Lonza Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Lonza Group faces intense supplier and buyer dynamics driven by high-tech pharmaceuticals, significant regulatory barriers, and moderate threat from specialized entrants and substitutes, yet its scale and integrated services create meaningful defensive advantages; this snapshot highlights key pressures but omits detailed metrics and implications.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lonza Group’s competitive dynamics, market pressures, and strategic advantages in detail.

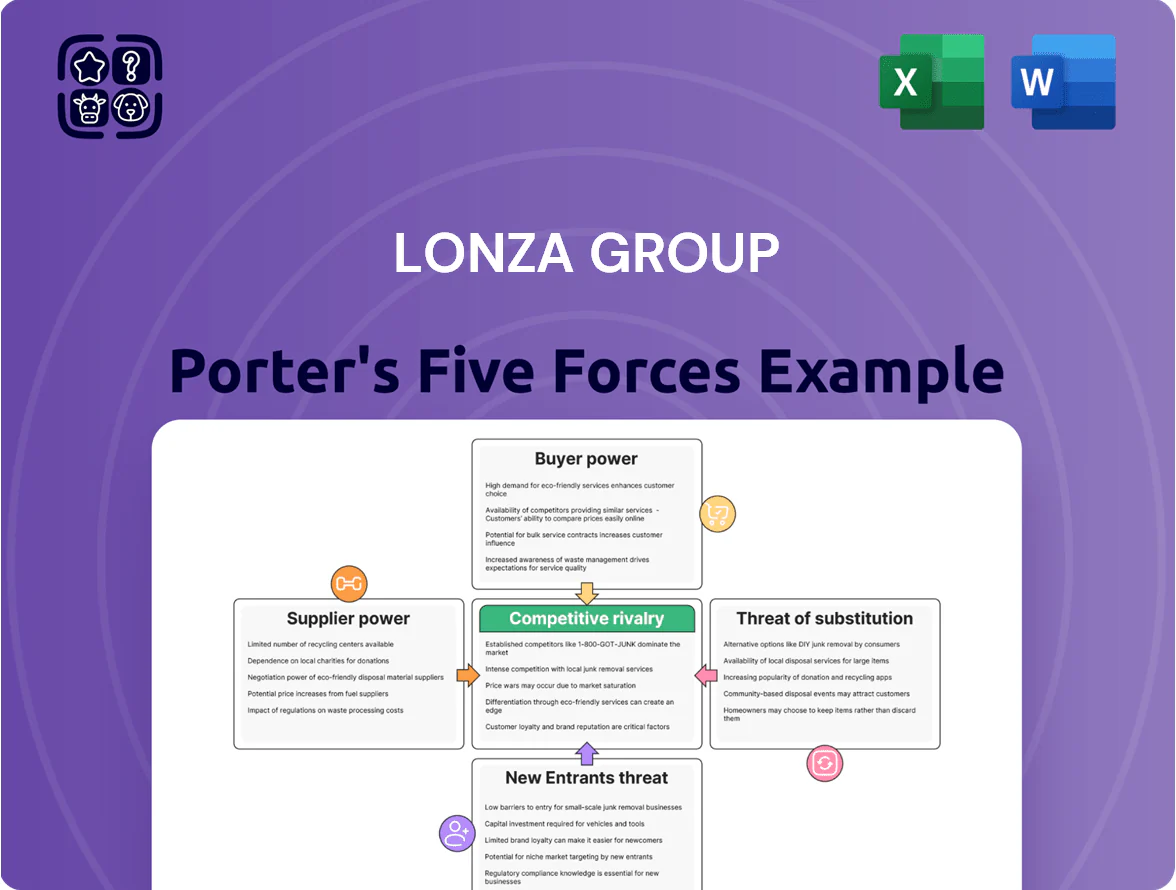

Suppliers Bargaining Power

Specialized Raw Material Dependency

Lonza depends on high-purity chemicals, biological media, and specialized resins for biologics and small-molecule production; roughly 60–70% of critical inputs come from a small pool of certified suppliers as of 2025.

These vendors must meet strict Good Manufacturing Practice (GMP) standards, raising barriers to entry and limiting alternatives.

Supplier concentration gives them leverage on price and supply priority, risking cost increases and short-term allocation advantage during demand spikes.

Regulatory Compliance Standards

Suppliers must meet strict FDA and EMA standards—pharmaceutical GMP and ISO 13485—so only certified vendors enter Lonza’s chain; noncompliant firms are excluded. Switching suppliers triggers validation, stability studies and batch comparability testing that can cost $1–5M and take 6–18 months, raising tangible exit costs. This technical lock-in boosts bargaining power of compliant suppliers already integrated into Lonza’s quality systems, reducing Lonza’s leverage.

Energy and Utility Volatility

Energy-intensive pharma and nutrition manufacturing makes Lonza vulnerable to fuel price swings; industrial electricity jumped 18% in Europe in 2022–24, squeezing margins.

By late 2025, demand for certified green power rose; renewable suppliers gained leverage as utilities offering guarantees of origin charge 5–12% premiums.

Lonza’s net-zero pledge (2050 target; 2030 interim scopes) narrows suppliers to certified-renewable providers, raising switching costs and supplier power.

Equipment Manufacturer Influence

Advanced biologics manufacturing needs complex single-use bioreactors and automation from a few global firms; top suppliers like Sartorius and GE Healthcare Life Sciences held over 40% market share in single-use systems by 2024, concentrating supplier power.

These vendors protect margins with proprietary tech and multi-year service contracts—industry spare-part and service margins often exceed 20%—making Lonza dependent during procurement and upgrades for its large-scale Swiss and US sites.

- Few suppliers: >40% market share (2024)

- High service margins: ~20%+

- Long contracts: multi-year maintenance common

- Dependency: ecosystem lock-in raises switching costs

Geopolitical Supply Chain Risks

- China ~60% rare earth output (2024)

- Long-term contracts raise supplier leverage

- Dual-sourcing and forward-buying mitigate risk

High supplier leverage: 60–70% inputs concentrated, costly switches, energy & rare-earth risks

Supplier power is high: 60–70% critical inputs from few GMP-certified vendors (2025), single-use systems suppliers held >40% share (2024), switching costs $1–5M and 6–18 months, energy up 18% (Europe 2022–24), renewables 5–12% premium (2025), China ~60% rare earths (2024); Lonza mitigates via dual-sourcing, long-term contracts, and forward-buying.

| Metric | Value |

|---|---|

| Critical-input concentration | 60–70% |

| Single-use market share | >40% |

| Switch cost/time | $1–5M / 6–18m |

| Energy rise (EU) | +18% |

| Rare earth output (China) | ~60% |

What is included in the product

Tailored exclusively for Lonza Group, this Porter's Five Forces overview uncovers competitive intensity, supplier and buyer power, entry barriers, substitute threats, and disruptive forces shaping its pricing power and strategic positioning.

Quick, one-sheet Porter’s Five Forces for Lonza—instantly spot supplier, buyer, and competitive pressures to streamline strategic decisions.

Customers Bargaining Power

High Switching Costs

Once a pharma partner embeds Lonza’s processes into clinical or commercial supply, switching to another CDMO becomes extremely costly and slow; regulatory re-validation for a drug substance often takes 12–36 months and can exceed $5–20 million per SKU, locking customers into Lonza’s ecosystem. This creates high switching costs that materially lower customer bargaining power once production commences. Lonza’s long-term contracts and tech-transfer expertise amplify the lock-in, and customers face supply-risk and regulatory delays if they try to move.

Customer Concentration Risk

Lonza serves both large-cap pharma and smaller biotech clients, with top 10 pharma customers contributing about 45% of 2024 revenues, so customer concentration risk is high. Large clients negotiate steep volume discounts and priority scheduling, pressuring gross margins and capacity allocation. Losing a single top-tier contract could cut facility utilization by ~10–20% and reduce EBITDA margin by several percentage points based on 2024 operating metrics.

Demand for End-to-End Services

Modern biopharma clients prefer one-stop-shop providers handling discovery to commercial fill-finish; Lonza’s integrated services—R&D, clinical, and commercial manufacturing—boost its value proposition but raise expectations for bundled pricing. In 2024 Lonza reported CHF 5.2bn revenue and highlighted growth in integrated CDMO contracts, so sophisticated buyers now pressure for lower bundle rates versus standalone fees. This shifts margin mix and increases negotiation leverage for large pharma customers.

Biotech Funding Environment

Small and mid-sized biotech firms’ R&D now tracks funding: VC deal value fell 28% in 2024 to about $34bn and IPOs dropped 62% vs 2021, so customers are price-sensitive and cut discretionary pharma/CDMO spend.

In 2025 these clients push for flexible terms—milestone payments, net-90 or revenue-share—raising Lonza’s sales negotiation burden and compressing margins.

Their collective bargaining power rises when funding tightens, forcing Lonza to offer discounts, capacity guarantees, or co-development clauses to retain projects.

- 2024 VC funding: ~$34bn (−28% YoY)

- 2024 biotech IPOs: −62% vs 2021

- Common asks: milestone pay, net-60/90, revenue-share

- Impact: pricing pressure, longer receivables, more contract complexity

Transparency and Quality Audits

Customers in healthcare exert strong bargaining power through frequent, rigorous audits of Lonza’s plants; in 2024 Lonza reported 18% of CAPA (corrective actions) tied to audit findings, reflecting audit intensity.

Clients demand transparency on data integrity and end-to-end traceability, pushing Lonza to disclose serialization and batch data and meet GDP/GMP standards.

This forces ongoing investment in digital quality systems; Lonza spent CHF 120m on quality and IT in 2024 to maintain compliance with sophisticated buyers.

- Frequent audits: high audit-driven CAPA (18% in 2024)

- Transparency needs: serialization, batch traceability, data integrity

- Capex: CHF 120m quality/IT spend in 2024

Concentrated buyers and funding cuts tighten margins despite post-sale lock‑in

Customers hold moderate-to-high bargaining power: high switching costs and regulatory lock-in reduce it post-qualification, but customer concentration (top-10 ≈45% of 2024 revenue), large-client discounting, funding-driven price sensitivity (2024 VC ≈$34bn) and demands for flexible terms squeeze margins and raise negotiation complexity.

| Metric | Value (2024) |

|---|---|

| Top-10 revenue share | ≈45% |

| VC funding | $34bn (−28% YoY) |

| Quality/IT spend | CHF120m |

Same Document Delivered

Lonza Group Porter's Five Forces Analysis

This preview shows the exact Lonza Group Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, fully formatted, and ready for use. It covers supplier and buyer power, competitive rivalry, threat of substitution, and barriers to entry with actionable insights and evidence-based scoring. What you see here is the final deliverable available for instant download once you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Lonza Group faces intense supplier and buyer dynamics driven by high-tech pharmaceuticals, significant regulatory barriers, and moderate threat from specialized entrants and substitutes, yet its scale and integrated services create meaningful defensive advantages; this snapshot highlights key pressures but omits detailed metrics and implications.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lonza Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

Lonza depends on high-purity chemicals, biological media, and specialized resins for biologics and small-molecule production; roughly 60–70% of critical inputs come from a small pool of certified suppliers as of 2025.

These vendors must meet strict Good Manufacturing Practice (GMP) standards, raising barriers to entry and limiting alternatives.

Supplier concentration gives them leverage on price and supply priority, risking cost increases and short-term allocation advantage during demand spikes.

Regulatory Compliance Standards

Suppliers must meet strict FDA and EMA standards—pharmaceutical GMP and ISO 13485—so only certified vendors enter Lonza’s chain; noncompliant firms are excluded. Switching suppliers triggers validation, stability studies and batch comparability testing that can cost $1–5M and take 6–18 months, raising tangible exit costs. This technical lock-in boosts bargaining power of compliant suppliers already integrated into Lonza’s quality systems, reducing Lonza’s leverage.

Energy and Utility Volatility

Energy-intensive pharma and nutrition manufacturing makes Lonza vulnerable to fuel price swings; industrial electricity jumped 18% in Europe in 2022–24, squeezing margins.

By late 2025, demand for certified green power rose; renewable suppliers gained leverage as utilities offering guarantees of origin charge 5–12% premiums.

Lonza’s net-zero pledge (2050 target; 2030 interim scopes) narrows suppliers to certified-renewable providers, raising switching costs and supplier power.

Equipment Manufacturer Influence

Advanced biologics manufacturing needs complex single-use bioreactors and automation from a few global firms; top suppliers like Sartorius and GE Healthcare Life Sciences held over 40% market share in single-use systems by 2024, concentrating supplier power.

These vendors protect margins with proprietary tech and multi-year service contracts—industry spare-part and service margins often exceed 20%—making Lonza dependent during procurement and upgrades for its large-scale Swiss and US sites.

- Few suppliers: >40% market share (2024)

- High service margins: ~20%+

- Long contracts: multi-year maintenance common

- Dependency: ecosystem lock-in raises switching costs

Geopolitical Supply Chain Risks

- China ~60% rare earth output (2024)

- Long-term contracts raise supplier leverage

- Dual-sourcing and forward-buying mitigate risk

High supplier leverage: 60–70% inputs concentrated, costly switches, energy & rare-earth risks

Supplier power is high: 60–70% critical inputs from few GMP-certified vendors (2025), single-use systems suppliers held >40% share (2024), switching costs $1–5M and 6–18 months, energy up 18% (Europe 2022–24), renewables 5–12% premium (2025), China ~60% rare earths (2024); Lonza mitigates via dual-sourcing, long-term contracts, and forward-buying.

| Metric | Value |

|---|---|

| Critical-input concentration | 60–70% |

| Single-use market share | >40% |

| Switch cost/time | $1–5M / 6–18m |

| Energy rise (EU) | +18% |

| Rare earth output (China) | ~60% |

What is included in the product

Tailored exclusively for Lonza Group, this Porter's Five Forces overview uncovers competitive intensity, supplier and buyer power, entry barriers, substitute threats, and disruptive forces shaping its pricing power and strategic positioning.

Quick, one-sheet Porter’s Five Forces for Lonza—instantly spot supplier, buyer, and competitive pressures to streamline strategic decisions.

Customers Bargaining Power

High Switching Costs

Once a pharma partner embeds Lonza’s processes into clinical or commercial supply, switching to another CDMO becomes extremely costly and slow; regulatory re-validation for a drug substance often takes 12–36 months and can exceed $5–20 million per SKU, locking customers into Lonza’s ecosystem. This creates high switching costs that materially lower customer bargaining power once production commences. Lonza’s long-term contracts and tech-transfer expertise amplify the lock-in, and customers face supply-risk and regulatory delays if they try to move.

Customer Concentration Risk

Lonza serves both large-cap pharma and smaller biotech clients, with top 10 pharma customers contributing about 45% of 2024 revenues, so customer concentration risk is high. Large clients negotiate steep volume discounts and priority scheduling, pressuring gross margins and capacity allocation. Losing a single top-tier contract could cut facility utilization by ~10–20% and reduce EBITDA margin by several percentage points based on 2024 operating metrics.

Demand for End-to-End Services

Modern biopharma clients prefer one-stop-shop providers handling discovery to commercial fill-finish; Lonza’s integrated services—R&D, clinical, and commercial manufacturing—boost its value proposition but raise expectations for bundled pricing. In 2024 Lonza reported CHF 5.2bn revenue and highlighted growth in integrated CDMO contracts, so sophisticated buyers now pressure for lower bundle rates versus standalone fees. This shifts margin mix and increases negotiation leverage for large pharma customers.

Biotech Funding Environment

Small and mid-sized biotech firms’ R&D now tracks funding: VC deal value fell 28% in 2024 to about $34bn and IPOs dropped 62% vs 2021, so customers are price-sensitive and cut discretionary pharma/CDMO spend.

In 2025 these clients push for flexible terms—milestone payments, net-90 or revenue-share—raising Lonza’s sales negotiation burden and compressing margins.

Their collective bargaining power rises when funding tightens, forcing Lonza to offer discounts, capacity guarantees, or co-development clauses to retain projects.

- 2024 VC funding: ~$34bn (−28% YoY)

- 2024 biotech IPOs: −62% vs 2021

- Common asks: milestone pay, net-60/90, revenue-share

- Impact: pricing pressure, longer receivables, more contract complexity

Transparency and Quality Audits

Customers in healthcare exert strong bargaining power through frequent, rigorous audits of Lonza’s plants; in 2024 Lonza reported 18% of CAPA (corrective actions) tied to audit findings, reflecting audit intensity.

Clients demand transparency on data integrity and end-to-end traceability, pushing Lonza to disclose serialization and batch data and meet GDP/GMP standards.

This forces ongoing investment in digital quality systems; Lonza spent CHF 120m on quality and IT in 2024 to maintain compliance with sophisticated buyers.

- Frequent audits: high audit-driven CAPA (18% in 2024)

- Transparency needs: serialization, batch traceability, data integrity

- Capex: CHF 120m quality/IT spend in 2024

Concentrated buyers and funding cuts tighten margins despite post-sale lock‑in

Customers hold moderate-to-high bargaining power: high switching costs and regulatory lock-in reduce it post-qualification, but customer concentration (top-10 ≈45% of 2024 revenue), large-client discounting, funding-driven price sensitivity (2024 VC ≈$34bn) and demands for flexible terms squeeze margins and raise negotiation complexity.

| Metric | Value (2024) |

|---|---|

| Top-10 revenue share | ≈45% |

| VC funding | $34bn (−28% YoY) |

| Quality/IT spend | CHF120m |

Same Document Delivered

Lonza Group Porter's Five Forces Analysis

This preview shows the exact Lonza Group Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, fully formatted, and ready for use. It covers supplier and buyer power, competitive rivalry, threat of substitution, and barriers to entry with actionable insights and evidence-based scoring. What you see here is the final deliverable available for instant download once you buy.