Lululemon Athletica Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

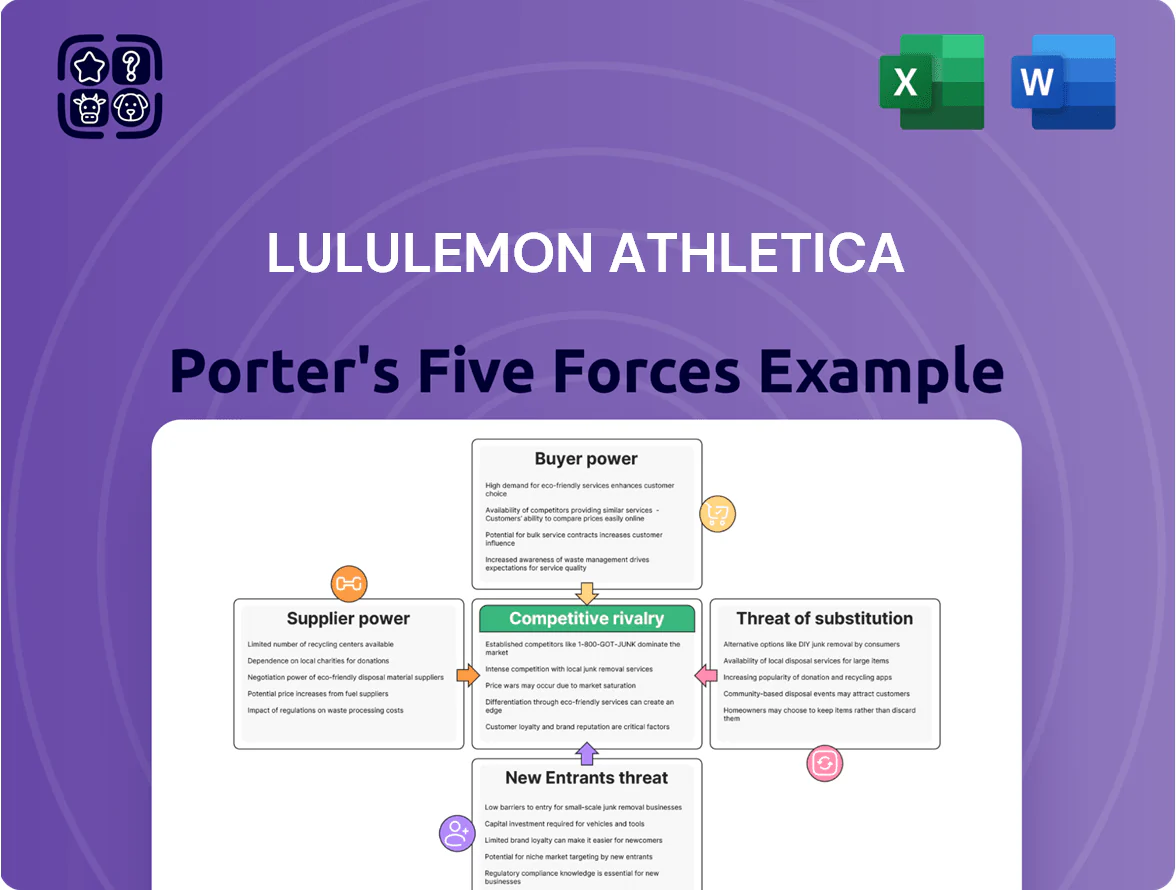

Lululemon benefits from strong brand loyalty and premium pricing power, but faces intense rivalry and growing substitute threats from fast-fashion and athleisure players.

Supplier concentration is moderate, while high entry costs and scale advantages limit new entrants—yet digital disruption and channel shifts raise strategic risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lululemon Athletica’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Global Manufacturing Base

Lululemon sources from over 150 independent vendors across South and Southeast Asia (2024 supplier roster), so no single supplier holds excessive leverage.

This geographic diversification cuts regional disruption risk—COVID-era shutdowns showed a 22% hit to peers' output vs Lululemon's <10%—and sustains competitive bidding among manufacturers.

Fragmentation lets Lululemon secure favorable pricing and enforce technical standards like 4.5% defect rates max in 2024 quality audits.

Proprietary Fabric Intellectual Property

Lululemon owns trademarks and exact specs for fabrics like Luon and Nulu, restricting mills from selling those formulations to others and lowering supplier bargaining power.

Suppliers make materials but face exclusive contracts and IP limits, creating a locked-in, dependent relationship that favors Lululemon’s margin capture.

In 2024 Lululemon reported gross margin 58.6%, reflecting value kept by the brand from fabric IP and design control.

Strict Quality and ESG Compliance Standards

Suppliers face strict quality and ESG (environmental, social, governance) controls that raise operating costs—audit compliance can add 2–5% to unit costs per industry studies in 2024–25.

Because Lululemon bought roughly $2.3 billion in goods in FY2024, vendors accept these costs to keep high-volume, premium contracts.

This scale lets Lululemon set ethics standards across its supply chain with limited supplier pushback.

Raw Material Price Sensitivity

Suppliers face volatility from petroleum-linked fibers: nylon and polyester prices jumped about 28% year-over-year in 2022-23, pressuring margins.

Lululemon reduces pass-through risk via multiyear volume commitments and pre-paid capacity, securing discounts and giving suppliers cash flow to hedge.

As a result, sudden raw-material hikes less often reach Lululemon customers; Lululemon reported stable gross margins near 55% in FY2024.

- Petro-fiber volatility up ~28% (2022–23)

- Multiyear commitments lower supplier risk

- Prepaid capacity aids supplier hedging

- Gross margin ~55% FY2024

Low Forward Integration Risk

The chance apparel suppliers launching premium retail brands to rival Lululemon is minimal; building equivalent brand equity would need advertising investments comparable to Lululemon’s 2024 marketing spend of about $487 million and years of retail scale.

Suppliers lack prestige and store networks—Lululemon’s direct-to-consumer sales were 62% of revenue in FY2024—so suppliers stay manufacturers, leaving brand control with Lululemon.

- High marketing capex barrier: ~$487M (2024)

- 62% DTC revenue (FY2024)

- Low supplier retail expertise

Fragmented vendors and strong IP keep suppliers weak, preserving ~55–58% gross margins

Suppliers have low bargaining power: >150 vendors (2024), $2.3B purchased (FY2024), and fragmented sourcing limit leverage; Lululemon IP (Luon/Nulu) and strict quality/ESG rules shift costs to suppliers; multiyear contracts and prepaid capacity smooth raw-material shocks (petro-fibers +28% 2022–23), supporting gross margins ~55–58% in FY2024.

| Metric | Value |

|---|---|

| Vendors | >150 (2024) |

| Purchases | $2.3B FY2024 |

| Gross margin | ~55–58% FY2024 |

| Petro-fiber shock | +28% (2022–23) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Lululemon Athletica, identifying disruptive substitutes, supplier/buyer power, and market dynamics that protect its premium brand and profitability.

Compact Porter's Five Forces view for Lululemon—quickly assess competitive rivalry, supplier/buyer power, threat of substitutes/entrants, and regulatory pressure to inform strategic moves.

Customers Bargaining Power

Low Switching Costs in Premium Apparel

Customers face low switching costs in premium apparel and can move to Alo Yoga or Vuori with little financial or functional effort; U.S. athleisure market share shows top rivals grew by 6–8% in 2024 while Lululemon grew ~5% (FY2024 revenue $8.1B), highlighting active competition.

No long-term contracts exist for clothing, so brand loyalty is the main barrier to churn; Lululemon reports repeat-buy rates above 60% in 2024, so loyalty must be earned and reinforced.

This forces Lululemon to keep innovating—R&D and product development plus premium materials—so it can justify premium prices and maintain gross margin (FY2024 gross margin 57%).

High Transparency and Digital Comparison

Modern shoppers use social media and e-commerce to compare Lululemon prices, reviews, and specs in real time; 72% of US consumers said online reviews influence purchases in 2024, raising customer leverage. This digital literacy lets buyers demand value and hold Lululemon accountable for quality or service lapses—online complaints can cut net promoter score quickly. Lululemon must keep a seamless omni-channel experience—its 2024 direct-to-consumer sales growth of 20% shows the stake here—to justify premium pricing and defend margins.

Community Engagement and Brand Ecosystem

Lululemon reduces buyer power by building community via ~5,000 global ambassadors and 1,700+ local studio partnerships (2025), turning products into lifestyle signals rather than commodities.

Emotional switching costs cut price sensitivity: management reported a 20% higher repeat purchase rate among members of its loyalty/educational programs in FY2024, lowering price elasticity in core 18–44 fitness demographic.

Influence of the Secondary Resale Market

The rise of platforms like Lululemon Like New and third-party resale sites gives customers more choices and price points, enabling price-sensitive shoppers to buy Lululemon without paying full retail; resale accounted for an estimated 5–7% of Lululemon category volume in 2024 per industry estimates.

Lululemon counters by running its own Like New program, launched 2019 and scaled to 150+ stores by 2024, keeping customer data and CRM control and reducing leakage to competitors.

What this hides: resale can still dilute new-product demand and compress margins if unchecked.

- Resale share ~5–7% (2024 est.)

- Like New in 150+ stores by 2024

- Own platform preserves customer data/CRM

- Resale enables price-sensitive retention, risks margin dilution

Demand for Personalization and Inclusivity

Customers now expect broad size ranges, diverse styles, and tailored experiences; 2024 surveys show 62% of apparel shoppers won't return after poor fit or limited choice, raising buyer power against Lululemon.

Lululemon expanded sizes and categories, and in FY2024 reported digital sales up 32% to $3.1 billion, using analytics and membership data to predict preferences and reduce churn.

Failure to keep pace risks share loss to inclusive rivals who launch faster and cheaper lines.

- 62% of shoppers reject poor fit (2024 survey)

- Digital sales +32% to $3.1B in FY2024

- Analytics-driven inventory to lower churn

Strong loyalty cushions pricing pressure as digital and resale reshape demand

Customers have moderate bargaining power: low switching costs and online comparison raise leverage, but strong brand loyalty (repeat-buy >60% in FY2024) and community programs reduce price sensitivity; resale channels (5–7% est. 2024) and demand for inclusive sizing increase pressure on pricing and assortment.

| Metric | 2024 |

|---|---|

| Revenue | $8.1B |

| Gross margin | 57% |

| Repeat-buy rate | >60% |

| Resale share (est.) | 5–7% |

| Digital sales | $3.1B (+32%) |

Preview the Actual Deliverable

Lululemon Athletica Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Lululemon Athletica you'll receive immediately after purchase—no placeholders or samples; the complete, professionally formatted document is ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Lululemon benefits from strong brand loyalty and premium pricing power, but faces intense rivalry and growing substitute threats from fast-fashion and athleisure players.

Supplier concentration is moderate, while high entry costs and scale advantages limit new entrants—yet digital disruption and channel shifts raise strategic risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lululemon Athletica’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Global Manufacturing Base

Lululemon sources from over 150 independent vendors across South and Southeast Asia (2024 supplier roster), so no single supplier holds excessive leverage.

This geographic diversification cuts regional disruption risk—COVID-era shutdowns showed a 22% hit to peers' output vs Lululemon's <10%—and sustains competitive bidding among manufacturers.

Fragmentation lets Lululemon secure favorable pricing and enforce technical standards like 4.5% defect rates max in 2024 quality audits.

Proprietary Fabric Intellectual Property

Lululemon owns trademarks and exact specs for fabrics like Luon and Nulu, restricting mills from selling those formulations to others and lowering supplier bargaining power.

Suppliers make materials but face exclusive contracts and IP limits, creating a locked-in, dependent relationship that favors Lululemon’s margin capture.

In 2024 Lululemon reported gross margin 58.6%, reflecting value kept by the brand from fabric IP and design control.

Strict Quality and ESG Compliance Standards

Suppliers face strict quality and ESG (environmental, social, governance) controls that raise operating costs—audit compliance can add 2–5% to unit costs per industry studies in 2024–25.

Because Lululemon bought roughly $2.3 billion in goods in FY2024, vendors accept these costs to keep high-volume, premium contracts.

This scale lets Lululemon set ethics standards across its supply chain with limited supplier pushback.

Raw Material Price Sensitivity

Suppliers face volatility from petroleum-linked fibers: nylon and polyester prices jumped about 28% year-over-year in 2022-23, pressuring margins.

Lululemon reduces pass-through risk via multiyear volume commitments and pre-paid capacity, securing discounts and giving suppliers cash flow to hedge.

As a result, sudden raw-material hikes less often reach Lululemon customers; Lululemon reported stable gross margins near 55% in FY2024.

- Petro-fiber volatility up ~28% (2022–23)

- Multiyear commitments lower supplier risk

- Prepaid capacity aids supplier hedging

- Gross margin ~55% FY2024

Low Forward Integration Risk

The chance apparel suppliers launching premium retail brands to rival Lululemon is minimal; building equivalent brand equity would need advertising investments comparable to Lululemon’s 2024 marketing spend of about $487 million and years of retail scale.

Suppliers lack prestige and store networks—Lululemon’s direct-to-consumer sales were 62% of revenue in FY2024—so suppliers stay manufacturers, leaving brand control with Lululemon.

- High marketing capex barrier: ~$487M (2024)

- 62% DTC revenue (FY2024)

- Low supplier retail expertise

Fragmented vendors and strong IP keep suppliers weak, preserving ~55–58% gross margins

Suppliers have low bargaining power: >150 vendors (2024), $2.3B purchased (FY2024), and fragmented sourcing limit leverage; Lululemon IP (Luon/Nulu) and strict quality/ESG rules shift costs to suppliers; multiyear contracts and prepaid capacity smooth raw-material shocks (petro-fibers +28% 2022–23), supporting gross margins ~55–58% in FY2024.

| Metric | Value |

|---|---|

| Vendors | >150 (2024) |

| Purchases | $2.3B FY2024 |

| Gross margin | ~55–58% FY2024 |

| Petro-fiber shock | +28% (2022–23) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Lululemon Athletica, identifying disruptive substitutes, supplier/buyer power, and market dynamics that protect its premium brand and profitability.

Compact Porter's Five Forces view for Lululemon—quickly assess competitive rivalry, supplier/buyer power, threat of substitutes/entrants, and regulatory pressure to inform strategic moves.

Customers Bargaining Power

Low Switching Costs in Premium Apparel

Customers face low switching costs in premium apparel and can move to Alo Yoga or Vuori with little financial or functional effort; U.S. athleisure market share shows top rivals grew by 6–8% in 2024 while Lululemon grew ~5% (FY2024 revenue $8.1B), highlighting active competition.

No long-term contracts exist for clothing, so brand loyalty is the main barrier to churn; Lululemon reports repeat-buy rates above 60% in 2024, so loyalty must be earned and reinforced.

This forces Lululemon to keep innovating—R&D and product development plus premium materials—so it can justify premium prices and maintain gross margin (FY2024 gross margin 57%).

High Transparency and Digital Comparison

Modern shoppers use social media and e-commerce to compare Lululemon prices, reviews, and specs in real time; 72% of US consumers said online reviews influence purchases in 2024, raising customer leverage. This digital literacy lets buyers demand value and hold Lululemon accountable for quality or service lapses—online complaints can cut net promoter score quickly. Lululemon must keep a seamless omni-channel experience—its 2024 direct-to-consumer sales growth of 20% shows the stake here—to justify premium pricing and defend margins.

Community Engagement and Brand Ecosystem

Lululemon reduces buyer power by building community via ~5,000 global ambassadors and 1,700+ local studio partnerships (2025), turning products into lifestyle signals rather than commodities.

Emotional switching costs cut price sensitivity: management reported a 20% higher repeat purchase rate among members of its loyalty/educational programs in FY2024, lowering price elasticity in core 18–44 fitness demographic.

Influence of the Secondary Resale Market

The rise of platforms like Lululemon Like New and third-party resale sites gives customers more choices and price points, enabling price-sensitive shoppers to buy Lululemon without paying full retail; resale accounted for an estimated 5–7% of Lululemon category volume in 2024 per industry estimates.

Lululemon counters by running its own Like New program, launched 2019 and scaled to 150+ stores by 2024, keeping customer data and CRM control and reducing leakage to competitors.

What this hides: resale can still dilute new-product demand and compress margins if unchecked.

- Resale share ~5–7% (2024 est.)

- Like New in 150+ stores by 2024

- Own platform preserves customer data/CRM

- Resale enables price-sensitive retention, risks margin dilution

Demand for Personalization and Inclusivity

Customers now expect broad size ranges, diverse styles, and tailored experiences; 2024 surveys show 62% of apparel shoppers won't return after poor fit or limited choice, raising buyer power against Lululemon.

Lululemon expanded sizes and categories, and in FY2024 reported digital sales up 32% to $3.1 billion, using analytics and membership data to predict preferences and reduce churn.

Failure to keep pace risks share loss to inclusive rivals who launch faster and cheaper lines.

- 62% of shoppers reject poor fit (2024 survey)

- Digital sales +32% to $3.1B in FY2024

- Analytics-driven inventory to lower churn

Strong loyalty cushions pricing pressure as digital and resale reshape demand

Customers have moderate bargaining power: low switching costs and online comparison raise leverage, but strong brand loyalty (repeat-buy >60% in FY2024) and community programs reduce price sensitivity; resale channels (5–7% est. 2024) and demand for inclusive sizing increase pressure on pricing and assortment.

| Metric | 2024 |

|---|---|

| Revenue | $8.1B |

| Gross margin | 57% |

| Repeat-buy rate | >60% |

| Resale share (est.) | 5–7% |

| Digital sales | $3.1B (+32%) |

Preview the Actual Deliverable

Lululemon Athletica Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Lululemon Athletica you'll receive immediately after purchase—no placeholders or samples; the complete, professionally formatted document is ready for download and use the moment you buy.