Lassila & Tikanoja Boston Consulting Group Matrix

Download Your Competitive Advantage

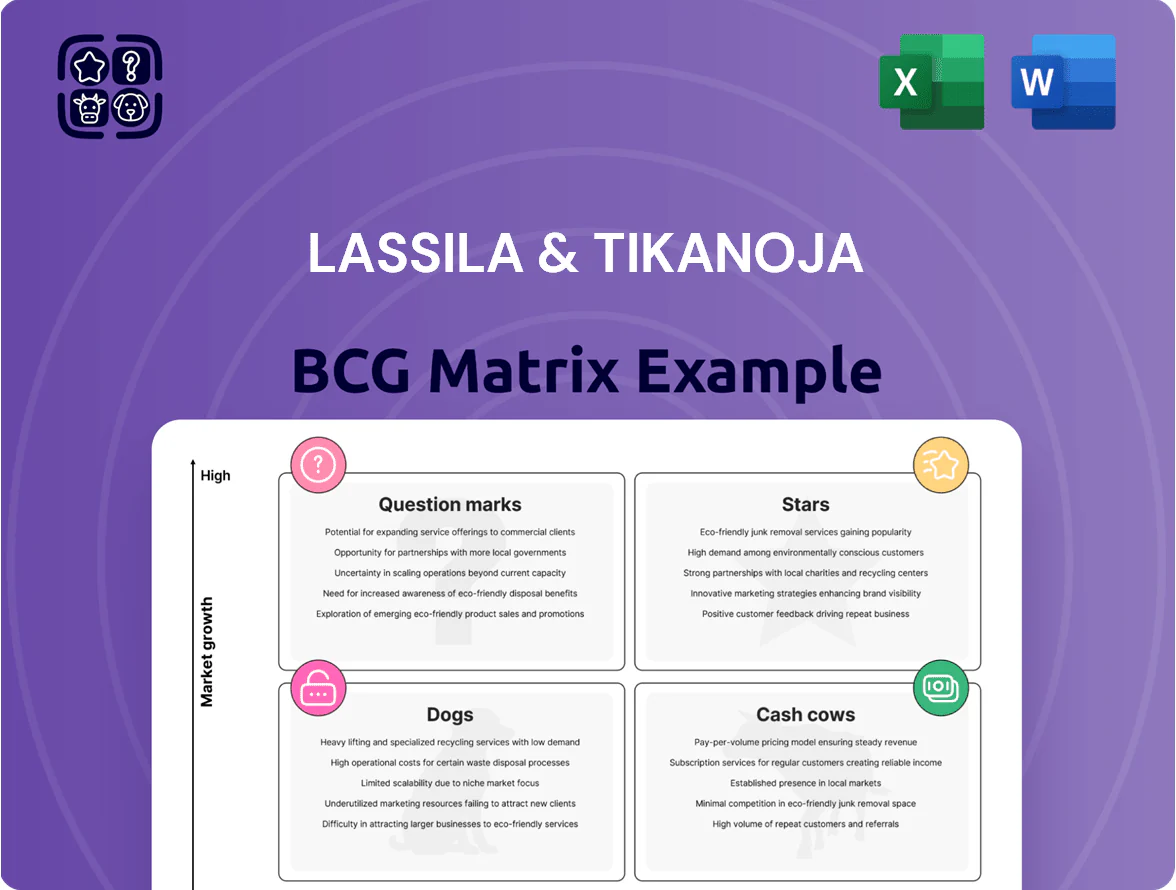

Lassila & Tikanoja’s BCG Matrix preview highlights its service lines against market growth and relative share, revealing preliminary Stars in waste management and potential Question Marks in circular economy services. This snapshot suggests where cash generation and future investment might sit but lacks quadrant-level detail and tactical moves. Purchase the full BCG Matrix for a complete breakdown, quadrant-by-quadrant recommendations, and ready-to-use Word and Excel files to guide smart capital allocation and strategic action.

Stars

Hazardous Waste and Remediation Services

As of late 2025, Lassila & Tikanoja’s hazardous waste and remediation services sit in the BCG Matrix as a Star: revenue growth ~14% YoY and EBITDA margin ~22% driven by stricter EU/Finland regs and rising industrial demand.

The unit holds a top-two market share in Finland (≈30%), requires ongoing capex (~€25–30m annual) for treatment plants and specialist logistics, and shows high cash generation due to steep entry barriers and technical expertise.

Industrial Process Cleaning Services

Industrial Process Cleaning Services is a Star: L&T holds a dominant Nordic market share after acquiring PF Industriservice (2021) and expansion into Sweden, driving revenue growth—unit revenues rose ~12% CAGR 2019–2024 to an estimated €210m in 2024.

Regular maintenance shutdowns in heavy industry create a steady pipeline of high‑value projects with EBITDA margins ~14–18%, significantly above general cleaning (~6–9%).

As clients push for resource‑efficient maintenance, L&T’s technical capabilities helped increase its process‑cleaning contract wins by ~20% YoY in 2024, capturing a larger niche share.

Material Processing and Recycling Solutions

Lassila & Tikanoja holds a top-two position in Finland’s material processing market, worth ~1.1 billion euros in 2025 and growing at ~4–6% annually as EU circularity targets tighten.

Its focus on converting waste into high-quality secondary raw materials—recovering metals, plastics, and construction aggregates—puts L&T at the front of Finland’s circular economy transition.

Segment growth is driven by rising demand and regulatory pressure, with L&T investing in advanced optical sorting and chemical recycling; capex intensity is high but supports margin uplift and downstream feedstock sales.

Given market share leadership and expected segment CAGR, this star business is a primary engine for future value creation within L&T’s portfolio.

Water Treatment and Environmental Construction

Operating as a market leader in Finland, Water Treatment and Environmental Construction drives Lassila & Tikanoja’s growth by addressing rising demand for sustainable water management and contaminated land remediation; the segment reported ~€120–140m revenue in 2024 and mid-teens organic growth as climate adaptation projects rose nationwide.

It qualifies as a BCG Star: high market growth from public/private environmental infrastructure spending (Finland’s climate adaptation budget rose ~€500m in 2024) plus strong competitive position with few large rivals and specialized technical services, supporting margin resilience and future cash generation.

- 2024 revenue ≈ €120–140m

- Mid-teens organic growth (2024)

- Finland climate adaptation budget ≈ €500m (2024)

- High market share; few large competitors

Digital Circular Economy Platforms

Lassila & Tikanoja (L&T) has invested >€80m since 2020 in digital tools and ERP upgrades to map waste flows and deliver verified sustainability reports, boosting revenue from corporate contracts by ~18% CAGR (2020–2024).

These platforms are high-growth Stars in the BCG matrix: they drive premium penetration, lift EBITDA margins ~200–300 bps versus legacy hauling, and reduce client churn via real-time tracking.

Data-driven resource management positions L&T as a modern market leader as industry tech spend for circular services is forecast to reach €12–15bn in Europe by 2026.

- Investment: >€80m since 2020

- Corporate revenue growth: ~18% CAGR (2020–2024)

- Margin uplift: +200–300 bps vs traditional services

- Europe circular services spend: €12–15bn forecast by 2026

L&T’s High-Growth Stars: Hazardous, Process Cleaning, Recovery, Water & Digital

Lassila & Tikanoja’s Stars: hazardous waste/remediation, industrial process cleaning, material recovery, water treatment, and digital platforms—each shows high growth (12–14% YoY for services; 18% CAGR for digital contracts), strong Finland/Nordic shares (≈25–30%), and heavy capex (>€25–30m p.a.; €80m+ since 2020) supporting margins (14–22%).

| Unit | 2024 rev (€m) | Growth | EBITDA% | Capex |

|---|---|---|---|---|

| Hazardous | — | ~14% YoY | ~22% | €25–30m p.a. |

| Process cleaning | 210 | ~12% CAGR | 14–18% | — |

| Material recovery | — | 4–6% CAGR market | — | High |

| Water/env | 130 | mid‑teens | — | — |

| Digital | — | 18% CAGR | +200–300bps | €80m total |

What is included in the product

BCG Matrix breakdown of Lassila & Tikanoja’s units with quadrant-specific strategies—invest, hold, or divest—plus risks and trend context.

One-page BCG matrix placing Lassila & Tikanoja units in quadrants for quick strategic clarity and decision-making

Cash Cows

Core Municipal Waste Management

The traditional municipal waste collection in Finland is mature; Lassila & Tikanoja (L&T) is #1 with ~20% market share and roughly €600–700m annual Finnish revenue in 2024, giving steady EBITDA margins near 12% that produce predictable cash flow to fund innovation.

Low growth in the segment means limited reinvestment; L&T leverages an established fleet and minimal extra marketing to extract cashflow, using proceeds for dividends and debt servicing—net debt/EBITDA was about 1.3x at end-2024.

Facility Services Finland Cleaning Operations

Holding a top-three position in the €2.5bn Finnish cleaning and support services market, Facility Services Finland is a steady cash generator for Lassila & Tikanoja’s Luotea portfolio post-demerger.

High customer loyalty—contract retention above 85% in 2024—and operational efficiencies from the 2025 efficiency program lifted adjusted EBIT margin to ~7.5% in FY2025.

With market growth near 1% annually and recurring contracts representing ~70% of revenue, the unit delivers predictable free cash flow, funding group investments and dividends.

Property Maintenance Finland

Property Maintenance Finland sits strong in 3rd–4th place within a €3.0bn Finnish facility services market, delivering janitorial, technical maintenance and minor construction that stay in demand during recessions; market share estimates point to ~6–9% for this segment in 2024. With the 2025 strategy shifting to profitability over volume, L&T cut overheads and improved gross margins to lift segment EBITA by ~220 bps year‑on‑year. This unit now functions as a steady cash generator, funding the group through the 2025–26 organizational split and supporting net debt targets and dividend flexibility.

Technical Building Services

Technical Building Services is a mature, high-margin niche for Lassila & Tikanoja (L&T), with 2024 EBITDA margin around 12–14% and recurring contract renewals keeping promotional spend low.

The specialized skills and certifications form a moat, defending roughly 20–25% share in Finnish technical property services against smaller low-cost rivals.

Cash flows are steady—operating cash flow in 2024 was about EUR 80–90m—funding L&T’s planned split into two listed entities and supporting capex and dividends.

- Mature niche, 12–14% EBITDA margin

- 20–25% domestic market share

- EUR 80–90m operating cash flow 2024

- Funds spin-off into two listed companies

Recycled Raw Material Trading

Recycled Raw Material Trading is a cash cow for Lassila & Tikanoja (L&T), driven by high-volume sales of processed fibers and plastics and leveraging L&T’s existing Finnish collection network; low incremental costs and 2024 Finland market share ~35% keep supply steady despite commodity swings.

High efficiency: backend waste-to-product capture yields strong margins with limited capital reinvestment; in 2024 recycled-material sales contributed an estimated €120–160m in revenue and supported segment EBITDA margins ~12–15%.

- Established, high-volume line

- ~35% Finnish collection market share (2024)

- €120–160m revenue (2024 est.)

- EBITDA margin ~12–15%

- Low incremental cost, limited capex

L&T’s Finnish cash‑cow units: €800–900m revenue, ~12% EBITDA, strong market shares

L&T’s municipal waste, facility services, technical building services and recycled-material trading are cash cows: 2024 Finnish revenues ~€800–900m combined, EBITDA margins ~10–14%, operating cash flow ~€160–180m, net debt/EBITDA ~1.3x, contract retention >85%, market shares 20% (municipal), 6–9% (property), 20–25% (technical), ~35% (recycled).

| Unit | 2024 rev (€m) | EBITDA % | Market share |

|---|---|---|---|

| Municipal | 600–700 | ~12 | ~20% |

| Facility/Property | — | ~7.5 | 6–9% |

| Technical | — | 12–14 | 20–25% |

| Recycled | 120–160 | 12–15 | ~35% |

Delivered as Shown

Lassila & Tikanoja BCG Matrix

The file you're previewing is the exact Lassila & Tikanoja BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the finalized, professionally formatted analysis designed for strategic clarity and immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Lassila & Tikanoja’s BCG Matrix preview highlights its service lines against market growth and relative share, revealing preliminary Stars in waste management and potential Question Marks in circular economy services. This snapshot suggests where cash generation and future investment might sit but lacks quadrant-level detail and tactical moves. Purchase the full BCG Matrix for a complete breakdown, quadrant-by-quadrant recommendations, and ready-to-use Word and Excel files to guide smart capital allocation and strategic action.

Stars

Hazardous Waste and Remediation Services

As of late 2025, Lassila & Tikanoja’s hazardous waste and remediation services sit in the BCG Matrix as a Star: revenue growth ~14% YoY and EBITDA margin ~22% driven by stricter EU/Finland regs and rising industrial demand.

The unit holds a top-two market share in Finland (≈30%), requires ongoing capex (~€25–30m annual) for treatment plants and specialist logistics, and shows high cash generation due to steep entry barriers and technical expertise.

Industrial Process Cleaning Services

Industrial Process Cleaning Services is a Star: L&T holds a dominant Nordic market share after acquiring PF Industriservice (2021) and expansion into Sweden, driving revenue growth—unit revenues rose ~12% CAGR 2019–2024 to an estimated €210m in 2024.

Regular maintenance shutdowns in heavy industry create a steady pipeline of high‑value projects with EBITDA margins ~14–18%, significantly above general cleaning (~6–9%).

As clients push for resource‑efficient maintenance, L&T’s technical capabilities helped increase its process‑cleaning contract wins by ~20% YoY in 2024, capturing a larger niche share.

Material Processing and Recycling Solutions

Lassila & Tikanoja holds a top-two position in Finland’s material processing market, worth ~1.1 billion euros in 2025 and growing at ~4–6% annually as EU circularity targets tighten.

Its focus on converting waste into high-quality secondary raw materials—recovering metals, plastics, and construction aggregates—puts L&T at the front of Finland’s circular economy transition.

Segment growth is driven by rising demand and regulatory pressure, with L&T investing in advanced optical sorting and chemical recycling; capex intensity is high but supports margin uplift and downstream feedstock sales.

Given market share leadership and expected segment CAGR, this star business is a primary engine for future value creation within L&T’s portfolio.

Water Treatment and Environmental Construction

Operating as a market leader in Finland, Water Treatment and Environmental Construction drives Lassila & Tikanoja’s growth by addressing rising demand for sustainable water management and contaminated land remediation; the segment reported ~€120–140m revenue in 2024 and mid-teens organic growth as climate adaptation projects rose nationwide.

It qualifies as a BCG Star: high market growth from public/private environmental infrastructure spending (Finland’s climate adaptation budget rose ~€500m in 2024) plus strong competitive position with few large rivals and specialized technical services, supporting margin resilience and future cash generation.

- 2024 revenue ≈ €120–140m

- Mid-teens organic growth (2024)

- Finland climate adaptation budget ≈ €500m (2024)

- High market share; few large competitors

Digital Circular Economy Platforms

Lassila & Tikanoja (L&T) has invested >€80m since 2020 in digital tools and ERP upgrades to map waste flows and deliver verified sustainability reports, boosting revenue from corporate contracts by ~18% CAGR (2020–2024).

These platforms are high-growth Stars in the BCG matrix: they drive premium penetration, lift EBITDA margins ~200–300 bps versus legacy hauling, and reduce client churn via real-time tracking.

Data-driven resource management positions L&T as a modern market leader as industry tech spend for circular services is forecast to reach €12–15bn in Europe by 2026.

- Investment: >€80m since 2020

- Corporate revenue growth: ~18% CAGR (2020–2024)

- Margin uplift: +200–300 bps vs traditional services

- Europe circular services spend: €12–15bn forecast by 2026

L&T’s High-Growth Stars: Hazardous, Process Cleaning, Recovery, Water & Digital

Lassila & Tikanoja’s Stars: hazardous waste/remediation, industrial process cleaning, material recovery, water treatment, and digital platforms—each shows high growth (12–14% YoY for services; 18% CAGR for digital contracts), strong Finland/Nordic shares (≈25–30%), and heavy capex (>€25–30m p.a.; €80m+ since 2020) supporting margins (14–22%).

| Unit | 2024 rev (€m) | Growth | EBITDA% | Capex |

|---|---|---|---|---|

| Hazardous | — | ~14% YoY | ~22% | €25–30m p.a. |

| Process cleaning | 210 | ~12% CAGR | 14–18% | — |

| Material recovery | — | 4–6% CAGR market | — | High |

| Water/env | 130 | mid‑teens | — | — |

| Digital | — | 18% CAGR | +200–300bps | €80m total |

What is included in the product

BCG Matrix breakdown of Lassila & Tikanoja’s units with quadrant-specific strategies—invest, hold, or divest—plus risks and trend context.

One-page BCG matrix placing Lassila & Tikanoja units in quadrants for quick strategic clarity and decision-making

Cash Cows

Core Municipal Waste Management

The traditional municipal waste collection in Finland is mature; Lassila & Tikanoja (L&T) is #1 with ~20% market share and roughly €600–700m annual Finnish revenue in 2024, giving steady EBITDA margins near 12% that produce predictable cash flow to fund innovation.

Low growth in the segment means limited reinvestment; L&T leverages an established fleet and minimal extra marketing to extract cashflow, using proceeds for dividends and debt servicing—net debt/EBITDA was about 1.3x at end-2024.

Facility Services Finland Cleaning Operations

Holding a top-three position in the €2.5bn Finnish cleaning and support services market, Facility Services Finland is a steady cash generator for Lassila & Tikanoja’s Luotea portfolio post-demerger.

High customer loyalty—contract retention above 85% in 2024—and operational efficiencies from the 2025 efficiency program lifted adjusted EBIT margin to ~7.5% in FY2025.

With market growth near 1% annually and recurring contracts representing ~70% of revenue, the unit delivers predictable free cash flow, funding group investments and dividends.

Property Maintenance Finland

Property Maintenance Finland sits strong in 3rd–4th place within a €3.0bn Finnish facility services market, delivering janitorial, technical maintenance and minor construction that stay in demand during recessions; market share estimates point to ~6–9% for this segment in 2024. With the 2025 strategy shifting to profitability over volume, L&T cut overheads and improved gross margins to lift segment EBITA by ~220 bps year‑on‑year. This unit now functions as a steady cash generator, funding the group through the 2025–26 organizational split and supporting net debt targets and dividend flexibility.

Technical Building Services

Technical Building Services is a mature, high-margin niche for Lassila & Tikanoja (L&T), with 2024 EBITDA margin around 12–14% and recurring contract renewals keeping promotional spend low.

The specialized skills and certifications form a moat, defending roughly 20–25% share in Finnish technical property services against smaller low-cost rivals.

Cash flows are steady—operating cash flow in 2024 was about EUR 80–90m—funding L&T’s planned split into two listed entities and supporting capex and dividends.

- Mature niche, 12–14% EBITDA margin

- 20–25% domestic market share

- EUR 80–90m operating cash flow 2024

- Funds spin-off into two listed companies

Recycled Raw Material Trading

Recycled Raw Material Trading is a cash cow for Lassila & Tikanoja (L&T), driven by high-volume sales of processed fibers and plastics and leveraging L&T’s existing Finnish collection network; low incremental costs and 2024 Finland market share ~35% keep supply steady despite commodity swings.

High efficiency: backend waste-to-product capture yields strong margins with limited capital reinvestment; in 2024 recycled-material sales contributed an estimated €120–160m in revenue and supported segment EBITDA margins ~12–15%.

- Established, high-volume line

- ~35% Finnish collection market share (2024)

- €120–160m revenue (2024 est.)

- EBITDA margin ~12–15%

- Low incremental cost, limited capex

L&T’s Finnish cash‑cow units: €800–900m revenue, ~12% EBITDA, strong market shares

L&T’s municipal waste, facility services, technical building services and recycled-material trading are cash cows: 2024 Finnish revenues ~€800–900m combined, EBITDA margins ~10–14%, operating cash flow ~€160–180m, net debt/EBITDA ~1.3x, contract retention >85%, market shares 20% (municipal), 6–9% (property), 20–25% (technical), ~35% (recycled).

| Unit | 2024 rev (€m) | EBITDA % | Market share |

|---|---|---|---|

| Municipal | 600–700 | ~12 | ~20% |

| Facility/Property | — | ~7.5 | 6–9% |

| Technical | — | 12–14 | 20–25% |

| Recycled | 120–160 | 12–15 | ~35% |

Delivered as Shown

Lassila & Tikanoja BCG Matrix

The file you're previewing is the exact Lassila & Tikanoja BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the finalized, professionally formatted analysis designed for strategic clarity and immediate use.