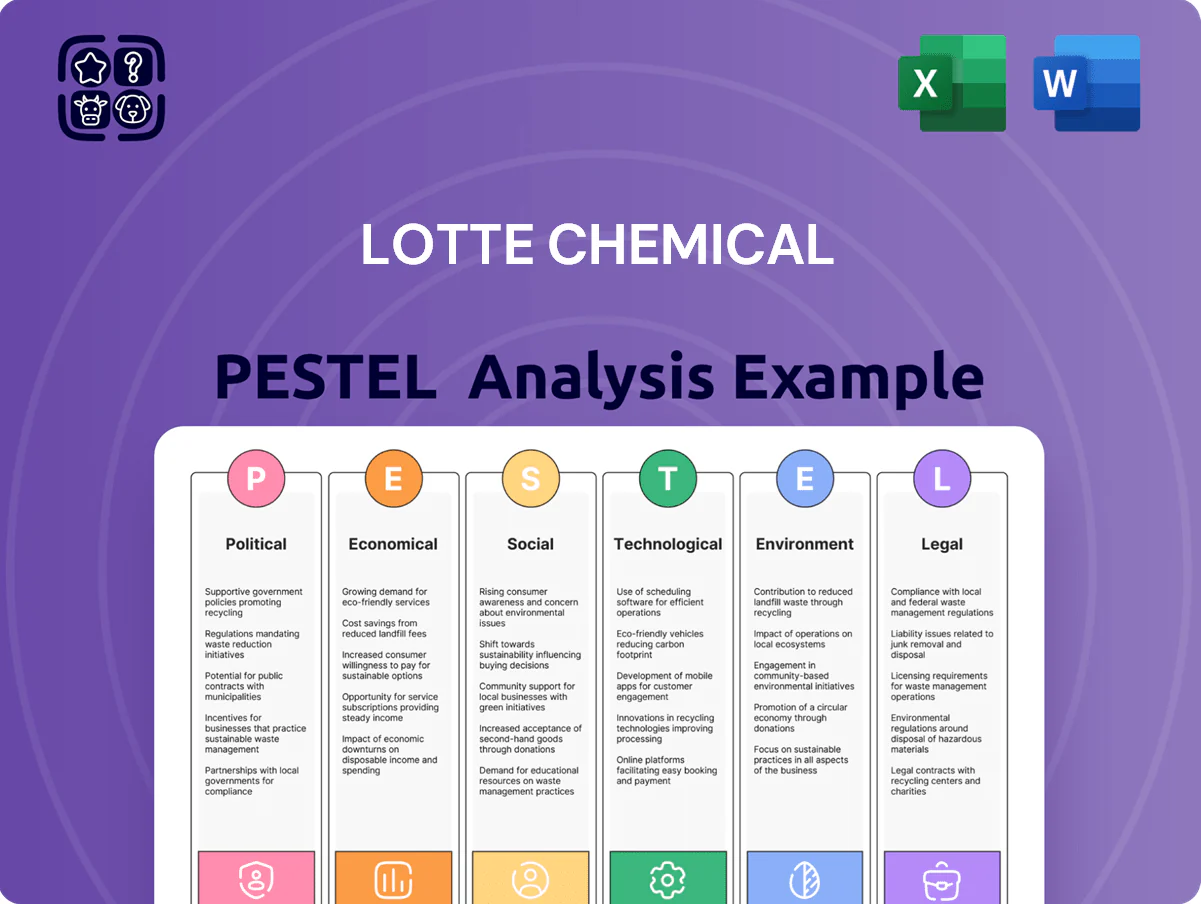

Lotte Chemical PESTLE Analysis

Skip the Research. Get the Strategy.

Navigate the forces shaping Lotte Chemical with our concise PESTLE snapshot—covering regulatory risks, supply‑chain pressures, market demand shifts, and tech-driven efficiency gains to inform smarter decisions. Purchase the full PESTLE for a detailed, ready‑to‑use report that equips investors and strategists with actionable insights and downloadable Word/Excel files.

Political factors

Geopolitical Trade Dynamics with China

The 2024 slowdown in South Korea-China trade, with chemical exports to China down about 8% YoY, pressures Lotte Chemical’s export volumes and risks market-share erosion in key segments where China boosted domestic petrochemical capacity by an estimated 5–7 MT in 2023–24.

South Korean Government Hydrogen Roadmap

Lotte Chemical is central to South Korea’s Hydrogen Economy Roadmap to 2030, targeting 6.2 million tons H2 demand by 2030; government subsidies and a 35.4 trillion KRW energy transition fund (2024–2030) support capex for hydrogen production and distribution, enabling Lotte to scale green/ammonia cracking projects and potentially tap into expected H2 market value of ~54 trillion KRW by 2030, reducing fossil-fuel exposure and strengthening energy security.

US Inflation Reduction Act Benefits

Global Trade Protectionism and Tariffs

Rising protectionism in Europe and North America has driven anti-dumping duties and safeguard measures on chemical imports; EU anti-dumping investigations rose 18% in 2023 and US duties on polyethylene imports averaged 12–25% in recent cases.

Lotte Chemical must monitor political shifts that could impose new tariffs on polyethylene and other polymers, potentially cutting export margins by several percentage points and affecting FY2024 export revenue share (~30%).

Strategic diplomacy and localized production—Lotte’s existing US and ASEAN sites—are increasingly necessary to mitigate tariff risk and preserve market access.

- EU investigations +18% (2023)

- US polyethylene duties 12–25%

- Exports ~30% of FY2024 revenue

- Mitigation: diplomacy + local plants

Energy Security and Middle East Stability

Political instability in oil-producing regions raises naphtha costs—naphtha feedstock rose ~38% in 2022 and crude Brent volatility (2022–2024) kept margins pressured, directly impacting Lotte Chemical's cracker economics and EBITDA sensitivity.

The company faces profitability risk from geopolitical conflicts that can spike crude; maintaining diverse political ties and multi-year supply contracts (e.g., long-term LNG/naphtha hedges covering a significant portion of feedstock) is essential to stabilize input costs.

- 2022–2024 Brent volatility elevated feedstock-driven margin risk

- Long-term supply agreements and diversified sourcing reduce exposure

- Geopolitical disruptions can materially affect Lotte Chemical EBITDA through naphtha price swings

Lotte Chemical faces export headwinds as protectionism, feedstock volatility meet green incentives

Trade slowdown with China (-8% chemical exports YoY 2024) and rising protectionism (EU probes +18% 2023; US polyethylene duties 12–25%) threaten Lotte Chemical’s ~30% export revenue; US IRA incentives (up to 30% PTC) support US battery material investments while Korea’s 35.4 trillion KRW energy transition fund and H2 roadmap (6.2Mt demand by 2030) enable hydrogen projects; Brent/naphtha volatility (feedstock +38% in 2022) elevates margin risk.

| Metric | Value |

|---|---|

| China export change 2024 | -8% YoY |

| Exports of revenue | ~30% FY2024 |

| EU investigations 2023 | +18% |

| US PE duties | 12–25% |

| Korean energy fund | 35.4T KRW (2024–2030) |

| H2 demand target 2030 | 6.2Mt |

| Naphtha rise 2022 | +38% |

What is included in the product

Explores how macro-environmental factors uniquely affect Lotte Chemical across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary of Lotte Chemical that’s ready to drop into presentations or strategy packs, easing cross-team alignment and enabling quick updates or localized notes for rapid planning sessions.

Economic factors

Volatility in Global Naphtha and Oil Prices

Lotte Chemical's margins are tightly tied to naphtha, the primary feedstock for steam crackers, which tracked Brent crude swings—Brent averaged ~USD 85/bbl in 2024 and rose to ~USD 92/bbl by Q4 2025—keeping naphtha premiums volatile and compressing upstream EBITDA. Continued 2025 volatility forced expanded hedging: company reports show hedged volumes rose ~20% YoY and feedstock diversification into LPG and recycled feedstocks increased to ~12% of intake. Sudden energy-market shifts can move ethylene/propylene cost curves by several hundred dollars/ton within months, directly affecting Lotte Chemical's basic-chemicals cost structure and cash margins.

Cyclical Nature of the Petrochemical Industry

The petrochemical industry is in a fragile recovery after 2023–24 global oversupply and weak demand; global ethylene margins rebounded to about $250–350/ton in H2 2024 from negative spreads in mid‑2023, but capacity additions keep pressure on prices.

Demand for Lotte Chemical’s polymers and specialty materials is closely tied to construction and auto cycles; global auto production rose ~6% in 2024 to ~83 million units, supporting polymer demand.

Analysts should track the IIP and OECD industrial production—OECD industrial output grew ~2.2% in 2024—to time the next upswing in chemical demand.

Impact of High Interest Rates on Capital Expenditure

Sustained high interest rates through 2025—global policy rates averaging about 4.5–5.0% and South Korea's base rate at 3.5% as of Dec 2025—have raised Lotte Chemical's borrowing costs for large-scale infrastructure and R&D projects.

Expansion into eco-friendly materials and hydrogen, estimated capex needs of $1.2–1.8 billion over 2024–2027, makes higher debt servicing a significant economic burden.

Maintaining a strong balance sheet—net debt/EBITDA targeted below 2.5x—will be crucial for funding long-term initiatives without over-leveraging.

Currency Exchange Rate Fluctuations

As a major exporter, Lotte Chemical is highly sensitive to KRW/USD moves; a 10% Won depreciation in 2023 raised import feedstock costs (naphtha) while boosting export competitiveness, contributing to a 7% swing in EBITDA margins in 2023-24.

A weakening Won increases local costs for imported raw materials but supports dollar-denominated revenue; a strong Won compresses export margins and reduced operating cash flow by about KRW 150–250bn in 2024 FX headwinds.

South Korea financial-market stability—KRW volatility (2024 annualized FX volatility ~8%) and USD liquidity—remains a key determinant of Lotte Chemical’s quarterly earnings and cash-flow predictability.

- KRW/USD sensitivity: ~7% EBITDA margin swing (2023–24)

- 2024 FX volatility: ~8% annualized

- Estimated 2024 FX impact on cash flow: KRW 150–250bn

Emerging Market Growth in Southeast Asia

Economic expansion in Southeast Asia, with IMF 2025 GDP growth forecasts of about 4.5–5.5% for Indonesia, Vietnam and the Philippines, boosts demand for Lotte Chemical's regional hubs like Lotte Chemical Indonesia.

Rising industrialization and per-capita consumption—ASEAN household consumption grew ~6% YoY in 2024—drives packaging, electronics and automotive polymer demand.

Lotte Chemical's earnings are increasingly linked to capturing market share in these high-growth markets; Indonesia accounted for ~12–15% of the company’s Southeast Asia segment revenue in 2024.

- IMF 2025 GDP growth 4.5–5.5% (Indonesia, Vietnam, Philippines)

- ASEAN household consumption +~6% YoY in 2024

- Indonesia ~12–15% of Lotte Chemical SEA segment revenue in 2024

Naphtha margin risk, FX swing KRW150–250bn; Brent 85→92, ethylene $250–350/t

Naphtha-linked margins remain core risk: Brent ~USD 85/bbl (2024) to ~USD 92/bbl (Q4 2025); hedged volumes +20% YoY; ethylene margins ~$250–350/ton H2 2024. KRW/USD moves ~10% drove ~7% EBITDA swing; 2024 FX volatility ~8%; estimated FX cash impact KRW 150–250bn. ASEAN GDP 2025 ~4.5–5.5%; Indonesia ~12–15% SEA revenue (2024).

| Metric | Value |

|---|---|

| Brent (2024–Q4 2025) | 85→92 USD/bbl |

| Hedged volumes | +20% YoY |

| Ethylene margin H2 2024 | 250–350 USD/t |

| KRW vol. 2024 | ~8% ann. |

| FX cash impact 2024 | KRW 150–250bn |

| ASEAN GDP 2025 | 4.5–5.5% |

Same Document Delivered

Lotte Chemical PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Lotte Chemical PESTLE analysis covers political, economic, social, technological, legal, and environmental factors with clear insights and actionable implications. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Navigate the forces shaping Lotte Chemical with our concise PESTLE snapshot—covering regulatory risks, supply‑chain pressures, market demand shifts, and tech-driven efficiency gains to inform smarter decisions. Purchase the full PESTLE for a detailed, ready‑to‑use report that equips investors and strategists with actionable insights and downloadable Word/Excel files.

Political factors

Geopolitical Trade Dynamics with China

The 2024 slowdown in South Korea-China trade, with chemical exports to China down about 8% YoY, pressures Lotte Chemical’s export volumes and risks market-share erosion in key segments where China boosted domestic petrochemical capacity by an estimated 5–7 MT in 2023–24.

South Korean Government Hydrogen Roadmap

Lotte Chemical is central to South Korea’s Hydrogen Economy Roadmap to 2030, targeting 6.2 million tons H2 demand by 2030; government subsidies and a 35.4 trillion KRW energy transition fund (2024–2030) support capex for hydrogen production and distribution, enabling Lotte to scale green/ammonia cracking projects and potentially tap into expected H2 market value of ~54 trillion KRW by 2030, reducing fossil-fuel exposure and strengthening energy security.

US Inflation Reduction Act Benefits

Global Trade Protectionism and Tariffs

Rising protectionism in Europe and North America has driven anti-dumping duties and safeguard measures on chemical imports; EU anti-dumping investigations rose 18% in 2023 and US duties on polyethylene imports averaged 12–25% in recent cases.

Lotte Chemical must monitor political shifts that could impose new tariffs on polyethylene and other polymers, potentially cutting export margins by several percentage points and affecting FY2024 export revenue share (~30%).

Strategic diplomacy and localized production—Lotte’s existing US and ASEAN sites—are increasingly necessary to mitigate tariff risk and preserve market access.

- EU investigations +18% (2023)

- US polyethylene duties 12–25%

- Exports ~30% of FY2024 revenue

- Mitigation: diplomacy + local plants

Energy Security and Middle East Stability

Political instability in oil-producing regions raises naphtha costs—naphtha feedstock rose ~38% in 2022 and crude Brent volatility (2022–2024) kept margins pressured, directly impacting Lotte Chemical's cracker economics and EBITDA sensitivity.

The company faces profitability risk from geopolitical conflicts that can spike crude; maintaining diverse political ties and multi-year supply contracts (e.g., long-term LNG/naphtha hedges covering a significant portion of feedstock) is essential to stabilize input costs.

- 2022–2024 Brent volatility elevated feedstock-driven margin risk

- Long-term supply agreements and diversified sourcing reduce exposure

- Geopolitical disruptions can materially affect Lotte Chemical EBITDA through naphtha price swings

Lotte Chemical faces export headwinds as protectionism, feedstock volatility meet green incentives

Trade slowdown with China (-8% chemical exports YoY 2024) and rising protectionism (EU probes +18% 2023; US polyethylene duties 12–25%) threaten Lotte Chemical’s ~30% export revenue; US IRA incentives (up to 30% PTC) support US battery material investments while Korea’s 35.4 trillion KRW energy transition fund and H2 roadmap (6.2Mt demand by 2030) enable hydrogen projects; Brent/naphtha volatility (feedstock +38% in 2022) elevates margin risk.

| Metric | Value |

|---|---|

| China export change 2024 | -8% YoY |

| Exports of revenue | ~30% FY2024 |

| EU investigations 2023 | +18% |

| US PE duties | 12–25% |

| Korean energy fund | 35.4T KRW (2024–2030) |

| H2 demand target 2030 | 6.2Mt |

| Naphtha rise 2022 | +38% |

What is included in the product

Explores how macro-environmental factors uniquely affect Lotte Chemical across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary of Lotte Chemical that’s ready to drop into presentations or strategy packs, easing cross-team alignment and enabling quick updates or localized notes for rapid planning sessions.

Economic factors

Volatility in Global Naphtha and Oil Prices

Lotte Chemical's margins are tightly tied to naphtha, the primary feedstock for steam crackers, which tracked Brent crude swings—Brent averaged ~USD 85/bbl in 2024 and rose to ~USD 92/bbl by Q4 2025—keeping naphtha premiums volatile and compressing upstream EBITDA. Continued 2025 volatility forced expanded hedging: company reports show hedged volumes rose ~20% YoY and feedstock diversification into LPG and recycled feedstocks increased to ~12% of intake. Sudden energy-market shifts can move ethylene/propylene cost curves by several hundred dollars/ton within months, directly affecting Lotte Chemical's basic-chemicals cost structure and cash margins.

Cyclical Nature of the Petrochemical Industry

The petrochemical industry is in a fragile recovery after 2023–24 global oversupply and weak demand; global ethylene margins rebounded to about $250–350/ton in H2 2024 from negative spreads in mid‑2023, but capacity additions keep pressure on prices.

Demand for Lotte Chemical’s polymers and specialty materials is closely tied to construction and auto cycles; global auto production rose ~6% in 2024 to ~83 million units, supporting polymer demand.

Analysts should track the IIP and OECD industrial production—OECD industrial output grew ~2.2% in 2024—to time the next upswing in chemical demand.

Impact of High Interest Rates on Capital Expenditure

Sustained high interest rates through 2025—global policy rates averaging about 4.5–5.0% and South Korea's base rate at 3.5% as of Dec 2025—have raised Lotte Chemical's borrowing costs for large-scale infrastructure and R&D projects.

Expansion into eco-friendly materials and hydrogen, estimated capex needs of $1.2–1.8 billion over 2024–2027, makes higher debt servicing a significant economic burden.

Maintaining a strong balance sheet—net debt/EBITDA targeted below 2.5x—will be crucial for funding long-term initiatives without over-leveraging.

Currency Exchange Rate Fluctuations

As a major exporter, Lotte Chemical is highly sensitive to KRW/USD moves; a 10% Won depreciation in 2023 raised import feedstock costs (naphtha) while boosting export competitiveness, contributing to a 7% swing in EBITDA margins in 2023-24.

A weakening Won increases local costs for imported raw materials but supports dollar-denominated revenue; a strong Won compresses export margins and reduced operating cash flow by about KRW 150–250bn in 2024 FX headwinds.

South Korea financial-market stability—KRW volatility (2024 annualized FX volatility ~8%) and USD liquidity—remains a key determinant of Lotte Chemical’s quarterly earnings and cash-flow predictability.

- KRW/USD sensitivity: ~7% EBITDA margin swing (2023–24)

- 2024 FX volatility: ~8% annualized

- Estimated 2024 FX impact on cash flow: KRW 150–250bn

Emerging Market Growth in Southeast Asia

Economic expansion in Southeast Asia, with IMF 2025 GDP growth forecasts of about 4.5–5.5% for Indonesia, Vietnam and the Philippines, boosts demand for Lotte Chemical's regional hubs like Lotte Chemical Indonesia.

Rising industrialization and per-capita consumption—ASEAN household consumption grew ~6% YoY in 2024—drives packaging, electronics and automotive polymer demand.

Lotte Chemical's earnings are increasingly linked to capturing market share in these high-growth markets; Indonesia accounted for ~12–15% of the company’s Southeast Asia segment revenue in 2024.

- IMF 2025 GDP growth 4.5–5.5% (Indonesia, Vietnam, Philippines)

- ASEAN household consumption +~6% YoY in 2024

- Indonesia ~12–15% of Lotte Chemical SEA segment revenue in 2024

Naphtha margin risk, FX swing KRW150–250bn; Brent 85→92, ethylene $250–350/t

Naphtha-linked margins remain core risk: Brent ~USD 85/bbl (2024) to ~USD 92/bbl (Q4 2025); hedged volumes +20% YoY; ethylene margins ~$250–350/ton H2 2024. KRW/USD moves ~10% drove ~7% EBITDA swing; 2024 FX volatility ~8%; estimated FX cash impact KRW 150–250bn. ASEAN GDP 2025 ~4.5–5.5%; Indonesia ~12–15% SEA revenue (2024).

| Metric | Value |

|---|---|

| Brent (2024–Q4 2025) | 85→92 USD/bbl |

| Hedged volumes | +20% YoY |

| Ethylene margin H2 2024 | 250–350 USD/t |

| KRW vol. 2024 | ~8% ann. |

| FX cash impact 2024 | KRW 150–250bn |

| ASEAN GDP 2025 | 4.5–5.5% |

Same Document Delivered

Lotte Chemical PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Lotte Chemical PESTLE analysis covers political, economic, social, technological, legal, and environmental factors with clear insights and actionable implications. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase.