LSB Industries Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore LSB Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Natural Gas Feedstock

Natural gas is LSB Industries’ largest raw-material cost, often >50% of production expenses; US Henry Hub prices rose 35% in 2023-24, squeezing margins.

Suppliers thus exert strong bargaining power since regional pipeline constraints and global LNG flows set spot prices beyond LSB’s control.

LSB hedges via futures and swaps covering ~60% of expected 12‑month demand, lowering but not removing exposure to sudden price spikes.

Geographic Dependency on Pipeline Infrastructure

LSB’s raw-materials delivery relies on a few central/southern US pipeline networks, giving pipeline operators leverage since switching to trucking raises transport costs by 2–5x; trucking adds ~$25–$75/ton vs pipeline rates near $12–$30/ton (2024 regional data).

That geographic concentration means a local pipeline outage or a 10–20% tariff hike would directly lift LSB’s COGS and compress margins, so midstream utilities hold strong bargaining power due to limited alternatives.

Concentration of Specialized Catalyst Providers

The chemical synthesis of ammonia and nitric acid depends on specialized catalysts and proprietary tech from a few global firms; roughly 70–80% of high-performance catalysts for these processes come from three major suppliers as of 2025. LSB Industries must keep long-term contracts to secure optimal yields and meet OSHA and EPA safety standards, since supplier switching raises downtime and costs. This supplier concentration limits LSB’s bargaining power, keeping price and service negotiation weak and capex/maintenance margins pressured. Continued reliance increases operational and regulatory risk if a key vendor fails.

Logistics and Rail Transport Monopolies

Shipping bulky chemical and fertilizer products forces heavy reliance on Class I railroads; North American rail consolidation means LSB Industries (LSB) often has only one or two viable carriers per plant, boosting supplier leverage.

Rail providers set freight rates and schedules—key drivers of delivered cost—and reported combined market share of the top four Class I rails exceeded 80% in 2024, strengthening their pricing power over LSB.

The scarcity of alternative transport (limited barge/short‑haul options) magnifies rail bargaining power, making freight rate moves directly material to LSB’s margins and SG&A.

- High dependence on Class I rails

- Top‑4 rails >80% market share (2024)

- Only 1–2 carrier options per plant

- Freight rates/schedules drive delivered cost

Energy Intensity and Utility Reliance

LSB’s plants are heavy electricity and water users supplied by local regulated monopolies, leaving the company almost unable to switch providers after site selection; in 2024 US industrial electricity prices averaged about 11.7 cents/kWh, raising exposure to regional rate changes.

Utility commission-approved rate hikes pass straight to LSB as higher fixed production costs with no competitive alternative, so utilities exert steady supplier power over margins.

That structural dependency keeps suppliers influential: a 10% regional utility rate rise can add materially to unit costs and compress EBITDA unless passed to customers.

- Large, fixed utility demand; limited supplier choice

- 2024 US industrial power ≈11.7 cents/kWh

- Rate hikes increase fixed costs, squeeze margins

- 10% tariff rise = notable EBITDA pressure

Suppliers Dominate Costs: Gas, pipelines & rails concentrate pricing power

Suppliers hold strong bargaining power: natural gas >50% of costs with Henry Hub +35% in 2023‑24; ~60% hedged for 12 months; pipelines concentrated regionally (truck cost 2–5x; pipeline $12–$30/ton vs truck $25–$75/ton); catalysts 70–80% from three suppliers (2025); top‑4 Class I rails >80% share (2024); US industrial power ~11.7¢/kWh (2024).

| Input | Key metric |

|---|---|

| Natural gas | >50% costs; HH +35% (2023‑24) |

| Hedging | ~60% 12‑month cover |

| Pipelines vs truck | Pipeline $12–$30/ton; Truck $25–$75/ton |

| Catalysts | 70–80% from 3 suppliers (2025) |

| Rail | Top‑4 >80% market share (2024) |

| Power | 11.7¢/kWh US industrial (2024) |

What is included in the product

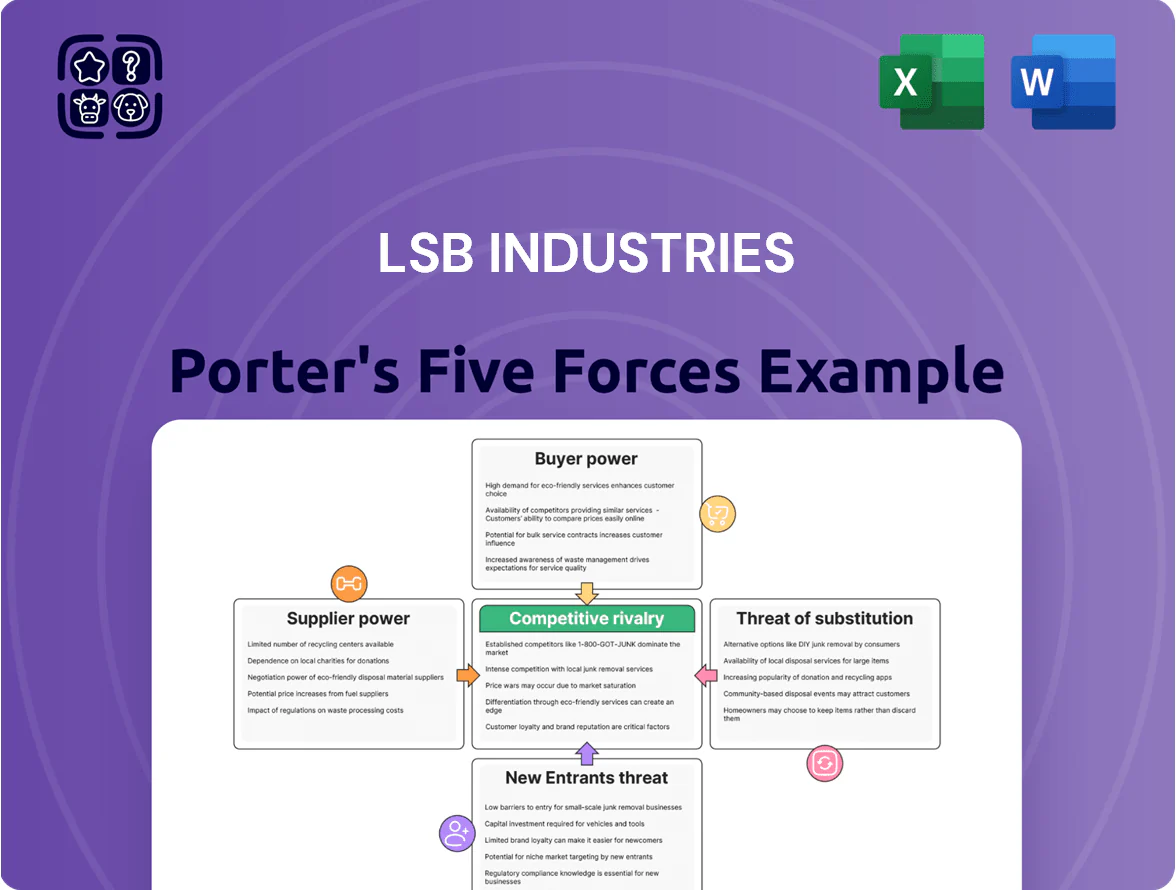

Tailored Porter's Five Forces analysis for LSB Industries uncovering competitive drivers, supplier and buyer bargaining power, threat of new entrants and substitutes, and strategic barriers protecting its market position.

Clear, one-sheet Porter's Five Forces for LSB Industries—quickly assess supplier power, buyer dynamics, substitutes, entry threats, and competitive rivalry to speed strategic decisions and investor briefings.

Customers Bargaining Power

Commodity Nature of Nitrogen Products

Most of LSB Industries' fertilizers and nitrogen-based chemicals are undifferentiated commodities meeting standard specs, so buyers view products from different makers as interchangeable and switch on price alone.

Market transparency—US ammonium nitrate and UAN spot prices fell ~18% in 2024 vs 2023—limits brand premium in agriculture, forcing LSB to compete on cost.

Thus LSB must stay a low-cost producer to retain price-sensitive customers and protect margins.

Concentration of Large Industrial and Mining Buyers

A large share of LSB Industries’ 2024 industrial revenue—about 60% per company filings—comes from a handful of mining and explosives firms, concentrating buying power. These high-volume customers can demand steep discounts and contract concessions, squeezing LSB’s gross margins (LSB reported a 2024 adjusted gross margin near 18%).

If a single major buyer shifts suppliers, LSB’s plant utilization could drop by double digits, hurting fixed-cost absorption and EBITDA. This concentration lets buyers push prices down and lengthen payment terms.

Consolidation of Agricultural Distributors

The agricultural market is now concentrated: the top 10 U.S. cooperatives and retail chains buy roughly 40–50% of fertilizer tonnage, giving them scale to pit nitrogen producers against each other during planting season.

These intermediaries secure volume discounts often 5–15% below spot and extend favorable credit terms—sharply reducing margins for smaller suppliers and forcing producers to accept lower prices.

For LSB Industries, this means its sales team must negotiate with a few powerful gatekeepers who control farmer access, so account-level pricing and credit strategy are decisive for maintaining volumes and margins.

Global Price Transparency and Benchmarking

Customers access real-time global benchmarks for ammonia, UAN, and urea (Platts, Argus), so LSB Industries cannot conceal price hikes; 2025 CFR ammonia spot prices averaged about $650–$900/ton, making deviations obvious.

Buyers track natural gas-to-fertilizer pass-through—US Henry Hub at ~$3.50–4.50/MMBtu in 2025 links directly to production costs—letting them resist increases during negotiations.

Information symmetry lets buyers delay purchases when global prices fall; spot-to-contract spreads tightened to ~5–8% in 2025, capping opportunistic pricing in tight markets.

- Real-time benchmarks expose price moves

- Gas-price transparency strengthens buyer leverage

- Buyers can delay purchases to wait out drops

- Spot-contract spreads (~5–8% in 2025) limit opportunism

Seasonality and Timing of Agricultural Demand

Seasonal fertilizer demand lets large buyers time purchases to press LSB for discounts; US spring planting drives ~60% of annual ammonia sales into March–May, concentrating buying power.

If distributors hold high post-season inventories, they can wait for producers to cut prices; conversely, peak-season urgency lets loyal buyers secure prioritized supply versus smaller customers.

This cyclicality lets sophisticated buyers exploit LSB’s need for steady plant runs and inventory turnover, raising price and volume negotiation leverage.

- Spring (Mar–May) ≈ 60% demand

- High end-season stock → forced price cuts

- Peak-season loyalty → guaranteed allocation

- Continuous ops pressure → stronger buyer leverage

Concentrated buyers squeeze LSB: 40–50% demand concentration, margins at 18%

Buyers hold strong leverage: commodity nature, market transparency, and concentrated purchases (top 10 buyers ~40–50% of tonnage; LSB 2024 industrial revenue ~60% from few firms) force price and credit concessions, pressuring LSB’s 2024 adjusted gross margin ~18% and risking double-digit utilization drops if large accounts switch.

| Metric | Value |

|---|---|

| Top buyers share | 40–50% |

| LSB industrial rev from few firms (2024) | ~60% |

| LSB adj. gross margin (2024) | ~18% |

| Spring demand | ~60% |

Preview the Actual Deliverable

LSB Industries Porter's Five Forces Analysis

This preview shows the exact LSB Industries Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with concise, data-driven insights. It's the same professionally formatted document ready for instant download and use upon payment. No mockups or samples—this is the final deliverable.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore LSB Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Natural Gas Feedstock

Natural gas is LSB Industries’ largest raw-material cost, often >50% of production expenses; US Henry Hub prices rose 35% in 2023-24, squeezing margins.

Suppliers thus exert strong bargaining power since regional pipeline constraints and global LNG flows set spot prices beyond LSB’s control.

LSB hedges via futures and swaps covering ~60% of expected 12‑month demand, lowering but not removing exposure to sudden price spikes.

Geographic Dependency on Pipeline Infrastructure

LSB’s raw-materials delivery relies on a few central/southern US pipeline networks, giving pipeline operators leverage since switching to trucking raises transport costs by 2–5x; trucking adds ~$25–$75/ton vs pipeline rates near $12–$30/ton (2024 regional data).

That geographic concentration means a local pipeline outage or a 10–20% tariff hike would directly lift LSB’s COGS and compress margins, so midstream utilities hold strong bargaining power due to limited alternatives.

Concentration of Specialized Catalyst Providers

The chemical synthesis of ammonia and nitric acid depends on specialized catalysts and proprietary tech from a few global firms; roughly 70–80% of high-performance catalysts for these processes come from three major suppliers as of 2025. LSB Industries must keep long-term contracts to secure optimal yields and meet OSHA and EPA safety standards, since supplier switching raises downtime and costs. This supplier concentration limits LSB’s bargaining power, keeping price and service negotiation weak and capex/maintenance margins pressured. Continued reliance increases operational and regulatory risk if a key vendor fails.

Logistics and Rail Transport Monopolies

Shipping bulky chemical and fertilizer products forces heavy reliance on Class I railroads; North American rail consolidation means LSB Industries (LSB) often has only one or two viable carriers per plant, boosting supplier leverage.

Rail providers set freight rates and schedules—key drivers of delivered cost—and reported combined market share of the top four Class I rails exceeded 80% in 2024, strengthening their pricing power over LSB.

The scarcity of alternative transport (limited barge/short‑haul options) magnifies rail bargaining power, making freight rate moves directly material to LSB’s margins and SG&A.

- High dependence on Class I rails

- Top‑4 rails >80% market share (2024)

- Only 1–2 carrier options per plant

- Freight rates/schedules drive delivered cost

Energy Intensity and Utility Reliance

LSB’s plants are heavy electricity and water users supplied by local regulated monopolies, leaving the company almost unable to switch providers after site selection; in 2024 US industrial electricity prices averaged about 11.7 cents/kWh, raising exposure to regional rate changes.

Utility commission-approved rate hikes pass straight to LSB as higher fixed production costs with no competitive alternative, so utilities exert steady supplier power over margins.

That structural dependency keeps suppliers influential: a 10% regional utility rate rise can add materially to unit costs and compress EBITDA unless passed to customers.

- Large, fixed utility demand; limited supplier choice

- 2024 US industrial power ≈11.7 cents/kWh

- Rate hikes increase fixed costs, squeeze margins

- 10% tariff rise = notable EBITDA pressure

Suppliers Dominate Costs: Gas, pipelines & rails concentrate pricing power

Suppliers hold strong bargaining power: natural gas >50% of costs with Henry Hub +35% in 2023‑24; ~60% hedged for 12 months; pipelines concentrated regionally (truck cost 2–5x; pipeline $12–$30/ton vs truck $25–$75/ton); catalysts 70–80% from three suppliers (2025); top‑4 Class I rails >80% share (2024); US industrial power ~11.7¢/kWh (2024).

| Input | Key metric |

|---|---|

| Natural gas | >50% costs; HH +35% (2023‑24) |

| Hedging | ~60% 12‑month cover |

| Pipelines vs truck | Pipeline $12–$30/ton; Truck $25–$75/ton |

| Catalysts | 70–80% from 3 suppliers (2025) |

| Rail | Top‑4 >80% market share (2024) |

| Power | 11.7¢/kWh US industrial (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for LSB Industries uncovering competitive drivers, supplier and buyer bargaining power, threat of new entrants and substitutes, and strategic barriers protecting its market position.

Clear, one-sheet Porter's Five Forces for LSB Industries—quickly assess supplier power, buyer dynamics, substitutes, entry threats, and competitive rivalry to speed strategic decisions and investor briefings.

Customers Bargaining Power

Commodity Nature of Nitrogen Products

Most of LSB Industries' fertilizers and nitrogen-based chemicals are undifferentiated commodities meeting standard specs, so buyers view products from different makers as interchangeable and switch on price alone.

Market transparency—US ammonium nitrate and UAN spot prices fell ~18% in 2024 vs 2023—limits brand premium in agriculture, forcing LSB to compete on cost.

Thus LSB must stay a low-cost producer to retain price-sensitive customers and protect margins.

Concentration of Large Industrial and Mining Buyers

A large share of LSB Industries’ 2024 industrial revenue—about 60% per company filings—comes from a handful of mining and explosives firms, concentrating buying power. These high-volume customers can demand steep discounts and contract concessions, squeezing LSB’s gross margins (LSB reported a 2024 adjusted gross margin near 18%).

If a single major buyer shifts suppliers, LSB’s plant utilization could drop by double digits, hurting fixed-cost absorption and EBITDA. This concentration lets buyers push prices down and lengthen payment terms.

Consolidation of Agricultural Distributors

The agricultural market is now concentrated: the top 10 U.S. cooperatives and retail chains buy roughly 40–50% of fertilizer tonnage, giving them scale to pit nitrogen producers against each other during planting season.

These intermediaries secure volume discounts often 5–15% below spot and extend favorable credit terms—sharply reducing margins for smaller suppliers and forcing producers to accept lower prices.

For LSB Industries, this means its sales team must negotiate with a few powerful gatekeepers who control farmer access, so account-level pricing and credit strategy are decisive for maintaining volumes and margins.

Global Price Transparency and Benchmarking

Customers access real-time global benchmarks for ammonia, UAN, and urea (Platts, Argus), so LSB Industries cannot conceal price hikes; 2025 CFR ammonia spot prices averaged about $650–$900/ton, making deviations obvious.

Buyers track natural gas-to-fertilizer pass-through—US Henry Hub at ~$3.50–4.50/MMBtu in 2025 links directly to production costs—letting them resist increases during negotiations.

Information symmetry lets buyers delay purchases when global prices fall; spot-to-contract spreads tightened to ~5–8% in 2025, capping opportunistic pricing in tight markets.

- Real-time benchmarks expose price moves

- Gas-price transparency strengthens buyer leverage

- Buyers can delay purchases to wait out drops

- Spot-contract spreads (~5–8% in 2025) limit opportunism

Seasonality and Timing of Agricultural Demand

Seasonal fertilizer demand lets large buyers time purchases to press LSB for discounts; US spring planting drives ~60% of annual ammonia sales into March–May, concentrating buying power.

If distributors hold high post-season inventories, they can wait for producers to cut prices; conversely, peak-season urgency lets loyal buyers secure prioritized supply versus smaller customers.

This cyclicality lets sophisticated buyers exploit LSB’s need for steady plant runs and inventory turnover, raising price and volume negotiation leverage.

- Spring (Mar–May) ≈ 60% demand

- High end-season stock → forced price cuts

- Peak-season loyalty → guaranteed allocation

- Continuous ops pressure → stronger buyer leverage

Concentrated buyers squeeze LSB: 40–50% demand concentration, margins at 18%

Buyers hold strong leverage: commodity nature, market transparency, and concentrated purchases (top 10 buyers ~40–50% of tonnage; LSB 2024 industrial revenue ~60% from few firms) force price and credit concessions, pressuring LSB’s 2024 adjusted gross margin ~18% and risking double-digit utilization drops if large accounts switch.

| Metric | Value |

|---|---|

| Top buyers share | 40–50% |

| LSB industrial rev from few firms (2024) | ~60% |

| LSB adj. gross margin (2024) | ~18% |

| Spring demand | ~60% |

Preview the Actual Deliverable

LSB Industries Porter's Five Forces Analysis

This preview shows the exact LSB Industries Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with concise, data-driven insights. It's the same professionally formatted document ready for instant download and use upon payment. No mockups or samples—this is the final deliverable.