L'Oréal Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

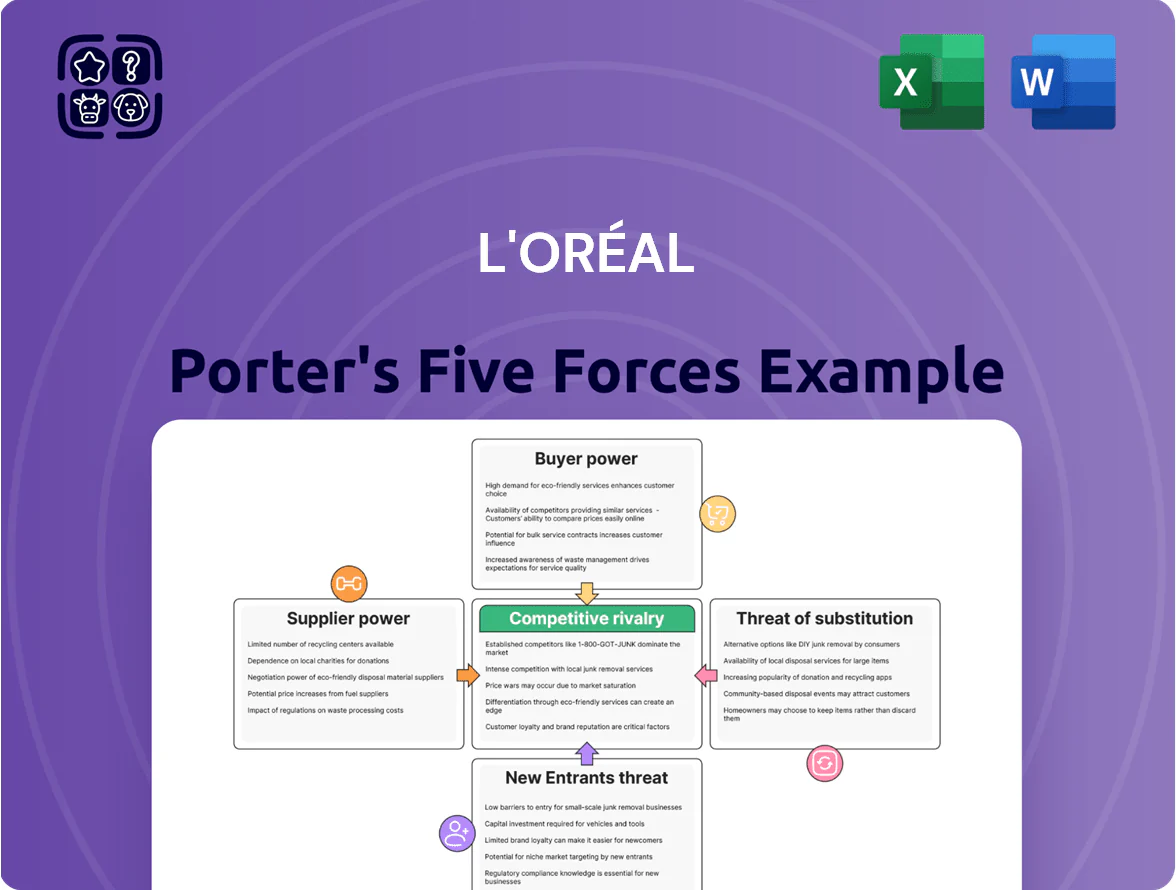

L'Oréal faces intense rivalry from global and indie beauty players, strong buyer power driven by brand-savvy consumers, and moderate supplier leverage thanks to diversified sourcing and R&D prowess.

Regulatory hurdles and high capital requirements limit new entrants, while substitutes from wellness and tech-enabled personalisation pose rising threats to market share.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore L'Oréal’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Low Concentration of Raw Material Providers

The beauty sector sources chemicals, packaging and agri inputs from thousands of suppliers, so no single provider monopolises key inputs; global cosmetics chemical suppliers numbered over 3,000 in 2024. L'Oréal’s 2024 procurement spend exceeded €10.8bn, letting it split orders across regions and cut dependence on any vendor. This supplier fragmentation and L'Oréal’s scale constrain suppliers’ bargaining power, since a >€1bn contract loss would be likely if prices rose sharply.

High Volume Purchases and Economies of Scale

As the world leader in beauty with 2024 sales of €42.6 billion, L'Oréal leverages massive purchase volumes to extract lower input costs and priority supply, often securing discounts of 5–15% on raw materials versus smaller rivals.

Suppliers treat L'Oréal as a stable anchor client—its ~88,000 SKUs and global sourcing give vendors predictable demand, making supplier revenue exposure skewed toward L'Oréal and reducing their bargaining power.

Strategic Focus on Green Chemistry and Sustainability

Low Switching Costs for Standard Components

For standardized ingredients like surfactants, emollients and basic packaging, L'Oréal faces low switching costs, letting it change suppliers quickly to protect margins.

As of 2024 L'Oréal sourced from 2,000+ suppliers globally and allocated >40% of procurement to multi‑sourced commodities, reducing single‑provider risk.

This diversified base and ready alternatives curb supplier price power, since sellers risk losing volumes to competitors.

- Low switching costs for standard inputs

- 2,000+ suppliers (2024)

- >40% procurement from multi‑sourced commodities

Backward Integration and R&D Capabilities

L'Oréal’s 2024 R&D spend was €1.3bn, funding 21 research centers that produce proprietary formulations and select actives in-house, creating a real threat of backward integration and reducing supplier dependence.

This technical autonomy boosts bargaining leverage in supplier negotiations, helps preserve gross margins (group 2024 gross margin ~74%), and lowers price and supply risks for key ingredients.

- 2024 R&D: €1.3bn; 21 centers

- In-house actives reduce supplier reliance

- Creates credible backward-integration threat

- Supports ~74% gross margin protection

L'Oréal’s scale, R&D and multi‑sourcing cap supplier power, saving €120–150m/yr

Supplier power is low: L'Oréal’s €10.8bn+ 2024 procurement, 2,000+ suppliers, >40% multi‑sourced commodities, and €1.3bn R&D (21 centres) enable volume discounts (5–15%), multi‑sourcing, co‑investments (42% botanical/biotech via partnerships in 2024) and backward‑integration, capping supplier hold‑up and saving ~€120–150m/year in premiums.

| Metric | 2024 |

|---|---|

| Procurement spend | €10.8bn+ |

| Suppliers | 2,000+ |

| R&D | €1.3bn (21 centres) |

| Biotech partnerships | 42% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier dynamics, substitute threats, and entry barriers in L'Oréal's market, highlighting disruptive forces, pricing power, and strategic protections that shape its profitability and competitive positioning.

Compact Porter's Five Forces for L'Oréal—distills competitive intensity, supplier/buyer power, threat of substitutes and entrants into one slide-ready summary to speed strategic decisions.

Customers Bargaining Power

High Leverage of Global Retail Giants

Low Switching Costs for Individual Consumers

Individual consumers face near-zero financial switching costs when moving from L'Oréal to rivals, so a 2024 Euromonitor estimate showing 12% annual churn in global prestige and mass beauty highlights constant defections.

The market’s 2023-24 flood of launches—over 30,000 SKUs in skin, makeup, hair—keeps loyalty fragile as viral trends shift demand within weeks.

As a result, L'Oréal spent €3.9bn on R&D and marketing in 2024, reflecting necessary continuous investment to defend market share and pricing tiers.

Transparency and Price Sensitivity in E-commerce

By late 2025, e-commerce accounted for ~32% of global beauty sales and widespread price-comparison tools mean consumers find best deals instantly, capping L'Oréal's room for blunt price hikes.

L'Oréal reports 20% of sales tied to online channels and so uses advanced analytics to deliver personalized promos and loyalty rewards, reducing churn from price-sensitive buyers.

Influence of Social Media and Peer Reviews

Modern consumers use social proof, influencers, and reviews more than ads, giving buyers soft power: a viral negative post can dent sales across lines within days.

L'Oréal counters by investing in community engagement and product trials; in 2024 it increased digital spend 18% and cites average 4.4/5 ratings across key third-party retailers.

- Single viral complaint can cut weekly sales by double digits

- L'Oréal 2024 digital spend +18%

- Average ratings ~4.4/5 on major platforms

Demand for Sustainable and Ethical Practices

By 2025, roughly 60% of global consumers prioritize ethical sourcing, vegan formulas, and plastic-free packaging, giving shoppers collective leverage to boycott brands that fail ESG tests.

L'Oréal responds via its L'Oréal for the Future program, pledging 100% biodegradable or refillable packaging by 2030 and reporting a 65% cut in carbon intensity since 2005 to align with buyer demands.

- 60% consumers prefer ethical products (2025)

- Consumers can boycott—raises switching risk

- L'Oréal for the Future: 100% refillable/biodegradable by 2030

- 65% cut carbon intensity since 2005

Retailers Hold the Leverage: L'Oréal €36.5bn Faces Margin Pressure, 32% e‑commerce

Major retailers (Walmart, Sephora, Carrefour) drove ~35% of L'Oréal sales in 2024, giving them strong trade leverage; L'Oréal €36.5bn 2024 revenue means big buyers can press margins. Consumers have near-zero switching costs (Euromonitor 12% churn, prestige+m ass 2024) and e‑commerce ~32% by 2025, forcing continuous €3.9bn R&D/marketing spend and ESG moves (2030 refillable goal).

| Metric | Value |

|---|---|

| 2024 Revenue | €36.5bn |

| Retailer share | ~35% |

| Churn (2024) | 12% |

| R&D & Mktg (2024) | €3.9bn |

| E‑commerce (2025) | ~32% |

Preview Before You Purchase

L'Oréal Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of L'Oréal you'll receive immediately after purchase—no placeholders or mockups; the full, professionally formatted document is ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

L'Oréal faces intense rivalry from global and indie beauty players, strong buyer power driven by brand-savvy consumers, and moderate supplier leverage thanks to diversified sourcing and R&D prowess.

Regulatory hurdles and high capital requirements limit new entrants, while substitutes from wellness and tech-enabled personalisation pose rising threats to market share.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore L'Oréal’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Low Concentration of Raw Material Providers

The beauty sector sources chemicals, packaging and agri inputs from thousands of suppliers, so no single provider monopolises key inputs; global cosmetics chemical suppliers numbered over 3,000 in 2024. L'Oréal’s 2024 procurement spend exceeded €10.8bn, letting it split orders across regions and cut dependence on any vendor. This supplier fragmentation and L'Oréal’s scale constrain suppliers’ bargaining power, since a >€1bn contract loss would be likely if prices rose sharply.

High Volume Purchases and Economies of Scale

As the world leader in beauty with 2024 sales of €42.6 billion, L'Oréal leverages massive purchase volumes to extract lower input costs and priority supply, often securing discounts of 5–15% on raw materials versus smaller rivals.

Suppliers treat L'Oréal as a stable anchor client—its ~88,000 SKUs and global sourcing give vendors predictable demand, making supplier revenue exposure skewed toward L'Oréal and reducing their bargaining power.

Strategic Focus on Green Chemistry and Sustainability

Low Switching Costs for Standard Components

For standardized ingredients like surfactants, emollients and basic packaging, L'Oréal faces low switching costs, letting it change suppliers quickly to protect margins.

As of 2024 L'Oréal sourced from 2,000+ suppliers globally and allocated >40% of procurement to multi‑sourced commodities, reducing single‑provider risk.

This diversified base and ready alternatives curb supplier price power, since sellers risk losing volumes to competitors.

- Low switching costs for standard inputs

- 2,000+ suppliers (2024)

- >40% procurement from multi‑sourced commodities

Backward Integration and R&D Capabilities

L'Oréal’s 2024 R&D spend was €1.3bn, funding 21 research centers that produce proprietary formulations and select actives in-house, creating a real threat of backward integration and reducing supplier dependence.

This technical autonomy boosts bargaining leverage in supplier negotiations, helps preserve gross margins (group 2024 gross margin ~74%), and lowers price and supply risks for key ingredients.

- 2024 R&D: €1.3bn; 21 centers

- In-house actives reduce supplier reliance

- Creates credible backward-integration threat

- Supports ~74% gross margin protection

L'Oréal’s scale, R&D and multi‑sourcing cap supplier power, saving €120–150m/yr

Supplier power is low: L'Oréal’s €10.8bn+ 2024 procurement, 2,000+ suppliers, >40% multi‑sourced commodities, and €1.3bn R&D (21 centres) enable volume discounts (5–15%), multi‑sourcing, co‑investments (42% botanical/biotech via partnerships in 2024) and backward‑integration, capping supplier hold‑up and saving ~€120–150m/year in premiums.

| Metric | 2024 |

|---|---|

| Procurement spend | €10.8bn+ |

| Suppliers | 2,000+ |

| R&D | €1.3bn (21 centres) |

| Biotech partnerships | 42% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier dynamics, substitute threats, and entry barriers in L'Oréal's market, highlighting disruptive forces, pricing power, and strategic protections that shape its profitability and competitive positioning.

Compact Porter's Five Forces for L'Oréal—distills competitive intensity, supplier/buyer power, threat of substitutes and entrants into one slide-ready summary to speed strategic decisions.

Customers Bargaining Power

High Leverage of Global Retail Giants

Low Switching Costs for Individual Consumers

Individual consumers face near-zero financial switching costs when moving from L'Oréal to rivals, so a 2024 Euromonitor estimate showing 12% annual churn in global prestige and mass beauty highlights constant defections.

The market’s 2023-24 flood of launches—over 30,000 SKUs in skin, makeup, hair—keeps loyalty fragile as viral trends shift demand within weeks.

As a result, L'Oréal spent €3.9bn on R&D and marketing in 2024, reflecting necessary continuous investment to defend market share and pricing tiers.

Transparency and Price Sensitivity in E-commerce

By late 2025, e-commerce accounted for ~32% of global beauty sales and widespread price-comparison tools mean consumers find best deals instantly, capping L'Oréal's room for blunt price hikes.

L'Oréal reports 20% of sales tied to online channels and so uses advanced analytics to deliver personalized promos and loyalty rewards, reducing churn from price-sensitive buyers.

Influence of Social Media and Peer Reviews

Modern consumers use social proof, influencers, and reviews more than ads, giving buyers soft power: a viral negative post can dent sales across lines within days.

L'Oréal counters by investing in community engagement and product trials; in 2024 it increased digital spend 18% and cites average 4.4/5 ratings across key third-party retailers.

- Single viral complaint can cut weekly sales by double digits

- L'Oréal 2024 digital spend +18%

- Average ratings ~4.4/5 on major platforms

Demand for Sustainable and Ethical Practices

By 2025, roughly 60% of global consumers prioritize ethical sourcing, vegan formulas, and plastic-free packaging, giving shoppers collective leverage to boycott brands that fail ESG tests.

L'Oréal responds via its L'Oréal for the Future program, pledging 100% biodegradable or refillable packaging by 2030 and reporting a 65% cut in carbon intensity since 2005 to align with buyer demands.

- 60% consumers prefer ethical products (2025)

- Consumers can boycott—raises switching risk

- L'Oréal for the Future: 100% refillable/biodegradable by 2030

- 65% cut carbon intensity since 2005

Retailers Hold the Leverage: L'Oréal €36.5bn Faces Margin Pressure, 32% e‑commerce

Major retailers (Walmart, Sephora, Carrefour) drove ~35% of L'Oréal sales in 2024, giving them strong trade leverage; L'Oréal €36.5bn 2024 revenue means big buyers can press margins. Consumers have near-zero switching costs (Euromonitor 12% churn, prestige+m ass 2024) and e‑commerce ~32% by 2025, forcing continuous €3.9bn R&D/marketing spend and ESG moves (2030 refillable goal).

| Metric | Value |

|---|---|

| 2024 Revenue | €36.5bn |

| Retailer share | ~35% |

| Churn (2024) | 12% |

| R&D & Mktg (2024) | €3.9bn |

| E‑commerce (2025) | ~32% |

Preview Before You Purchase

L'Oréal Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of L'Oréal you'll receive immediately after purchase—no placeholders or mockups; the full, professionally formatted document is ready for download and use the moment you buy.