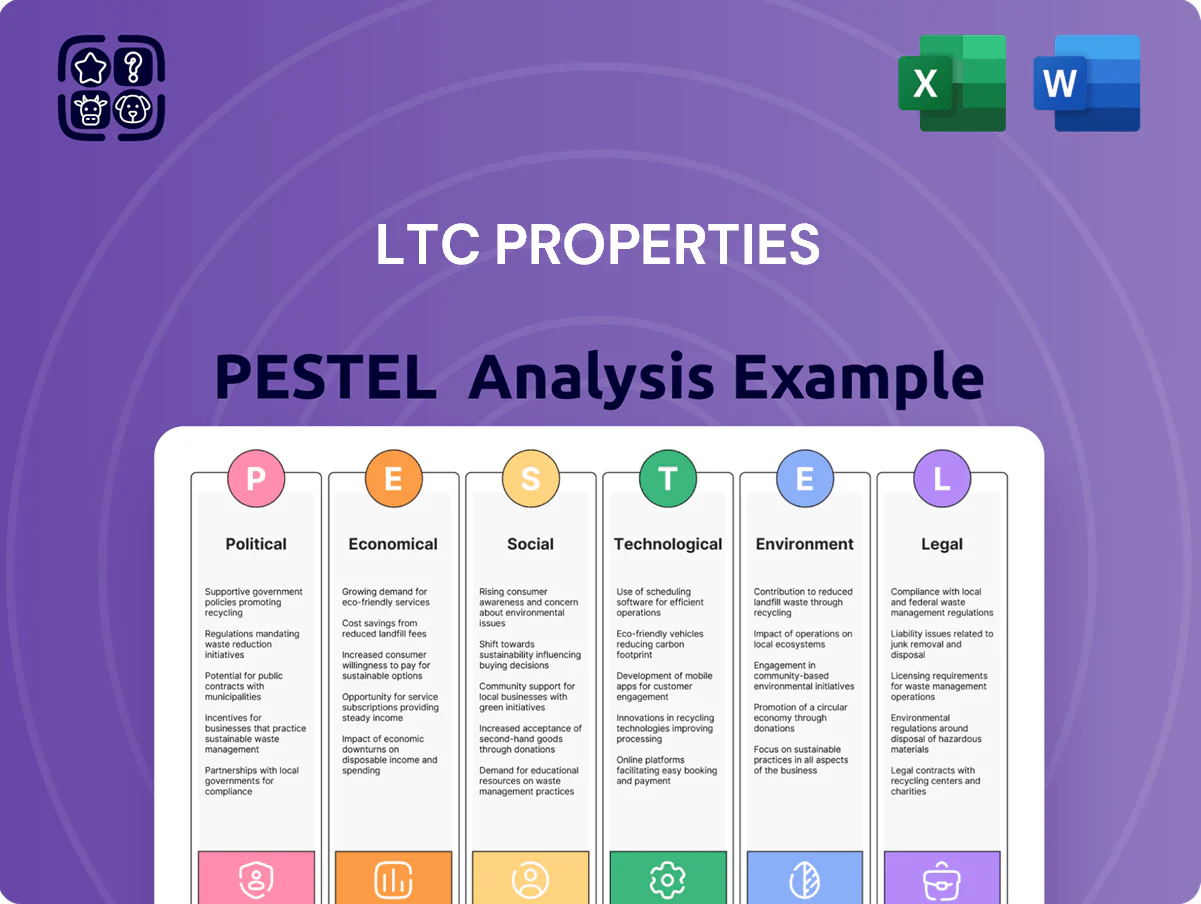

LTC Properties PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE Analysis of LTC Properties reveals how regulation, demographics, and healthcare funding trends drive risk and opportunity for the REIT—insights that help investors and strategists anticipate shifts and allocate capital smarter. Buy the full report to access the complete, ready-to-use breakdown and actionable recommendations in editable formats.

Political factors

Government healthcare reimbursement policy

Changes in Medicare and Medicaid funding levels directly affect operators' revenue; in 2024 Medicaid accounted for about 50% of skilled nursing facility revenue nationally and the 2025 proposed Medicare payment rule targeted a 1.8% net increase, influencing tenant cash flow at LTC Properties.

As a REIT, LTC relies on tenant solvency—over 60% of its rent is tied to skilled nursing tenants—so cuts or delayed reimbursements heighten lease default and mortgage risk.

Legislative shifts toward value-based care, with CMS expanding bundled payments and ACO incentives (affecting an estimated 20–30% of post-acute payments by 2025), continue to reshape federal and state support patterns for skilled nursing providers.

Federal and state election cycles

Political transitions in late 2024 and throughout 2025 reshape healthcare priorities and regulatory oversight, with the 2024 federal elections producing a divided Congress and several governorship flips affecting Medicaid policy in states representing roughly 38% of LTC Properties’ portfolio beds.

Shifts in party control can change levels of support for private-sector senior housing; for example, states that expanded Medicaid saw average occupancy gains of 2.1% in 2023–24 versus nonexpansion states.

Investors must monitor administrative impacts on HHS and CMS rulemaking—CMS rule changes in 2023–25 altered reimbursement trajectories, affecting SNF margins by an estimated 80–150 basis points for exposed operators.

Geopolitical stability and trade relations

Although LTC Properties is U.S.-focused, heightened geopolitical tensions in 2024—including strained US-China ties and sanctions on Russia—have pushed global borrowing spreads higher, contributing to a 40–60 bps rise in BBB corporate yields and tighter REIT financing conditions.

Supply-chain disruptions in 2024 raised medical-equipment and construction-material costs by roughly 6–9% year-over-year, increasing renovation capex for healthcare properties.

International economic uncertainty trimmed non-U.S. institutional allocations to U.S. REITs, with foreign ownership of U.S. REITs down about 3% in 2023–24, reducing a potential source of capital for LTC.

Immigration policy and healthcare labor

- 27% of nursing aides/personal care workers foreign-born (2024)

- Potential 10-15% wage inflation if immigration tightens

- Estimated 3-5% occupancy decline in assisted living under labor constraints

State-level regulatory environments

LTC Properties holds skilled nursing and senior housing assets across 30+ states, each with distinct licensing and certificate-of-need rules that affect expansion and capex timing; state regulatory delays contributed to 2024 occupancy pressures industry-wide (U.S. SNF occupancy ~73% in 2024 per NAHC trends).

State political shifts determine reimbursement policy—Medicaid long-term care spending varies widely (e.g., 2023 per-capita LTC Medicaid spending ranged from <$500 to >$3,000), materially impacting regional NOI and returns.

- 30+ state footprint; varied licensure/CN laws

- U.S. SNF occupancy ~73% (2024)

- Medicaid LTC per-capita spending range: <$500 to >$3,000 (2023)

- State policy changes can swing regional NOI and valuation

Policy shifts, staffing risks squeeze SNF cashflows—state variance and rates amplify NOI pressure

Political shifts (2024–25) alter Medicaid/Medicare funding—Medicaid ~50% of SNF revenue (2024), proposed 2025 Medicare +1.8%—affecting tenant cash flow; state policy variance (Medicaid LTC spend <$500–>$3,000 per capita, 2023) and 30+ state footprint drive regional NOI; staffing/visa debates (27% foreign-born aides, 2024) risk 10–15% wage pressure and 3–5% occupancy drops; macro tensions tightened BBB yields +40–60bps.

| Metric | Value |

|---|---|

| Medicaid share of SNF revenue (2024) | ~50% |

| Proposed Medicare rule (2025) | +1.8% net |

| SNF occupancy (2024) | ~73% |

| Foreign-born nursing aides (2024) | 27% |

| BBB yield change (2024–25) | +40–60 bps |

What is included in the product

Explores how macro-environmental factors uniquely affect LTC Properties across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights tailored to the senior housing and healthcare REIT sector.

A concise, PESTLE-segmented summary of LTC Properties that clarifies regulatory, demographic, economic, technological, environmental and political risks—ready to drop into presentations or share across teams for faster strategy alignment and decision-making.

Economic factors

Interest rate environment and cost of capital

As a REIT, LTC Properties is highly sensitive to interest rate moves that raise borrowing costs and widen acquisition cap rates; its average borrowing rate was about 4.1% in FY 2024, up from ~2.8% in 2021. By end-2025, rate stabilization near 4.5%–5.0% supports refinancing plans and selective acquisitions while limiting margin compression. Higher rates push investors to demand larger yields, contributing to LTCP trading at a dividend yield ~6.8% vs. 10-year Treasury ~4.4%, pressuring valuation relative to fixed income.

Inflationary pressures on operating expenses

Rising costs for food, utilities, and medical supplies—US CPI for medical care up 4.1% year-on-year (2025) and food CPI up 3.9%—compress operator margins for LTC Properties, risking tenant solvency despite net-lease pass-throughs.

Net leases often shift expense inflation to tenants, but LTC’s exposure hinges on operator financial health: Q4 2024 occupancy in skilled nursing averaged 79%, pressuring cashflows.

Persistent inflation may force LTC to adopt steeper rent escalators or renegotiate leases; average REIT rent escalators of 2–3% may prove inadequate against 3–5% input-cost inflation, prompting lease restructures to protect NOI.

Labor market dynamics and wage growth

The US skilled nursing sector faces acute labor shortages, driving median wage growth ~6–8% in 2023–24 and turnover rates near 70% for CNAs; higher operator payrolls have cut average EBITDARM margins by ~200–400 bps, raising effective lease credit risk for LTC Properties. LTC must assess local labor supply metrics—state CNA vacancy rates, average hourly RN/LPN wages and recent Medicaid rate changes—when allocating capital or negotiating renewals to avoid concentrated labor-driven downside.

Consumer discretionary spending and wealth

Assisted living demand at LTC Properties is sensitive to consumer wealth: about 70% of assisted living residents are private-pay, tying occupancy to housing and retirement savings—US household net worth fell 3.5% in 2022 but rebounded to a record $154.1 trillion by Q3 2023, supporting higher private-pay admissions.

Market volatility and recessions delay moves to private-pay facilities; during the 2020–2022 downturns occupancy dipped industry-wide by roughly 5–7%, while a stronger economy in 2023–2024 pushed occupancy and enabled operators to raise rents by 2–4% annually.

- ~70% private-pay reliance

- US household net worth $154.1T (Q3 2023)

- Occupancy swings ±5–7% in downturns

- Typical rate increases 2–4% in strong markets

Consolidation in the healthcare REIT sector

Economic strain in 2025—US inflation ~3.5% and healthcare operator margins compressed—has driven M&A in healthcare REITs as smaller operators and REITs seek scale to manage rising labor and regulatory costs.

LTC Properties can target distressed skilled-nursing and assisted-living assets; 2024-25 transaction volume in healthcare real estate rose ~18%, creating acquisition opportunities to diversify cash flows.

Access to liquidity and secondary equity market health (US REIT ETF flows down ~5% YTD in 2025) will determine LTCs ability to fund deals or pursue strategic mergers.

- 2025 inflation ~3.5% and margin pressure

- Healthcare REIT M&A volume +18% (2024-25)

- REIT ETF flows -5% YTD 2025 affecting liquidity

LTC Properties under rate and occupancy strain—selective M&A amid tightening liquidity

LTC Properties faces rate-driven funding pressure (avg borrowing ~4.1% FY2024; market yield gap: LTCP div yield ~6.8% vs 10y Treasury ~4.4%), input-cost inflation (~3.5% 2025) squeezing operator margins and occupancy (skilled nursing occupancy ~79% Q4 2024), raising tenant credit risk; 2024–25 healthcare REIT M&A +18% creates selective acquisition opportunities amid tighter liquidity (REIT ETF flows -5% YTD 2025).

| Metric | Value |

|---|---|

| Avg borrowing rate FY2024 | 4.1% |

| LTCP div yield | 6.8% |

| 10y Treasury | 4.4% |

| Inflation 2025 | 3.5% |

| Skilled nursing occ. | 79% |

| M&A volume 2024–25 | +18% |

| REIT ETF flows YTD 2025 | -5% |

Preview Before You Purchase

LTC Properties PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; this LTC Properties PESTLE analysis delivers the same structured insights, headings, and data as the downloadable file.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE Analysis of LTC Properties reveals how regulation, demographics, and healthcare funding trends drive risk and opportunity for the REIT—insights that help investors and strategists anticipate shifts and allocate capital smarter. Buy the full report to access the complete, ready-to-use breakdown and actionable recommendations in editable formats.

Political factors

Government healthcare reimbursement policy

Changes in Medicare and Medicaid funding levels directly affect operators' revenue; in 2024 Medicaid accounted for about 50% of skilled nursing facility revenue nationally and the 2025 proposed Medicare payment rule targeted a 1.8% net increase, influencing tenant cash flow at LTC Properties.

As a REIT, LTC relies on tenant solvency—over 60% of its rent is tied to skilled nursing tenants—so cuts or delayed reimbursements heighten lease default and mortgage risk.

Legislative shifts toward value-based care, with CMS expanding bundled payments and ACO incentives (affecting an estimated 20–30% of post-acute payments by 2025), continue to reshape federal and state support patterns for skilled nursing providers.

Federal and state election cycles

Political transitions in late 2024 and throughout 2025 reshape healthcare priorities and regulatory oversight, with the 2024 federal elections producing a divided Congress and several governorship flips affecting Medicaid policy in states representing roughly 38% of LTC Properties’ portfolio beds.

Shifts in party control can change levels of support for private-sector senior housing; for example, states that expanded Medicaid saw average occupancy gains of 2.1% in 2023–24 versus nonexpansion states.

Investors must monitor administrative impacts on HHS and CMS rulemaking—CMS rule changes in 2023–25 altered reimbursement trajectories, affecting SNF margins by an estimated 80–150 basis points for exposed operators.

Geopolitical stability and trade relations

Although LTC Properties is U.S.-focused, heightened geopolitical tensions in 2024—including strained US-China ties and sanctions on Russia—have pushed global borrowing spreads higher, contributing to a 40–60 bps rise in BBB corporate yields and tighter REIT financing conditions.

Supply-chain disruptions in 2024 raised medical-equipment and construction-material costs by roughly 6–9% year-over-year, increasing renovation capex for healthcare properties.

International economic uncertainty trimmed non-U.S. institutional allocations to U.S. REITs, with foreign ownership of U.S. REITs down about 3% in 2023–24, reducing a potential source of capital for LTC.

Immigration policy and healthcare labor

- 27% of nursing aides/personal care workers foreign-born (2024)

- Potential 10-15% wage inflation if immigration tightens

- Estimated 3-5% occupancy decline in assisted living under labor constraints

State-level regulatory environments

LTC Properties holds skilled nursing and senior housing assets across 30+ states, each with distinct licensing and certificate-of-need rules that affect expansion and capex timing; state regulatory delays contributed to 2024 occupancy pressures industry-wide (U.S. SNF occupancy ~73% in 2024 per NAHC trends).

State political shifts determine reimbursement policy—Medicaid long-term care spending varies widely (e.g., 2023 per-capita LTC Medicaid spending ranged from <$500 to >$3,000), materially impacting regional NOI and returns.

- 30+ state footprint; varied licensure/CN laws

- U.S. SNF occupancy ~73% (2024)

- Medicaid LTC per-capita spending range: <$500 to >$3,000 (2023)

- State policy changes can swing regional NOI and valuation

Policy shifts, staffing risks squeeze SNF cashflows—state variance and rates amplify NOI pressure

Political shifts (2024–25) alter Medicaid/Medicare funding—Medicaid ~50% of SNF revenue (2024), proposed 2025 Medicare +1.8%—affecting tenant cash flow; state policy variance (Medicaid LTC spend <$500–>$3,000 per capita, 2023) and 30+ state footprint drive regional NOI; staffing/visa debates (27% foreign-born aides, 2024) risk 10–15% wage pressure and 3–5% occupancy drops; macro tensions tightened BBB yields +40–60bps.

| Metric | Value |

|---|---|

| Medicaid share of SNF revenue (2024) | ~50% |

| Proposed Medicare rule (2025) | +1.8% net |

| SNF occupancy (2024) | ~73% |

| Foreign-born nursing aides (2024) | 27% |

| BBB yield change (2024–25) | +40–60 bps |

What is included in the product

Explores how macro-environmental factors uniquely affect LTC Properties across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights tailored to the senior housing and healthcare REIT sector.

A concise, PESTLE-segmented summary of LTC Properties that clarifies regulatory, demographic, economic, technological, environmental and political risks—ready to drop into presentations or share across teams for faster strategy alignment and decision-making.

Economic factors

Interest rate environment and cost of capital

As a REIT, LTC Properties is highly sensitive to interest rate moves that raise borrowing costs and widen acquisition cap rates; its average borrowing rate was about 4.1% in FY 2024, up from ~2.8% in 2021. By end-2025, rate stabilization near 4.5%–5.0% supports refinancing plans and selective acquisitions while limiting margin compression. Higher rates push investors to demand larger yields, contributing to LTCP trading at a dividend yield ~6.8% vs. 10-year Treasury ~4.4%, pressuring valuation relative to fixed income.

Inflationary pressures on operating expenses

Rising costs for food, utilities, and medical supplies—US CPI for medical care up 4.1% year-on-year (2025) and food CPI up 3.9%—compress operator margins for LTC Properties, risking tenant solvency despite net-lease pass-throughs.

Net leases often shift expense inflation to tenants, but LTC’s exposure hinges on operator financial health: Q4 2024 occupancy in skilled nursing averaged 79%, pressuring cashflows.

Persistent inflation may force LTC to adopt steeper rent escalators or renegotiate leases; average REIT rent escalators of 2–3% may prove inadequate against 3–5% input-cost inflation, prompting lease restructures to protect NOI.

Labor market dynamics and wage growth

The US skilled nursing sector faces acute labor shortages, driving median wage growth ~6–8% in 2023–24 and turnover rates near 70% for CNAs; higher operator payrolls have cut average EBITDARM margins by ~200–400 bps, raising effective lease credit risk for LTC Properties. LTC must assess local labor supply metrics—state CNA vacancy rates, average hourly RN/LPN wages and recent Medicaid rate changes—when allocating capital or negotiating renewals to avoid concentrated labor-driven downside.

Consumer discretionary spending and wealth

Assisted living demand at LTC Properties is sensitive to consumer wealth: about 70% of assisted living residents are private-pay, tying occupancy to housing and retirement savings—US household net worth fell 3.5% in 2022 but rebounded to a record $154.1 trillion by Q3 2023, supporting higher private-pay admissions.

Market volatility and recessions delay moves to private-pay facilities; during the 2020–2022 downturns occupancy dipped industry-wide by roughly 5–7%, while a stronger economy in 2023–2024 pushed occupancy and enabled operators to raise rents by 2–4% annually.

- ~70% private-pay reliance

- US household net worth $154.1T (Q3 2023)

- Occupancy swings ±5–7% in downturns

- Typical rate increases 2–4% in strong markets

Consolidation in the healthcare REIT sector

Economic strain in 2025—US inflation ~3.5% and healthcare operator margins compressed—has driven M&A in healthcare REITs as smaller operators and REITs seek scale to manage rising labor and regulatory costs.

LTC Properties can target distressed skilled-nursing and assisted-living assets; 2024-25 transaction volume in healthcare real estate rose ~18%, creating acquisition opportunities to diversify cash flows.

Access to liquidity and secondary equity market health (US REIT ETF flows down ~5% YTD in 2025) will determine LTCs ability to fund deals or pursue strategic mergers.

- 2025 inflation ~3.5% and margin pressure

- Healthcare REIT M&A volume +18% (2024-25)

- REIT ETF flows -5% YTD 2025 affecting liquidity

LTC Properties under rate and occupancy strain—selective M&A amid tightening liquidity

LTC Properties faces rate-driven funding pressure (avg borrowing ~4.1% FY2024; market yield gap: LTCP div yield ~6.8% vs 10y Treasury ~4.4%), input-cost inflation (~3.5% 2025) squeezing operator margins and occupancy (skilled nursing occupancy ~79% Q4 2024), raising tenant credit risk; 2024–25 healthcare REIT M&A +18% creates selective acquisition opportunities amid tighter liquidity (REIT ETF flows -5% YTD 2025).

| Metric | Value |

|---|---|

| Avg borrowing rate FY2024 | 4.1% |

| LTCP div yield | 6.8% |

| 10y Treasury | 4.4% |

| Inflation 2025 | 3.5% |

| Skilled nursing occ. | 79% |

| M&A volume 2024–25 | +18% |

| REIT ETF flows YTD 2025 | -5% |

Preview Before You Purchase

LTC Properties PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; this LTC Properties PESTLE analysis delivers the same structured insights, headings, and data as the downloadable file.