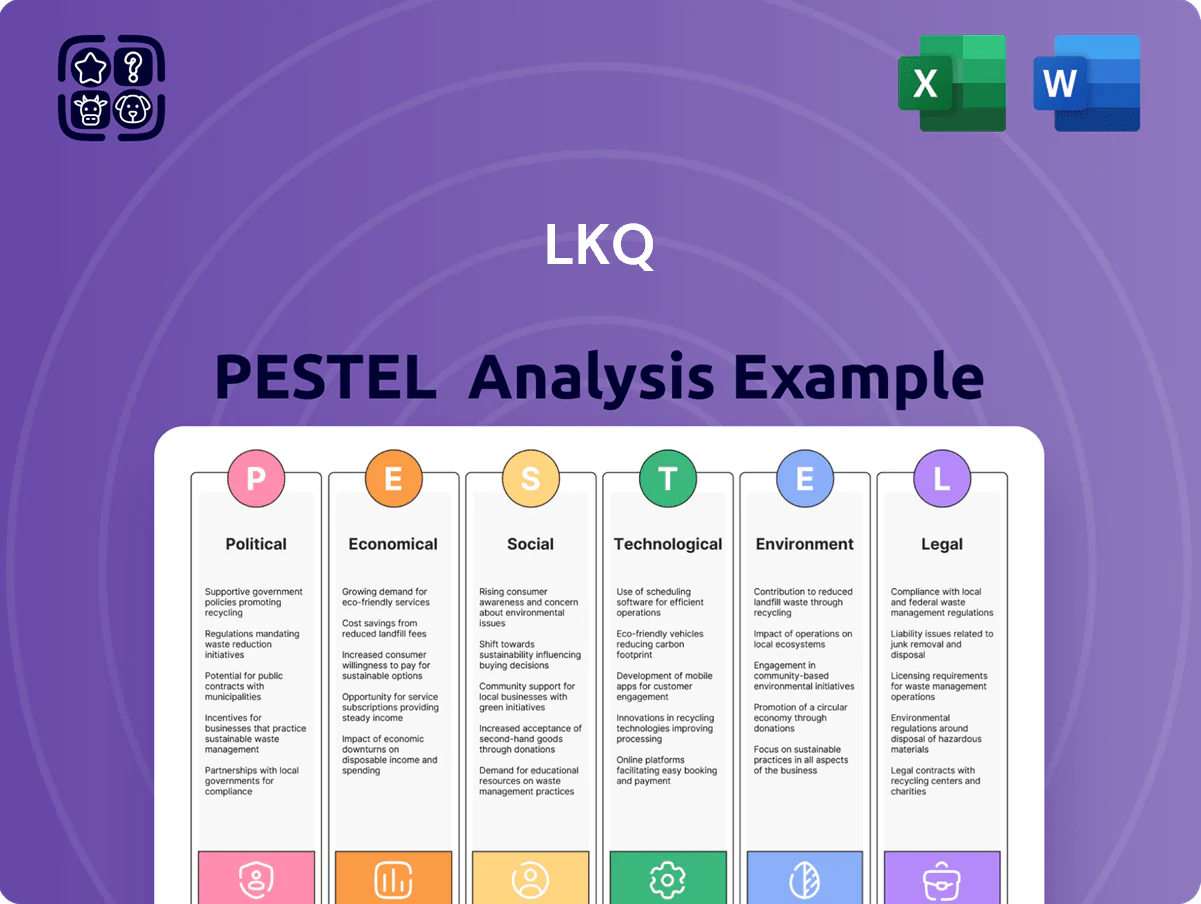

LKQ PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political, economic, social, technological, legal, and environmental forces are reshaping LKQ’s roadmap—our concise PESTLE highlights key risks and opportunities tied to supply chains, regulation, EV transition, and sustainability. Ideal for investors and strategists seeking quick, actionable context, the full PESTLE delivers the deep-dive data and recommendations you need—purchase now for the complete, ready-to-use analysis.

Political factors

International Trade Policy and Tariffs

As of late 2025, tariff measures between the US, China and EU have raised input costs for parts suppliers, with global steel tariffs adding an estimated 5–8% to LKQ’s COGS on metal-intensive SKUs and import duties on finished components increasing procurement expenses by ~3% in FY2024–25.

Right to Repair Legislation

Political support for Right to Repair in North America and Europe is pivotal for LKQ, with US state actions and the EU's 2023 mobility package increasing independent access to vehicle data—affecting LKQ's addressable aftermarket valued at about $255 billion in Europe and North America (2024 est.).

These laws aim to grant independent repairers and parts distributors parity with OEMs on diagnostic tools and telematics, preserving LKQ's wholesale and retail channels that contributed over $9.8 billion in revenue in 2024.

Continued legislative momentum reduces dealer market power, sustaining competitive pricing and margins in the secondary market where LKQ captures significant share of collision and mechanical parts distribution.

Geopolitical Stability in European Markets

With roughly 45% of 2024 revenue generated in Europe (LKQ full-year 2024 revenue €8.2bn), LKQ is highly sensitive to Eurozone and UK political stability and fiscal policy shifts.

Heightened EU-UK trade frictions or regional tensions can disrupt cross-border logistics and reduce labor availability across its 1,200+ European locations.

LKQ monitors EU integration trends and uses scenario planning to adjust regional distribution, aiming to protect service levels and contain incremental operating costs that rose ~3% in 2024.

Government Incentives for Electric Vehicles

Government mandates and subsidies accelerating EV adoption—e.g., 2025 EU target for 50% new car sales to be zero-emission and US federal EV tax credits up to $7,500—reshape the global fleet, reducing ICE vehicles and raising demand for EV parts.

These policies create opportunities for LKQ to expand recycled EV components and battery refurbishment; global EV stock surpassed 26 million in 2023 and is projected to exceed 40 million by 2025, enlarging the used-EV parts market.

Timing and scale of interventions dictate how quickly LKQ must retool inventory, charging it with capex and M&A decisions to build recycling and battery-disassembly capacity within a 2–5 year window.

- EV stock 26M (2023), >40M projected by 2025

- US tax credit: up to $7,500; EU 2025 ZEV targets

- Opportunity: recycled EV parts, battery refurbishment

- Pivot timeframe: 2–5 years; requires capex/M&A

Corporate Tax Policy and Regulation

Changes in corporate tax rates and international tax treaties directly affect LKQ's net margin and capital allocation; a 1 percentage-point rise in effective tax rate on LKQ's 2025 adjusted pre-tax income (~$1.1B FY2024 operating income) could reduce net income by ~$11M annually.

As governments fund infrastructure and green programs, proposed tax hikes or border adjustment taxes could lift LKQ's effective rate from its ~18–20% range, pressuring free cash flow and reinvestment.

Analysts incorporate these policy scenarios into DCFs; a 2-point tax increase can lower terminal value by several percent, altering valuation and dividend/capex plans.

- FY2024 operating income ≈ $1.1B — sensitive to tax-rate shifts

- Effective tax range 18–20% — potential +1–2 ppt downside risk

- 1 ppt tax hike ≈ $11M net income impact; 2 ppt reduces terminal value by multiple %

LKQ: Tariffs, Right‑to‑Repair & EV mandates reshape a $255B aftermarket—45% revenue at risk

Political forces—tariffs (5–8% added COGS on metal SKUs), Right to Repair laws expanding a ~$255bn EU/NA aftermarket, EV mandates (EU 50% ZEV 2025, US tax credits up to $7,500) and tax-rate sensitivity (FY24 op income ~$1.1bn; 1ppt tax ≈ $11m)—drive LKQ’s cost, addressable market and capex/M&A timing; geopolitical or EU‑UK trade friction threatens cross‑border ops and ~45% Europe revenue exposure.

| Metric | Value |

|---|---|

| Europe revenue share | ~45% (2024) |

| FY24 op income | $1.1bn |

| Aftermarket EU/NA | $255bn (2024 est.) |

| EV stock | >40M projected 2025 |

What is included in the product

Explores how macro-environmental factors uniquely affect LKQ across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify threats and opportunities for executives and investors.

A concise, visually segmented LKQ PESTLE summary that can be dropped into presentations or shared across teams to streamline strategic discussions and quickly highlight external risks and market positioning.

Economic factors

Average Age of the Vehicle Fleet

Rising new-car prices and 2024–2025 elevated interest rates have pushed U.S. average vehicle age to a record 12.6 years (IHS Markit), directly benefiting LKQ as older cars need more repairs and replacement parts; each additional year in fleet age historically lifts aftermarket parts demand by ~3–5%, supporting LKQ’s recycled and aftermarket sales which accounted for over 80% of revenue in recent quarters.

Currency Exchange Rate Volatility

Because LKQ operates heavily in Europe and the UK, 2024 FX moves—USD strengthening ~6% vs EUR and ~8% vs GBP year-to-date—can swing reported EPS materially; LKQ noted a $0.10 per-share FX headwind in FY2023. Translation gains or losses flow through consolidated results, with currency volatility affecting revenue converted to USD. Management mitigates exposure via hedging (forwards, options) and increased localized sourcing to reduce transactional risk.

Inflationary Pressures on Logistics and Labor

By end-2025 persistent inflation pushed US fuel prices up ~18% vs 2022 averages and nationwide wage growth for transport/logistics roles ran near 6–8% annually, squeezing margins for distribution-heavy firms like LKQ.

LKQ faces higher costs transporting heavy vehicle parts across its 1,000+ facilities and 120k SKUs while needing to keep competitive pricing for aftermarket customers.

Efficiency gains via route optimization, which can cut fuel costs 5–15%, and warehouse automation investments yielding 10–30% labor productivity improvements are essential to offset rising input costs.

Consumer Disposable Income and Spending

Economic cycles shift household budgets and can push consumers toward DIY repairs; in 2024 US personal saving rate averaged about 3.8% versus 7.5% pre-pandemic, increasing price sensitivity and demand for lower-cost options.

In downturns LKQ’s recycled and aftermarket parts—often 30–60% cheaper than OEM—gain appeal, supporting revenue resilience: LKQ reported 2024 gross margin stability and parts sales growth despite softer discretionary spending.

- Consumer price sensitivity up; saving rate ~3.8% (2024)

- Aftermarket/recycled parts 30–60% cheaper than OEM

- Counter-cyclical demand helps LKQ maintain margins and sales

Interest Rate Environment and Financing Costs

The 2025 US federal funds rate at ~5.25%–5.50% raises LKQ’s average borrowing cost, increasing interest expense and weighing on deal returns for its M&A-driven growth strategy; higher rates make large acquisitions more costly and may slow transaction volume compared with 2021–2023.

Elevated rates also constrain financing options for independent collision repair shops—LKQ’s core B2B customers—reducing demand for inventory and parts financing and pressuring aftermarket sales.

- US policy rate ~5.25%–5.50% (2025)

- Higher cost of debt lowers deal IRR, curbs M&A appetite

- Dealer/shop financing tightened—potential short-term revenue headwind

LKQ poised as aftermarket wins from aging fleet despite FX, cost & rate headwinds

Rising vehicle age (12.6 years, IHS Markit 2024) and 3–5%/year aftermarket demand elasticity benefit LKQ, with recycled/aftermarket >80% revenue; FX volatility (USD +6% vs EUR, +8% vs GBP YTD 2024) and a ~$0.10 FY2023 FX hit affect reported EPS; higher input costs—fuel +18% vs 2022, wages +6–8%—pressure margins but route/warehouse efficiencies (5–30%) can offset; Fed funds ~5.25–5.50% (2025) raises borrowing costs and cools M&A.

| Metric | Value/Impact |

|---|---|

| Avg vehicle age (US) | 12.6 yrs (2024) |

| FX moves (YTD 2024) | USD +6% vs EUR, +8% vs GBP |

| Fuel change | +18% vs 2022 |

| Wage growth | 6–8% (transport/logistics) |

| Fed funds | 5.25–5.50% (2025) |

Preview Before You Purchase

LKQ PESTLE Analysis

The preview shown here is the exact LKQ PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview match the downloadable file you’ll get immediately after checkout; no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political, economic, social, technological, legal, and environmental forces are reshaping LKQ’s roadmap—our concise PESTLE highlights key risks and opportunities tied to supply chains, regulation, EV transition, and sustainability. Ideal for investors and strategists seeking quick, actionable context, the full PESTLE delivers the deep-dive data and recommendations you need—purchase now for the complete, ready-to-use analysis.

Political factors

International Trade Policy and Tariffs

As of late 2025, tariff measures between the US, China and EU have raised input costs for parts suppliers, with global steel tariffs adding an estimated 5–8% to LKQ’s COGS on metal-intensive SKUs and import duties on finished components increasing procurement expenses by ~3% in FY2024–25.

Right to Repair Legislation

Political support for Right to Repair in North America and Europe is pivotal for LKQ, with US state actions and the EU's 2023 mobility package increasing independent access to vehicle data—affecting LKQ's addressable aftermarket valued at about $255 billion in Europe and North America (2024 est.).

These laws aim to grant independent repairers and parts distributors parity with OEMs on diagnostic tools and telematics, preserving LKQ's wholesale and retail channels that contributed over $9.8 billion in revenue in 2024.

Continued legislative momentum reduces dealer market power, sustaining competitive pricing and margins in the secondary market where LKQ captures significant share of collision and mechanical parts distribution.

Geopolitical Stability in European Markets

With roughly 45% of 2024 revenue generated in Europe (LKQ full-year 2024 revenue €8.2bn), LKQ is highly sensitive to Eurozone and UK political stability and fiscal policy shifts.

Heightened EU-UK trade frictions or regional tensions can disrupt cross-border logistics and reduce labor availability across its 1,200+ European locations.

LKQ monitors EU integration trends and uses scenario planning to adjust regional distribution, aiming to protect service levels and contain incremental operating costs that rose ~3% in 2024.

Government Incentives for Electric Vehicles

Government mandates and subsidies accelerating EV adoption—e.g., 2025 EU target for 50% new car sales to be zero-emission and US federal EV tax credits up to $7,500—reshape the global fleet, reducing ICE vehicles and raising demand for EV parts.

These policies create opportunities for LKQ to expand recycled EV components and battery refurbishment; global EV stock surpassed 26 million in 2023 and is projected to exceed 40 million by 2025, enlarging the used-EV parts market.

Timing and scale of interventions dictate how quickly LKQ must retool inventory, charging it with capex and M&A decisions to build recycling and battery-disassembly capacity within a 2–5 year window.

- EV stock 26M (2023), >40M projected by 2025

- US tax credit: up to $7,500; EU 2025 ZEV targets

- Opportunity: recycled EV parts, battery refurbishment

- Pivot timeframe: 2–5 years; requires capex/M&A

Corporate Tax Policy and Regulation

Changes in corporate tax rates and international tax treaties directly affect LKQ's net margin and capital allocation; a 1 percentage-point rise in effective tax rate on LKQ's 2025 adjusted pre-tax income (~$1.1B FY2024 operating income) could reduce net income by ~$11M annually.

As governments fund infrastructure and green programs, proposed tax hikes or border adjustment taxes could lift LKQ's effective rate from its ~18–20% range, pressuring free cash flow and reinvestment.

Analysts incorporate these policy scenarios into DCFs; a 2-point tax increase can lower terminal value by several percent, altering valuation and dividend/capex plans.

- FY2024 operating income ≈ $1.1B — sensitive to tax-rate shifts

- Effective tax range 18–20% — potential +1–2 ppt downside risk

- 1 ppt tax hike ≈ $11M net income impact; 2 ppt reduces terminal value by multiple %

LKQ: Tariffs, Right‑to‑Repair & EV mandates reshape a $255B aftermarket—45% revenue at risk

Political forces—tariffs (5–8% added COGS on metal SKUs), Right to Repair laws expanding a ~$255bn EU/NA aftermarket, EV mandates (EU 50% ZEV 2025, US tax credits up to $7,500) and tax-rate sensitivity (FY24 op income ~$1.1bn; 1ppt tax ≈ $11m)—drive LKQ’s cost, addressable market and capex/M&A timing; geopolitical or EU‑UK trade friction threatens cross‑border ops and ~45% Europe revenue exposure.

| Metric | Value |

|---|---|

| Europe revenue share | ~45% (2024) |

| FY24 op income | $1.1bn |

| Aftermarket EU/NA | $255bn (2024 est.) |

| EV stock | >40M projected 2025 |

What is included in the product

Explores how macro-environmental factors uniquely affect LKQ across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify threats and opportunities for executives and investors.

A concise, visually segmented LKQ PESTLE summary that can be dropped into presentations or shared across teams to streamline strategic discussions and quickly highlight external risks and market positioning.

Economic factors

Average Age of the Vehicle Fleet

Rising new-car prices and 2024–2025 elevated interest rates have pushed U.S. average vehicle age to a record 12.6 years (IHS Markit), directly benefiting LKQ as older cars need more repairs and replacement parts; each additional year in fleet age historically lifts aftermarket parts demand by ~3–5%, supporting LKQ’s recycled and aftermarket sales which accounted for over 80% of revenue in recent quarters.

Currency Exchange Rate Volatility

Because LKQ operates heavily in Europe and the UK, 2024 FX moves—USD strengthening ~6% vs EUR and ~8% vs GBP year-to-date—can swing reported EPS materially; LKQ noted a $0.10 per-share FX headwind in FY2023. Translation gains or losses flow through consolidated results, with currency volatility affecting revenue converted to USD. Management mitigates exposure via hedging (forwards, options) and increased localized sourcing to reduce transactional risk.

Inflationary Pressures on Logistics and Labor

By end-2025 persistent inflation pushed US fuel prices up ~18% vs 2022 averages and nationwide wage growth for transport/logistics roles ran near 6–8% annually, squeezing margins for distribution-heavy firms like LKQ.

LKQ faces higher costs transporting heavy vehicle parts across its 1,000+ facilities and 120k SKUs while needing to keep competitive pricing for aftermarket customers.

Efficiency gains via route optimization, which can cut fuel costs 5–15%, and warehouse automation investments yielding 10–30% labor productivity improvements are essential to offset rising input costs.

Consumer Disposable Income and Spending

Economic cycles shift household budgets and can push consumers toward DIY repairs; in 2024 US personal saving rate averaged about 3.8% versus 7.5% pre-pandemic, increasing price sensitivity and demand for lower-cost options.

In downturns LKQ’s recycled and aftermarket parts—often 30–60% cheaper than OEM—gain appeal, supporting revenue resilience: LKQ reported 2024 gross margin stability and parts sales growth despite softer discretionary spending.

- Consumer price sensitivity up; saving rate ~3.8% (2024)

- Aftermarket/recycled parts 30–60% cheaper than OEM

- Counter-cyclical demand helps LKQ maintain margins and sales

Interest Rate Environment and Financing Costs

The 2025 US federal funds rate at ~5.25%–5.50% raises LKQ’s average borrowing cost, increasing interest expense and weighing on deal returns for its M&A-driven growth strategy; higher rates make large acquisitions more costly and may slow transaction volume compared with 2021–2023.

Elevated rates also constrain financing options for independent collision repair shops—LKQ’s core B2B customers—reducing demand for inventory and parts financing and pressuring aftermarket sales.

- US policy rate ~5.25%–5.50% (2025)

- Higher cost of debt lowers deal IRR, curbs M&A appetite

- Dealer/shop financing tightened—potential short-term revenue headwind

LKQ poised as aftermarket wins from aging fleet despite FX, cost & rate headwinds

Rising vehicle age (12.6 years, IHS Markit 2024) and 3–5%/year aftermarket demand elasticity benefit LKQ, with recycled/aftermarket >80% revenue; FX volatility (USD +6% vs EUR, +8% vs GBP YTD 2024) and a ~$0.10 FY2023 FX hit affect reported EPS; higher input costs—fuel +18% vs 2022, wages +6–8%—pressure margins but route/warehouse efficiencies (5–30%) can offset; Fed funds ~5.25–5.50% (2025) raises borrowing costs and cools M&A.

| Metric | Value/Impact |

|---|---|

| Avg vehicle age (US) | 12.6 yrs (2024) |

| FX moves (YTD 2024) | USD +6% vs EUR, +8% vs GBP |

| Fuel change | +18% vs 2022 |

| Wage growth | 6–8% (transport/logistics) |

| Fed funds | 5.25–5.50% (2025) |

Preview Before You Purchase

LKQ PESTLE Analysis

The preview shown here is the exact LKQ PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview match the downloadable file you’ll get immediately after checkout; no placeholders or surprises.