Loxam PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and evolving tech trends shape Loxam’s strategic position—our concise PESTLE preview highlights key external risks and opportunities to inform your next move. Purchase the full PESTLE to access in-depth, ready-to-use analysis—perfect for investors, consultants, and planners seeking actionable intelligence and editable deliverables. Get the complete report now and make smarter, faster decisions.

Political factors

EU Infrastructure Stimulus Programs

The continued rollout of NextGenerationEU funds, with €806.9bn in grants and loans of which member states had committed over €450bn by end-2024, sustains construction demand through 2025 and boosts Loxam’s heavy-equipment rental for transport and energy-transition projects.

Major public works in France and Germany, supported by national recovery plans that channel billions into rail, road and renewable infrastructure, create high-margin rental opportunities for Loxam on large-scale contracts.

Government stability in core markets—France’s 2024 budget continuity and Germany’s coalition commitment to infrastructure spending—underpins the multi-year project pipeline that drives Loxam’s fleet utilization and revenue visibility.

Geopolitical Trade Relations

Trade tensions and EU tariffs on non-EU heavy machinery—up to 10–15% on certain imports in 2024—could raise Loxam’s fleet renewal costs, given capex for equipment reached €680m in 2023. As a global renter, Loxam faces supply-chain exposure: 40% of specialized parts sourced outside the EU in 2024, making shifting trade policies a cost and lead-time risk.

Political stability in markets like Brazil and parts of the Middle East affects regional investment: Brazil’s construction output fell 3.5% in 2024 vs 2023, prompting cautious local deployment, while Gulf infrastructure spending projections for 2025–26 buoy selective expansion decisions.

Public Sector Housing Policies

Government mandates to tackle housing shortages via subsidized residential construction have driven a 12% rise in rental demand for earthmoving and lifting equipment in France in 2024, directly benefiting Loxam’s revenues (equipment rental market ≈ €8.5bn in 2024).

Shifts in political leadership can change zoning and permitting—France saw municipal zoning reforms in 2023 that accelerated approvals by 15%, creating short-term spikes or delays in rental cycles affecting branch utilization.

Loxam actively monitors local policy changes and adjusted its branch network in 2024, reallocating assets to high-growth regions such as Île-de-France and Occitanie where construction starts grew 10–18%, optimizing fleet deployment and utilization rates.

Labor Union Dynamics in Europe

- Union wage premium 10–15%

- Union density 20–30% (France/UK)

- 11,000+ employees across 30 countries

- EU 2024 proposals tighten temporary worker protections

Green Public Procurement Mandates

Governments now embed strict environmental criteria in public tenders for infrastructure, with the EU Green Public Procurement target aiming for 50% of public procurement to be green by 2025 and France’s 2024 building tenders requiring low-emission equipment; this pressures rental firms like Loxam to shift fleets toward electric/zero-emission units.

Failing to comply risks losing state-funded contracts—public sector clients represented about 22% of European construction procurement in 2023—so Loxam must accelerate capex for low-emission assets to stay competitive.

- EU target: 50% green procurement by 2025

- Public sector ≈22% of EU construction spend (2023)

- Loxam fleet electrification capex needed to meet mandates

Loxam faces €100sM electrification capex, tariff & supply‑chain risk as EU green rules bite

Political drivers—NextGenerationEU (€806.9bn, €450bn committed by end‑2024), national infrastructure budgets, green procurement targets (EU 50% by 2025), and tighter labor/temporary‑worker rules—raise demand and compliance costs for Loxam, requiring €hundreds of millions in electrification capex while exposing fleet renewal to 10–15% import tariffs and 40% non‑EU parts supply risk.

| Metric | Value |

|---|---|

| NextGenerationEU | €806.9bn (€450bn committed) |

| Public procurement green target | 50% by 2025 |

| Import tariffs (selected) | 10–15% |

| Non‑EU parts | 40% |

| Loxam employees/markets | 11,000+/30 countries |

What is included in the product

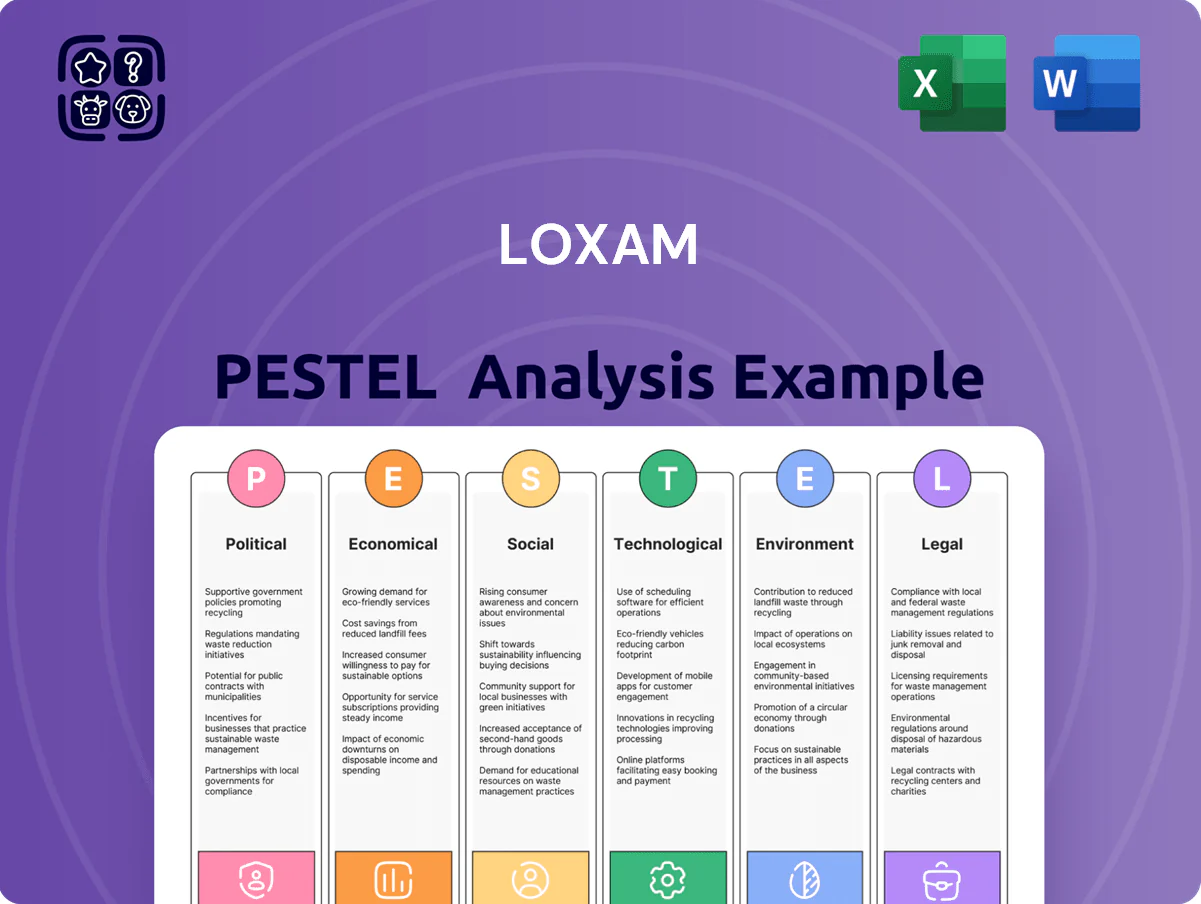

Explores how external macro-environmental factors uniquely affect Loxam across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to highlight specific risks and opportunities for the equipment rental leader.

Summarized PESTLE insights for Loxam, organized by category for quick reference, easily dropped into presentations or shared across teams to streamline external risk discussions and strategic planning.

Economic factors

Interest Rate and Financing Costs

As of late 2025 Loxam faces higher servicing costs after ECB rates rose to around 4.0%–4.5%, increasing annual interest expense on its ~€1.6bn debt and compressing 2025 EBITDA margins by an estimated 70–120 basis points versus 2023.

Elevated rates also raise the hurdle for fleet expansion, with lease and acquisition financing costs up ~1.5–2.0 percentage points since 2022, slowing capex-backed M&A.

Stabilization of rates at current levels would restore predictability, aiding five-year fleet planning and enabling targeted investment in higher-margin equipment categories.

Shift from CAPEX to OPEX

Economic uncertainty and rising inflation have driven clients toward rental models to preserve cash and flexibility, supporting Loxam’s shift from CAPEX to OPEX; in 2024 the European equipment rental penetration reached ~9–10% (vs ~6–7% a decade ago), and industry forecasts project CAGR ~6–8% through 2028, providing a steady tailwind as customers avoid upfront purchase and escalating ownership and maintenance costs.

Inflationary Pressure on Maintenance

Rising costs for spare parts, specialized labor and energy increased Loxam’s maintenance expense pressure in 2024, with European diesel prices up ~18% YoY and EU producer price inflation averaging 7% in 2024, squeezing margins on lower-yield rentals.

Loxam faces a trade-off: passing costs via higher rental rates risks share loss to local independents—industry price elasticity estimates suggest a 3–5% volume drop for a 5% price rise in some markets.

Effective supply-chain management and bulk purchasing remain key moats: Loxam’s scale-enabled fleet procurement and centralized parts sourcing aimed to reduce unit maintenance cost by an estimated 6–8% in 2024 versus smaller peers.

European GDP and Construction Output

Loxam’s revenue is highly tied to Eurozone GDP; 2024 Eurozone GDP growth was 0.6% (IMF 2025 WEO), and slower growth drove weaker demand for heavy construction rentals in H1 2024, lowering fleet utilization to ~72% in parts of Western Europe.

To offset cyclicality, Loxam serves events, landscaping, and green infrastructure—sectors that grew ~3–5% in 2023–24—helping stabilize revenue and reduce sensitivity to construction downturns.

- Eurozone GDP growth 2024: ~0.6%

- Construction output weakness cut utilization to ~72%

- Events/green sectors growing 3–5% (2023–24)

Currency Exchange Rate Volatility

Currency exchange rate volatility materially affects Loxam, which reported 2024 pro forma revenue of about €4.8bn; movements in GBP, BRL and other currencies can swing consolidated results by several percentage points—e.g., a 5% depreciation in GBP versus EUR could reduce translated revenue by ~€50–€100m on an annualized basis.

Volatility also revalues international assets and raises import costs for machinery—Brazilian Real fell ~8% vs EUR in 2024, increasing local equipment costs—so hedging (forwards/options) and driving localized revenue streams are essential risk mitigants.

- ~€4.8bn 2024 pro forma revenue exposure

- 5% FX move ≈ €50–€100m impact

- BRL ~8% weaker vs EUR in 2024 raises import costs

- Hedging and local revenue reduce macro FX risk

Loxam hit by higher ECB rates and FX, trimming margins despite rental growth

Higher ECB rates (~4.0–4.5% in 2025) raised interest on Loxam’s ~€1.6bn debt, shaving ~70–120bps off 2025 EBITDA margins; 2024 pro forma revenue ~€4.8bn. Rental penetration rose to ~9–10% in 2024 with industry CAGR ~6–8% to 2028, offsetting weaker construction (Eurozone GDP 2024 ~0.6%, utilization ~72%). FX moves (5% ≈ €50–€100m) and 2024 BRL ≈-8% vs EUR amplify cost and translation risk.

| Metric | Value |

|---|---|

| Pro forma revenue 2024 | €4.8bn |

| Debt | ~€1.6bn |

| ECB rate (2025) | ~4.0–4.5% |

| Eurozone GDP 2024 | ~0.6% |

| Utilization (W. Europe H1 2024) | ~72% |

| Rental penetration 2024 | ~9–10% |

| FX sensitivity | 5% ≈ €50–€100m |

| BRL vs EUR 2024 | ≈-8% |

What You See Is What You Get

Loxam PESTLE Analysis

The preview shown here is the exact Loxam PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and evolving tech trends shape Loxam’s strategic position—our concise PESTLE preview highlights key external risks and opportunities to inform your next move. Purchase the full PESTLE to access in-depth, ready-to-use analysis—perfect for investors, consultants, and planners seeking actionable intelligence and editable deliverables. Get the complete report now and make smarter, faster decisions.

Political factors

EU Infrastructure Stimulus Programs

The continued rollout of NextGenerationEU funds, with €806.9bn in grants and loans of which member states had committed over €450bn by end-2024, sustains construction demand through 2025 and boosts Loxam’s heavy-equipment rental for transport and energy-transition projects.

Major public works in France and Germany, supported by national recovery plans that channel billions into rail, road and renewable infrastructure, create high-margin rental opportunities for Loxam on large-scale contracts.

Government stability in core markets—France’s 2024 budget continuity and Germany’s coalition commitment to infrastructure spending—underpins the multi-year project pipeline that drives Loxam’s fleet utilization and revenue visibility.

Geopolitical Trade Relations

Trade tensions and EU tariffs on non-EU heavy machinery—up to 10–15% on certain imports in 2024—could raise Loxam’s fleet renewal costs, given capex for equipment reached €680m in 2023. As a global renter, Loxam faces supply-chain exposure: 40% of specialized parts sourced outside the EU in 2024, making shifting trade policies a cost and lead-time risk.

Political stability in markets like Brazil and parts of the Middle East affects regional investment: Brazil’s construction output fell 3.5% in 2024 vs 2023, prompting cautious local deployment, while Gulf infrastructure spending projections for 2025–26 buoy selective expansion decisions.

Public Sector Housing Policies

Government mandates to tackle housing shortages via subsidized residential construction have driven a 12% rise in rental demand for earthmoving and lifting equipment in France in 2024, directly benefiting Loxam’s revenues (equipment rental market ≈ €8.5bn in 2024).

Shifts in political leadership can change zoning and permitting—France saw municipal zoning reforms in 2023 that accelerated approvals by 15%, creating short-term spikes or delays in rental cycles affecting branch utilization.

Loxam actively monitors local policy changes and adjusted its branch network in 2024, reallocating assets to high-growth regions such as Île-de-France and Occitanie where construction starts grew 10–18%, optimizing fleet deployment and utilization rates.

Labor Union Dynamics in Europe

- Union wage premium 10–15%

- Union density 20–30% (France/UK)

- 11,000+ employees across 30 countries

- EU 2024 proposals tighten temporary worker protections

Green Public Procurement Mandates

Governments now embed strict environmental criteria in public tenders for infrastructure, with the EU Green Public Procurement target aiming for 50% of public procurement to be green by 2025 and France’s 2024 building tenders requiring low-emission equipment; this pressures rental firms like Loxam to shift fleets toward electric/zero-emission units.

Failing to comply risks losing state-funded contracts—public sector clients represented about 22% of European construction procurement in 2023—so Loxam must accelerate capex for low-emission assets to stay competitive.

- EU target: 50% green procurement by 2025

- Public sector ≈22% of EU construction spend (2023)

- Loxam fleet electrification capex needed to meet mandates

Loxam faces €100sM electrification capex, tariff & supply‑chain risk as EU green rules bite

Political drivers—NextGenerationEU (€806.9bn, €450bn committed by end‑2024), national infrastructure budgets, green procurement targets (EU 50% by 2025), and tighter labor/temporary‑worker rules—raise demand and compliance costs for Loxam, requiring €hundreds of millions in electrification capex while exposing fleet renewal to 10–15% import tariffs and 40% non‑EU parts supply risk.

| Metric | Value |

|---|---|

| NextGenerationEU | €806.9bn (€450bn committed) |

| Public procurement green target | 50% by 2025 |

| Import tariffs (selected) | 10–15% |

| Non‑EU parts | 40% |

| Loxam employees/markets | 11,000+/30 countries |

What is included in the product

Explores how external macro-environmental factors uniquely affect Loxam across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to highlight specific risks and opportunities for the equipment rental leader.

Summarized PESTLE insights for Loxam, organized by category for quick reference, easily dropped into presentations or shared across teams to streamline external risk discussions and strategic planning.

Economic factors

Interest Rate and Financing Costs

As of late 2025 Loxam faces higher servicing costs after ECB rates rose to around 4.0%–4.5%, increasing annual interest expense on its ~€1.6bn debt and compressing 2025 EBITDA margins by an estimated 70–120 basis points versus 2023.

Elevated rates also raise the hurdle for fleet expansion, with lease and acquisition financing costs up ~1.5–2.0 percentage points since 2022, slowing capex-backed M&A.

Stabilization of rates at current levels would restore predictability, aiding five-year fleet planning and enabling targeted investment in higher-margin equipment categories.

Shift from CAPEX to OPEX

Economic uncertainty and rising inflation have driven clients toward rental models to preserve cash and flexibility, supporting Loxam’s shift from CAPEX to OPEX; in 2024 the European equipment rental penetration reached ~9–10% (vs ~6–7% a decade ago), and industry forecasts project CAGR ~6–8% through 2028, providing a steady tailwind as customers avoid upfront purchase and escalating ownership and maintenance costs.

Inflationary Pressure on Maintenance

Rising costs for spare parts, specialized labor and energy increased Loxam’s maintenance expense pressure in 2024, with European diesel prices up ~18% YoY and EU producer price inflation averaging 7% in 2024, squeezing margins on lower-yield rentals.

Loxam faces a trade-off: passing costs via higher rental rates risks share loss to local independents—industry price elasticity estimates suggest a 3–5% volume drop for a 5% price rise in some markets.

Effective supply-chain management and bulk purchasing remain key moats: Loxam’s scale-enabled fleet procurement and centralized parts sourcing aimed to reduce unit maintenance cost by an estimated 6–8% in 2024 versus smaller peers.

European GDP and Construction Output

Loxam’s revenue is highly tied to Eurozone GDP; 2024 Eurozone GDP growth was 0.6% (IMF 2025 WEO), and slower growth drove weaker demand for heavy construction rentals in H1 2024, lowering fleet utilization to ~72% in parts of Western Europe.

To offset cyclicality, Loxam serves events, landscaping, and green infrastructure—sectors that grew ~3–5% in 2023–24—helping stabilize revenue and reduce sensitivity to construction downturns.

- Eurozone GDP growth 2024: ~0.6%

- Construction output weakness cut utilization to ~72%

- Events/green sectors growing 3–5% (2023–24)

Currency Exchange Rate Volatility

Currency exchange rate volatility materially affects Loxam, which reported 2024 pro forma revenue of about €4.8bn; movements in GBP, BRL and other currencies can swing consolidated results by several percentage points—e.g., a 5% depreciation in GBP versus EUR could reduce translated revenue by ~€50–€100m on an annualized basis.

Volatility also revalues international assets and raises import costs for machinery—Brazilian Real fell ~8% vs EUR in 2024, increasing local equipment costs—so hedging (forwards/options) and driving localized revenue streams are essential risk mitigants.

- ~€4.8bn 2024 pro forma revenue exposure

- 5% FX move ≈ €50–€100m impact

- BRL ~8% weaker vs EUR in 2024 raises import costs

- Hedging and local revenue reduce macro FX risk

Loxam hit by higher ECB rates and FX, trimming margins despite rental growth

Higher ECB rates (~4.0–4.5% in 2025) raised interest on Loxam’s ~€1.6bn debt, shaving ~70–120bps off 2025 EBITDA margins; 2024 pro forma revenue ~€4.8bn. Rental penetration rose to ~9–10% in 2024 with industry CAGR ~6–8% to 2028, offsetting weaker construction (Eurozone GDP 2024 ~0.6%, utilization ~72%). FX moves (5% ≈ €50–€100m) and 2024 BRL ≈-8% vs EUR amplify cost and translation risk.

| Metric | Value |

|---|---|

| Pro forma revenue 2024 | €4.8bn |

| Debt | ~€1.6bn |

| ECB rate (2025) | ~4.0–4.5% |

| Eurozone GDP 2024 | ~0.6% |

| Utilization (W. Europe H1 2024) | ~72% |

| Rental penetration 2024 | ~9–10% |

| FX sensitivity | 5% ≈ €50–€100m |

| BRL vs EUR 2024 | ≈-8% |

What You See Is What You Get

Loxam PESTLE Analysis

The preview shown here is the exact Loxam PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.