Longfor Group Holdings Boston Consulting Group Matrix

Unlock Strategic Clarity

Longfor Group’s diversified property portfolio likely spans Stars (high-growth urban developments), Cash Cows (mature rental and managed properties), Question Marks (new non-core ventures like logistics or senior living), and Dogs (underperforming assets in oversupplied locales); our preview highlights strategic tensions between landbank monetization and recurring income. Purchase the full BCG Matrix for quadrant-by-quadrant placements, actionable recommendations, and editable Word/Excel deliverables to guide capital allocation and portfolio optimization.

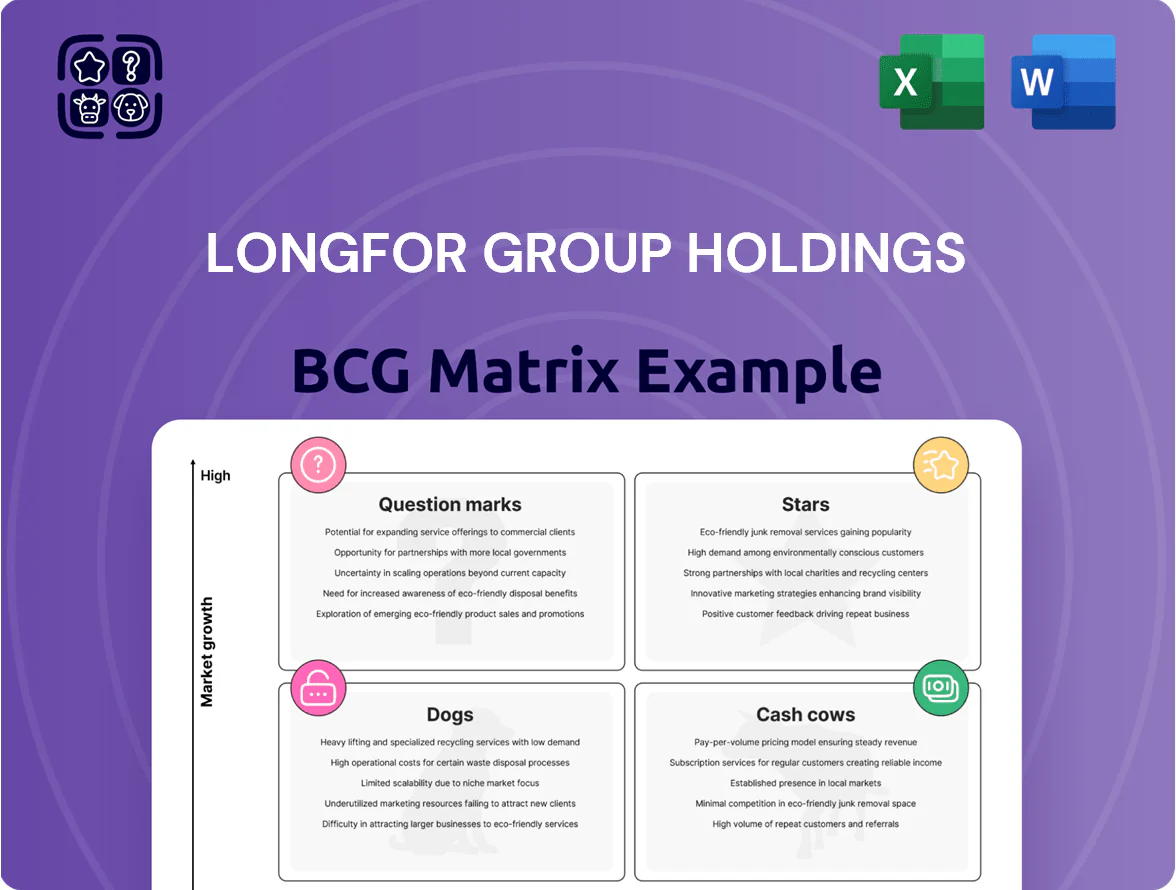

Stars

Commercial Investment and Shopping Malls

Longfor Commercial runs ~90 malls (Paradise Walk, Starry Street) as of mid-2025 with a 96.8% occupancy, marking it a clear Star in the BCG Matrix.

Rental income rose 4.9% YoY H1 2025 to RMB 5.5bn, and the company plans 10 new mall openings in H2 2025 plus 10 annually through 2027, fueling growth.

Heavy capex for construction continues, but high market share in core cities and steady income growth justify Star status.

Goyoo Rental Housing

Goyoo Rental Housing is a market leader in long-term rentals with over 127,000 rooms across tier-1 and tier-2 cities by 2025, posting a 95.6% occupancy rate and driving asset-management revenue—up 2.5% in early 2025—making it a high-growth, high-share Star for Longfor.

Longfor Intelligent Living

Longfor Intelligent Living serves 3.25 million homeowners and manages over 90 shopping centers across ~400 million sq m, generating 6.26 billion RMB in H1 2025 and showing strong third-party expansion.

With customer satisfaction above 90% and operations in 100+ cities, it holds high market share and scales digital service capabilities, keeping it a Star in Longfor Group’s BCG matrix.

Asset-Light Management Services

Longfor is shifting to an asset-light model in commercial and rental housing to cut capital intensity while keeping rapid expansion; in 2025 it reported that 30% of new mall openings were light-asset management projects, where Longfor supplies operations rather than owning assets.

This lets Longfor use its brand and ops expertise to enter new regions with lower balance-sheet risk; the segment’s revenue-from-fees grew 45% YoY in 2025, signaling high growth and Star potential.

- 30% of 2025 new malls: light-asset

- Fee revenue +45% YoY in 2025

- Lower capex per mall: ~60% reduction

- High growth, scalable, lower-risk Star

Smart Construction and Agent Construction

Longfor Smart Construction has secured over 210 agent construction projects totaling more than 33 million square meters by mid-2025, leveraging Longfor’s digital tech and development know-how to offer third-party construction and management services.

Demand is rising as traditional developers outsource to professional partners; Longfor’s move into service-based development created a high-market-share niche in agent construction with rapid project wins and low capital needs.

The segment’s fast project acquisition, scalable tech platform, and asset-light model make Smart Construction a clear Star in Longfor’s BCG Matrix, supporting strong revenue growth and margins.

- 210+ projects; 33M+ sqm by mid-2025

- Third-party construction + management services

- High market share in emerging agent construction

- Asset-light model: rapid scale, low capex

- Classified as Star: high growth, high share

Longfor's Stars: High-Occupancy Commercial, 127k Goyoo Rooms, 3.25M Users, 33M sqm

Longfor’s commercial, rental housing, intelligent living, and smart construction are Stars: high market share and robust growth—commercial: ~90 malls, 96.8% occ., RMB5.5bn rent H1 2025; Goyoo: 127k rooms, 95.6% occ.; Intelligent Living: 3.25m homeowners, RMB6.26bn H1 2025; Smart Construction: 210+ projects, 33M+ sqm mid-2025.

| Segment | Key metric |

|---|---|

| Commercial | 90 malls; 96.8% occ.; RMB5.5bn H1 2025 |

| Goyoo | 127k rooms; 95.6% occ. |

| Intelligent Living | 3.25m users; RMB6.26bn H1 2025 |

| Smart Construction | 210+ projects; 33M+ sqm |

What is included in the product

Comprehensive BCG review of Longfor’s units: Stars to invest, Cash Cows to harvest, Question Marks to evaluate, Dogs to divest.

One-page BCG Matrix placing Longfor Group units in quadrants for swift strategic decisions.

Cash Cows

Residential Property Sales in Tier-1 Cities

Longfor’s Tier-1 residential sales remain a cash cow, generating steady cash flow from mature markets like Beijing and Shanghai where the group holds strong brand and market share.

In 2025 first- and second-tier cities made ~90% of contracted sales, supplying liquidity to fund other units and enabling value harvesting from existing land banks with minimal promo spend.

Paradise Walk Mature Malls

Paradise Walk mature malls are Longfor Group’s cash cows, delivering stable recurring rental income with a 77.7% gross profit margin in H1 2025 and lower volatility than property sales.

Fully occupied and with stabilized foot traffic, these assets need minimal maintenance capex versus new projects, freeing cash to service corporate debt and fund dividends while extracting value from Longfor’s early-mover commercial foothold.

Residential Property Management

The core residential property management business is a classic Cash Cow for Longfor Group Holdings, delivering steady service-fee revenue from roughly 3.2 million homeowners as of 2025 and covering administrative costs while funding R&D.

The mature market for managing existing communities gives Longfor high margins—reported 2024 gross margin ~34%—and predictable operating cash flow, which underpins group financial resilience and funds growth investments.

Commercial Asset Management

Longfor’s Commercial Asset Management is a cash cow: mature mall management for both owned and third-party assets yields high-margin, low-capex revenue, with a 2025 gross profit margin near 30% and recurring fees smoothing cash flow through downturns.

With core-city market saturation, Longfor prioritizes margin and efficiency gains over aggressive footprint growth, keeping operating costs flat while preserving steady free cash for reinvesting in higher-growth Question Marks.

- 2025 gross profit margin ~30%

- Low capital intensity, high recurring fees

- Focus on efficiency, not expansion in core cities

- Provides stable funds to finance Question Marks

Legacy Land Bank Projects

Longfor’s legacy land bank in top-tier and strong second-tier cities, largely bought at pre-2018 prices, is being developed and sold as steady cash cows; as of 2025 the listed inventory liquidation generated roughly RMB 28–35 billion in operating cash flow annually, supporting margins above the portfolio average.

These projects hold high local market share of quality inventory in core districts even as China’s property growth slowed to ~1–3% in 2024–25; Longfor now prioritizes cash-flow health over volume, trimming new land spends and selling down stock.

Steady sell-down funds the pivot to a service-and-operation-led model by 2026, giving liquidity for R&D and operations while reducing leverage from peak net gearing near 80% in 2021 to company-reported mid-40s percent by 2024–25.

- Legacy projects: acquired pre-2018, lower basis

- 2025 cash from inventory: ~RMB 28–35bn

- Market growth: ~1–3% (2024–25)

- Net gearing: peak ~80% (2021) → mid-40s% (2024–25)

- Target: service-and-operation-led by 2026

Longfor’s 2025 cash engine: RMB28–35bn from inventory, high-margin malls & recurring ops

Longfor’s cash cows: Tier‑1 residential sales, Paradise Walk malls, property management, commercial asset management, and legacy land-bank sell‑down—together generating ~RMB28–35bn operating cash in 2025, gross margins 30–77.7%, and supporting net gearing cut to mid‑40s% (2024–25).

| Asset | 2025 cash/Rm | Gross % | Notes |

|---|---|---|---|

| Legacy inventory | 28–35bn | — | low basis |

| Malls | — | 77.7 | stable rent |

| Comm. mgmt | — | ~30 | recurring |

Delivered as Shown

Longfor Group Holdings BCG Matrix

The file you're previewing on this page is the exact Longfor Group Holdings BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, strategy-ready document tailored for clear portfolio analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Longfor Group’s diversified property portfolio likely spans Stars (high-growth urban developments), Cash Cows (mature rental and managed properties), Question Marks (new non-core ventures like logistics or senior living), and Dogs (underperforming assets in oversupplied locales); our preview highlights strategic tensions between landbank monetization and recurring income. Purchase the full BCG Matrix for quadrant-by-quadrant placements, actionable recommendations, and editable Word/Excel deliverables to guide capital allocation and portfolio optimization.

Stars

Commercial Investment and Shopping Malls

Longfor Commercial runs ~90 malls (Paradise Walk, Starry Street) as of mid-2025 with a 96.8% occupancy, marking it a clear Star in the BCG Matrix.

Rental income rose 4.9% YoY H1 2025 to RMB 5.5bn, and the company plans 10 new mall openings in H2 2025 plus 10 annually through 2027, fueling growth.

Heavy capex for construction continues, but high market share in core cities and steady income growth justify Star status.

Goyoo Rental Housing

Goyoo Rental Housing is a market leader in long-term rentals with over 127,000 rooms across tier-1 and tier-2 cities by 2025, posting a 95.6% occupancy rate and driving asset-management revenue—up 2.5% in early 2025—making it a high-growth, high-share Star for Longfor.

Longfor Intelligent Living

Longfor Intelligent Living serves 3.25 million homeowners and manages over 90 shopping centers across ~400 million sq m, generating 6.26 billion RMB in H1 2025 and showing strong third-party expansion.

With customer satisfaction above 90% and operations in 100+ cities, it holds high market share and scales digital service capabilities, keeping it a Star in Longfor Group’s BCG matrix.

Asset-Light Management Services

Longfor is shifting to an asset-light model in commercial and rental housing to cut capital intensity while keeping rapid expansion; in 2025 it reported that 30% of new mall openings were light-asset management projects, where Longfor supplies operations rather than owning assets.

This lets Longfor use its brand and ops expertise to enter new regions with lower balance-sheet risk; the segment’s revenue-from-fees grew 45% YoY in 2025, signaling high growth and Star potential.

- 30% of 2025 new malls: light-asset

- Fee revenue +45% YoY in 2025

- Lower capex per mall: ~60% reduction

- High growth, scalable, lower-risk Star

Smart Construction and Agent Construction

Longfor Smart Construction has secured over 210 agent construction projects totaling more than 33 million square meters by mid-2025, leveraging Longfor’s digital tech and development know-how to offer third-party construction and management services.

Demand is rising as traditional developers outsource to professional partners; Longfor’s move into service-based development created a high-market-share niche in agent construction with rapid project wins and low capital needs.

The segment’s fast project acquisition, scalable tech platform, and asset-light model make Smart Construction a clear Star in Longfor’s BCG Matrix, supporting strong revenue growth and margins.

- 210+ projects; 33M+ sqm by mid-2025

- Third-party construction + management services

- High market share in emerging agent construction

- Asset-light model: rapid scale, low capex

- Classified as Star: high growth, high share

Longfor's Stars: High-Occupancy Commercial, 127k Goyoo Rooms, 3.25M Users, 33M sqm

Longfor’s commercial, rental housing, intelligent living, and smart construction are Stars: high market share and robust growth—commercial: ~90 malls, 96.8% occ., RMB5.5bn rent H1 2025; Goyoo: 127k rooms, 95.6% occ.; Intelligent Living: 3.25m homeowners, RMB6.26bn H1 2025; Smart Construction: 210+ projects, 33M+ sqm mid-2025.

| Segment | Key metric |

|---|---|

| Commercial | 90 malls; 96.8% occ.; RMB5.5bn H1 2025 |

| Goyoo | 127k rooms; 95.6% occ. |

| Intelligent Living | 3.25m users; RMB6.26bn H1 2025 |

| Smart Construction | 210+ projects; 33M+ sqm |

What is included in the product

Comprehensive BCG review of Longfor’s units: Stars to invest, Cash Cows to harvest, Question Marks to evaluate, Dogs to divest.

One-page BCG Matrix placing Longfor Group units in quadrants for swift strategic decisions.

Cash Cows

Residential Property Sales in Tier-1 Cities

Longfor’s Tier-1 residential sales remain a cash cow, generating steady cash flow from mature markets like Beijing and Shanghai where the group holds strong brand and market share.

In 2025 first- and second-tier cities made ~90% of contracted sales, supplying liquidity to fund other units and enabling value harvesting from existing land banks with minimal promo spend.

Paradise Walk Mature Malls

Paradise Walk mature malls are Longfor Group’s cash cows, delivering stable recurring rental income with a 77.7% gross profit margin in H1 2025 and lower volatility than property sales.

Fully occupied and with stabilized foot traffic, these assets need minimal maintenance capex versus new projects, freeing cash to service corporate debt and fund dividends while extracting value from Longfor’s early-mover commercial foothold.

Residential Property Management

The core residential property management business is a classic Cash Cow for Longfor Group Holdings, delivering steady service-fee revenue from roughly 3.2 million homeowners as of 2025 and covering administrative costs while funding R&D.

The mature market for managing existing communities gives Longfor high margins—reported 2024 gross margin ~34%—and predictable operating cash flow, which underpins group financial resilience and funds growth investments.

Commercial Asset Management

Longfor’s Commercial Asset Management is a cash cow: mature mall management for both owned and third-party assets yields high-margin, low-capex revenue, with a 2025 gross profit margin near 30% and recurring fees smoothing cash flow through downturns.

With core-city market saturation, Longfor prioritizes margin and efficiency gains over aggressive footprint growth, keeping operating costs flat while preserving steady free cash for reinvesting in higher-growth Question Marks.

- 2025 gross profit margin ~30%

- Low capital intensity, high recurring fees

- Focus on efficiency, not expansion in core cities

- Provides stable funds to finance Question Marks

Legacy Land Bank Projects

Longfor’s legacy land bank in top-tier and strong second-tier cities, largely bought at pre-2018 prices, is being developed and sold as steady cash cows; as of 2025 the listed inventory liquidation generated roughly RMB 28–35 billion in operating cash flow annually, supporting margins above the portfolio average.

These projects hold high local market share of quality inventory in core districts even as China’s property growth slowed to ~1–3% in 2024–25; Longfor now prioritizes cash-flow health over volume, trimming new land spends and selling down stock.

Steady sell-down funds the pivot to a service-and-operation-led model by 2026, giving liquidity for R&D and operations while reducing leverage from peak net gearing near 80% in 2021 to company-reported mid-40s percent by 2024–25.

- Legacy projects: acquired pre-2018, lower basis

- 2025 cash from inventory: ~RMB 28–35bn

- Market growth: ~1–3% (2024–25)

- Net gearing: peak ~80% (2021) → mid-40s% (2024–25)

- Target: service-and-operation-led by 2026

Longfor’s 2025 cash engine: RMB28–35bn from inventory, high-margin malls & recurring ops

Longfor’s cash cows: Tier‑1 residential sales, Paradise Walk malls, property management, commercial asset management, and legacy land-bank sell‑down—together generating ~RMB28–35bn operating cash in 2025, gross margins 30–77.7%, and supporting net gearing cut to mid‑40s% (2024–25).

| Asset | 2025 cash/Rm | Gross % | Notes |

|---|---|---|---|

| Legacy inventory | 28–35bn | — | low basis |

| Malls | — | 77.7 | stable rent |

| Comm. mgmt | — | ~30 | recurring |

Delivered as Shown

Longfor Group Holdings BCG Matrix

The file you're previewing on this page is the exact Longfor Group Holdings BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, strategy-ready document tailored for clear portfolio analysis.