Shanxi Lu'an Environmental Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

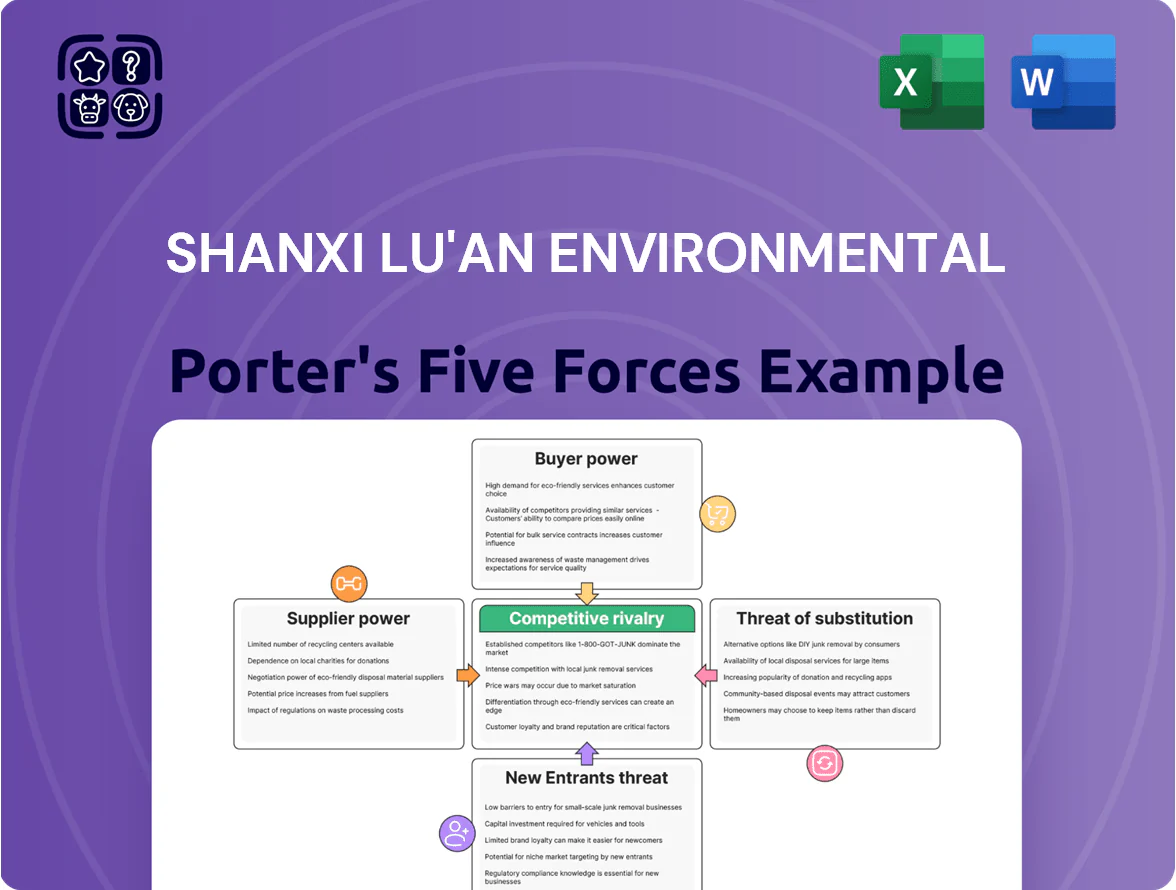

Shanxi Lu'an Environmental faces intense regulatory scrutiny and moderate supplier leverage amid rising demand for waste-to-energy solutions, while buyer power and substitutes exert uneven pressure across segments—this snapshot teases strategic risks and competitive levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to investment and strategy decisions.

Suppliers Bargaining Power

Government Control Over Mining Rights and Resource Allocation

The Chinese state is the primary supplier of mining licences and land-use rights, so its control strongly constrains Shanxi Lu'an operations; in 2024 China held 95% of coal mine approvals centrally administered.

By end-2025 strict Dual Carbon (carbon peak by 2030, neutrality by 2060) enforcement tightened new permits—national coal permit growth fell 18% in 2024—raising supplier power.

Shanxi Lu'an depends on renewals to sustain reserves (2024 reserves 1.2 billion tonnes), so state quota shifts and energy-security directives directly set production limits and resource access.

Specialized Mining Equipment and Technology Providers

The procurement of automated mining machinery and clean-coal processing tech for Shanxi Lu'an depends on a small set of high-tech domestic and global vendors; by 2025 about 60–70% of smart-mine kit in China comes from five suppliers, raising supplier influence. As Lu'an shifts to smart mines, integration and training create high switching costs, giving these vendors moderate leverage. Ongoing maintenance contracts and software updates—often 10–15% of capex annually—further lock in suppliers.

Energy and Utility Costs for Processing Facilities

The coal washing and chemical units need large electricity and water volumes, supplied mainly by state-owned utility monopolies, leaving Shanxi Luan Environmental with almost no bargaining leverage. Industrial power price swings—driven by 2025 grid reforms and national carbon pricing averaging about 60 CNY/ton CO2—have pushed regional industrial tariffs up roughly 8–12% year-on-year, squeezing margins. With no viable alternative sources or captive generation capacity covering only ~15% of demand, the firm is a clear price taker. Rising utility costs therefore directly erode EBITDA and operational flexibility.

Labor Supply and Increasing Safety Compliance Costs

The skilled underground mining workforce is shrinking as median miner age in China reached ~45 in 2024 and youth entry fell 12% since 2018, forcing Shanxi Lu an to pay premium wages and training to fill roles.

Rising safety compliance—mandatory occupational injury insurance up 18% in 2023 and new mine safety rules from 2022—plus higher health benefits and union-negotiated pay in state-owned peers raises per-ton labor costs and squeezes margins.

- Median miner age ~45 (2024)

- Youth entry down 12% since 2018

- Occupational insurance costs +18% (2023)

- Union bargaining raises base compensation

- Higher labor cost lowers coal extraction margins

Logistics and Railway Transportation Networks

Coal relies on China’s national railway for bulk moves; lines from western coalfields to eastern ports carry ~70% of coal freight, so rail access is critical.

China State Railway Group (CSRG) sets freight rates and wagon allocation; peak-season slot scarcity boosts CSRG bargaining power and can raise costs for producers like Shanxi Lu’an.

Without rail, road transport raises unit costs by an estimated 20–40% and limits shipment scale, squeezing margins.

- ~70% coal moved by rail

- CSRG controls rates/wagons

- Peak-season scarcity increases leverage

- Road alternatives 20–40% costlier

Regulatory choke, vendor lock‑in & rising logistics/grid costs make Lu’an a price‑taker

State controls licences/quota (95% approvals centrally, 2024); permit growth −18% (2024) raising supplier power. Key tech vendors supply 60–70% smart-mine kit (2025), creating switching costs; maintenance ~10–15% capex annually. Utilities (state-owned) and CSRG rail dominate—~70% coal by rail; road +20–40% cost; grid/carbon costs +8–12% y/y (2025), leaving Lu’an price-taker.

| Item | Metric |

|---|---|

| Licence control | 95% central (2024) |

| Permit growth | −18% (2024) |

| Smart-mine vendors | 60–70% from 5 (2025) |

| Maintenance cost | 10–15% capex/yr |

| Rail share | ~70% coal |

| Road cost premium | +20–40% |

| Grid/carbon tariff rise | +8–12% y/y (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Shanxi Lu'an Environmental, uncovering competitive drivers, supplier and buyer power, substitution risks, and entry barriers with strategic insights to inform investor materials and internal strategy.

A concise Porter's Five Forces snapshot for Shanxi Lu'an Environmental—quickly reveals supplier, buyer, entrant, substitute, and rivalry pressures so leadership can prioritize mitigation actions.

Customers Bargaining Power

Concentration of the Steel Industry and PCI Coal Demand

As a major PCI coal producer, Shanxi Luan depends on a few giant steel buyers; by 2025 China's top 10 steel groups account for about 55% of crude steel output, raising buyer power.

Consolidation lets these buyers demand volume discounts and tighter specs; typical PCI contracts now require ash <8% and calorific value ≥5,800 kcal/kg.

Shanxi Luan must keep product purity and supply reliability to retain preferred-supplier status and protect ~30–40% margin on PCI sales.

Impact of Long Term Supply Agreements

Long-term contracts with power plants and industrial users account for roughly 60–70% of Shanxi Lu'an Environmental's coal sales, giving predictable cash flow but embedding price caps or adjustment formulas that tilt benefits to buyers during price spikes.

These clauses prevented the company from capturing the 2021–2023 international-driven spot price surge and would similarly limit upside if domestic spot prices rose 20–30% in 2024–2025.

By late 2025 Beijing continues to favor stable pricing in coal contracts to curb CPI pressure, reinforcing buyer leverage and constraining Lu'an’s ability to monetize short-term demand shocks.

Price Sensitivity in the Methanol and Chemical Markets

Buyers in Shanxi Luan’s methanol and coal-chemical segment are highly price-sensitive; global methanol prices fell ~18% in 2024 to an annual average of about $300/ton, pushing buyers to switch suppliers or feedstocks.

High elasticity is visible: spot methanol trade volumes rose 12% in 2024 as buyers chased cheaper cargoes, reducing Shanxi Luan’s pricing power.

Consequently, margins track global supply-demand: IMO-driven demand shifts and China’s coal-to-chemicals capacity expansions left Shanxi Luan exposed, with EBITDA per ton fluctuating +/-25% year-over-year.

Availability of Imported Coal Alternatives

Coastal power plants and steel mills can import cheaper coal from Indonesia, Russia, or Mongolia; in 2024 China imported about 287 million tonnes of coal, keeping domestic prices under pressure.

The threat of substitution lets buyers negotiate lower prices when seaborne coal trades below Shanxi Lu an’s spot rates, despite import quotas the government sets.

This global competition forces Shanxi Lu an to cut costs and improve logistics to match sea-borne delivered prices and protect margins.

- 2024 China coal imports ~287 Mt

- Imports cap domestic pricing

- Buyers use threat to negotiate

- Firm must focus on cost, logistics

Industrial Decarbonization and ESG Mandates

By end-2025 many buyers face scope 3 cuts tied to net-zero targets, pushing demand toward low-ash, high-efficiency coal or fuel switching; this reduces Shanxi Lu'an Environmental’s long-term pricing leverage as buyers favor greener suppliers or alternatives.

Customers now require emissions data and certifications (e.g., ISO 14064) as procurement filters; corporates report scope 3 up to 70% of value-chain emissions, so suppliers without verified footprints lose contracts.

Buyers dominate: steel concentration, cheap imports and methanol squeeze margins

Buyers hold high power: top-10 steel groups ~55% crude steel (2025), long-term contracts 60–70% sales, China coal imports ~287 Mt (2024) cap domestic prices, methanol avg $300/ton (2024) down 18%, spot volumes +12% (2024), scope‑3 procurement rising (2025) favors low-ash coal—pressures margins and forces cost/logistics focus.

| Metric | Value |

|---|---|

| Top-10 steel share | 55% (2025) |

| Long-term sales | 60–70% |

| China coal imports | 287 Mt (2024) |

| Methanol price | $300/t avg (2024) |

Preview the Actual Deliverable

Shanxi Lu'an Environmental Porter's Five Forces Analysis

This preview shows the exact Shanxi Lu'an Environmental Porter’s Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Shanxi Lu'an Environmental faces intense regulatory scrutiny and moderate supplier leverage amid rising demand for waste-to-energy solutions, while buyer power and substitutes exert uneven pressure across segments—this snapshot teases strategic risks and competitive levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to investment and strategy decisions.

Suppliers Bargaining Power

Government Control Over Mining Rights and Resource Allocation

The Chinese state is the primary supplier of mining licences and land-use rights, so its control strongly constrains Shanxi Lu'an operations; in 2024 China held 95% of coal mine approvals centrally administered.

By end-2025 strict Dual Carbon (carbon peak by 2030, neutrality by 2060) enforcement tightened new permits—national coal permit growth fell 18% in 2024—raising supplier power.

Shanxi Lu'an depends on renewals to sustain reserves (2024 reserves 1.2 billion tonnes), so state quota shifts and energy-security directives directly set production limits and resource access.

Specialized Mining Equipment and Technology Providers

The procurement of automated mining machinery and clean-coal processing tech for Shanxi Lu'an depends on a small set of high-tech domestic and global vendors; by 2025 about 60–70% of smart-mine kit in China comes from five suppliers, raising supplier influence. As Lu'an shifts to smart mines, integration and training create high switching costs, giving these vendors moderate leverage. Ongoing maintenance contracts and software updates—often 10–15% of capex annually—further lock in suppliers.

Energy and Utility Costs for Processing Facilities

The coal washing and chemical units need large electricity and water volumes, supplied mainly by state-owned utility monopolies, leaving Shanxi Luan Environmental with almost no bargaining leverage. Industrial power price swings—driven by 2025 grid reforms and national carbon pricing averaging about 60 CNY/ton CO2—have pushed regional industrial tariffs up roughly 8–12% year-on-year, squeezing margins. With no viable alternative sources or captive generation capacity covering only ~15% of demand, the firm is a clear price taker. Rising utility costs therefore directly erode EBITDA and operational flexibility.

Labor Supply and Increasing Safety Compliance Costs

The skilled underground mining workforce is shrinking as median miner age in China reached ~45 in 2024 and youth entry fell 12% since 2018, forcing Shanxi Lu an to pay premium wages and training to fill roles.

Rising safety compliance—mandatory occupational injury insurance up 18% in 2023 and new mine safety rules from 2022—plus higher health benefits and union-negotiated pay in state-owned peers raises per-ton labor costs and squeezes margins.

- Median miner age ~45 (2024)

- Youth entry down 12% since 2018

- Occupational insurance costs +18% (2023)

- Union bargaining raises base compensation

- Higher labor cost lowers coal extraction margins

Logistics and Railway Transportation Networks

Coal relies on China’s national railway for bulk moves; lines from western coalfields to eastern ports carry ~70% of coal freight, so rail access is critical.

China State Railway Group (CSRG) sets freight rates and wagon allocation; peak-season slot scarcity boosts CSRG bargaining power and can raise costs for producers like Shanxi Lu’an.

Without rail, road transport raises unit costs by an estimated 20–40% and limits shipment scale, squeezing margins.

- ~70% coal moved by rail

- CSRG controls rates/wagons

- Peak-season scarcity increases leverage

- Road alternatives 20–40% costlier

Regulatory choke, vendor lock‑in & rising logistics/grid costs make Lu’an a price‑taker

State controls licences/quota (95% approvals centrally, 2024); permit growth −18% (2024) raising supplier power. Key tech vendors supply 60–70% smart-mine kit (2025), creating switching costs; maintenance ~10–15% capex annually. Utilities (state-owned) and CSRG rail dominate—~70% coal by rail; road +20–40% cost; grid/carbon costs +8–12% y/y (2025), leaving Lu’an price-taker.

| Item | Metric |

|---|---|

| Licence control | 95% central (2024) |

| Permit growth | −18% (2024) |

| Smart-mine vendors | 60–70% from 5 (2025) |

| Maintenance cost | 10–15% capex/yr |

| Rail share | ~70% coal |

| Road cost premium | +20–40% |

| Grid/carbon tariff rise | +8–12% y/y (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Shanxi Lu'an Environmental, uncovering competitive drivers, supplier and buyer power, substitution risks, and entry barriers with strategic insights to inform investor materials and internal strategy.

A concise Porter's Five Forces snapshot for Shanxi Lu'an Environmental—quickly reveals supplier, buyer, entrant, substitute, and rivalry pressures so leadership can prioritize mitigation actions.

Customers Bargaining Power

Concentration of the Steel Industry and PCI Coal Demand

As a major PCI coal producer, Shanxi Luan depends on a few giant steel buyers; by 2025 China's top 10 steel groups account for about 55% of crude steel output, raising buyer power.

Consolidation lets these buyers demand volume discounts and tighter specs; typical PCI contracts now require ash <8% and calorific value ≥5,800 kcal/kg.

Shanxi Luan must keep product purity and supply reliability to retain preferred-supplier status and protect ~30–40% margin on PCI sales.

Impact of Long Term Supply Agreements

Long-term contracts with power plants and industrial users account for roughly 60–70% of Shanxi Lu'an Environmental's coal sales, giving predictable cash flow but embedding price caps or adjustment formulas that tilt benefits to buyers during price spikes.

These clauses prevented the company from capturing the 2021–2023 international-driven spot price surge and would similarly limit upside if domestic spot prices rose 20–30% in 2024–2025.

By late 2025 Beijing continues to favor stable pricing in coal contracts to curb CPI pressure, reinforcing buyer leverage and constraining Lu'an’s ability to monetize short-term demand shocks.

Price Sensitivity in the Methanol and Chemical Markets

Buyers in Shanxi Luan’s methanol and coal-chemical segment are highly price-sensitive; global methanol prices fell ~18% in 2024 to an annual average of about $300/ton, pushing buyers to switch suppliers or feedstocks.

High elasticity is visible: spot methanol trade volumes rose 12% in 2024 as buyers chased cheaper cargoes, reducing Shanxi Luan’s pricing power.

Consequently, margins track global supply-demand: IMO-driven demand shifts and China’s coal-to-chemicals capacity expansions left Shanxi Luan exposed, with EBITDA per ton fluctuating +/-25% year-over-year.

Availability of Imported Coal Alternatives

Coastal power plants and steel mills can import cheaper coal from Indonesia, Russia, or Mongolia; in 2024 China imported about 287 million tonnes of coal, keeping domestic prices under pressure.

The threat of substitution lets buyers negotiate lower prices when seaborne coal trades below Shanxi Lu an’s spot rates, despite import quotas the government sets.

This global competition forces Shanxi Lu an to cut costs and improve logistics to match sea-borne delivered prices and protect margins.

- 2024 China coal imports ~287 Mt

- Imports cap domestic pricing

- Buyers use threat to negotiate

- Firm must focus on cost, logistics

Industrial Decarbonization and ESG Mandates

By end-2025 many buyers face scope 3 cuts tied to net-zero targets, pushing demand toward low-ash, high-efficiency coal or fuel switching; this reduces Shanxi Lu'an Environmental’s long-term pricing leverage as buyers favor greener suppliers or alternatives.

Customers now require emissions data and certifications (e.g., ISO 14064) as procurement filters; corporates report scope 3 up to 70% of value-chain emissions, so suppliers without verified footprints lose contracts.

Buyers dominate: steel concentration, cheap imports and methanol squeeze margins

Buyers hold high power: top-10 steel groups ~55% crude steel (2025), long-term contracts 60–70% sales, China coal imports ~287 Mt (2024) cap domestic prices, methanol avg $300/ton (2024) down 18%, spot volumes +12% (2024), scope‑3 procurement rising (2025) favors low-ash coal—pressures margins and forces cost/logistics focus.

| Metric | Value |

|---|---|

| Top-10 steel share | 55% (2025) |

| Long-term sales | 60–70% |

| China coal imports | 287 Mt (2024) |

| Methanol price | $300/t avg (2024) |

Preview the Actual Deliverable

Shanxi Lu'an Environmental Porter's Five Forces Analysis

This preview shows the exact Shanxi Lu'an Environmental Porter’s Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.