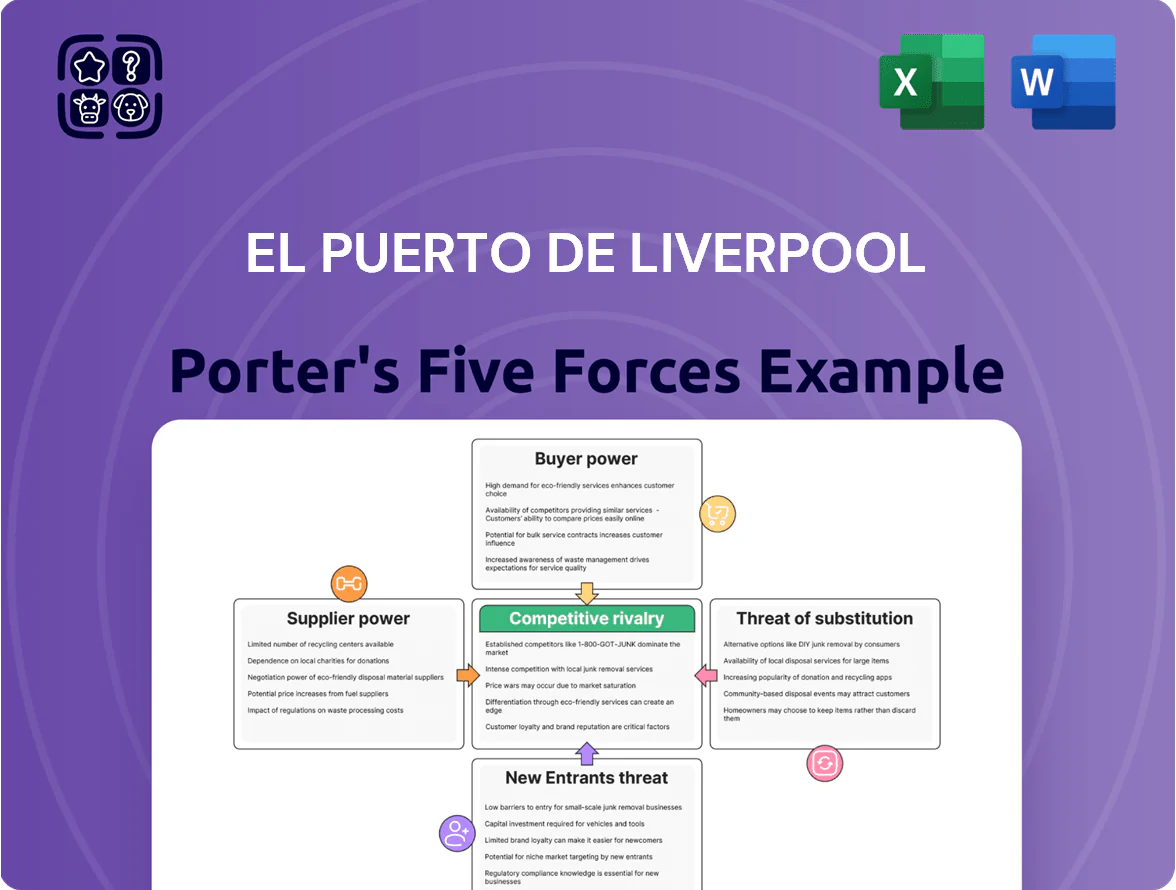

El Puerto de Liverpool Porter's Five Forces Analysis

Don't Miss the Bigger Picture

El Puerto de Liverpool faces intense rivalry from omnichannel retailers and growing pressure from cost-conscious suppliers, while brand loyalty and scale temper buyer power; digital disruption and regional entrants pose moderate threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore El Puerto de Liverpool’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented supplier base for consumer goods

El Puerto de Liverpool sources from thousands of global and local vendors—over 7,500 suppliers in 2024—so no single supplier holds pricing power.

Diversified procurement across apparel, electronics and home goods (category mix: ~40% apparel, 30% home, 30% electronics in 2024) strengthens Liverpool’s leverage in negotiations.

Supplier fragmentation and standardized sourcing allow quick switches if quality or terms worsen, reducing supply risk and preserving margins.

Dominance of premium global brands

While general merchandise suppliers show low bargaining power, premium luxury brands and tech majors like Apple and Sony wield higher leverage; Apple alone accounted for about 6% of Liverpool’s 2024 electronics sales (approx $120m), making replacement costly.

These brands secure better shelf placement and can enforce MAP pricing (minimum advertised price); in 2024 Liverpool granted preferred floor space to 12 luxury labels, boosting category margins by ~1.8 percentage points.

Integration of private label brands

Liverpool and Suburbia have expanded private labels to ~18% of apparel sales by 2025, lifting gross margins for those lines by ~6 percentage points and reducing spend with third-party suppliers by an estimated MXN 3.2 billion in 2024.

Controlling design and production lets the group capture higher margins and cut supply disruption risks, creating a credible backward-integration threat that lowers suppliers’ bargaining power and forces price concessions.

Massive procurement scale and volume

Liverpool’s scale gives it outsized supplier leverage: in 2024 the group reported MXN 165.5 billion in revenue, so suppliers rely on Liverpool to reach Mexico’s ~130m consumers and wider Latin America.

That volume drives preferred payment terms, annual volume discounts often 3–7%, and inventory financing arrangements that smaller rivals cannot secure.

- MXN 165.5bn revenue (2024)

- Market reach: ~130m Mexican consumers

- Typical volume discounts: 3–7%

- Favorable payment and financing terms

Logistics and distribution self-sufficiency

- MXN 2.4bn Arco Norte capex

- 60% national fulfillment handled

- 12% lower transport cost per unit

- Lead time cut: 7→3 days

Diversified supplier base weakens bargaining power despite Apple & luxury pockets

Liverpool’s supplier power is low overall due to 7,500+ suppliers (2024) and MXN 165.5bn revenue, diversified category mix (40% apparel/30% home/30% electronics) and private labels at ~18% of apparel; yet Apple (~6% of electronics sales, ≈$120m) and 12 luxury brands hold localized leverage for shelf space and MAP pricing, while Arco Norte (MXN 2.4bn) cut lead times 7→3 days, lowering supplier bargaining.

| Metric | 2024/2025 |

|---|---|

| Revenue | MXN 165.5bn |

| Suppliers | 7,500+ |

| Category mix | 40/30/30 apparel/home/electronics |

| Private label (apparel) | ~18% |

| Apple share (electronics) | ~6% (~$120m) |

| Arco Norte capex | MXN 2.4bn |

| Lead time | 7→3 days |

What is included in the product

Tailored Porter's Five Forces analysis for El Puerto de Liverpool that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats affecting its retail dominance and profitability.

One-sheet Porter's Five Forces for El Puerto de Liverpool—quickly spot competitive threats and bargaining shifts to inform merchandising, pricing, and expansion decisions.

Customers Bargaining Power

High price sensitivity in the mid-market segment

Through Suburbia, El Puerto de Liverpool targets mid-market shoppers who are highly price-sensitive; 2024 INEGI data show real wages down ~1.2% YoY, boosting sensitivity. These customers face low switching costs and can shift to Coppel or Walmart—Liverpool reported Suburbia sales growth of 2.3% in FY2024 versus Coppel’s 4.1%, signalling competitive pressure. Liverpool must balance tight, value-driven pricing with cost cuts—logistics and inventory turnover improvements—to protect share.

Influence of digital price transparency

Ubiquitous smartphones and e-commerce let customers compare prices in real time inside Liverpool stores, raising buyer power; 82% of Mexican shoppers used mobile price checks in 2024 per Kantar, so Liverpool faces immediate online competition.

This transparency forces Liverpool to match or beat rivals like Amazon and Mercado Libre—Amazon.mx grew 28% and Mercado Libre México GMV rose 22% in 2024—compressing margins.

To keep a price premium, Liverpool must deliver superior service, loyalty perks, or exclusive brands; its 2024 member base of 8.1 million shoppers and LIVERPOOL credit products help, but product exclusivity remains vital.

Lock-in effect of proprietary credit services

Liverpool’s credit arm—over 5.2 million active accounts in 2024—creates strong customer lock-in by making instalment financing easier than bank loans, raising repeat purchase rates (estimated +18% vs non-cardholders). This proprietary credit ecosystem reduces buyer power by embedding loyalty via deferred-pay plans and targeted offers, lowering churn and switching costs and sustaining higher average basket size and lifetime value.

Demand for seamless omnichannel experiences

By 2025 shoppers expect a seamless omnichannel experience across stores, mobile apps, and web, forcing El Puerto de Liverpool to invest in unified inventory and UX; Mexican e-commerce grows 25% y/y (2024), so poor digital performance risks losing market share to agile natives.

If checkout, app stability, or same‑day delivery lag, customers will switch quickly—online retailers capture higher ticket frequency—giving buyers leverage to set Liverpool’s tech and logistics priorities.

- 2024 Mexican e‑commerce +25% y/y

- Same‑day/next‑day demanded by ~40% of shoppers

- Digital failures raise churn and shift spend to natives

Low switching costs for general merchandise

For apparel and household items, customers face low switching costs—no fees or penalties—so they can buy identical brands at specialty stores or chains, giving consumers strong choice power; Mexico's apparel market saw online and off-price options grow 8.2% in 2024, increasing alternatives.

Liverpool counters by investing in store experience and its Liverpool Pay loyalty program (over 4.5 million active users in 2024) to build emotional switching costs and higher retention.

- Low financial switching costs

- Brands widely available elsewhere

- 8.2% market growth in omnichannel/discount 2024

- 4.5M+ active Liverpool Pay users 2024

High buyer leverage pressures margins; Liverpool's membership and exclusives are key

Buyers hold high leverage: price-sensitive mid-market shoppers, low switching costs, and mobile price checks (82% in 2024) compress margins; e‑commerce growth (+25% y/y 2024) and Amazon/Mercado Libre gains force price and service matching. Liverpool’s 8.1M members and 5.2M credit accounts raise retention but product exclusivity and omnichannel execution remain key to limit buyer power.

| Metric | 2024 |

|---|---|

| Mobile price checks | 82% |

| e‑commerce growth | +25% y/y |

| Liverpool members | 8.1M |

| Credit accounts | 5.2M |

Preview the Actual Deliverable

El Puerto de Liverpool Porter's Five Forces Analysis

This preview shows the exact El Puerto de Liverpool Porter’s Five Forces analysis you'll receive after purchase—no placeholders or samples.

The document displayed is the final, professionally formatted file—ready for immediate download and use upon payment.

No mockups: what you see here is the complete deliverable you’ll get instantly after buying.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

El Puerto de Liverpool faces intense rivalry from omnichannel retailers and growing pressure from cost-conscious suppliers, while brand loyalty and scale temper buyer power; digital disruption and regional entrants pose moderate threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore El Puerto de Liverpool’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented supplier base for consumer goods

El Puerto de Liverpool sources from thousands of global and local vendors—over 7,500 suppliers in 2024—so no single supplier holds pricing power.

Diversified procurement across apparel, electronics and home goods (category mix: ~40% apparel, 30% home, 30% electronics in 2024) strengthens Liverpool’s leverage in negotiations.

Supplier fragmentation and standardized sourcing allow quick switches if quality or terms worsen, reducing supply risk and preserving margins.

Dominance of premium global brands

While general merchandise suppliers show low bargaining power, premium luxury brands and tech majors like Apple and Sony wield higher leverage; Apple alone accounted for about 6% of Liverpool’s 2024 electronics sales (approx $120m), making replacement costly.

These brands secure better shelf placement and can enforce MAP pricing (minimum advertised price); in 2024 Liverpool granted preferred floor space to 12 luxury labels, boosting category margins by ~1.8 percentage points.

Integration of private label brands

Liverpool and Suburbia have expanded private labels to ~18% of apparel sales by 2025, lifting gross margins for those lines by ~6 percentage points and reducing spend with third-party suppliers by an estimated MXN 3.2 billion in 2024.

Controlling design and production lets the group capture higher margins and cut supply disruption risks, creating a credible backward-integration threat that lowers suppliers’ bargaining power and forces price concessions.

Massive procurement scale and volume

Liverpool’s scale gives it outsized supplier leverage: in 2024 the group reported MXN 165.5 billion in revenue, so suppliers rely on Liverpool to reach Mexico’s ~130m consumers and wider Latin America.

That volume drives preferred payment terms, annual volume discounts often 3–7%, and inventory financing arrangements that smaller rivals cannot secure.

- MXN 165.5bn revenue (2024)

- Market reach: ~130m Mexican consumers

- Typical volume discounts: 3–7%

- Favorable payment and financing terms

Logistics and distribution self-sufficiency

- MXN 2.4bn Arco Norte capex

- 60% national fulfillment handled

- 12% lower transport cost per unit

- Lead time cut: 7→3 days

Diversified supplier base weakens bargaining power despite Apple & luxury pockets

Liverpool’s supplier power is low overall due to 7,500+ suppliers (2024) and MXN 165.5bn revenue, diversified category mix (40% apparel/30% home/30% electronics) and private labels at ~18% of apparel; yet Apple (~6% of electronics sales, ≈$120m) and 12 luxury brands hold localized leverage for shelf space and MAP pricing, while Arco Norte (MXN 2.4bn) cut lead times 7→3 days, lowering supplier bargaining.

| Metric | 2024/2025 |

|---|---|

| Revenue | MXN 165.5bn |

| Suppliers | 7,500+ |

| Category mix | 40/30/30 apparel/home/electronics |

| Private label (apparel) | ~18% |

| Apple share (electronics) | ~6% (~$120m) |

| Arco Norte capex | MXN 2.4bn |

| Lead time | 7→3 days |

What is included in the product

Tailored Porter's Five Forces analysis for El Puerto de Liverpool that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats affecting its retail dominance and profitability.

One-sheet Porter's Five Forces for El Puerto de Liverpool—quickly spot competitive threats and bargaining shifts to inform merchandising, pricing, and expansion decisions.

Customers Bargaining Power

High price sensitivity in the mid-market segment

Through Suburbia, El Puerto de Liverpool targets mid-market shoppers who are highly price-sensitive; 2024 INEGI data show real wages down ~1.2% YoY, boosting sensitivity. These customers face low switching costs and can shift to Coppel or Walmart—Liverpool reported Suburbia sales growth of 2.3% in FY2024 versus Coppel’s 4.1%, signalling competitive pressure. Liverpool must balance tight, value-driven pricing with cost cuts—logistics and inventory turnover improvements—to protect share.

Influence of digital price transparency

Ubiquitous smartphones and e-commerce let customers compare prices in real time inside Liverpool stores, raising buyer power; 82% of Mexican shoppers used mobile price checks in 2024 per Kantar, so Liverpool faces immediate online competition.

This transparency forces Liverpool to match or beat rivals like Amazon and Mercado Libre—Amazon.mx grew 28% and Mercado Libre México GMV rose 22% in 2024—compressing margins.

To keep a price premium, Liverpool must deliver superior service, loyalty perks, or exclusive brands; its 2024 member base of 8.1 million shoppers and LIVERPOOL credit products help, but product exclusivity remains vital.

Lock-in effect of proprietary credit services

Liverpool’s credit arm—over 5.2 million active accounts in 2024—creates strong customer lock-in by making instalment financing easier than bank loans, raising repeat purchase rates (estimated +18% vs non-cardholders). This proprietary credit ecosystem reduces buyer power by embedding loyalty via deferred-pay plans and targeted offers, lowering churn and switching costs and sustaining higher average basket size and lifetime value.

Demand for seamless omnichannel experiences

By 2025 shoppers expect a seamless omnichannel experience across stores, mobile apps, and web, forcing El Puerto de Liverpool to invest in unified inventory and UX; Mexican e-commerce grows 25% y/y (2024), so poor digital performance risks losing market share to agile natives.

If checkout, app stability, or same‑day delivery lag, customers will switch quickly—online retailers capture higher ticket frequency—giving buyers leverage to set Liverpool’s tech and logistics priorities.

- 2024 Mexican e‑commerce +25% y/y

- Same‑day/next‑day demanded by ~40% of shoppers

- Digital failures raise churn and shift spend to natives

Low switching costs for general merchandise

For apparel and household items, customers face low switching costs—no fees or penalties—so they can buy identical brands at specialty stores or chains, giving consumers strong choice power; Mexico's apparel market saw online and off-price options grow 8.2% in 2024, increasing alternatives.

Liverpool counters by investing in store experience and its Liverpool Pay loyalty program (over 4.5 million active users in 2024) to build emotional switching costs and higher retention.

- Low financial switching costs

- Brands widely available elsewhere

- 8.2% market growth in omnichannel/discount 2024

- 4.5M+ active Liverpool Pay users 2024

High buyer leverage pressures margins; Liverpool's membership and exclusives are key

Buyers hold high leverage: price-sensitive mid-market shoppers, low switching costs, and mobile price checks (82% in 2024) compress margins; e‑commerce growth (+25% y/y 2024) and Amazon/Mercado Libre gains force price and service matching. Liverpool’s 8.1M members and 5.2M credit accounts raise retention but product exclusivity and omnichannel execution remain key to limit buyer power.

| Metric | 2024 |

|---|---|

| Mobile price checks | 82% |

| e‑commerce growth | +25% y/y |

| Liverpool members | 8.1M |

| Credit accounts | 5.2M |

Preview the Actual Deliverable

El Puerto de Liverpool Porter's Five Forces Analysis

This preview shows the exact El Puerto de Liverpool Porter’s Five Forces analysis you'll receive after purchase—no placeholders or samples.

The document displayed is the final, professionally formatted file—ready for immediate download and use upon payment.

No mockups: what you see here is the complete deliverable you’ll get instantly after buying.