Loews Porter's Five Forces Analysis

Don't Miss the Bigger Picture

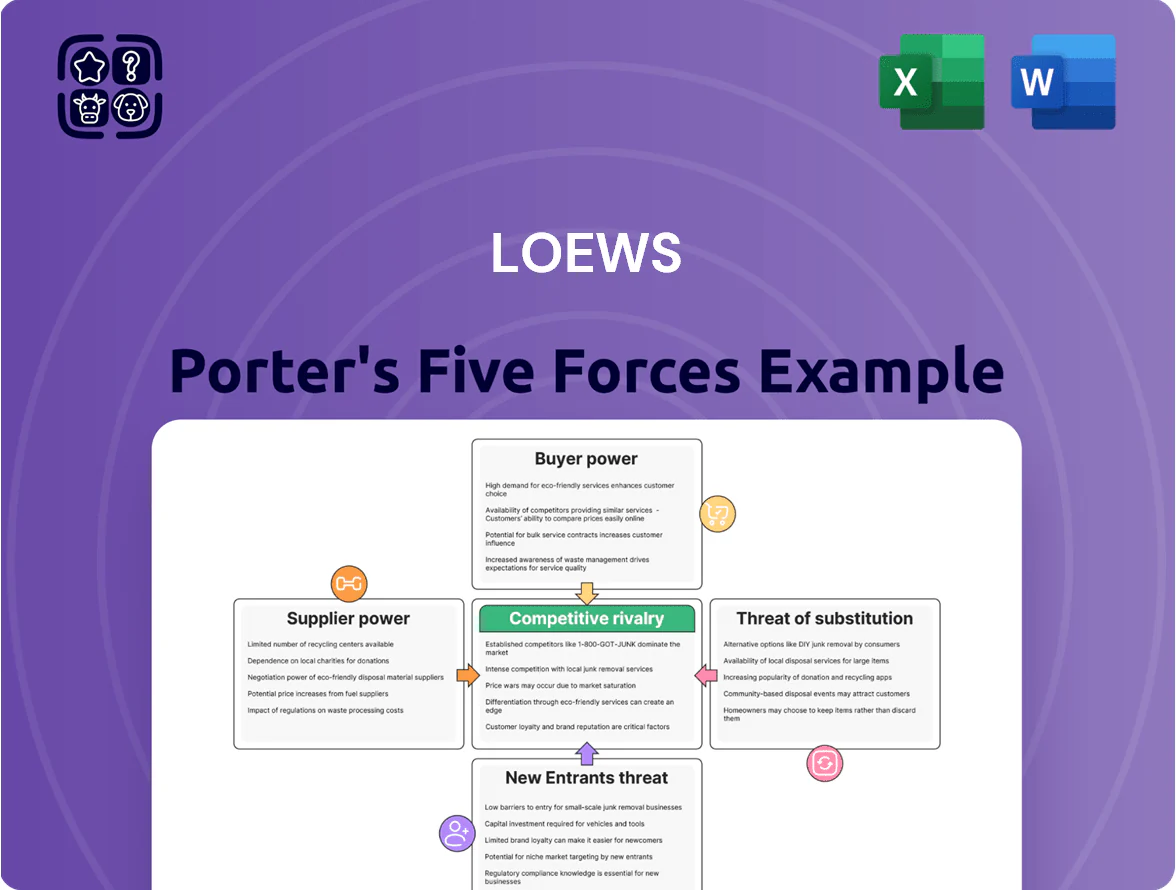

Loews faces mixed industry forces—diverse supplier relationships, moderate buyer power across its insurance and hospitality segments, and manageable threats from substitutes and new entrants thanks to scale and brand strength.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Loews’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reinsurance market concentration

Reinsurance availability is critical for CNA Financial (Loews subsidiary) to manage risk and capital efficiency; global reinsurers control about 60–70% of excess capacity, giving them leverage at renewals after big-cat loss years like 2023–2024 when global catastrophe insured losses hit ~$150bn (Swiss Re, 2024).

If reinsurance rates spike or capacity falls, Loews faces higher ceded costs or must cut underwriting volume—CNA ceded ~20% of net written premium in 2024, so a 25% reinsurance rate rise would raise loss-adjusted expenses materially.

Energy infrastructure labor and materials

Boardwalk Pipelines relies on a small set of specialized engineering firms and high-grade steel makers for pipeline builds and upkeep, giving suppliers moderate-to-high bargaining power; only ~10–15 global mills meet API 5L high-strength specs.

Global steel spot prices rose ~18% in 2024 and skilled pipeline welders command 20–30% wage premiums, so steel shocks or labor shortages can raise energy-capex by double-digit percentages on projects.

Hospitality labor and service vendors

Loews Hotels needs steady skilled staff and premium F&B vendors to keep its luxury positioning; US hotel wage growth ran 5.8% year-over-year in 2024, pushing payroll share above 30% of operating costs for upscale properties. Tight 2024 labor markets raised bargaining power for workers, driving higher wages and turnover costs; reliance on specialized vendors (spa, linens, artisanal F&B) adds markup pressure—vendor services can add 6–12% to per-room variable costs, hard to cut without hurting guest experience.

Technology and distribution platforms

Loews faces high supplier power as hotels and CNA depend on major tech and distribution platforms: OTAs and global distribution systems control roughly 60–70% of digital bookings for large chains, driving commission rates and visibility, while CNA uses complex underwriting and analytics stacks with switching costs often exceeding millions and multi-year vendor lock-in.

- OTAs/GDS: 60–70% digital booking share

- Commissions: 15–25% common on OTA bookings

- Switching costs: vendor contracts often $1M+

- Analytics dependence: improved loss prediction by 10–20%

Regulatory and compliance consultants

As a diversified holding, Loews faces complex rules across insurance, energy, and hospitality, so specialized regulatory and compliance consultants wield strong bargaining power because their expertise secures licenses and meets EPA and state requirements.

Non-compliance costs are high—fines, license loss, and remediation can exceed tens to hundreds of millions (Berkshire Energy cases show >$100M remediations), making these firms indispensable to Loews’ risk strategy and budgeting.

- Essential expertise: licensing, EPA, state insurance regulators

- High stakes: potential fines/remediation >$100M

- Limited suppliers: niche legal/compliance boutiques

- Costs passed to Loews: increases operating risk and expense

Supplier Concentration: Reinsurers, Steel, OTAs & Compliance Squeeze Margins

Suppliers exert material power across Loews: reinsurers (60–70% excess capacity; ~$150bn nat-cat losses 2023–24) can raise rates—CNA ceded ~20% premium in 2024; specialized steel mills (~10–15 meeting API 5L) and welders pushed pipeline capex +18% steel, 20–30% wage premiums; OTAs/GDS control 60–70% digital bookings with 15–25% commissions; niche compliance firms vital given >$100M remediation risks.

| Supplier | Key stat | Impact |

|---|---|---|

| Reinsurers | 60–70% capacity; ~$150bn losses | Higher rates; CNA ceded ~20% |

| Steel/welders | 10–15 mills; +18% price; 20–30% wages | Capex up double digits |

| OTAs/GDS | 60–70% bookings; 15–25% commissions | Margin pressure |

| Compliance firms | Remediations >$100M | Indispensable, costly |

What is included in the product

Provides a Loews-specific Porter's Five Forces overview that uncovers competitive drivers, supplier and buyer power, barriers to entry, substitutes, and disruptive threats—delivering industry-backed insights to inform strategy and investor materials.

Concise Porter's Five Forces summary for Loews—translate complex competitive pressures into a single, decision-ready sheet to speed strategic choices.

Customers Bargaining Power

Insurance broker influence

Energy producer contract negotiations

Boardwalk Pipelines serves large gas producers and utilities that demand long-term, fixed-rate transport; in 2024 top shippers accounted for about 60% of firm capacity, giving them scale to press for lower tariffs and priority scheduling.

Corporate travel procurement power

Loews Hotels depends on corporate accounts and group bookings for many luxury sites; in 2024 corporate segment made ~42% of RevPAR at comparable properties, letting firms demand steep discounts and flexible cancellation windows.

Large corporations and associations booking thousands of room nights annually secure rates often 15–30% below retail and lenient terms, pressuring Loews’ average daily rate (ADR) and GOP margins.

During 2023–2024 economic slowdowns corporate booking volumes fell ~12%, compressing margins as negotiated rates stayed low while fixed hotel costs remained.

Retail consumer price sensitivity

Individual luxury travelers show high price sensitivity and low switching costs because online platforms let them compare rates and reviews instantly; TripAdvisor and OTA price parity engines mean 70% of US luxury bookings in 2024 checked at least three sites before purchase.

This transparency forces Loews to compete on clear service differentiation and loyalty perks; without it, raising ADR (average daily rate) above the 2024 US luxury segment median of $465 risks lost bookings.

- High expectations + low switching costs

- 70% check 3+ sites (2024)

- 2024 US luxury median ADR $465

- Must use clear differentiation or loyalty to hold price

Policyholder retention in commercial lines

Sophisticated commercial policyholders can shift to captives, parametric covers, or self-insure; industry surveys show 22% of large commercial buyers considered alternatives in 2024, keeping insurers like CNA under pressure.

If CNA raises premiums above perceived value, firms reduce limits or exit—commercial churn rose to 7.8% in 2024 for standard risks, so client bargaining power remains high.

- 22% large buyers eyed alternatives (2024)

- 7.8% commercial churn (2024)

- High price sensitivity for standard risks

Buyers Hold Leverage: Top clients drive discounts, higher churn squeeze Loews margins

| Metric | Value (2024) |

|---|---|

| CNA via top 10 brokers | ~40% |

| Boardwalk top shippers | ~60% |

| Loews Hotels corporate RevPAR | ~42% |

| US luxury median ADR | $465 |

| Large buyers eyed alternatives | 22% |

| Commercial churn | 7.8% |

Same Document Delivered

Loews Porter's Five Forces Analysis

This preview shows the exact Loews Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, placeholders, or mockups.

The document displayed is the complete, professionally formatted file ready for download and use the moment you buy.

You're looking at the final deliverable: a thorough, ready-to-use analysis of Loews' competitive forces available instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Loews faces mixed industry forces—diverse supplier relationships, moderate buyer power across its insurance and hospitality segments, and manageable threats from substitutes and new entrants thanks to scale and brand strength.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Loews’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reinsurance market concentration

Reinsurance availability is critical for CNA Financial (Loews subsidiary) to manage risk and capital efficiency; global reinsurers control about 60–70% of excess capacity, giving them leverage at renewals after big-cat loss years like 2023–2024 when global catastrophe insured losses hit ~$150bn (Swiss Re, 2024).

If reinsurance rates spike or capacity falls, Loews faces higher ceded costs or must cut underwriting volume—CNA ceded ~20% of net written premium in 2024, so a 25% reinsurance rate rise would raise loss-adjusted expenses materially.

Energy infrastructure labor and materials

Boardwalk Pipelines relies on a small set of specialized engineering firms and high-grade steel makers for pipeline builds and upkeep, giving suppliers moderate-to-high bargaining power; only ~10–15 global mills meet API 5L high-strength specs.

Global steel spot prices rose ~18% in 2024 and skilled pipeline welders command 20–30% wage premiums, so steel shocks or labor shortages can raise energy-capex by double-digit percentages on projects.

Hospitality labor and service vendors

Loews Hotels needs steady skilled staff and premium F&B vendors to keep its luxury positioning; US hotel wage growth ran 5.8% year-over-year in 2024, pushing payroll share above 30% of operating costs for upscale properties. Tight 2024 labor markets raised bargaining power for workers, driving higher wages and turnover costs; reliance on specialized vendors (spa, linens, artisanal F&B) adds markup pressure—vendor services can add 6–12% to per-room variable costs, hard to cut without hurting guest experience.

Technology and distribution platforms

Loews faces high supplier power as hotels and CNA depend on major tech and distribution platforms: OTAs and global distribution systems control roughly 60–70% of digital bookings for large chains, driving commission rates and visibility, while CNA uses complex underwriting and analytics stacks with switching costs often exceeding millions and multi-year vendor lock-in.

- OTAs/GDS: 60–70% digital booking share

- Commissions: 15–25% common on OTA bookings

- Switching costs: vendor contracts often $1M+

- Analytics dependence: improved loss prediction by 10–20%

Regulatory and compliance consultants

As a diversified holding, Loews faces complex rules across insurance, energy, and hospitality, so specialized regulatory and compliance consultants wield strong bargaining power because their expertise secures licenses and meets EPA and state requirements.

Non-compliance costs are high—fines, license loss, and remediation can exceed tens to hundreds of millions (Berkshire Energy cases show >$100M remediations), making these firms indispensable to Loews’ risk strategy and budgeting.

- Essential expertise: licensing, EPA, state insurance regulators

- High stakes: potential fines/remediation >$100M

- Limited suppliers: niche legal/compliance boutiques

- Costs passed to Loews: increases operating risk and expense

Supplier Concentration: Reinsurers, Steel, OTAs & Compliance Squeeze Margins

Suppliers exert material power across Loews: reinsurers (60–70% excess capacity; ~$150bn nat-cat losses 2023–24) can raise rates—CNA ceded ~20% premium in 2024; specialized steel mills (~10–15 meeting API 5L) and welders pushed pipeline capex +18% steel, 20–30% wage premiums; OTAs/GDS control 60–70% digital bookings with 15–25% commissions; niche compliance firms vital given >$100M remediation risks.

| Supplier | Key stat | Impact |

|---|---|---|

| Reinsurers | 60–70% capacity; ~$150bn losses | Higher rates; CNA ceded ~20% |

| Steel/welders | 10–15 mills; +18% price; 20–30% wages | Capex up double digits |

| OTAs/GDS | 60–70% bookings; 15–25% commissions | Margin pressure |

| Compliance firms | Remediations >$100M | Indispensable, costly |

What is included in the product

Provides a Loews-specific Porter's Five Forces overview that uncovers competitive drivers, supplier and buyer power, barriers to entry, substitutes, and disruptive threats—delivering industry-backed insights to inform strategy and investor materials.

Concise Porter's Five Forces summary for Loews—translate complex competitive pressures into a single, decision-ready sheet to speed strategic choices.

Customers Bargaining Power

Insurance broker influence

Energy producer contract negotiations

Boardwalk Pipelines serves large gas producers and utilities that demand long-term, fixed-rate transport; in 2024 top shippers accounted for about 60% of firm capacity, giving them scale to press for lower tariffs and priority scheduling.

Corporate travel procurement power

Loews Hotels depends on corporate accounts and group bookings for many luxury sites; in 2024 corporate segment made ~42% of RevPAR at comparable properties, letting firms demand steep discounts and flexible cancellation windows.

Large corporations and associations booking thousands of room nights annually secure rates often 15–30% below retail and lenient terms, pressuring Loews’ average daily rate (ADR) and GOP margins.

During 2023–2024 economic slowdowns corporate booking volumes fell ~12%, compressing margins as negotiated rates stayed low while fixed hotel costs remained.

Retail consumer price sensitivity

Individual luxury travelers show high price sensitivity and low switching costs because online platforms let them compare rates and reviews instantly; TripAdvisor and OTA price parity engines mean 70% of US luxury bookings in 2024 checked at least three sites before purchase.

This transparency forces Loews to compete on clear service differentiation and loyalty perks; without it, raising ADR (average daily rate) above the 2024 US luxury segment median of $465 risks lost bookings.

- High expectations + low switching costs

- 70% check 3+ sites (2024)

- 2024 US luxury median ADR $465

- Must use clear differentiation or loyalty to hold price

Policyholder retention in commercial lines

Sophisticated commercial policyholders can shift to captives, parametric covers, or self-insure; industry surveys show 22% of large commercial buyers considered alternatives in 2024, keeping insurers like CNA under pressure.

If CNA raises premiums above perceived value, firms reduce limits or exit—commercial churn rose to 7.8% in 2024 for standard risks, so client bargaining power remains high.

- 22% large buyers eyed alternatives (2024)

- 7.8% commercial churn (2024)

- High price sensitivity for standard risks

Buyers Hold Leverage: Top clients drive discounts, higher churn squeeze Loews margins

| Metric | Value (2024) |

|---|---|

| CNA via top 10 brokers | ~40% |

| Boardwalk top shippers | ~60% |

| Loews Hotels corporate RevPAR | ~42% |

| US luxury median ADR | $465 |

| Large buyers eyed alternatives | 22% |

| Commercial churn | 7.8% |

Same Document Delivered

Loews Porter's Five Forces Analysis

This preview shows the exact Loews Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, placeholders, or mockups.

The document displayed is the complete, professionally formatted file ready for download and use the moment you buy.

You're looking at the final deliverable: a thorough, ready-to-use analysis of Loews' competitive forces available instantly after payment.