Longfor Group Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

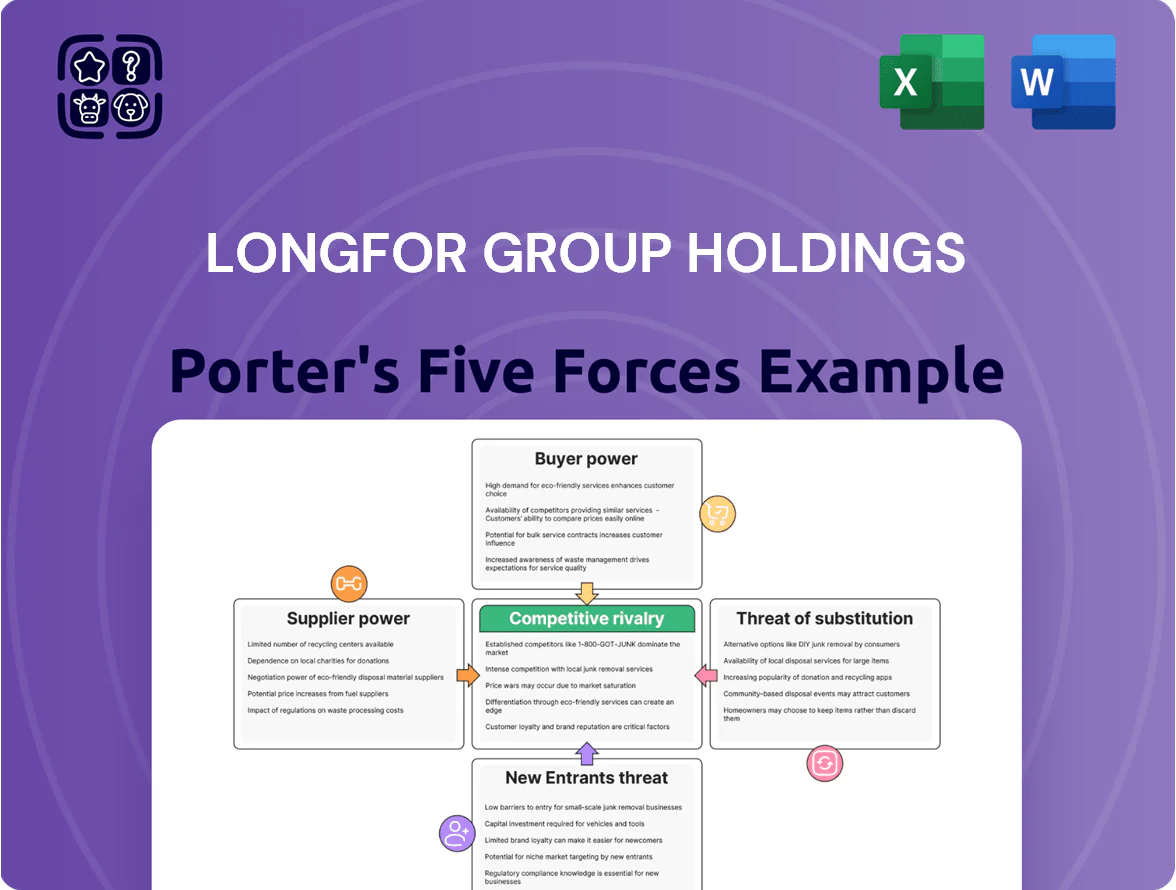

Longfor Group faces moderate supplier power, high buyer sensitivity in China’s property market, and strong rivalry amid policy-driven demand shifts—plus growing threats from substitutes like build-to-rent and proptech.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Longfor Group Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated Land Supply Control

The Chinese state controls over 90% of urban land supply via centralized auctions, keeping Longfor Group Holdings dependent on state-timed land releases and pricing; in 2024, government land-sale revenues reached about RMB 7.2 trillion, underscoring state pricing power.

Financial Capital and Credit Access

After the early-2020s liquidity shocks, banks and bond investors sharply tightened underwriting; by 2025 China property bond spreads averaged ~420 bps above sovereigns, making low-cost capital scarce for private developers.

Longfor Group Holdings keeps a relatively strong credit profile—2024 net gearing ~55% and RMB bond issuance access—but its dependence on bank loans and the bond market gives creditors leverage over interest rates and loan covenants.

With RMB lending rates for developers often 100–200 bps above prime in 2025, lenders effectively control Longfor’s expansion pace and operational stability through pricing and covenant terms.

Construction Material Price Volatility

Suppliers of steel, cement and glass trade in cyclical markets tied to global commodity swings and China’s industrial policies; steel rebar prices in China rose about 12% year-on-year in 2024, pressuring builders.

Longfor is largely price-taker on cost spikes because multi-year contracts limit mid-project material switches, raising margin risk on ongoing projects.

The firm offsets supplier leverage via long-term procurement deals and bulk buying; Longfor reported RMB 32.4 billion in inventories at end-2024, supporting hedging and volume discounts.

Specialized PropTech and Software Providers

As Longfor shifts to AI-driven property management, reliance on niche PropTech vendors for analytics and IoT systems has risen; in 2024 Longfor reported digital investment growth of ~22% year-on-year, raising vendor importance.

Deep integration creates high switching costs—migration can exceed millions per campus—so suppliers gain leverage over pricing and roadmap influence, pressuring the digital transformation budget.

- 2024 digital spend +22%

- High switching costs: millions per campus

- Vendors influence pricing and roadmap

- Dependency raises budgetary risk

Labor Scarcity in Construction and Services

China’s aging workforce has cut skilled construction and property-management labor, pushing wages up—China Ministry of Human Resources showed urban labor shortages rising 12% in 2024, with construction wages up ~8% YoY.

Longfor faces fierce competition for reliable contractors who choose developers by payment track record and safety; delayed payments raise contractor selectivity and cost of capital for projects.

Developers now must offer better pay, on-site safety, and faster payments to secure crews, increasing project OPEX and bid premiums.

- Skilled labor pool shrank; construction wages +8% (2024)

- Contractor selectivity tied to payment reliability

- Higher OPEX and bid premiums for Longfor

Supplier power squeezes Longfor: land, capital, materials and tech inflate costs

Suppliers (state land, banks, materials, tech vendors, labor) hold significant leverage over Longfor via land auction control (state land-sale revenues ~RMB7.2tn in 2024), tight capital (2025 bond spreads ~420bps), material cost shocks (steel +12% YoY 2024), digital vendor switching costs (millions/campus), and rising wages (+8% 2024), constraining margins and expansion.

| Metric | 2024/25 |

|---|---|

| State land revenue | RMB7.2tn (2024) |

| Bond spread | ~420bps (2025) |

| Steel price | +12% YoY (2024) |

| Digital spend | +22% YoY (2024) |

| Wages | +8% YoY (2024) |

What is included in the product

Tailored exclusively for Longfor Group Holdings, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier power, and barriers to entry while identifying disruptive threats and substitutes that could pressure margins and market share.

Concise Porter's Five Forces snapshot for Longfor Group—quickly assess supplier, buyer, entrant, substitute, and rivalry pressures to guide real estate investment and strategic planning.

Customers Bargaining Power

Residential Buyer Price Sensitivity

Residential buyers in 2025 stay highly cautious, prioritizing value and safety after volatility; 62% of Chinese homebuyers surveyed in 2024 said price stability mattered more than appreciation, giving buyers strong leverage to delay purchases or choose secondary-market flats if Longfor prices seem high. Longfor must offer sharper discounts, flexible mortgage support, and premium finishes—projects with >10% price incentive and 90+ quality scores convert wary buyers into 30-year mortgage commitments.

Commercial Tenant Retention Leverage

Retailers and corporate tenants at Longfor Group Holdings face increased bargaining power as e-commerce grew 12.2% YoY in China in 2024 and hybrid work cut office occupancy ~18% versus 2019; large anchors now secure rent-free periods or revenue-share deals, pressuring effective rents down by up to 10-15% in premium malls.

Rental Housing Flexibility

The Goyoo rental brand targets young renters who value mobility and are price- and service-sensitive; surveys show Chinese urban millennials switch providers 28% faster than homeowners, raising churn risk for Longfor.

Short leases (often 1–12 months) create low switching costs, letting tenants move to competitors or subsidized housing—China added ~1.2M public rental units in 2024—so Longfor must keep occupancy above its 92% target.

That pressure forces higher service levels and amenity investment; Longfor reported RMB 850–1,200 monthly ARPU for Goyoo in 2024, squeezing margins if turnover rises.

Information Transparency and Digital Comparison

The rise of digital platforms lets buyers compare prices, management fees, and developer reputations in real time across China’s market, shrinking information asymmetry that once favored developers.

With 2024 data showing 68% of Chinese property searches start online and third-party review sites influencing 42% of purchase decisions, Longfor must be more transparent and consistent to keep investor trust.

- 68% start searches online (2024)

- 42% influenced by reviews (2024)

- Transparency reduces price margins

- Consistency needed to retain informed buyers

Institutional Investor Expectations

Institutional clients buying bulk commercial assets or REIT stakes demand transparent reporting and strict ESG; in 2025 global ESG AUM hit $40.5tr, pushing Longfor to tighten disclosures across its portfolio.

These investors use advanced analytics to challenge Longfor’s valuations and press for higher yields—Chinese office cap rates rose ~120bp in 2023–24—raising funding pressure amid higher rates.

Their ability to shift large capital pools gives them sway over Longfor’s asset-management strategy, influencing asset sales, JV terms, and ESG-linked targets.

- ESG AUM: $40.5tr (2025)

- Office cap-rate rise: ~120bp (2023–24)

- Institutional leverage: large-ticket REIT/joint-venture influence

Buyers seize power 2025: price-savvy, online-first, reviews-driven — rents down, ESG demands up

Buyers hold strong leverage in 2025: 62% cite price stability (2024), 68% start searches online (2024), and 42% influenced by reviews (2024), forcing Longfor into >10% incentives or flexible mortgage support to convert sales; retail tenants push effective rents down 10–15% as e‑commerce grew 12.2% YoY (2024); institutional investors (ESG AUM $40.5tr, 2025) demand transparency and higher yields.

| Metric | Value |

|---|---|

| Price-sensitivity | 62% (2024) |

| Online search start | 68% (2024) |

| Review influence | 42% (2024) |

| E‑commerce growth | 12.2% YoY (2024) |

| Retail rent pressure | -10–15% |

| ESG AUM | $40.5tr (2025) |

Preview the Actual Deliverable

Longfor Group Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Longfor Group Holdings you’ll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the full, professionally formatted analysis—ready for download and use the moment you buy.

You’re viewing the actual deliverable; once you complete payment, you’ll get instant access to this same file with complete Five Forces insights.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Longfor Group faces moderate supplier power, high buyer sensitivity in China’s property market, and strong rivalry amid policy-driven demand shifts—plus growing threats from substitutes like build-to-rent and proptech.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Longfor Group Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated Land Supply Control

The Chinese state controls over 90% of urban land supply via centralized auctions, keeping Longfor Group Holdings dependent on state-timed land releases and pricing; in 2024, government land-sale revenues reached about RMB 7.2 trillion, underscoring state pricing power.

Financial Capital and Credit Access

After the early-2020s liquidity shocks, banks and bond investors sharply tightened underwriting; by 2025 China property bond spreads averaged ~420 bps above sovereigns, making low-cost capital scarce for private developers.

Longfor Group Holdings keeps a relatively strong credit profile—2024 net gearing ~55% and RMB bond issuance access—but its dependence on bank loans and the bond market gives creditors leverage over interest rates and loan covenants.

With RMB lending rates for developers often 100–200 bps above prime in 2025, lenders effectively control Longfor’s expansion pace and operational stability through pricing and covenant terms.

Construction Material Price Volatility

Suppliers of steel, cement and glass trade in cyclical markets tied to global commodity swings and China’s industrial policies; steel rebar prices in China rose about 12% year-on-year in 2024, pressuring builders.

Longfor is largely price-taker on cost spikes because multi-year contracts limit mid-project material switches, raising margin risk on ongoing projects.

The firm offsets supplier leverage via long-term procurement deals and bulk buying; Longfor reported RMB 32.4 billion in inventories at end-2024, supporting hedging and volume discounts.

Specialized PropTech and Software Providers

As Longfor shifts to AI-driven property management, reliance on niche PropTech vendors for analytics and IoT systems has risen; in 2024 Longfor reported digital investment growth of ~22% year-on-year, raising vendor importance.

Deep integration creates high switching costs—migration can exceed millions per campus—so suppliers gain leverage over pricing and roadmap influence, pressuring the digital transformation budget.

- 2024 digital spend +22%

- High switching costs: millions per campus

- Vendors influence pricing and roadmap

- Dependency raises budgetary risk

Labor Scarcity in Construction and Services

China’s aging workforce has cut skilled construction and property-management labor, pushing wages up—China Ministry of Human Resources showed urban labor shortages rising 12% in 2024, with construction wages up ~8% YoY.

Longfor faces fierce competition for reliable contractors who choose developers by payment track record and safety; delayed payments raise contractor selectivity and cost of capital for projects.

Developers now must offer better pay, on-site safety, and faster payments to secure crews, increasing project OPEX and bid premiums.

- Skilled labor pool shrank; construction wages +8% (2024)

- Contractor selectivity tied to payment reliability

- Higher OPEX and bid premiums for Longfor

Supplier power squeezes Longfor: land, capital, materials and tech inflate costs

Suppliers (state land, banks, materials, tech vendors, labor) hold significant leverage over Longfor via land auction control (state land-sale revenues ~RMB7.2tn in 2024), tight capital (2025 bond spreads ~420bps), material cost shocks (steel +12% YoY 2024), digital vendor switching costs (millions/campus), and rising wages (+8% 2024), constraining margins and expansion.

| Metric | 2024/25 |

|---|---|

| State land revenue | RMB7.2tn (2024) |

| Bond spread | ~420bps (2025) |

| Steel price | +12% YoY (2024) |

| Digital spend | +22% YoY (2024) |

| Wages | +8% YoY (2024) |

What is included in the product

Tailored exclusively for Longfor Group Holdings, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier power, and barriers to entry while identifying disruptive threats and substitutes that could pressure margins and market share.

Concise Porter's Five Forces snapshot for Longfor Group—quickly assess supplier, buyer, entrant, substitute, and rivalry pressures to guide real estate investment and strategic planning.

Customers Bargaining Power

Residential Buyer Price Sensitivity

Residential buyers in 2025 stay highly cautious, prioritizing value and safety after volatility; 62% of Chinese homebuyers surveyed in 2024 said price stability mattered more than appreciation, giving buyers strong leverage to delay purchases or choose secondary-market flats if Longfor prices seem high. Longfor must offer sharper discounts, flexible mortgage support, and premium finishes—projects with >10% price incentive and 90+ quality scores convert wary buyers into 30-year mortgage commitments.

Commercial Tenant Retention Leverage

Retailers and corporate tenants at Longfor Group Holdings face increased bargaining power as e-commerce grew 12.2% YoY in China in 2024 and hybrid work cut office occupancy ~18% versus 2019; large anchors now secure rent-free periods or revenue-share deals, pressuring effective rents down by up to 10-15% in premium malls.

Rental Housing Flexibility

The Goyoo rental brand targets young renters who value mobility and are price- and service-sensitive; surveys show Chinese urban millennials switch providers 28% faster than homeowners, raising churn risk for Longfor.

Short leases (often 1–12 months) create low switching costs, letting tenants move to competitors or subsidized housing—China added ~1.2M public rental units in 2024—so Longfor must keep occupancy above its 92% target.

That pressure forces higher service levels and amenity investment; Longfor reported RMB 850–1,200 monthly ARPU for Goyoo in 2024, squeezing margins if turnover rises.

Information Transparency and Digital Comparison

The rise of digital platforms lets buyers compare prices, management fees, and developer reputations in real time across China’s market, shrinking information asymmetry that once favored developers.

With 2024 data showing 68% of Chinese property searches start online and third-party review sites influencing 42% of purchase decisions, Longfor must be more transparent and consistent to keep investor trust.

- 68% start searches online (2024)

- 42% influenced by reviews (2024)

- Transparency reduces price margins

- Consistency needed to retain informed buyers

Institutional Investor Expectations

Institutional clients buying bulk commercial assets or REIT stakes demand transparent reporting and strict ESG; in 2025 global ESG AUM hit $40.5tr, pushing Longfor to tighten disclosures across its portfolio.

These investors use advanced analytics to challenge Longfor’s valuations and press for higher yields—Chinese office cap rates rose ~120bp in 2023–24—raising funding pressure amid higher rates.

Their ability to shift large capital pools gives them sway over Longfor’s asset-management strategy, influencing asset sales, JV terms, and ESG-linked targets.

- ESG AUM: $40.5tr (2025)

- Office cap-rate rise: ~120bp (2023–24)

- Institutional leverage: large-ticket REIT/joint-venture influence

Buyers seize power 2025: price-savvy, online-first, reviews-driven — rents down, ESG demands up

Buyers hold strong leverage in 2025: 62% cite price stability (2024), 68% start searches online (2024), and 42% influenced by reviews (2024), forcing Longfor into >10% incentives or flexible mortgage support to convert sales; retail tenants push effective rents down 10–15% as e‑commerce grew 12.2% YoY (2024); institutional investors (ESG AUM $40.5tr, 2025) demand transparency and higher yields.

| Metric | Value |

|---|---|

| Price-sensitivity | 62% (2024) |

| Online search start | 68% (2024) |

| Review influence | 42% (2024) |

| E‑commerce growth | 12.2% YoY (2024) |

| Retail rent pressure | -10–15% |

| ESG AUM | $40.5tr (2025) |

Preview the Actual Deliverable

Longfor Group Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Longfor Group Holdings you’ll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the full, professionally formatted analysis—ready for download and use the moment you buy.

You’re viewing the actual deliverable; once you complete payment, you’ll get instant access to this same file with complete Five Forces insights.