Loews PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock how political shifts, economic cycles, and technological change are shaping Loews’s strategic outlook with our concise PESTLE snapshot—tailored for investors and strategists who need clarity fast. Purchase the full PESTLE analysis to access an expert, fully editable report with deep-dive insights, risk scenarios, and actionable recommendations you can use immediately.

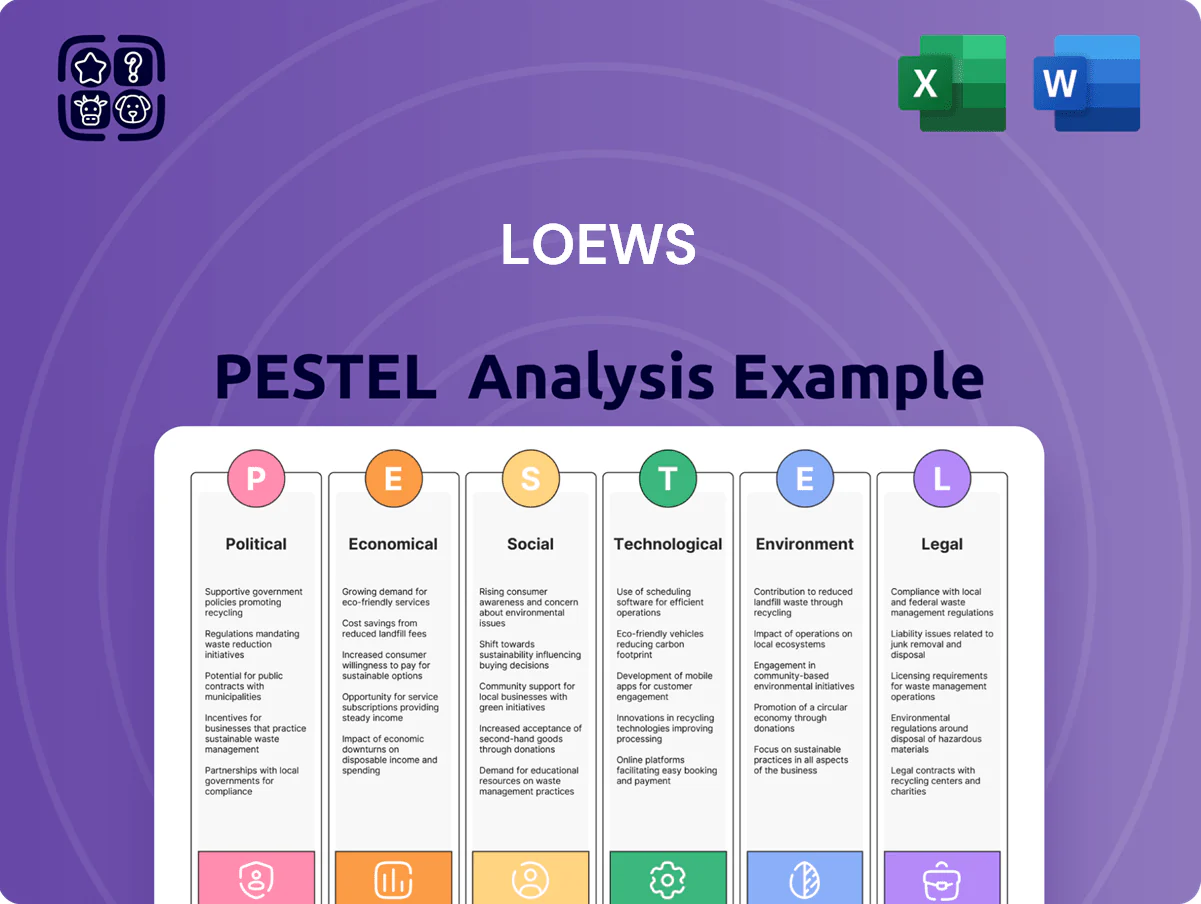

Political factors

Federal Energy Policy Shifts

The regulatory environment for Boardwalk Pipelines is shaped by federal energy priorities; under the Biden administration since 2021, FERC permit scrutiny and methane rules tightened, with EPA proposing 87% reduction-target leak standards in 2023 affecting operations.

Shifts in pipeline permit policy and methane controls alter project timelines and capital costs—estimated capex increases of 5–12% for new midstream builds per industry analyses in 2024.

Executives must monitor executive orders and federal guidance, as changes could reduce utilization of fossil fuel transport assets over the 10–20 year horizon and affect asset valuations.

Corporate Tax Environment

Loews, a diversified holding company, is highly sensitive to federal corporate tax rate and capital gains changes; a 1 percentage-point federal rate shift alters after-tax earnings for subsidiaries such as CNA Financial, which reported $1.9 billion pre-tax income in 2024. As of late 2025, proposed federal tax adjustments and capital gains treatment debates could materially change Loews’ consolidated net income and cash available for dividends and share repurchases. Investors track tax-policy risks to assess buyback/dividend capacity, noting Loews returned $500 million in dividends and repurchases in 2024.

Insurance Regulatory Oversight

CNA Financial faces stringent state-level regulation that enforces risk-based capital ratios; as of year-end 2024 CNA reported a consolidated risk-based capital ratio above 300%, reflecting regulatory capital adequacy while limiting pricing flexibility.

Political pressure on insurance commissioners has constrained rate increases in states like New York and California, where regulators approved single-digit rate hikes in 2023–2024 despite rising loss costs.

Consequently Loews must keep CNA’s portfolio geographically diversified—CNA wrote premiums across all 50 states in 2024—to dilute localized regulatory restrictions and protect underwriting margins.

Geopolitical Impact on Energy Markets

Global political instability—Russia-Ukraine war and Middle East tensions—keeps demand for US domestic energy high; US natural gas production averaged ~98 Bcf/d in 2024, supporting export growth.

Boardwalk Pipelines benefits from US policy backing LNG exports (US LNG capacity ~16.4 BTPA in 2024) and infrastructure spending, boosting throughput and tariff revenues.

Trade tensions and tariffs raised 2024 pipeline equipment costs ~5–8%, risking project delays and increasing market volatility for energy prices.

- US gas production ~98 Bcf/d (2024)

- US LNG capacity ~16.4 BTPA (2024)

- Pipeline equipment cost rise 5–8% (2024)

Trade Policy and Material Costs

Tariffs and trade agreements directly affect Loews’ material costs: U.S. steel tariffs raised import prices by about 25% in 2018–2024 cycles, contributing to a 6–8% rise in construction capex per project; aluminum volatility added another 2–4%. Political moves on Section 232 and USMCA adjustments force Loews Hotels & Co. to model 5–10% contingency in new development budgets and delay some projects.

- Tariff-driven steel/aluminum price increases: +6–12% impact on capex

- Required contingency in project budgets: 5–10%

- Policy risk: delays via import restrictions and supply-chain shifts

Loews faces political risk as energy, costs, and strong CNA capital shape 2024 outlook

Political risks affect Loews via energy regulation, tax policy, insurance oversight, trade tariffs, and geopolitical-driven demand; 2024 figures: US gas prod ~98 Bcf/d, LNG capacity ~16.4 BTPA, pipeline equipment costs +5–8%, Loews buybacks/dividends ~$500M, CNA RBC >300%.

| Factor | 2024 Metric |

|---|---|

| US gas prod | 98 Bcf/d |

| LNG capacity | 16.4 BTPA |

| Equip. cost rise | +5–8% |

| Loews returns | $500M |

| CNA RBC | >300% |

What is included in the product

Explores how macro-environmental factors uniquely affect Loews across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific insights to identify threats and opportunities for executives, consultants, and investors.

Condenses Loews' full PESTLE into a clean, shareable summary that’s visually segmented by category for quick interpretation during meetings and easily dropped into presentations or planning packs.

Economic factors

Interest Rate Cycle Management

As of late 2025, a higher interest rate regime—US 10-year at ~4.5% and Fed funds near 5.25%—boosts CNA Financial’s ability to reinvest premium float into yields, improving investment income and helping Loews’ consolidated ROE; CNA’s investment yield rose toward ~3.8–4.2% in 2024–25. Rapid rate swings, however, can mark-to-market fixed-income losses (duration exposure) and raise Loews’ borrowing costs, tightening capital deployment.

Inflationary Pressure on Claims

Persistent inflation raises claim severity for property & casualty lines as repair, medical and material costs climb; U.S. CPI was 3.4% year-over-year in Jan 2026, and construction material costs rose ~6% in 2024–25, increasing Loews-owned CNA’s loss severity exposure.

CNA must tighten pricing and underwriting to reflect social inflation—U.S. liability jury awards grew ~9% CAGR 2018–2023—and elevated input costs to avoid margin compression.

Failure to anticipate these trends can force reserve strengthening; U.S. P&C insurers took roughly $4–6 billion of reserve increases industry-wide in 2024, risking lower underwriting income for Loews’ insurance segment.

Hospitality Demand and Discretionary Spending

Loews Hotels and Co is highly cyclical, reliant on corporate travel budgets and consumer discretionary income; US GDP growth easing to ~1.5% in 2025 would pressure occupancy and ADRs. Hospitality revenue represented about 62% of Loews consolidated revenue in 2024, so a 100–200 bps drop in REVPAR could materially hit margins. Cooling economic conditions typically reduce group bookings and luxury stays, lowering segment EBITDA contribution. Recent STR data showed US luxury segment occupancy down ~2.3% year-over-year through 2025 Q1.

Capital Market Volatility

As a value-oriented holding company, Loews depends on stable capital markets to pursue opportunistic share buybacks and acquisitions; 2024 equity market volatility (VIX avg ~20–22) can raise buyback costs and compress deal activity, obscuring the sum-of-the-parts valuation of subsidiaries like CNA Financial and Boardwalk.

High volatility makes it harder for markets to price intrinsic asset value, so Loews maintains strong liquidity—$4.6 billion in cash and equivalents at year-end 2024—to weather uncertainty and preserve acquisition flexibility.

- VIX (2024 avg): ~20–22

- Loews cash & equivalents (2024 YE): $4.6B

- Strategy: prioritize liquidity to enable buybacks/acquisitions amid market swings

Labor Market Dynamics

The hospitality and packaging sectors in Loews’ portfolio confront wage growth and labor shortages; US leisure and hospitality job openings were 1.1 million in Dec 2025 while average hourly earnings rose 4.2% YoY in 2025, pressuring margins.

Competition for service workers forces higher pay and benefits, requiring productivity gains or pricing power to protect operating margins; Loews must retain luxury standards while managing labor cost inflation.

- 1.1M leisure/hospitality openings (Dec 2025)

- Average hourly earnings +4.2% YoY (2025)

- Higher compensation risks margin compression

- Retention essential to preserve luxury service levels

Higher rates boost yields but fuel P&C claims and squeeze hospitality margins

Higher rates (US 10‑yr ~4.5%, fed funds ~5.25% in 2025) lift CNA investment yields (~3.8–4.2% 2024–25) but increase mark‑to‑market risk and funding costs; inflation (CPI ~3.4% Jan 2026) and rising materials (+~6% 2024–25) boost P&C claim severity; hospitality REVPAR/occupancy pressured by slower GDP (~1.5% 2025) and labor costs (avg hourly earnings +4.2% 2025).

| Metric | Value |

|---|---|

| US 10‑yr (2025) | ~4.5% |

| Fed funds (2025) | ~5.25% |

| CNA yield | 3.8–4.2% |

| CPI (Jan 2026) | 3.4% YoY |

| Materials cost (2024–25) | +~6% |

| GDP growth (2025) | ~1.5% |

| Avg hourly earnings (2025) | +4.2% YoY |

Full Version Awaits

Loews PESTLE Analysis

The preview shown here is the exact Loews PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This file is the final version, with complete content and professional structure, not a teaser or placeholder. After checkout you’ll instantly download the same document visible in the preview, containing the same layout, analysis, and conclusions. What you see is what you’ll own and can apply immediately.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock how political shifts, economic cycles, and technological change are shaping Loews’s strategic outlook with our concise PESTLE snapshot—tailored for investors and strategists who need clarity fast. Purchase the full PESTLE analysis to access an expert, fully editable report with deep-dive insights, risk scenarios, and actionable recommendations you can use immediately.

Political factors

Federal Energy Policy Shifts

The regulatory environment for Boardwalk Pipelines is shaped by federal energy priorities; under the Biden administration since 2021, FERC permit scrutiny and methane rules tightened, with EPA proposing 87% reduction-target leak standards in 2023 affecting operations.

Shifts in pipeline permit policy and methane controls alter project timelines and capital costs—estimated capex increases of 5–12% for new midstream builds per industry analyses in 2024.

Executives must monitor executive orders and federal guidance, as changes could reduce utilization of fossil fuel transport assets over the 10–20 year horizon and affect asset valuations.

Corporate Tax Environment

Loews, a diversified holding company, is highly sensitive to federal corporate tax rate and capital gains changes; a 1 percentage-point federal rate shift alters after-tax earnings for subsidiaries such as CNA Financial, which reported $1.9 billion pre-tax income in 2024. As of late 2025, proposed federal tax adjustments and capital gains treatment debates could materially change Loews’ consolidated net income and cash available for dividends and share repurchases. Investors track tax-policy risks to assess buyback/dividend capacity, noting Loews returned $500 million in dividends and repurchases in 2024.

Insurance Regulatory Oversight

CNA Financial faces stringent state-level regulation that enforces risk-based capital ratios; as of year-end 2024 CNA reported a consolidated risk-based capital ratio above 300%, reflecting regulatory capital adequacy while limiting pricing flexibility.

Political pressure on insurance commissioners has constrained rate increases in states like New York and California, where regulators approved single-digit rate hikes in 2023–2024 despite rising loss costs.

Consequently Loews must keep CNA’s portfolio geographically diversified—CNA wrote premiums across all 50 states in 2024—to dilute localized regulatory restrictions and protect underwriting margins.

Geopolitical Impact on Energy Markets

Global political instability—Russia-Ukraine war and Middle East tensions—keeps demand for US domestic energy high; US natural gas production averaged ~98 Bcf/d in 2024, supporting export growth.

Boardwalk Pipelines benefits from US policy backing LNG exports (US LNG capacity ~16.4 BTPA in 2024) and infrastructure spending, boosting throughput and tariff revenues.

Trade tensions and tariffs raised 2024 pipeline equipment costs ~5–8%, risking project delays and increasing market volatility for energy prices.

- US gas production ~98 Bcf/d (2024)

- US LNG capacity ~16.4 BTPA (2024)

- Pipeline equipment cost rise 5–8% (2024)

Trade Policy and Material Costs

Tariffs and trade agreements directly affect Loews’ material costs: U.S. steel tariffs raised import prices by about 25% in 2018–2024 cycles, contributing to a 6–8% rise in construction capex per project; aluminum volatility added another 2–4%. Political moves on Section 232 and USMCA adjustments force Loews Hotels & Co. to model 5–10% contingency in new development budgets and delay some projects.

- Tariff-driven steel/aluminum price increases: +6–12% impact on capex

- Required contingency in project budgets: 5–10%

- Policy risk: delays via import restrictions and supply-chain shifts

Loews faces political risk as energy, costs, and strong CNA capital shape 2024 outlook

Political risks affect Loews via energy regulation, tax policy, insurance oversight, trade tariffs, and geopolitical-driven demand; 2024 figures: US gas prod ~98 Bcf/d, LNG capacity ~16.4 BTPA, pipeline equipment costs +5–8%, Loews buybacks/dividends ~$500M, CNA RBC >300%.

| Factor | 2024 Metric |

|---|---|

| US gas prod | 98 Bcf/d |

| LNG capacity | 16.4 BTPA |

| Equip. cost rise | +5–8% |

| Loews returns | $500M |

| CNA RBC | >300% |

What is included in the product

Explores how macro-environmental factors uniquely affect Loews across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific insights to identify threats and opportunities for executives, consultants, and investors.

Condenses Loews' full PESTLE into a clean, shareable summary that’s visually segmented by category for quick interpretation during meetings and easily dropped into presentations or planning packs.

Economic factors

Interest Rate Cycle Management

As of late 2025, a higher interest rate regime—US 10-year at ~4.5% and Fed funds near 5.25%—boosts CNA Financial’s ability to reinvest premium float into yields, improving investment income and helping Loews’ consolidated ROE; CNA’s investment yield rose toward ~3.8–4.2% in 2024–25. Rapid rate swings, however, can mark-to-market fixed-income losses (duration exposure) and raise Loews’ borrowing costs, tightening capital deployment.

Inflationary Pressure on Claims

Persistent inflation raises claim severity for property & casualty lines as repair, medical and material costs climb; U.S. CPI was 3.4% year-over-year in Jan 2026, and construction material costs rose ~6% in 2024–25, increasing Loews-owned CNA’s loss severity exposure.

CNA must tighten pricing and underwriting to reflect social inflation—U.S. liability jury awards grew ~9% CAGR 2018–2023—and elevated input costs to avoid margin compression.

Failure to anticipate these trends can force reserve strengthening; U.S. P&C insurers took roughly $4–6 billion of reserve increases industry-wide in 2024, risking lower underwriting income for Loews’ insurance segment.

Hospitality Demand and Discretionary Spending

Loews Hotels and Co is highly cyclical, reliant on corporate travel budgets and consumer discretionary income; US GDP growth easing to ~1.5% in 2025 would pressure occupancy and ADRs. Hospitality revenue represented about 62% of Loews consolidated revenue in 2024, so a 100–200 bps drop in REVPAR could materially hit margins. Cooling economic conditions typically reduce group bookings and luxury stays, lowering segment EBITDA contribution. Recent STR data showed US luxury segment occupancy down ~2.3% year-over-year through 2025 Q1.

Capital Market Volatility

As a value-oriented holding company, Loews depends on stable capital markets to pursue opportunistic share buybacks and acquisitions; 2024 equity market volatility (VIX avg ~20–22) can raise buyback costs and compress deal activity, obscuring the sum-of-the-parts valuation of subsidiaries like CNA Financial and Boardwalk.

High volatility makes it harder for markets to price intrinsic asset value, so Loews maintains strong liquidity—$4.6 billion in cash and equivalents at year-end 2024—to weather uncertainty and preserve acquisition flexibility.

- VIX (2024 avg): ~20–22

- Loews cash & equivalents (2024 YE): $4.6B

- Strategy: prioritize liquidity to enable buybacks/acquisitions amid market swings

Labor Market Dynamics

The hospitality and packaging sectors in Loews’ portfolio confront wage growth and labor shortages; US leisure and hospitality job openings were 1.1 million in Dec 2025 while average hourly earnings rose 4.2% YoY in 2025, pressuring margins.

Competition for service workers forces higher pay and benefits, requiring productivity gains or pricing power to protect operating margins; Loews must retain luxury standards while managing labor cost inflation.

- 1.1M leisure/hospitality openings (Dec 2025)

- Average hourly earnings +4.2% YoY (2025)

- Higher compensation risks margin compression

- Retention essential to preserve luxury service levels

Higher rates boost yields but fuel P&C claims and squeeze hospitality margins

Higher rates (US 10‑yr ~4.5%, fed funds ~5.25% in 2025) lift CNA investment yields (~3.8–4.2% 2024–25) but increase mark‑to‑market risk and funding costs; inflation (CPI ~3.4% Jan 2026) and rising materials (+~6% 2024–25) boost P&C claim severity; hospitality REVPAR/occupancy pressured by slower GDP (~1.5% 2025) and labor costs (avg hourly earnings +4.2% 2025).

| Metric | Value |

|---|---|

| US 10‑yr (2025) | ~4.5% |

| Fed funds (2025) | ~5.25% |

| CNA yield | 3.8–4.2% |

| CPI (Jan 2026) | 3.4% YoY |

| Materials cost (2024–25) | +~6% |

| GDP growth (2025) | ~1.5% |

| Avg hourly earnings (2025) | +4.2% YoY |

Full Version Awaits

Loews PESTLE Analysis

The preview shown here is the exact Loews PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This file is the final version, with complete content and professional structure, not a teaser or placeholder. After checkout you’ll instantly download the same document visible in the preview, containing the same layout, analysis, and conclusions. What you see is what you’ll own and can apply immediately.