AJ Lucas Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

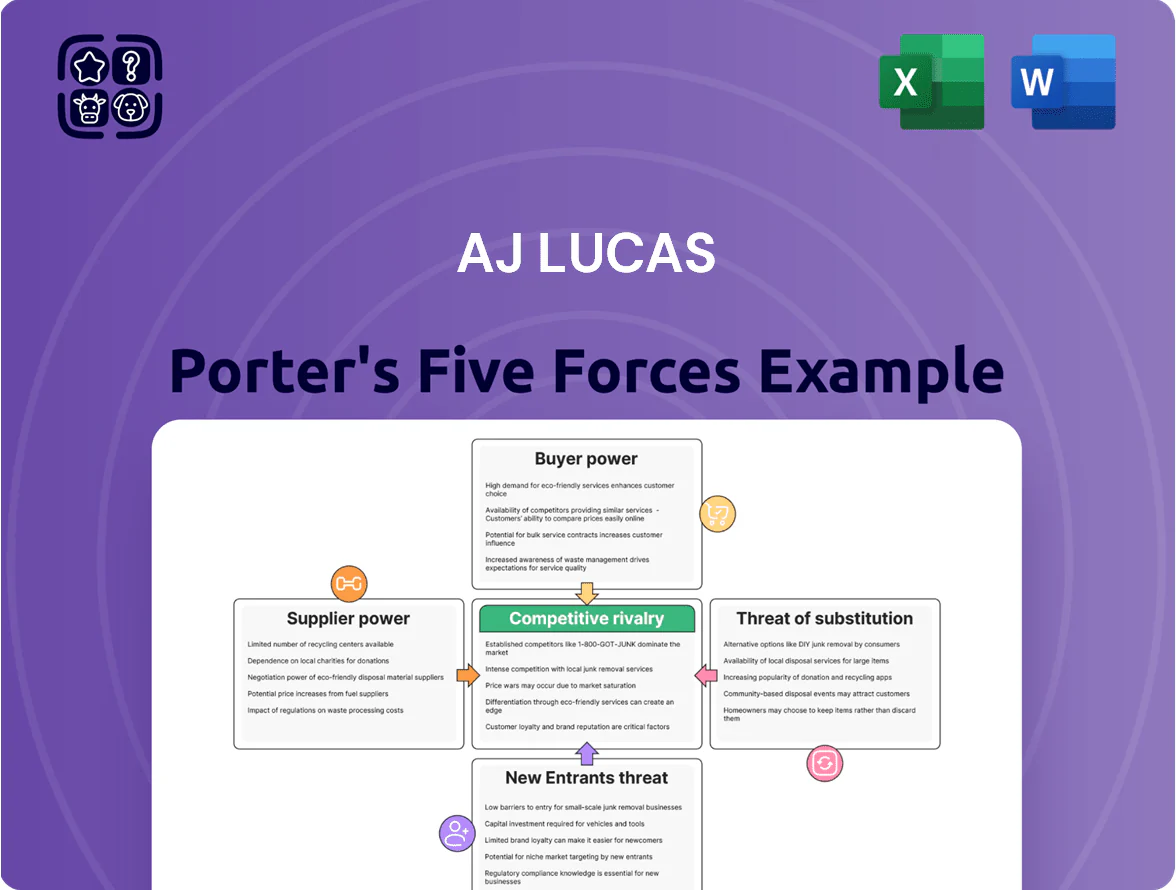

AJ Lucas faces concentrated supplier influence and fluctuating buyer demand amid capital-intensive mining services, while moderate entry barriers and evolving substitutes shape competitive intensity—this snapshot highlights key pressures and strategic levers.

This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AJ Lucas’s competitive dynamics, force-by-force ratings, visuals, and actionable insights for investment or strategy.

Suppliers Bargaining Power

Specialized Drilling Equipment and Rig Manufacturers

The market for high-spec drilling rigs and specialized components is concentrated among a few global manufacturers, giving suppliers moderate-to-high bargaining power; AJ Lucas depends on these vendors for deep-hole and directional projects, where custom rig lead times often exceed 9–12 months and OEM spare parts margins can be 20–40%. This supplier leverage raises capex uncertainty and risks operational downtime—Lucas reported capital commitments of A$24m in FY2024, so a supply delay could materially hit utilisation and revenue timing.

Availability of Highly Skilled Technical Labor

The drilling and engineering sector needs specialized staff—experienced drillers, engineers, and safety officers—and by end-2025 talent shortages persist as retirees exit and younger workers shift to renewables, with 28% fewer applicants for senior rigs roles year-over-year. This scarcity raises bargaining power of unions and specialists, pushing wage bills up (industry median rig overtime rates rose 12% in 2024) and lifting recruitment costs. AJ Lucas must spend more on retention and training—estimates suggest a 10–15% uplift in HR costs—to avoid losing critical expertise to competitors and other extractive firms.

Volatility in Energy and Fuel Input Costs

Diesel and electricity drive AJ Lucas’s drilling costs; diesel rose ~18% in 2021–2022 and global fuel volatility kept spot oil between $70–$110/barrel through 2025, complicating forecasts. While rise-and-fall clauses let AJ Lucas pass some increases, suppliers hold power because fuel is a commodity and short-term spikes—e.g., a 20% fuel jump—can cut operating margins by 3–6% if contracts lack flexibility.

Consolidation of Specialized Technology Providers

As drilling grows data-driven, AJ Lucas relies on third-party software and geological modeling from a small oligopoly; vendors like Schlumberger and Halliburton-owned tech units can set subscription terms, with industry reports noting top 5 providers controlling ~60–70% of market share in 2024.

This gives suppliers pricing power while AJ Lucas integrates these tools for directional drilling and methane drainage; switching costs rise from staff retraining and complex data migration, often costing millions and taking months.

- Oligopoly: top 5 ≈60–70% market share (2024)

- Subscription pricing power: vendors set terms

- Integration benefit: improves directional drilling, methane drainage

- High switching costs: staff retrain + data migration; often months and multi-million $)

Raw Material Supply for Infrastructure Projects

The engineering and infrastructure division is highly exposed to price and availability shifts in steel, cement and aggregates; global steel prices rose ~18% in 2024 and Australian domestic specialized steel shortages added ~10–15% to project steel costs in 2024–25, squeezing margins on pipeline and civil works.

Suppliers’ bargaining power varies with regional demand and trade policy: export curbs or shipping cost spikes can raise input costs quickly, so AJ Lucas must lock long‑lead contracts and use indexed price clauses to protect timelines and budgets.

- 2024 global steel +18%

- Australian specialized steel premium ~10–15% (2024–25)

- Use long‑lead contracts, indexed clauses

- Supplier consolidation raises risk in certain regions

Suppliers' Squeeze: Long OEM Lead Times, Rising Steel & Fuel Trim Margins

Suppliers hold moderate-to-high power: few rig OEMs (lead times 9–12+ months; OEM parts margins 20–40%), top-5 software firms ~60–70% share (2024), fuel volatility (oil $70–$110/bbl to 2025) and 2024 steel +18% (AU specialized premium 10–15%) raise capex, downtime and input costs—AJ Lucas reported A$24m capex FY2024; expect 10–15% higher HR costs and 3–6% margin hit from 20% fuel spikes.

| Metric | 2024–25 |

|---|---|

| Rig lead time | 9–12+ months |

| OEM parts margin | 20–40% |

| Top-5 software share | 60–70% |

| Steel price change | +18% (2024) |

| AU steel premium | +10–15% |

| AJ Lucas capex | A$24m FY2024 |

What is included in the product

Concise Porter's Five Forces analysis tailored to AJ Lucas that uncovers competitive intensity, supplier and buyer power, entry barriers, and substitute threats, with strategic insights to inform investor materials and internal planning.

A concise Five Forces one-sheet for AJ Lucas—instantly visualize competitive pressures and relieve decision-making friction with a clean, copy-ready layout and adjustable inputs for evolving market data.

Customers Bargaining Power

Concentration of Major Mining and Energy Clients

The customer base for AJ Lucas is highly concentrated, dominated by Tier 1 metallurgical coal producers and major energy firms; top five clients accounted for about 62% of revenue in FY2024, giving buyers strong leverage.

These large clients can insist on strict safety, high efficiency, and lower pricing, and contract terms often tie payments to performance metrics; losing one, such as BHP or Rio Tinto, could cut revenue by an estimated 15–25% and materially weaken cash flow.

Competitive Tender and Bidding Processes

Most drilling and infrastructure work is awarded via highly structured, competitive tenders; in 2024 Australian mining tenders saw average price compression of ~8–12%, pressure that forces AJ Lucas to bid with thin margins.

Clients use these auction-like processes to drive down prices and extract value, and AJ Lucas must show clear technical differentiation—e.g., demonstrated 10–15% higher ROP (rate of penetration) on trials—to win jobs.

The transparency of bids lets customers compare offerings and push aggressive commercial terms, contributing to AJ Lucas’s gross margins near industry lows of 6–9% in recent years.

Client Sensitivity to Commodity Price Cycles

The demand for AJ Lucas drilling is derived from coal, gas and mineral prices; when prices slide customers delay exploration to conserve cash. By end-2025 coal miners’ cost-cutting raised contractor pressure—Australian coal prices fell ~18% year-on-year in 2025, pushing clients to seek rate cuts. This cyclicality lets customers scale work or renegotiate contracts during downturns, reducing AJ Lucas’s pricing power and revenue visibility.

Low Switching Costs Between Service Providers

AJ Lucas holds specialized drilling skills, yet large contractors like Schlumberger, Worley, and Halliburton can provide similar services, so clients face low switching costs at contract end.

This keeps constant pressure on AJ Lucas to sustain high service quality and safety; in 2024 the Australian drilling sector saw contract churn rates near 18%, highlighting client mobility.

Customers routinely threaten to switch to enforce performance benchmarks and competitive pricing, making retention critical to AJ Lucas’s margins.

- Specialized but replaceable skills

- Low switching costs raise churn (~18% in 2024)

- Safety and quality directly tied to retention

- Switch threat used to enforce pricing/performance

Demand for Integrated and Sustainable Solutions

Modern clients demand integrated drilling services that bundle environmental management and methane drainage; 68% of oil and gas EPC contracts in 2024 included ESG KPIs, pushing suppliers to expand capabilities or lose premium work.

Buyers can insist on ESG metrics in contracts, affecting pricing and contract length; AJ Lucas must adapt its service model and reportable metrics to stay a preferred partner and protect revenue.

- 68% of 2024 EPC contracts had ESG KPIs

- Bundled services win higher-margin bids

- ESG clauses influence pricing and tenure

- AJ Lucas needs capability expansion and reporting

Concentrated buyers, 8–12% tender squeeze and 15–25% revenue loss risk

Buyers hold high leverage: top-5 clients ~62% of FY2024 revenue, giving them pricing power and tender-driven 8–12% price compression in 2024; losing a major client could cut revenue 15–25%.

Low switching costs and 18% contract churn (2024) force AJ Lucas to meet strict safety, efficiency and ESG KPIs (68% of EPCs had ESG clauses in 2024) to retain margin.

| Metric | Value |

|---|---|

| Top-5 client share (FY2024) | ~62% |

| Price compression (2024 tenders) | 8–12% |

| Contract churn (2024) | ~18% |

| ESG KPIs in EPCs (2024) | 68% |

Preview Before You Purchase

AJ Lucas Porter's Five Forces Analysis

This preview shows the exact AJ Lucas Porter’s Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

AJ Lucas faces concentrated supplier influence and fluctuating buyer demand amid capital-intensive mining services, while moderate entry barriers and evolving substitutes shape competitive intensity—this snapshot highlights key pressures and strategic levers.

This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AJ Lucas’s competitive dynamics, force-by-force ratings, visuals, and actionable insights for investment or strategy.

Suppliers Bargaining Power

Specialized Drilling Equipment and Rig Manufacturers

The market for high-spec drilling rigs and specialized components is concentrated among a few global manufacturers, giving suppliers moderate-to-high bargaining power; AJ Lucas depends on these vendors for deep-hole and directional projects, where custom rig lead times often exceed 9–12 months and OEM spare parts margins can be 20–40%. This supplier leverage raises capex uncertainty and risks operational downtime—Lucas reported capital commitments of A$24m in FY2024, so a supply delay could materially hit utilisation and revenue timing.

Availability of Highly Skilled Technical Labor

The drilling and engineering sector needs specialized staff—experienced drillers, engineers, and safety officers—and by end-2025 talent shortages persist as retirees exit and younger workers shift to renewables, with 28% fewer applicants for senior rigs roles year-over-year. This scarcity raises bargaining power of unions and specialists, pushing wage bills up (industry median rig overtime rates rose 12% in 2024) and lifting recruitment costs. AJ Lucas must spend more on retention and training—estimates suggest a 10–15% uplift in HR costs—to avoid losing critical expertise to competitors and other extractive firms.

Volatility in Energy and Fuel Input Costs

Diesel and electricity drive AJ Lucas’s drilling costs; diesel rose ~18% in 2021–2022 and global fuel volatility kept spot oil between $70–$110/barrel through 2025, complicating forecasts. While rise-and-fall clauses let AJ Lucas pass some increases, suppliers hold power because fuel is a commodity and short-term spikes—e.g., a 20% fuel jump—can cut operating margins by 3–6% if contracts lack flexibility.

Consolidation of Specialized Technology Providers

As drilling grows data-driven, AJ Lucas relies on third-party software and geological modeling from a small oligopoly; vendors like Schlumberger and Halliburton-owned tech units can set subscription terms, with industry reports noting top 5 providers controlling ~60–70% of market share in 2024.

This gives suppliers pricing power while AJ Lucas integrates these tools for directional drilling and methane drainage; switching costs rise from staff retraining and complex data migration, often costing millions and taking months.

- Oligopoly: top 5 ≈60–70% market share (2024)

- Subscription pricing power: vendors set terms

- Integration benefit: improves directional drilling, methane drainage

- High switching costs: staff retrain + data migration; often months and multi-million $)

Raw Material Supply for Infrastructure Projects

The engineering and infrastructure division is highly exposed to price and availability shifts in steel, cement and aggregates; global steel prices rose ~18% in 2024 and Australian domestic specialized steel shortages added ~10–15% to project steel costs in 2024–25, squeezing margins on pipeline and civil works.

Suppliers’ bargaining power varies with regional demand and trade policy: export curbs or shipping cost spikes can raise input costs quickly, so AJ Lucas must lock long‑lead contracts and use indexed price clauses to protect timelines and budgets.

- 2024 global steel +18%

- Australian specialized steel premium ~10–15% (2024–25)

- Use long‑lead contracts, indexed clauses

- Supplier consolidation raises risk in certain regions

Suppliers' Squeeze: Long OEM Lead Times, Rising Steel & Fuel Trim Margins

Suppliers hold moderate-to-high power: few rig OEMs (lead times 9–12+ months; OEM parts margins 20–40%), top-5 software firms ~60–70% share (2024), fuel volatility (oil $70–$110/bbl to 2025) and 2024 steel +18% (AU specialized premium 10–15%) raise capex, downtime and input costs—AJ Lucas reported A$24m capex FY2024; expect 10–15% higher HR costs and 3–6% margin hit from 20% fuel spikes.

| Metric | 2024–25 |

|---|---|

| Rig lead time | 9–12+ months |

| OEM parts margin | 20–40% |

| Top-5 software share | 60–70% |

| Steel price change | +18% (2024) |

| AU steel premium | +10–15% |

| AJ Lucas capex | A$24m FY2024 |

What is included in the product

Concise Porter's Five Forces analysis tailored to AJ Lucas that uncovers competitive intensity, supplier and buyer power, entry barriers, and substitute threats, with strategic insights to inform investor materials and internal planning.

A concise Five Forces one-sheet for AJ Lucas—instantly visualize competitive pressures and relieve decision-making friction with a clean, copy-ready layout and adjustable inputs for evolving market data.

Customers Bargaining Power

Concentration of Major Mining and Energy Clients

The customer base for AJ Lucas is highly concentrated, dominated by Tier 1 metallurgical coal producers and major energy firms; top five clients accounted for about 62% of revenue in FY2024, giving buyers strong leverage.

These large clients can insist on strict safety, high efficiency, and lower pricing, and contract terms often tie payments to performance metrics; losing one, such as BHP or Rio Tinto, could cut revenue by an estimated 15–25% and materially weaken cash flow.

Competitive Tender and Bidding Processes

Most drilling and infrastructure work is awarded via highly structured, competitive tenders; in 2024 Australian mining tenders saw average price compression of ~8–12%, pressure that forces AJ Lucas to bid with thin margins.

Clients use these auction-like processes to drive down prices and extract value, and AJ Lucas must show clear technical differentiation—e.g., demonstrated 10–15% higher ROP (rate of penetration) on trials—to win jobs.

The transparency of bids lets customers compare offerings and push aggressive commercial terms, contributing to AJ Lucas’s gross margins near industry lows of 6–9% in recent years.

Client Sensitivity to Commodity Price Cycles

The demand for AJ Lucas drilling is derived from coal, gas and mineral prices; when prices slide customers delay exploration to conserve cash. By end-2025 coal miners’ cost-cutting raised contractor pressure—Australian coal prices fell ~18% year-on-year in 2025, pushing clients to seek rate cuts. This cyclicality lets customers scale work or renegotiate contracts during downturns, reducing AJ Lucas’s pricing power and revenue visibility.

Low Switching Costs Between Service Providers

AJ Lucas holds specialized drilling skills, yet large contractors like Schlumberger, Worley, and Halliburton can provide similar services, so clients face low switching costs at contract end.

This keeps constant pressure on AJ Lucas to sustain high service quality and safety; in 2024 the Australian drilling sector saw contract churn rates near 18%, highlighting client mobility.

Customers routinely threaten to switch to enforce performance benchmarks and competitive pricing, making retention critical to AJ Lucas’s margins.

- Specialized but replaceable skills

- Low switching costs raise churn (~18% in 2024)

- Safety and quality directly tied to retention

- Switch threat used to enforce pricing/performance

Demand for Integrated and Sustainable Solutions

Modern clients demand integrated drilling services that bundle environmental management and methane drainage; 68% of oil and gas EPC contracts in 2024 included ESG KPIs, pushing suppliers to expand capabilities or lose premium work.

Buyers can insist on ESG metrics in contracts, affecting pricing and contract length; AJ Lucas must adapt its service model and reportable metrics to stay a preferred partner and protect revenue.

- 68% of 2024 EPC contracts had ESG KPIs

- Bundled services win higher-margin bids

- ESG clauses influence pricing and tenure

- AJ Lucas needs capability expansion and reporting

Concentrated buyers, 8–12% tender squeeze and 15–25% revenue loss risk

Buyers hold high leverage: top-5 clients ~62% of FY2024 revenue, giving them pricing power and tender-driven 8–12% price compression in 2024; losing a major client could cut revenue 15–25%.

Low switching costs and 18% contract churn (2024) force AJ Lucas to meet strict safety, efficiency and ESG KPIs (68% of EPCs had ESG clauses in 2024) to retain margin.

| Metric | Value |

|---|---|

| Top-5 client share (FY2024) | ~62% |

| Price compression (2024 tenders) | 8–12% |

| Contract churn (2024) | ~18% |

| ESG KPIs in EPCs (2024) | 68% |

Preview Before You Purchase

AJ Lucas Porter's Five Forces Analysis

This preview shows the exact AJ Lucas Porter’s Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use the moment you buy.