Lockheed Martin PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic advantage with our concise PESTLE snapshot for Lockheed Martin—spot how geopolitical shifts, defense budgets, tech innovation, and regulatory pressures converge on the company’s trajectory. Ideal for investors and strategists, this briefing highlights risks and opportunities you can act on immediately. Purchase the full PESTLE analysis for a complete, editable report packed with data-driven insights and tactical recommendations.

Political factors

US Defense Budget Allocations

The United States Department of Defense remains Lockheed Martin’s primary revenue source, with DoD budget growth to about $858 billion in FY2025 sustaining demand for advanced platforms amid modernized threats.

Analysts track the National Defense Authorization Act closely because it sets funding levels for the F-35 program—roughly $13.2 billion requested for procurement in FY2025—and for missile defense systems.

Congressional shifts toward Pacific deterrence have redirected capital into Aeronautics and Space, contributing to a 2024–2025 increase in segment backlog and program awards exceeding $20 billion.

Geopolitical Tensions in Eurasia and the Middle East

Persistent instability in Eastern Europe and the Middle East has driven allied demand for advanced weaponry and integrated air defense systems, boosting Lockheed Martin’s Foreign Military Sales; FMS obligations rose to about $18.5 billion in 2024, supporting a strong order flow. The firm’s backlog—$114.3 billion at end-2024—reflects robust demand for tactical missiles and rotary-wing platforms, with deliveries and contract awards expected to remain elevated through the mid-2020s.

NATO Defense Spending Commitments

NATO members' pledge to meet or exceed 2% of GDP on defense has expanded procurement; NATO defense spending reached about $1.23 trillion in 2024, up 4.2% year-on-year, boosting demand for US systems.

Lockheed Martin, as prime F-35 contractor, is central to European fleet upgrades—over 600 F-35s ordered by NATO allies through 2025—supporting interoperability with US forces.

These political commitments underpin multi-decade sustainment contracts; Lockheed reported $9.4 billion in F-35 program sustainment backlog at end-2024, creating predictable revenue streams.

Export Control and ITAR Regulations

Stringent US export controls and ITAR shape Lockheed Martin’s international expansion, limiting direct defense sales—US arms exports fell 12% to $220B in 2024, tightening licensing for platforms like F-35 and hypersonics.

Navigating technology-transfer politics is critical in the Indo-Pacific, where 2024 US security pacts (e.g., AUKUS/expanded ties) affect collaboration and offsets.

Shifts in bilateral agreements can open markets or restrict high-end system sales; hypersonic-related exports face added scrutiny and licensing hurdles.

- US arms exports: $220B in 2024, down 12%

Bipartisan Support for National Security

Despite political polarization, national security is a bipartisan consensus, providing stability for Lockheed Martin’s long-cycle programs; the company reported $67.1 billion in 2024 sales, much tied to multi-year defense contracts. Lockheed’s Washington lobbying and a supply chain spanning all 50 states—over 300,000 U.S. suppliers and suppliers’ economic impact cited in its 2024 reports—shield major programs from abrupt cancellations during political shifts.

- 2024 sales: $67.1B

- U.S. suppliers: ~300,000

- Broad political footprint protects multi-year programs

US Defense Spending, F-35 Sales & $114B Backlog Highlight 2024–25 Landscape

US DoD remains primary buyer with FY2025 budget ~ $858B; F-35 procurement request ~$13.2B; FMS obligations ~$18.5B (2024); backlog $114.3B at end-2024; F-35 sustainment backlog $9.4B; 2024 sales $67.1B; US arms exports $220B (−12%); NATO spending $1.23T (2024).

| Metric | Value (Year) |

|---|---|

| DoD budget | $858B (FY2025) |

| Backlog | $114.3B (2024) |

What is included in the product

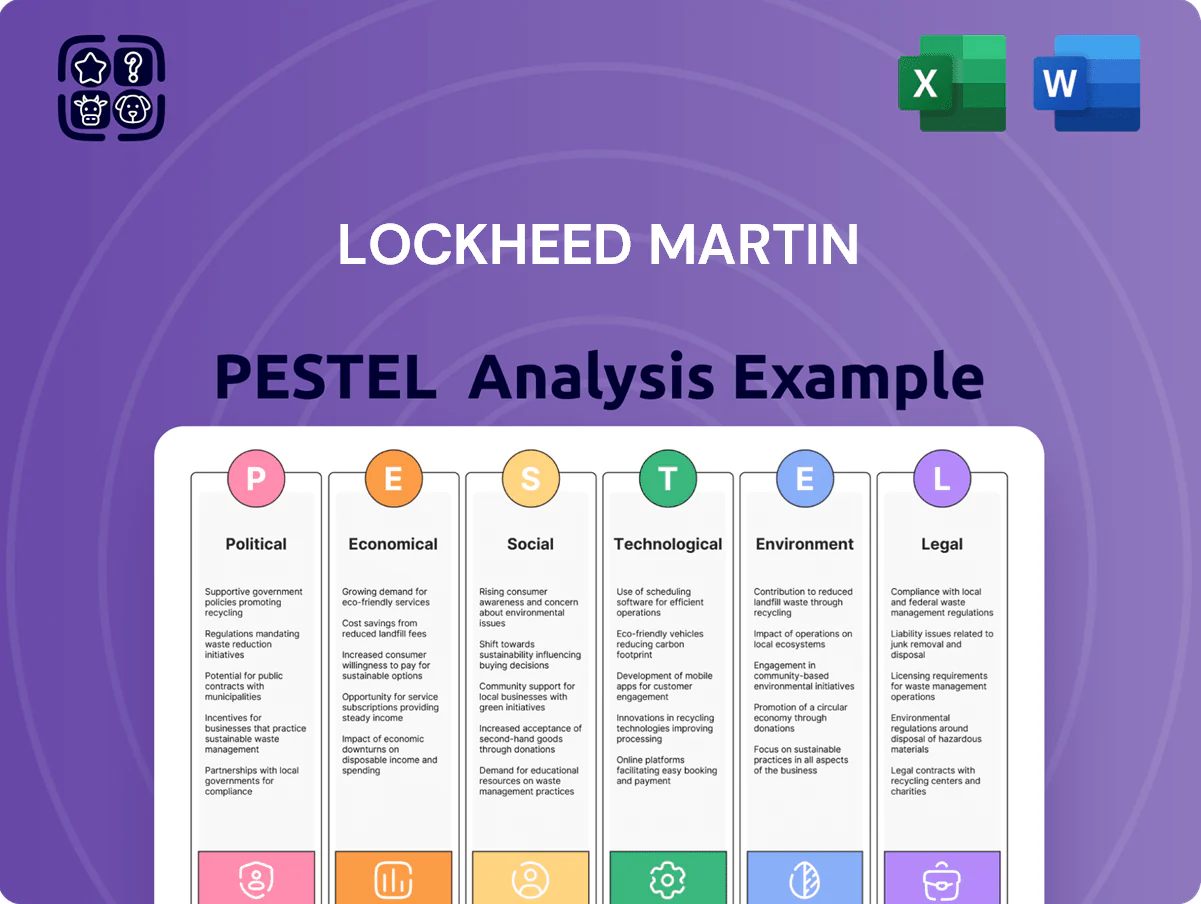

Explores how external macro-environmental factors uniquely affect Lockheed Martin across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE summary for Lockheed Martin that eases meeting prep and presentations by highlighting key political, economic, social, technological, legal, and environmental risks and opportunities in plain language for quick team alignment.

Economic factors

Impact of Inflation on Fixed-Price Contracts

Lockheed Martin faces margin compression on long-term fixed-price contracts signed during low-inflation periods as input costs rose: aluminum and titanium spiked 18–24% in 2022–24, and specialized labor costs rose ~12% cumulatively, squeezing 2024 aerospace margins by roughly 150–200 basis points.

Rising raw-material and labor costs can erode profitability unless mitigated by aggressive supply-chain optimization, hedging, and insertion of price-escalation clauses; Lockheed reported $1.5bn in supply-chain savings programs in 2024.

By end-2025 the company increasingly shifted toward cost-plus incentive contracts, with cost-plus mix rising to ~28% of new awards in 2025 versus 18% in 2022, reducing exposure to inflation-driven margin volatility.

Global Defense Market Expansion

The global defense market is in secular growth, projected at about 3.9% CAGR to reach roughly $2.3 trillion by 2026, as nations prioritize modernization over domestic spending. This tailwind enables Lockheed Martin to broaden revenues beyond the US—international sales rose to 19% of 2024 revenues—reducing single-buyer concentration. Strong demand for PAC-3 MSE and HIMARS boosts production, lowering unit costs via scale effects.

Supply Chain Stabilization and Cost Management

Following years of disruption, the aerospace supply chain reached a new equilibrium by 2025 with input costs ~12–18% above pre-pandemic levels; Lockheed Martin reports supply-chain-related cost headwinds but steady production rates. The company has invested over $500 million in digital transformation to improve visibility into tier‑2 and tier‑3 suppliers, reducing lead-time variability by an estimated 20%. Monitoring the economic health of small specialized vendors—who comprise ~40% of critical component suppliers—is essential to prevent bottlenecks and protect delivery schedules for complex systems.

Interest Rate Environment and Capital Allocation

The prevailing U.S. Fed funds rate at ~5.25–5.50% in 2024 raised Lockheed Martin’s blended cost of debt, pressuring free cash flow and prompting the company to moderate share repurchases while maintaining the 2024 dividend yield near 2.4% (2024 dividend ~$12.20/share annualized).

As a capital-intensive defense contractor, Lockheed balanced ~$2.5–3.0B annual R&D with shareholder returns, prioritizing programs with high IRR amid higher borrowing costs.

Management timed smaller defense-tech acquisitions toward late 2023–2024 when elevated rates compressed target valuations, keeping deal activity selective given higher cost of capital.

- Fed funds ~5.25–5.50% (2024)

- Dividend yield ~2.4%, annualized dividend ~$12.20 (2024)

- R&D spend ~$2.5–3.0B/year

- Selective M&A as higher rates compress valuations

Currency Exchange Volatility

Lockheed uses hedging and currency derivatives — 2024 disclosures show active FX risk management to limit P&L exposure from sudden devaluations in key export markets.

- ~20% revenue non-USD exposure

- USD up ~6% vs EUR in 2024

- Japan CPI 3.1% 2024 affects buyer budgets

- Active hedging recorded in 2024 filings

Inflation, input costs cut aerospace margins 150–200bps; cost‑plus 28%, intl 19%

Inflation and materials/labor cost rises trimmed 2024 aerospace margins ~150–200 bps; input costs remain ~12–18% above pre‑pandemic levels. Cost‑plus contracts rose to ~28% of new awards by 2025; international sales 19% of 2024 revenues; Fed funds ~5.25–5.50% (2024) raised blended debt cost; R&D ~$2.5–3.0B/year; non‑USD revenue ~20% (USD +6% vs EUR in 2024).

| Metric | 2024/2025 |

|---|---|

| Margin hit | 150–200 bps |

| Input cost delta | +12–18% |

| Cost‑plus mix | 28% |

| Intl sales | 19% |

| Fed funds | 5.25–5.50% |

| R&D | $2.5–3.0B |

| Non‑USD rev | ~20% |

Full Version Awaits

Lockheed Martin PESTLE Analysis

The preview shown here is the exact Lockheed Martin PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic advantage with our concise PESTLE snapshot for Lockheed Martin—spot how geopolitical shifts, defense budgets, tech innovation, and regulatory pressures converge on the company’s trajectory. Ideal for investors and strategists, this briefing highlights risks and opportunities you can act on immediately. Purchase the full PESTLE analysis for a complete, editable report packed with data-driven insights and tactical recommendations.

Political factors

US Defense Budget Allocations

The United States Department of Defense remains Lockheed Martin’s primary revenue source, with DoD budget growth to about $858 billion in FY2025 sustaining demand for advanced platforms amid modernized threats.

Analysts track the National Defense Authorization Act closely because it sets funding levels for the F-35 program—roughly $13.2 billion requested for procurement in FY2025—and for missile defense systems.

Congressional shifts toward Pacific deterrence have redirected capital into Aeronautics and Space, contributing to a 2024–2025 increase in segment backlog and program awards exceeding $20 billion.

Geopolitical Tensions in Eurasia and the Middle East

Persistent instability in Eastern Europe and the Middle East has driven allied demand for advanced weaponry and integrated air defense systems, boosting Lockheed Martin’s Foreign Military Sales; FMS obligations rose to about $18.5 billion in 2024, supporting a strong order flow. The firm’s backlog—$114.3 billion at end-2024—reflects robust demand for tactical missiles and rotary-wing platforms, with deliveries and contract awards expected to remain elevated through the mid-2020s.

NATO Defense Spending Commitments

NATO members' pledge to meet or exceed 2% of GDP on defense has expanded procurement; NATO defense spending reached about $1.23 trillion in 2024, up 4.2% year-on-year, boosting demand for US systems.

Lockheed Martin, as prime F-35 contractor, is central to European fleet upgrades—over 600 F-35s ordered by NATO allies through 2025—supporting interoperability with US forces.

These political commitments underpin multi-decade sustainment contracts; Lockheed reported $9.4 billion in F-35 program sustainment backlog at end-2024, creating predictable revenue streams.

Export Control and ITAR Regulations

Stringent US export controls and ITAR shape Lockheed Martin’s international expansion, limiting direct defense sales—US arms exports fell 12% to $220B in 2024, tightening licensing for platforms like F-35 and hypersonics.

Navigating technology-transfer politics is critical in the Indo-Pacific, where 2024 US security pacts (e.g., AUKUS/expanded ties) affect collaboration and offsets.

Shifts in bilateral agreements can open markets or restrict high-end system sales; hypersonic-related exports face added scrutiny and licensing hurdles.

- US arms exports: $220B in 2024, down 12%

Bipartisan Support for National Security

Despite political polarization, national security is a bipartisan consensus, providing stability for Lockheed Martin’s long-cycle programs; the company reported $67.1 billion in 2024 sales, much tied to multi-year defense contracts. Lockheed’s Washington lobbying and a supply chain spanning all 50 states—over 300,000 U.S. suppliers and suppliers’ economic impact cited in its 2024 reports—shield major programs from abrupt cancellations during political shifts.

- 2024 sales: $67.1B

- U.S. suppliers: ~300,000

- Broad political footprint protects multi-year programs

US Defense Spending, F-35 Sales & $114B Backlog Highlight 2024–25 Landscape

US DoD remains primary buyer with FY2025 budget ~ $858B; F-35 procurement request ~$13.2B; FMS obligations ~$18.5B (2024); backlog $114.3B at end-2024; F-35 sustainment backlog $9.4B; 2024 sales $67.1B; US arms exports $220B (−12%); NATO spending $1.23T (2024).

| Metric | Value (Year) |

|---|---|

| DoD budget | $858B (FY2025) |

| Backlog | $114.3B (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Lockheed Martin across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE summary for Lockheed Martin that eases meeting prep and presentations by highlighting key political, economic, social, technological, legal, and environmental risks and opportunities in plain language for quick team alignment.

Economic factors

Impact of Inflation on Fixed-Price Contracts

Lockheed Martin faces margin compression on long-term fixed-price contracts signed during low-inflation periods as input costs rose: aluminum and titanium spiked 18–24% in 2022–24, and specialized labor costs rose ~12% cumulatively, squeezing 2024 aerospace margins by roughly 150–200 basis points.

Rising raw-material and labor costs can erode profitability unless mitigated by aggressive supply-chain optimization, hedging, and insertion of price-escalation clauses; Lockheed reported $1.5bn in supply-chain savings programs in 2024.

By end-2025 the company increasingly shifted toward cost-plus incentive contracts, with cost-plus mix rising to ~28% of new awards in 2025 versus 18% in 2022, reducing exposure to inflation-driven margin volatility.

Global Defense Market Expansion

The global defense market is in secular growth, projected at about 3.9% CAGR to reach roughly $2.3 trillion by 2026, as nations prioritize modernization over domestic spending. This tailwind enables Lockheed Martin to broaden revenues beyond the US—international sales rose to 19% of 2024 revenues—reducing single-buyer concentration. Strong demand for PAC-3 MSE and HIMARS boosts production, lowering unit costs via scale effects.

Supply Chain Stabilization and Cost Management

Following years of disruption, the aerospace supply chain reached a new equilibrium by 2025 with input costs ~12–18% above pre-pandemic levels; Lockheed Martin reports supply-chain-related cost headwinds but steady production rates. The company has invested over $500 million in digital transformation to improve visibility into tier‑2 and tier‑3 suppliers, reducing lead-time variability by an estimated 20%. Monitoring the economic health of small specialized vendors—who comprise ~40% of critical component suppliers—is essential to prevent bottlenecks and protect delivery schedules for complex systems.

Interest Rate Environment and Capital Allocation

The prevailing U.S. Fed funds rate at ~5.25–5.50% in 2024 raised Lockheed Martin’s blended cost of debt, pressuring free cash flow and prompting the company to moderate share repurchases while maintaining the 2024 dividend yield near 2.4% (2024 dividend ~$12.20/share annualized).

As a capital-intensive defense contractor, Lockheed balanced ~$2.5–3.0B annual R&D with shareholder returns, prioritizing programs with high IRR amid higher borrowing costs.

Management timed smaller defense-tech acquisitions toward late 2023–2024 when elevated rates compressed target valuations, keeping deal activity selective given higher cost of capital.

- Fed funds ~5.25–5.50% (2024)

- Dividend yield ~2.4%, annualized dividend ~$12.20 (2024)

- R&D spend ~$2.5–3.0B/year

- Selective M&A as higher rates compress valuations

Currency Exchange Volatility

Lockheed uses hedging and currency derivatives — 2024 disclosures show active FX risk management to limit P&L exposure from sudden devaluations in key export markets.

- ~20% revenue non-USD exposure

- USD up ~6% vs EUR in 2024

- Japan CPI 3.1% 2024 affects buyer budgets

- Active hedging recorded in 2024 filings

Inflation, input costs cut aerospace margins 150–200bps; cost‑plus 28%, intl 19%

Inflation and materials/labor cost rises trimmed 2024 aerospace margins ~150–200 bps; input costs remain ~12–18% above pre‑pandemic levels. Cost‑plus contracts rose to ~28% of new awards by 2025; international sales 19% of 2024 revenues; Fed funds ~5.25–5.50% (2024) raised blended debt cost; R&D ~$2.5–3.0B/year; non‑USD revenue ~20% (USD +6% vs EUR in 2024).

| Metric | 2024/2025 |

|---|---|

| Margin hit | 150–200 bps |

| Input cost delta | +12–18% |

| Cost‑plus mix | 28% |

| Intl sales | 19% |

| Fed funds | 5.25–5.50% |

| R&D | $2.5–3.0B |

| Non‑USD rev | ~20% |

Full Version Awaits

Lockheed Martin PESTLE Analysis

The preview shown here is the exact Lockheed Martin PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.