Lucas Bols Porter's Five Forces Analysis

From Overview to Strategy Blueprint

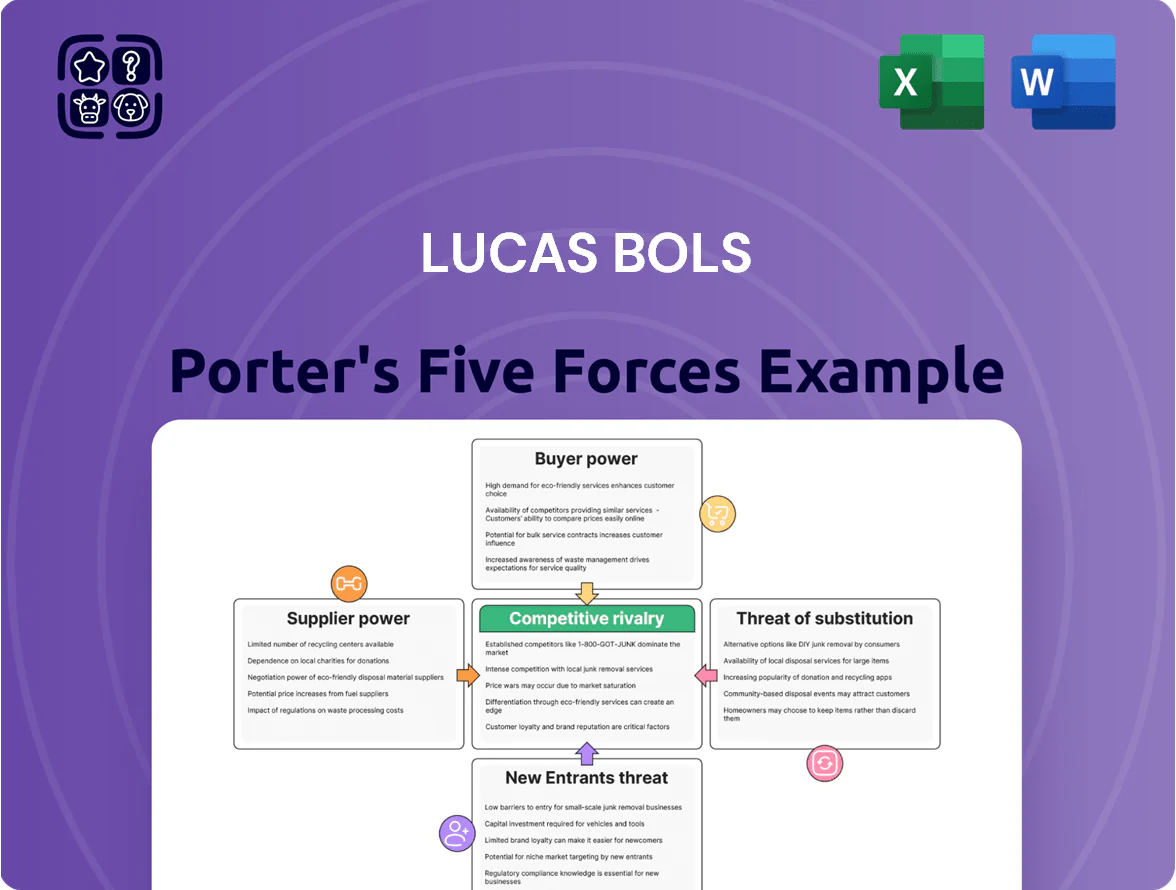

Lucas Bols faces moderate supplier power and evolving consumer tastes, with niche brand strength balancing intense competition and substitution risks; regulatory shifts and distribution dynamics further shape its strategic outlook.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lucas Bols’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity Price Sensitivity

Production of spirits depends on grain, sugar and botanicals; by late 2025 global commodity volatility raised input costs ~8–12% year-on-year, pressuring margins for premium brands like Lucas Bols that insist on high-quality inputs.

Suppliers hold moderate bargaining power: ingredients are commodities but strict quality and provenance needs cut viable sources, and long-term contracts or spot-price exposure affect cost pass-through.

Packaging Supply Concentration

Glass bottle manufacturing is concentrated among a handful of global players (Owens-Illinois, Ardagh, Verallia), giving suppliers strong bargaining power over spirits firms like Lucas Bols; global container glass capacity is ~55 million tonnes in 2024, limiting alternatives.

Lucas Bols needs specialized shapes and small runs across ~30+ SKUs, so it faces price risk and lead-time exposure if a key glass supplier raises prices or cuts capacity.

By 2025 the push for recycled and lightweight glass — recycled content targets ~40% in EU proposals and 10–15% higher production costs for recycled glass — narrows capable suppliers, increasing supply-side leverage.

Energy Costs for Distillation

Lucas Bols' pot and column distillation is energy-heavy, tying 2025 operations to utility providers; energy made up ~6–8% of production costs in EU spirit makers, so spot-price swings hit margins.

By 2025 Lucas Bols lowered grid reliance via 18% onsite renewables and heat-recovery, yet regional gas and electricity volatility in Netherlands and Spain keeps supplier leverage high.

Logistics and Distribution Partners

Third-party logistics (3PL) firms move Lucas Bols product from Dutch plants to global markets; in 2024 Lucas Bols reported 62% of shipments via outsourced carriers, heightening supplier influence.

Operating asset-light, Bols depends on specialists familiar with alcohol rules, giving 3PLs leverage through route control and certification needs.

Fuel and labor cost pass-throughs pressured distribution costs ~+7% in 2023–24, letting providers shift margin risk.

- 62% outsourced shipments (2024)

- 3PLs control key routes and compliance

- Distribution costs rose ~7% (2023–24)

Specialized Botanical Suppliers

Lucas Bols relies on secret recipes needing specific herbs and exotic botanicals sourced globally, creating reliance on a small set of specialized growers who match exact quality and provenance standards.

That niche supply base increases supplier bargaining power: limited substitution raises risk of price pressure and supply disruption, notably since specialty botanicals represented about 12% of COGS in comparable craft spirits in 2024.

Small suppliers can demand premiums or priority allocations, affecting margins and production scheduling for Bols’ liqueurs and genevers.

- Secret recipes require niche botanicals

- Few growers meet specs → higher supplier power

- Estimated 12% of COGS tied to specialty botanicals (2024)

- Risk: price pressure, supply disruption, allocation demands

Suppliers Hold Strong Leverage: Botanicals, Glass, Energy & Logistics Drive Cost Risk

Suppliers exert moderate-to-high power: commodity inputs limit leverage, but strict quality, niche botanicals (~12% COGS, 2024), concentrated glass producers (global capacity ~55 Mt, 2024), energy exposure (6–8% COGS) and 62% outsourced logistics (2024) raise costs and disruption risk; recycled-glass rules (~40% EU target) and small SKU runs increase supplier leverage.

| Item | 2024–25 |

|---|---|

| Botanicals | ~12% COGS |

| Glass capacity | ~55 Mt |

| Outsourced shipments | 62% |

| Energy share | 6–8% COGS |

What is included in the product

Tailored exclusively for Lucas Bols, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats shaping its profitability and market position.

Streamlined Porter's Five Forces for Lucas Bols—one-sheet clarity that highlights competitive threats and opportunities instantly, ready to drop into investor decks or strategic reviews.

Customers Bargaining Power

Consolidation of Global Retail Chains

Influence of Professional Bartenders

In the on-trade, professional bartenders and mixologists act as gatekeepers for Lucas Bols, shaping menu placement and consumer trends; one global survey (2024) found 62% of bartenders influence house spirit selection.

Individual bars have limited power, but the collective global bartending community can make or break liqueur lines—Bols reports 18% net sales tied to on-trade accounts in 2024.

Bols invests in the Bols Cocktail Academy to build loyalty; switching risk is high since bartenders can migrate to rivals if product quality or versatility drops.

Dominance of International Distributors

In many markets Lucas Bols depends on large third-party distributors that control access to bars, restaurants and retail, giving these intermediaries strong bargaining power over shelf placement and promotional support.

Distributors often carry 20+ spirit brands and prioritize those with higher margins or co-investment; a 2024 Euromonitor note showed off-trade distributors allocate prime placement to top 3 suppliers 65% of the time.

Maintaining relationships and funding trade support is vital: if distributors drop push activity, Lucas Bols can lose 5–10% local volume within a year.

Low Switching Costs for Consumers

Individual consumers face almost zero switching costs when choosing vodka, gin, or liqueurs in stores or bars, so buyer power is high and price or packaging can sway purchases quickly.

To counter this, Lucas Bols leverages 450+ years of brand heritage and distinct botanicals—marketing that raised global retail sales to about EUR 120m in 2024—to build emotional ties that reduce switching.

- Near-zero switching costs increase buyer leverage

- Price, packaging, campaigns drive rapid switching

- Heritage + unique flavors aim to lower churn

- EUR 120m retail sales (2024) supports brand investment

Growth of Private Label Spirits

The rise of high-quality private-label spirits from major retailers threatens Lucas Bols by offering cheaper, premium-like liqueurs and gins; by late 2025 retailers such as Tesco and Waitrose expanded own-brand spirits, with private-label spirits growing ~18% CAGR 2020–2024 in Europe and capturing ~9% market share in off-trade spirits by 2024.

This empowers buyers, pressures margins, and forces Lucas Bols to justify its price premium through product innovation, marketing, and selective trade promotions to defend revenue—private-label pricing typically sits 20–40% below branded equivalents, eroding brand loyalty.

- Private-label spirits growth ~18% CAGR (2020–2024)

- Off-trade private-label share ~9% in 2024

- Retailer pricing ~20–40% below branded SKUs

- Lucas Bols must boost innovation and promotions

Bols must innovate and promote to defend margins as retailers, private labels gain power

Retailer consolidation (≈60% off-trade share by 2025) and private-label growth (~18% CAGR 2020–24; 9% off-trade share in 2024) give buyers strong leverage; Bols (€238m net sales 2024; €120m retail) must fund promotions, tailored SKUs and innovation to protect margins and distribution.

| Metric | Value |

|---|---|

| Lucas Bols net sales | €238m (2024) |

| Retail sales | €120m (2024) |

| Off-trade retailer share | ~60% (2025) |

| Private-label CAGR | ~18% (2020–24) |

| Private-label off-trade share | ~9% (2024) |

Preview the Actual Deliverable

Lucas Bols Porter's Five Forces Analysis

This preview shows the exact Lucas Bols Porter’s Five Forces analysis you’ll receive—no placeholders or samples; the full document is fully formatted, professionally written, and ready for immediate download and use right after purchase.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Lucas Bols faces moderate supplier power and evolving consumer tastes, with niche brand strength balancing intense competition and substitution risks; regulatory shifts and distribution dynamics further shape its strategic outlook.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lucas Bols’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity Price Sensitivity

Production of spirits depends on grain, sugar and botanicals; by late 2025 global commodity volatility raised input costs ~8–12% year-on-year, pressuring margins for premium brands like Lucas Bols that insist on high-quality inputs.

Suppliers hold moderate bargaining power: ingredients are commodities but strict quality and provenance needs cut viable sources, and long-term contracts or spot-price exposure affect cost pass-through.

Packaging Supply Concentration

Glass bottle manufacturing is concentrated among a handful of global players (Owens-Illinois, Ardagh, Verallia), giving suppliers strong bargaining power over spirits firms like Lucas Bols; global container glass capacity is ~55 million tonnes in 2024, limiting alternatives.

Lucas Bols needs specialized shapes and small runs across ~30+ SKUs, so it faces price risk and lead-time exposure if a key glass supplier raises prices or cuts capacity.

By 2025 the push for recycled and lightweight glass — recycled content targets ~40% in EU proposals and 10–15% higher production costs for recycled glass — narrows capable suppliers, increasing supply-side leverage.

Energy Costs for Distillation

Lucas Bols' pot and column distillation is energy-heavy, tying 2025 operations to utility providers; energy made up ~6–8% of production costs in EU spirit makers, so spot-price swings hit margins.

By 2025 Lucas Bols lowered grid reliance via 18% onsite renewables and heat-recovery, yet regional gas and electricity volatility in Netherlands and Spain keeps supplier leverage high.

Logistics and Distribution Partners

Third-party logistics (3PL) firms move Lucas Bols product from Dutch plants to global markets; in 2024 Lucas Bols reported 62% of shipments via outsourced carriers, heightening supplier influence.

Operating asset-light, Bols depends on specialists familiar with alcohol rules, giving 3PLs leverage through route control and certification needs.

Fuel and labor cost pass-throughs pressured distribution costs ~+7% in 2023–24, letting providers shift margin risk.

- 62% outsourced shipments (2024)

- 3PLs control key routes and compliance

- Distribution costs rose ~7% (2023–24)

Specialized Botanical Suppliers

Lucas Bols relies on secret recipes needing specific herbs and exotic botanicals sourced globally, creating reliance on a small set of specialized growers who match exact quality and provenance standards.

That niche supply base increases supplier bargaining power: limited substitution raises risk of price pressure and supply disruption, notably since specialty botanicals represented about 12% of COGS in comparable craft spirits in 2024.

Small suppliers can demand premiums or priority allocations, affecting margins and production scheduling for Bols’ liqueurs and genevers.

- Secret recipes require niche botanicals

- Few growers meet specs → higher supplier power

- Estimated 12% of COGS tied to specialty botanicals (2024)

- Risk: price pressure, supply disruption, allocation demands

Suppliers Hold Strong Leverage: Botanicals, Glass, Energy & Logistics Drive Cost Risk

Suppliers exert moderate-to-high power: commodity inputs limit leverage, but strict quality, niche botanicals (~12% COGS, 2024), concentrated glass producers (global capacity ~55 Mt, 2024), energy exposure (6–8% COGS) and 62% outsourced logistics (2024) raise costs and disruption risk; recycled-glass rules (~40% EU target) and small SKU runs increase supplier leverage.

| Item | 2024–25 |

|---|---|

| Botanicals | ~12% COGS |

| Glass capacity | ~55 Mt |

| Outsourced shipments | 62% |

| Energy share | 6–8% COGS |

What is included in the product

Tailored exclusively for Lucas Bols, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats shaping its profitability and market position.

Streamlined Porter's Five Forces for Lucas Bols—one-sheet clarity that highlights competitive threats and opportunities instantly, ready to drop into investor decks or strategic reviews.

Customers Bargaining Power

Consolidation of Global Retail Chains

Influence of Professional Bartenders

In the on-trade, professional bartenders and mixologists act as gatekeepers for Lucas Bols, shaping menu placement and consumer trends; one global survey (2024) found 62% of bartenders influence house spirit selection.

Individual bars have limited power, but the collective global bartending community can make or break liqueur lines—Bols reports 18% net sales tied to on-trade accounts in 2024.

Bols invests in the Bols Cocktail Academy to build loyalty; switching risk is high since bartenders can migrate to rivals if product quality or versatility drops.

Dominance of International Distributors

In many markets Lucas Bols depends on large third-party distributors that control access to bars, restaurants and retail, giving these intermediaries strong bargaining power over shelf placement and promotional support.

Distributors often carry 20+ spirit brands and prioritize those with higher margins or co-investment; a 2024 Euromonitor note showed off-trade distributors allocate prime placement to top 3 suppliers 65% of the time.

Maintaining relationships and funding trade support is vital: if distributors drop push activity, Lucas Bols can lose 5–10% local volume within a year.

Low Switching Costs for Consumers

Individual consumers face almost zero switching costs when choosing vodka, gin, or liqueurs in stores or bars, so buyer power is high and price or packaging can sway purchases quickly.

To counter this, Lucas Bols leverages 450+ years of brand heritage and distinct botanicals—marketing that raised global retail sales to about EUR 120m in 2024—to build emotional ties that reduce switching.

- Near-zero switching costs increase buyer leverage

- Price, packaging, campaigns drive rapid switching

- Heritage + unique flavors aim to lower churn

- EUR 120m retail sales (2024) supports brand investment

Growth of Private Label Spirits

The rise of high-quality private-label spirits from major retailers threatens Lucas Bols by offering cheaper, premium-like liqueurs and gins; by late 2025 retailers such as Tesco and Waitrose expanded own-brand spirits, with private-label spirits growing ~18% CAGR 2020–2024 in Europe and capturing ~9% market share in off-trade spirits by 2024.

This empowers buyers, pressures margins, and forces Lucas Bols to justify its price premium through product innovation, marketing, and selective trade promotions to defend revenue—private-label pricing typically sits 20–40% below branded equivalents, eroding brand loyalty.

- Private-label spirits growth ~18% CAGR (2020–2024)

- Off-trade private-label share ~9% in 2024

- Retailer pricing ~20–40% below branded SKUs

- Lucas Bols must boost innovation and promotions

Bols must innovate and promote to defend margins as retailers, private labels gain power

Retailer consolidation (≈60% off-trade share by 2025) and private-label growth (~18% CAGR 2020–24; 9% off-trade share in 2024) give buyers strong leverage; Bols (€238m net sales 2024; €120m retail) must fund promotions, tailored SKUs and innovation to protect margins and distribution.

| Metric | Value |

|---|---|

| Lucas Bols net sales | €238m (2024) |

| Retail sales | €120m (2024) |

| Off-trade retailer share | ~60% (2025) |

| Private-label CAGR | ~18% (2020–24) |

| Private-label off-trade share | ~9% (2024) |

Preview the Actual Deliverable

Lucas Bols Porter's Five Forces Analysis

This preview shows the exact Lucas Bols Porter’s Five Forces analysis you’ll receive—no placeholders or samples; the full document is fully formatted, professionally written, and ready for immediate download and use right after purchase.