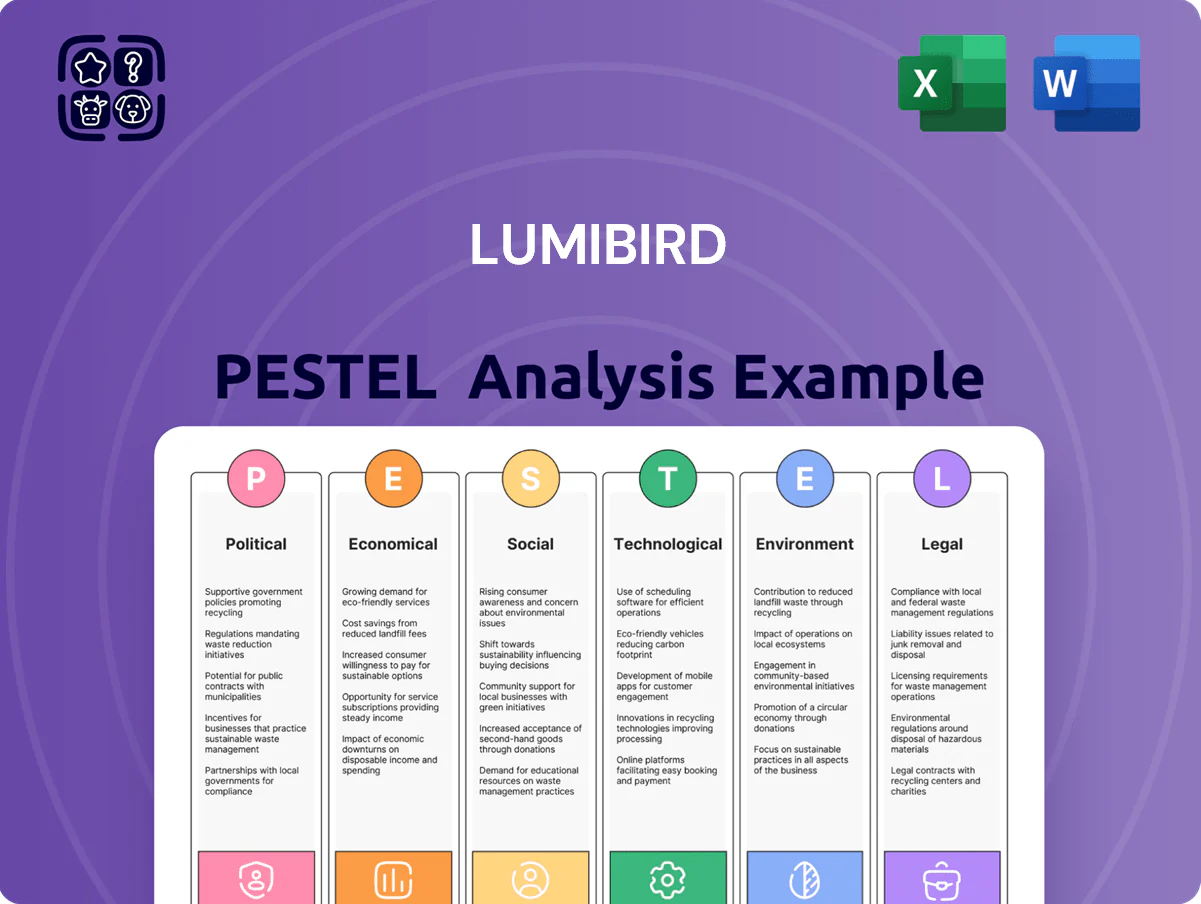

Lumibird PESTLE Analysis

Skip the Research. Get the Strategy.

Understand how political shifts, economic cycles, and rapid photonics innovations are shaping Lumibird’s prospects with our concise PESTLE snapshot—perfect for investors and strategists. This ready-to-use analysis highlights regulatory risks, market drivers, and sustainability trends that could affect valuation and strategy. Purchase the full PESTLE to access the complete, editable report and actionable recommendations for confident decision-making.

Political factors

Increased European Defense Autonomy

Rising EU strategic autonomy pushed total European defense spending up about 8% cumulatively 2021–2025, with 2025 NATO-eligible EU members reaching nearly €320bn; Lumibird gains as a domestic supplier of laser rangefinders, target designators and directed-energy components, capturing higher-margin government work. Procurement rules now favor local vendors—EU content requirements rose, boosting Lumibird’s defense revenue share and order book visibility into 2026.

Export Controls on Dual-Use Photonics

Geopolitical tensions have tightened export licenses for high-performance lasers, with EU and US dual-use controls expanding in 2023–2025 and penalties up to €1.8M or 4% of turnover for breaches; Lumibird reported €302M revenue in 2024 and must factor compliance costs into margins. Lumibird must navigate approvals for sales beyond NATO allies, where processing times can exceed six months and denial rates rose ~15% in 2024 for sensitive optoelectronics. These controls force Lumibird to implement rigorous compliance frameworks, audit trails, and IP segmentation to prevent unauthorized transfer of sensitive photonics technology.

Sovereign Technology Subsidies

European and North American governments committed over $150 billion in 2024–2025 to semiconductor and photonics subsidies, enabling Lumibird to secure multi-million euro R&D grants—including France’s Plan d’Investissement and the EU’s IPCEI frameworks—to advance next‑gen fiber lasers. These funds help Lumibird reduce exposure to Asian supply chains while supporting a competitive hardware roadmap and capacity investments that align with regional strategic tech sovereignty goals.

Geopolitical Trade Restrictions

Geopolitical trade restrictions and tariffs between blocs have pushed silica and rare-earth oxide costs up ~15–25% since 2022, increasing finished laser-system input costs and squeezing margins for suppliers like Lumibird.

Lumibird’s supply chain is exposed to import controls on specialized glass and rare-earth elements; ~30% of critical components originate outside the EU, heightening policy sensitivity.

Strategic placement of factories in France, the US and Malaysia reduces localized protectionism risk and supports resilience amid rising global tariff uncertainty.

- Input-cost rise: +15–25% (2022–2025)

- Critical imports: ~30% sourced outside EU

- Manufacturing footprint: France, US, Malaysia

National Security Procurement Protocols

Lumibird’s photonics are integral to aerospace and telecom, triggering strict EU and NATO procurement checks on vendor ownership; Lumibird reports 68% of 2024 defense-related revenues tied to vetted contracts, reflecting compliance with national security protocols.

Adherence to these standards secures Lumibird’s role in critical infrastructure projects, bolstering trust with government clients and creating regulatory barriers that limit non-European entrants; the company’s 2024 backlog included €120m in secured strategic contracts.

- 68% of 2024 defense-related revenue from vetted contracts

- €120m secured strategic-contract backlog in 2024

- Regulatory vetting and ownership rules hinder non-EU competitors

EU defense boom fuels Lumibird—€320bn NATO boost, €120m backlog, rising compliance costs

EU defense spending up ~8% (2021–25) and €320bn NATO-eligible 2025 boost Lumibird’s gov’t sales; 68% of 2024 defense revenue from vetted contracts and €120m secured backlog. Export controls tightened 2023–25, denial rates +15% in 2024 and fines up to €1.8m/4% turnover, raising compliance costs. Subsidies >€150bn (2024–25) and IPCEI grants support R&D; input costs +15–25% (2022–25) with ~30% critical imports outside EU.

| Metric | Value |

|---|---|

| EU defense spend change (2021–25) | +8% |

| NATO-eligible EU (2025) | €320bn |

| Lumibird defense revenue vetted (2024) | 68% |

| Secured backlog (2024) | €120m |

| Export denial rate change (2024) | +15% |

| Subsidies committed (2024–25) | €150bn+ |

| Input-cost rise (2022–25) | +15–25% |

| Critical imports outside EU | ~30% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Lumibird across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and current trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Concise, PESTLE-segmented summary of Lumibird’s external landscape that’s easily dropped into presentations or shared across teams to speed strategic alignment and risk discussions.

Economic factors

Industrial Automation Investment Trends

Rising global labor costs have accelerated investments in laser-based automation; the industrial laser market grew 6.8% in 2024 to about USD 11.2bn, boosting demand for Lumibird systems for cutting, marking and welding.

Automotive and aerospace modernization—CAPEX up ~4–7% in 2024—sustains orders for high-precision lasers, supporting Lumibird recurring revenue streams.

This shift to high-tech manufacturing helps offset consumer-market volatility, stabilizing Lumibird EBITDA margins through 2024–25.

Global Supply Chain Resilience

While global disruptions have eased, maintaining resilient supply chains still adds cost; Lumibird widened its supplier base and raised safety stocks of laser diodes, increasing inventory days to ~98 DIO in 2024 versus 78 in 2019, tying up roughly €45–60m more working capital (2024 est.), which cushions localized shocks but compresses free cash flow and requires tighter cash conversion cycle management.

Currency Volatility in Export Markets

As a company with significant international sales, Lumibird faces exposure to EUR/USD and EUR/JPY swings; EUR appreciated ~3% vs USD in 2024, affecting reported revenues for FY2024 where ~60% of sales were outside the eurozone. Financial hedging—forwards, options, and natural hedges—is essential: industry peers hedge 40–70% of FX exposure to protect EBITDA margins. Economic instability in emerging markets (e.g., 2024 GDP contractions in parts of Latin America ~0.5–1.5%) can reduce distributor purchasing power and delay orders. Rapid FX shifts can swing quarterly margins by several percentage points, so active treasury management is critical.

Rising R&D Capital Requirements

The photonics sector's rapid innovation requires rising R&D spend; global photonics R&D grew ~6% YoY in 2024, pushing Lumibird to increase R&D investment (2023 R&D ~€22m, ~8% of revenue) to remain competitive.

Economic pressure to preserve margins while funding costly lab equipment and specialized talent compresses free cash flow; EU-27 inflation-adjusted capex rose ~4% in 2024, tightening budgets.

Lumibird must reallocate capital between near-term operations and long-term breakthroughs, prioritizing projects with >15% IRR and leveraging partnerships or grants to mitigate funding strain.

- 2023 R&D ~€22m (~8% revenue)

- Photonics R&D growth ~6% YoY (2024)

- Target project hurdle >15% IRR

- Use grants/partnerships to reduce capex burden

Interest Rate Stabilization Impacts

The stabilization of global policy rates by end-2025 — ECB at 3.25% and Fed at 5.25% — has restored predictability for Lumibird’s five-year capex and M&A planning in lasers and photonics.

Lower borrowing costs versus 2022 peak inflation reduce average group interest expense; a 1.5 percentage-point drop can cut annual financing costs on a €150m debt by ~€2.25m, aiding expansion in medical and industrial segments.

- ECB 3.25% / Fed 5.25% (end-2025)

- Estimated financing saving ~€2.25m on €150m debt per 1.5pp drop

- Enables multi-year capex and targeted acquisitions

Lumibird: Industrial laser growth, rising photonics R&D, FX & inventory impact

Economic tailwinds for Lumibird include a 2024 industrial laser market at ~USD 11.2bn (+6.8%), rising photonics R&D (+6% YoY) and stabilized rates (ECB 3.25%, Fed 5.25% end-2025) improving capex/M&A visibility; higher inventory (98 DIO vs 78 in 2019) ties ~€45–60m working capital, EUR up ~3% vs USD in 2024 affecting ~60% non-euro sales, and 2023 R&D ≈€22m (~8% revenue).

| Metric | 2024/2023 |

|---|---|

| Industrial laser mkt | USD 11.2bn (+6.8%) |

| Photonics R&D | +6% YoY |

| Inventory days | 98 DIO (2019:78) |

| R&D spend | €22m (~8% rev) |

| EUR vs USD | +3% (2024) |

Preview Before You Purchase

Lumibird PESTLE Analysis

The preview shown here is the exact Lumibird PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making. The layout, content, and findings visible in this sample are the final file you’ll download immediately after checkout, with no placeholders or surprises. Use it as-is for presentations, reports, or further analysis.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Understand how political shifts, economic cycles, and rapid photonics innovations are shaping Lumibird’s prospects with our concise PESTLE snapshot—perfect for investors and strategists. This ready-to-use analysis highlights regulatory risks, market drivers, and sustainability trends that could affect valuation and strategy. Purchase the full PESTLE to access the complete, editable report and actionable recommendations for confident decision-making.

Political factors

Increased European Defense Autonomy

Rising EU strategic autonomy pushed total European defense spending up about 8% cumulatively 2021–2025, with 2025 NATO-eligible EU members reaching nearly €320bn; Lumibird gains as a domestic supplier of laser rangefinders, target designators and directed-energy components, capturing higher-margin government work. Procurement rules now favor local vendors—EU content requirements rose, boosting Lumibird’s defense revenue share and order book visibility into 2026.

Export Controls on Dual-Use Photonics

Geopolitical tensions have tightened export licenses for high-performance lasers, with EU and US dual-use controls expanding in 2023–2025 and penalties up to €1.8M or 4% of turnover for breaches; Lumibird reported €302M revenue in 2024 and must factor compliance costs into margins. Lumibird must navigate approvals for sales beyond NATO allies, where processing times can exceed six months and denial rates rose ~15% in 2024 for sensitive optoelectronics. These controls force Lumibird to implement rigorous compliance frameworks, audit trails, and IP segmentation to prevent unauthorized transfer of sensitive photonics technology.

Sovereign Technology Subsidies

European and North American governments committed over $150 billion in 2024–2025 to semiconductor and photonics subsidies, enabling Lumibird to secure multi-million euro R&D grants—including France’s Plan d’Investissement and the EU’s IPCEI frameworks—to advance next‑gen fiber lasers. These funds help Lumibird reduce exposure to Asian supply chains while supporting a competitive hardware roadmap and capacity investments that align with regional strategic tech sovereignty goals.

Geopolitical Trade Restrictions

Geopolitical trade restrictions and tariffs between blocs have pushed silica and rare-earth oxide costs up ~15–25% since 2022, increasing finished laser-system input costs and squeezing margins for suppliers like Lumibird.

Lumibird’s supply chain is exposed to import controls on specialized glass and rare-earth elements; ~30% of critical components originate outside the EU, heightening policy sensitivity.

Strategic placement of factories in France, the US and Malaysia reduces localized protectionism risk and supports resilience amid rising global tariff uncertainty.

- Input-cost rise: +15–25% (2022–2025)

- Critical imports: ~30% sourced outside EU

- Manufacturing footprint: France, US, Malaysia

National Security Procurement Protocols

Lumibird’s photonics are integral to aerospace and telecom, triggering strict EU and NATO procurement checks on vendor ownership; Lumibird reports 68% of 2024 defense-related revenues tied to vetted contracts, reflecting compliance with national security protocols.

Adherence to these standards secures Lumibird’s role in critical infrastructure projects, bolstering trust with government clients and creating regulatory barriers that limit non-European entrants; the company’s 2024 backlog included €120m in secured strategic contracts.

- 68% of 2024 defense-related revenue from vetted contracts

- €120m secured strategic-contract backlog in 2024

- Regulatory vetting and ownership rules hinder non-EU competitors

EU defense boom fuels Lumibird—€320bn NATO boost, €120m backlog, rising compliance costs

EU defense spending up ~8% (2021–25) and €320bn NATO-eligible 2025 boost Lumibird’s gov’t sales; 68% of 2024 defense revenue from vetted contracts and €120m secured backlog. Export controls tightened 2023–25, denial rates +15% in 2024 and fines up to €1.8m/4% turnover, raising compliance costs. Subsidies >€150bn (2024–25) and IPCEI grants support R&D; input costs +15–25% (2022–25) with ~30% critical imports outside EU.

| Metric | Value |

|---|---|

| EU defense spend change (2021–25) | +8% |

| NATO-eligible EU (2025) | €320bn |

| Lumibird defense revenue vetted (2024) | 68% |

| Secured backlog (2024) | €120m |

| Export denial rate change (2024) | +15% |

| Subsidies committed (2024–25) | €150bn+ |

| Input-cost rise (2022–25) | +15–25% |

| Critical imports outside EU | ~30% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Lumibird across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and current trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Concise, PESTLE-segmented summary of Lumibird’s external landscape that’s easily dropped into presentations or shared across teams to speed strategic alignment and risk discussions.

Economic factors

Industrial Automation Investment Trends

Rising global labor costs have accelerated investments in laser-based automation; the industrial laser market grew 6.8% in 2024 to about USD 11.2bn, boosting demand for Lumibird systems for cutting, marking and welding.

Automotive and aerospace modernization—CAPEX up ~4–7% in 2024—sustains orders for high-precision lasers, supporting Lumibird recurring revenue streams.

This shift to high-tech manufacturing helps offset consumer-market volatility, stabilizing Lumibird EBITDA margins through 2024–25.

Global Supply Chain Resilience

While global disruptions have eased, maintaining resilient supply chains still adds cost; Lumibird widened its supplier base and raised safety stocks of laser diodes, increasing inventory days to ~98 DIO in 2024 versus 78 in 2019, tying up roughly €45–60m more working capital (2024 est.), which cushions localized shocks but compresses free cash flow and requires tighter cash conversion cycle management.

Currency Volatility in Export Markets

As a company with significant international sales, Lumibird faces exposure to EUR/USD and EUR/JPY swings; EUR appreciated ~3% vs USD in 2024, affecting reported revenues for FY2024 where ~60% of sales were outside the eurozone. Financial hedging—forwards, options, and natural hedges—is essential: industry peers hedge 40–70% of FX exposure to protect EBITDA margins. Economic instability in emerging markets (e.g., 2024 GDP contractions in parts of Latin America ~0.5–1.5%) can reduce distributor purchasing power and delay orders. Rapid FX shifts can swing quarterly margins by several percentage points, so active treasury management is critical.

Rising R&D Capital Requirements

The photonics sector's rapid innovation requires rising R&D spend; global photonics R&D grew ~6% YoY in 2024, pushing Lumibird to increase R&D investment (2023 R&D ~€22m, ~8% of revenue) to remain competitive.

Economic pressure to preserve margins while funding costly lab equipment and specialized talent compresses free cash flow; EU-27 inflation-adjusted capex rose ~4% in 2024, tightening budgets.

Lumibird must reallocate capital between near-term operations and long-term breakthroughs, prioritizing projects with >15% IRR and leveraging partnerships or grants to mitigate funding strain.

- 2023 R&D ~€22m (~8% revenue)

- Photonics R&D growth ~6% YoY (2024)

- Target project hurdle >15% IRR

- Use grants/partnerships to reduce capex burden

Interest Rate Stabilization Impacts

The stabilization of global policy rates by end-2025 — ECB at 3.25% and Fed at 5.25% — has restored predictability for Lumibird’s five-year capex and M&A planning in lasers and photonics.

Lower borrowing costs versus 2022 peak inflation reduce average group interest expense; a 1.5 percentage-point drop can cut annual financing costs on a €150m debt by ~€2.25m, aiding expansion in medical and industrial segments.

- ECB 3.25% / Fed 5.25% (end-2025)

- Estimated financing saving ~€2.25m on €150m debt per 1.5pp drop

- Enables multi-year capex and targeted acquisitions

Lumibird: Industrial laser growth, rising photonics R&D, FX & inventory impact

Economic tailwinds for Lumibird include a 2024 industrial laser market at ~USD 11.2bn (+6.8%), rising photonics R&D (+6% YoY) and stabilized rates (ECB 3.25%, Fed 5.25% end-2025) improving capex/M&A visibility; higher inventory (98 DIO vs 78 in 2019) ties ~€45–60m working capital, EUR up ~3% vs USD in 2024 affecting ~60% non-euro sales, and 2023 R&D ≈€22m (~8% revenue).

| Metric | 2024/2023 |

|---|---|

| Industrial laser mkt | USD 11.2bn (+6.8%) |

| Photonics R&D | +6% YoY |

| Inventory days | 98 DIO (2019:78) |

| R&D spend | €22m (~8% rev) |

| EUR vs USD | +3% (2024) |

Preview Before You Purchase

Lumibird PESTLE Analysis

The preview shown here is the exact Lumibird PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making. The layout, content, and findings visible in this sample are the final file you’ll download immediately after checkout, with no placeholders or surprises. Use it as-is for presentations, reports, or further analysis.