Luceco PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, and technological advances are reshaping Luceco’s market position—our concise PESTLE highlights the key external forces affecting growth and risk. Ideal for investors and strategists, the full analysis delivers actionable insights and ready-to-use visuals to support decisions. Purchase now to access the comprehensive report and stay ahead.

Political factors

Trade Policy and Tariffs

Luceco relies heavily on global supply chains, making it sensitive to shifts in international trade agreements and import duties; tariffs on electronics from China rose to an average of 6.5% for LED components in 2024, with contingency tariffs adding up to 12% on certain lines by mid-2025.

Geopolitical tensions between the West and manufacturing hubs continue to shape cost structures, contributing to a 4–7% increase in COGS for lighting fixtures across FY2024–2025 for comparable UK import volumes.

Management must actively hedge supplier contracts and re‑route procurement to ASEAN or domestic suppliers to protect gross margins, where onshore sourcing could cut tariff exposure by up to 8 percentage points.

Energy Independence Initiatives

Global Supply Chain Geopolitics

Political stability in Southeast Asia and the South China Sea is critical for Luceco’s manufacturing and shipping; UNCTAD data show Asia-Pacific handled 80% of global container throughput in 2024, so regional disruptions could materially hit lead times and costs.

Ongoing disputes or diplomatic shifts have driven freight-rate spikes—SEA-Europe container rates rose 210% in 2021–22—and can force rapid near-shoring to protect continuity.

Luceco has diversified suppliers across Vietnam, India and Turkey, reducing single-country exposure to under 30% of key components by 2025 to hedge political risk.

Strategic stockpiling and agile logistics—buffer inventory covering 6–10 weeks of demand and flexible freight contracts—remain essential to absorb supply shocks and limit revenue volatility.

Infrastructure Investment Schemes

Public spending on social housing, NHS projects and schools drives demand for Luceco’s professional lighting and wiring; UK public sector construction spending was £120bn in 2024 with social housing and health a >30% share, supporting multi-year supply contracts.

By late 2025 government infrastructure schemes emphasize smart-city tech and grid upgrades—UK smart grid investment projected £6–8bn 2025–27—creating upsell for Luceco’s connected lighting and trunking systems.

Luceco can capture value from long-term public works if political focus stays on asset modernization; a change in government or fiscal tightening risks deferral or cancellation of contracts worth tens of millions per project to Luceco.

- Public construction spend ~£120bn (2024), health/housing >30%

- Smart-grid investment £6–8bn (2025–27)

- Multi-year contracts = stable revenue; political change = downside risk

Tax and Fiscal Policy

Corporate tax rates and R&D credits in the UK (corporation tax 25% from Apr 2023; R&D reliefs including SME R&D tax credit up to 14.5% and RDEC ~20%) and in EU/Asia affect Luceco’s reinvestment and net margins, influencing cash available for capex and product launches.

Green technology incentives—e.g., UK’s Clean Growth Fund and US Inflation Reduction Act credits—help offset development costs for energy-saving lighting, improving ROI on next-gen products.

Tightening fiscal policy or removal of investment allowances would compress margins and delay R&D; monitoring the UK 2025 autumn budget is crucial for forecasting capex, with potential EPS and free cash flow impacts.

- UK corporation tax 25% (since Apr 2023); RDEC ≈20%, SME credit ≈14.5%

- Green incentives (Clean Growth Fund, IRA) reduce effective R&D costs

- Removal of allowances could lower margins and slow product cycles

- Track 2025 autumn budget for capex, EPS and FCF guidance

Tariffs Lift COGS; UK £120bn Build & £6–8bn Smart‑Grid Spend Fuel Demand

Political factors: trade tariffs (LED component tariffs avg 6.5% in 2024; contingency up to 12% by mid‑2025) and geopolitical tensions raised COGS ~4–7% FY2024–25; UK public construction spend £120bn (2024) with >30% on health/housing and smart‑grid investment £6–8bn (2025–27) boosting demand; UK corporation tax 25% (since Apr 2023) with RDEC ≈20% and SME R&D credit ≈14.5% affecting margins and capex.

| Item | Figure |

|---|---|

| LED tariffs (2024) | 6.5% avg (up to 12%) |

| COGS impact | +4–7% FY24–25 |

| UK public construction (2024) | £120bn |

| Smart‑grid invest (2025–27) | £6–8bn |

| UK corp tax | 25% |

| RDEC / SME credit | ≈20% / ≈14.5% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Luceco across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and trends to identify threats and opportunities, tailored for executives, consultants, and investors, formatted for easy insertion into plans and reports with forward-looking insights and detailed sub-points specific to the business and its market dynamics.

A concise, visually segmented Luceco PESTLE summary that’s easy to drop into presentations or share across teams, helping stakeholders quickly align on external risks, market positioning, and regulatory impacts during planning sessions.

Economic factors

Interest Rate Volatility

Fluctuating interest rates directly affect construction and home improvement demand, core drivers for Luceco; UK base rate averaging 5.25% in 2025 has dampened new residential starts by about 12% year-on-year and delayed large commercial projects.

High borrowing costs through 2025 have shifted activity toward renovations and maintenance, which grew ~6% as homeowners deferred new builds.

Management should prioritize resilient retrofit and aftermarket channels to sustain revenue while investors monitor central bank guidance, since a 100–150bp cut would likely revive housing transactions and specialist electrical installations.

Raw Material Price Inflation

Raw material costs for copper, aluminum and specialized plastics—up 18–27% year-on-year by Q4 2025—have pressured Luceco’s margins; the group implemented hedging covering roughly 60% of expected 2026 copper exposure and introduced dynamic pricing that lifted average selling prices ~6% in H2 2025.

Semiconductor supply constraints pushed smart-controller component costs up ~22% in 2025, prompting Luceco to prioritize procurement scale and just-in-time inventory; inventory days fell from 94 to 72 between FY2024 and FY2025 to ease working capital strain.

Currency Exchange Fluctuations

As a UK-based group with ~40% revenue outside the UK, Luceco is highly exposed to GBP/USD and GBP/CNY moves; a 10% USD strength vs GBP raised Asian-sourced input costs by an estimated 6–8% in 2024, squeezing margins. A weak pound inflates reported GBP revenues but can depress consolidated profitability when import costs rise. Luceco uses forward contracts and natural hedges (local sourcing, USD-priced sales) to smooth FX impact; active FX management preserves price competitiveness in a crowded global market.

Consumer Spending Power

Disposable income levels directly affect Luceco’s DIY and portable power sales; UK real household disposable income fell 0.4% in 2023 and remained under pressure into 2024, tightening demand for non-essential home upgrades.

Economic stagnation and high living costs push consumers toward deferring projects or choosing lower-cost alternatives, reducing average selling prices in retail channels.

By end-2025 Luceco prioritized value-engineered SKUs to target budget-conscious buyers, aligning inventory and promotions with shifting sentiment to protect volume.

- UK real household disposable income: -0.4% in 2023

- Value-engineered product push completed by end-2025

- Shift causes lower ASPs, higher promo cadence

Labor Market Constraints

Rising wages and a skilled-labor shortage in manufacturing and logistics raised Luceco’s op-ex, with UK manufacturing wages up ~6% YoY in 2024 and Chinese manufacturing wages up ~5% in 2023–24, pressuring margins.

Competition for technical R&D talent for smart lighting and automation increases hiring costs; vacancy rates for tech roles rose ~12% in 2024.

Higher labor costs in China and other hubs shift the offshore vs local assembly calculus, prompting reshoring or hybrid sourcing decisions.

Accelerated automation investments aim to cut labor intensity; capital spend on factory automation rose ~15% in 2024 across EU manufacturers.

- Wage inflation: UK +6% (2024), China +5% (2023–24)

- Tech vacancy rate: +12% (2024)

- CapEx shift: +15% automation spend (2024)

- Offshore risk: rising labor costs drive partial reshoring

Inflation, rates and supply costs force retrofit shift, value SKUs and hedging

Economic headwinds—higher UK base rate (avg 5.25% in 2025), raw material inflation (copper/aluminum/plastics +18–27% YoY by Q4 2025), semiconductor cost +22% (2025), wage inflation UK +6% (2024)/China +5% (2023–24), FX exposure (~40% revenue abroad) —shifted sales to retrofit/aftermarket, drove value-SKU push and hedging/automation responses.

| Metric | Value |

|---|---|

| UK base rate (2025) | 5.25% |

| Copper/aluminum/plastics inflation | +18–27% YoY |

| Semiconductor cost | +22% (2025) |

| Wage inflation | UK +6% (2024), China +5% (2023–24) |

Preview the Actual Deliverable

Luceco PESTLE Analysis

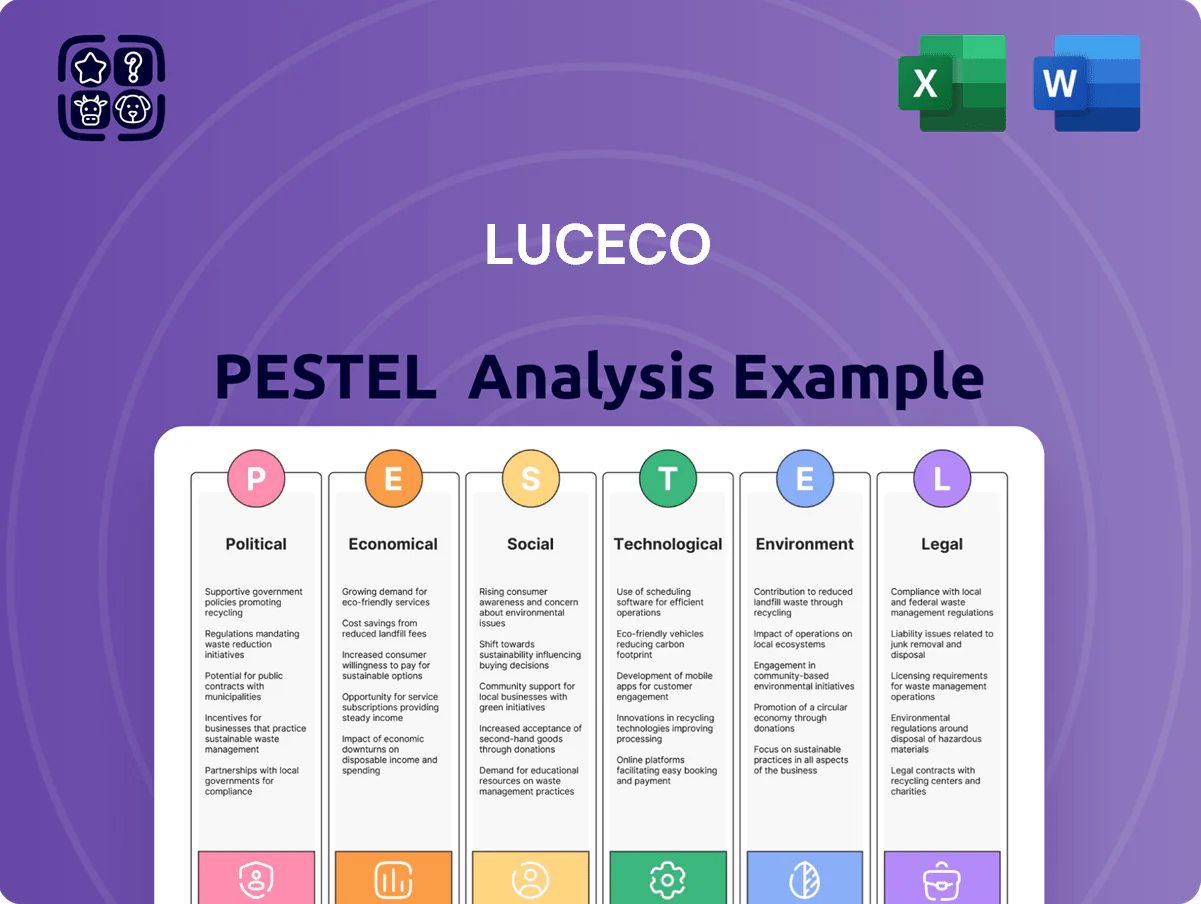

The preview shown here is the exact Luceco PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This screenshot reflects the real product with complete content and structure, not a teaser or placeholder. After checkout you’ll instantly download this exact, professionally structured file. Everything displayed is included in the final deliverable.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, and technological advances are reshaping Luceco’s market position—our concise PESTLE highlights the key external forces affecting growth and risk. Ideal for investors and strategists, the full analysis delivers actionable insights and ready-to-use visuals to support decisions. Purchase now to access the comprehensive report and stay ahead.

Political factors

Trade Policy and Tariffs

Luceco relies heavily on global supply chains, making it sensitive to shifts in international trade agreements and import duties; tariffs on electronics from China rose to an average of 6.5% for LED components in 2024, with contingency tariffs adding up to 12% on certain lines by mid-2025.

Geopolitical tensions between the West and manufacturing hubs continue to shape cost structures, contributing to a 4–7% increase in COGS for lighting fixtures across FY2024–2025 for comparable UK import volumes.

Management must actively hedge supplier contracts and re‑route procurement to ASEAN or domestic suppliers to protect gross margins, where onshore sourcing could cut tariff exposure by up to 8 percentage points.

Energy Independence Initiatives

Global Supply Chain Geopolitics

Political stability in Southeast Asia and the South China Sea is critical for Luceco’s manufacturing and shipping; UNCTAD data show Asia-Pacific handled 80% of global container throughput in 2024, so regional disruptions could materially hit lead times and costs.

Ongoing disputes or diplomatic shifts have driven freight-rate spikes—SEA-Europe container rates rose 210% in 2021–22—and can force rapid near-shoring to protect continuity.

Luceco has diversified suppliers across Vietnam, India and Turkey, reducing single-country exposure to under 30% of key components by 2025 to hedge political risk.

Strategic stockpiling and agile logistics—buffer inventory covering 6–10 weeks of demand and flexible freight contracts—remain essential to absorb supply shocks and limit revenue volatility.

Infrastructure Investment Schemes

Public spending on social housing, NHS projects and schools drives demand for Luceco’s professional lighting and wiring; UK public sector construction spending was £120bn in 2024 with social housing and health a >30% share, supporting multi-year supply contracts.

By late 2025 government infrastructure schemes emphasize smart-city tech and grid upgrades—UK smart grid investment projected £6–8bn 2025–27—creating upsell for Luceco’s connected lighting and trunking systems.

Luceco can capture value from long-term public works if political focus stays on asset modernization; a change in government or fiscal tightening risks deferral or cancellation of contracts worth tens of millions per project to Luceco.

- Public construction spend ~£120bn (2024), health/housing >30%

- Smart-grid investment £6–8bn (2025–27)

- Multi-year contracts = stable revenue; political change = downside risk

Tax and Fiscal Policy

Corporate tax rates and R&D credits in the UK (corporation tax 25% from Apr 2023; R&D reliefs including SME R&D tax credit up to 14.5% and RDEC ~20%) and in EU/Asia affect Luceco’s reinvestment and net margins, influencing cash available for capex and product launches.

Green technology incentives—e.g., UK’s Clean Growth Fund and US Inflation Reduction Act credits—help offset development costs for energy-saving lighting, improving ROI on next-gen products.

Tightening fiscal policy or removal of investment allowances would compress margins and delay R&D; monitoring the UK 2025 autumn budget is crucial for forecasting capex, with potential EPS and free cash flow impacts.

- UK corporation tax 25% (since Apr 2023); RDEC ≈20%, SME credit ≈14.5%

- Green incentives (Clean Growth Fund, IRA) reduce effective R&D costs

- Removal of allowances could lower margins and slow product cycles

- Track 2025 autumn budget for capex, EPS and FCF guidance

Tariffs Lift COGS; UK £120bn Build & £6–8bn Smart‑Grid Spend Fuel Demand

Political factors: trade tariffs (LED component tariffs avg 6.5% in 2024; contingency up to 12% by mid‑2025) and geopolitical tensions raised COGS ~4–7% FY2024–25; UK public construction spend £120bn (2024) with >30% on health/housing and smart‑grid investment £6–8bn (2025–27) boosting demand; UK corporation tax 25% (since Apr 2023) with RDEC ≈20% and SME R&D credit ≈14.5% affecting margins and capex.

| Item | Figure |

|---|---|

| LED tariffs (2024) | 6.5% avg (up to 12%) |

| COGS impact | +4–7% FY24–25 |

| UK public construction (2024) | £120bn |

| Smart‑grid invest (2025–27) | £6–8bn |

| UK corp tax | 25% |

| RDEC / SME credit | ≈20% / ≈14.5% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Luceco across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and trends to identify threats and opportunities, tailored for executives, consultants, and investors, formatted for easy insertion into plans and reports with forward-looking insights and detailed sub-points specific to the business and its market dynamics.

A concise, visually segmented Luceco PESTLE summary that’s easy to drop into presentations or share across teams, helping stakeholders quickly align on external risks, market positioning, and regulatory impacts during planning sessions.

Economic factors

Interest Rate Volatility

Fluctuating interest rates directly affect construction and home improvement demand, core drivers for Luceco; UK base rate averaging 5.25% in 2025 has dampened new residential starts by about 12% year-on-year and delayed large commercial projects.

High borrowing costs through 2025 have shifted activity toward renovations and maintenance, which grew ~6% as homeowners deferred new builds.

Management should prioritize resilient retrofit and aftermarket channels to sustain revenue while investors monitor central bank guidance, since a 100–150bp cut would likely revive housing transactions and specialist electrical installations.

Raw Material Price Inflation

Raw material costs for copper, aluminum and specialized plastics—up 18–27% year-on-year by Q4 2025—have pressured Luceco’s margins; the group implemented hedging covering roughly 60% of expected 2026 copper exposure and introduced dynamic pricing that lifted average selling prices ~6% in H2 2025.

Semiconductor supply constraints pushed smart-controller component costs up ~22% in 2025, prompting Luceco to prioritize procurement scale and just-in-time inventory; inventory days fell from 94 to 72 between FY2024 and FY2025 to ease working capital strain.

Currency Exchange Fluctuations

As a UK-based group with ~40% revenue outside the UK, Luceco is highly exposed to GBP/USD and GBP/CNY moves; a 10% USD strength vs GBP raised Asian-sourced input costs by an estimated 6–8% in 2024, squeezing margins. A weak pound inflates reported GBP revenues but can depress consolidated profitability when import costs rise. Luceco uses forward contracts and natural hedges (local sourcing, USD-priced sales) to smooth FX impact; active FX management preserves price competitiveness in a crowded global market.

Consumer Spending Power

Disposable income levels directly affect Luceco’s DIY and portable power sales; UK real household disposable income fell 0.4% in 2023 and remained under pressure into 2024, tightening demand for non-essential home upgrades.

Economic stagnation and high living costs push consumers toward deferring projects or choosing lower-cost alternatives, reducing average selling prices in retail channels.

By end-2025 Luceco prioritized value-engineered SKUs to target budget-conscious buyers, aligning inventory and promotions with shifting sentiment to protect volume.

- UK real household disposable income: -0.4% in 2023

- Value-engineered product push completed by end-2025

- Shift causes lower ASPs, higher promo cadence

Labor Market Constraints

Rising wages and a skilled-labor shortage in manufacturing and logistics raised Luceco’s op-ex, with UK manufacturing wages up ~6% YoY in 2024 and Chinese manufacturing wages up ~5% in 2023–24, pressuring margins.

Competition for technical R&D talent for smart lighting and automation increases hiring costs; vacancy rates for tech roles rose ~12% in 2024.

Higher labor costs in China and other hubs shift the offshore vs local assembly calculus, prompting reshoring or hybrid sourcing decisions.

Accelerated automation investments aim to cut labor intensity; capital spend on factory automation rose ~15% in 2024 across EU manufacturers.

- Wage inflation: UK +6% (2024), China +5% (2023–24)

- Tech vacancy rate: +12% (2024)

- CapEx shift: +15% automation spend (2024)

- Offshore risk: rising labor costs drive partial reshoring

Inflation, rates and supply costs force retrofit shift, value SKUs and hedging

Economic headwinds—higher UK base rate (avg 5.25% in 2025), raw material inflation (copper/aluminum/plastics +18–27% YoY by Q4 2025), semiconductor cost +22% (2025), wage inflation UK +6% (2024)/China +5% (2023–24), FX exposure (~40% revenue abroad) —shifted sales to retrofit/aftermarket, drove value-SKU push and hedging/automation responses.

| Metric | Value |

|---|---|

| UK base rate (2025) | 5.25% |

| Copper/aluminum/plastics inflation | +18–27% YoY |

| Semiconductor cost | +22% (2025) |

| Wage inflation | UK +6% (2024), China +5% (2023–24) |

Preview the Actual Deliverable

Luceco PESTLE Analysis

The preview shown here is the exact Luceco PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This screenshot reflects the real product with complete content and structure, not a teaser or placeholder. After checkout you’ll instantly download this exact, professionally structured file. Everything displayed is included in the final deliverable.