice increase (2023–24) | 3–7% |

| Warranty reimbursement coverage | 60–80% |

| Captive floorplan share (2024) | ~30% |

| Typical floorplan APR (2024) | 6–9% |

What is included in the product

Tailored exclusively for Lithia Motors, this Porter's Five Forces analysis uncovers competitive drivers, buyer and supplier power, threats from new entrants and substitutes, and emerging disruptors shaping pricing and profitability.

A concise Porter's Five Forces one-sheet for Lithia Motors—instantly highlights dealer consolidation, supplier leverage, entry threats from online disruptors, buyer bargaining via price comparison, and rivalry intensity to speed strategic decisions.

Customers Bargaining Power

Digital Price Transparency and Comparison Tools

Low Switching Costs Between Dealerships

Customers face almost zero financial penalty switching dealerships, since phone and online quotes and free transfers make moves simple; JD Power found 63% of buyers price-shop multiple dealers in 2024.

Many dealers stock identical brands/models, so price and service dominate—Lithia reported 2024 gross profit per retail unit of $5,200, pressuring margins when competing on price.

The low switching cost forces Lithia to invest in service, digital retail, and 75+ point inspections plus loyalty programs to retain buyers; retention drops raise risk of lost volume.

Omnichannel Purchasing Expectations

Modern buyers expect a seamless shift from online browsing to in-person signing, and Lithia’s Driveway platform—which enabled roughly 25% of Lithia’s US retail units to have digital-touch capabilities in 2024—meets that demand; dealerships without fully digital or hybrid experiences risk losing customers who can switch to competitors offering end-to-end online buying. This trend gives consumers leverage to choose transaction channel and timing, pressuring margins via price transparency and faster comparison shopping.

Financing and Insurance Independence

Buyers increasingly arrive with pre-approved loans from credit unions or online lenders—by 2024 about 32% of U.S. auto purchases used external financing—cutting Lithia Motors’ chance to earn F&I (finance and insurance) markups that once drove 20–25% of dealership gross profit.

That shift gives customers leverage to refuse dealer add-ons and pick cheaper third-party warranties, reducing per-vehicle F&I revenue and pressuring Lithia’s margins.

- ~32% external financing (2024, U.S. auto market)

Influence of Online Reviews and Reputation

Consumer sentiment on platforms like Google, Yelp and social media now shapes buying: a single negative review can be seen by thousands and reduce dealership visits; 2024 JD Power data shows online reviews influence 62% of US car buyers.

Lithia spends heavily on reputation: its 2024 SG&A rose 8% to $3.1B, reflecting customer-service and digital investments because buyers trust peer feedback over ads.

High customer power means consistent service quality is required to keep market share; Lithia’s 2024 same-store service revenue grew 4.5%, showing service focus prevents churn.

- 62% of buyers use online reviews (JD Power 2024)

- SG&A $3.1B in 2024, +8% YoY

- Same-store service revenue +4.5% in 2024

Lithia under margin pressure: shoppers price-shop, finance shifts and rising SG&A

| Metric | 2024 |

|---|---|

| New-vehicle gross profit/unit | −4.2% YoY |

| Price-shop buyers | 63% |

| External financing | ~32% |

| Online review influence | 62% |

| SG&A | $3.1B (+8%) |

What You See Is What You Get

Lithia Motors Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Lithia Motors you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written and fully formatted file you'll be able to download and use the moment you buy.