Lundin Mining Marketing Mix

Ready-Made Marketing Analysis, Ready to Use

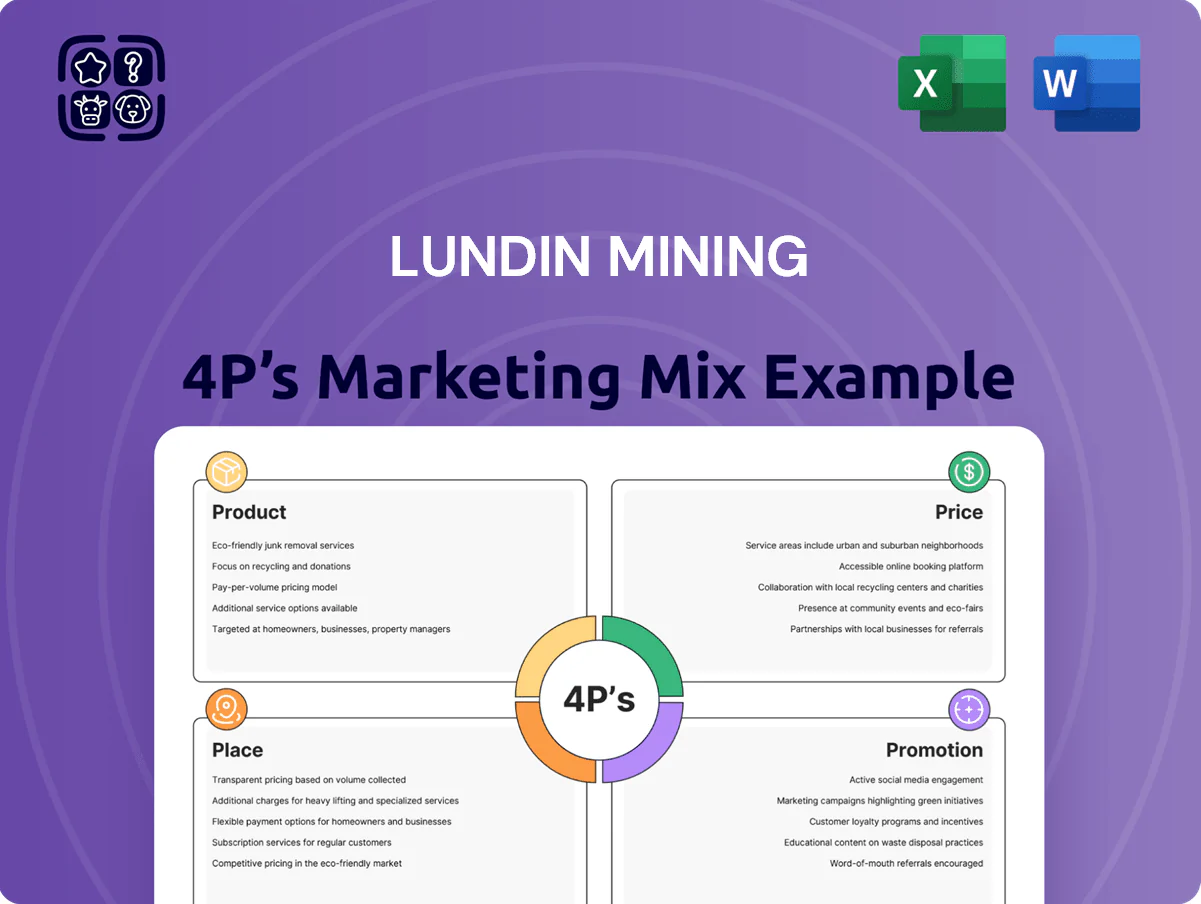

Lundin Mining’s 4P’s reveal a strategic blend of product diversification, value-driven pricing, targeted channel placement, and stakeholder-focused promotion that drives resilience in cyclical metals markets—download the full, editable Marketing Mix Analysis to see detailed data, channel maps, and tactical recommendations.

Product

Copper Concentrates and Cathodes

As of late 2025, copper drives ~62% of Lundin Mining’s revenue, with Candelaria (Chile) and Caserones (Chile) producing ~430 kt Cu in concentrate and cathode combined in 2024–25, supporting group 2025 guidance. The company supplies high-grade concentrates and cathodes meeting ISO and smelter specs, used in EV motors, batteries, and grid infrastructure. Average realized copper price was about $9,200/t in 2025 YTD, boosting margins and cash flow for ongoing expansion projects.

Zinc and Lead Production

Nickel for Battery Chemistry

Lundin Mining sells high-purity nickel concentrate from Eagle Mine (Michigan), supplying North American lithium-ion battery makers and chemical processors; Eagle produced ~35,000 tonnes of nickel-in-concentrate in 2024, targeting rising EV battery demand and US IRA supply-shift incentives. The concentrate’s low impurity profile boosts offtake value—market premiums of ~5–12% vs benchmark Class I nickel in 2024—and also attracts stainless-steel buyers.

Gold and Silver By-products

- 2024 contribution: ~8–12% of revenue

- Incremental cost: low, boosts margins

- Sold in concentrates to refiners

- Hedge: gold +6% in 2024 vs USD

Exploration and Resource Development

Lundin Mining's Exploration and Resource Development product is its pipeline of projects and reserve expansions, notably Vicuña, which at end-2024 added ~120 Mt of inferred resources and is expected to extend LOM (life of mine) across the portfolio by 8–12 years, boosting attributable contained copper by ~350 kt.

By de-risking deposits and advancing feasibility, Lundin increases long-term cashflow visibility and secures base-metal supply, supporting NAV upside and stakeholder value over multiple decades.

- Vicuña ~120 Mt inferred (end-2024)

- Estimated +350 kt contained Cu

- LOM extension ~8–12 years

- Improves NAV and long-term cashflow

Lundin Mining: Copper-led mix (~62% revenue), zinc & nickel significant; Vicuña adds ~8–12yr LOM

Lundin Mining’s product mix in 2024–25: copper ~62% revenue (~430 kt Cu from Candelaria+Caserones 2024–25), zinc ~35% payable metal (~180 kt Zn concentrate 2024), nickel ~35 kt Ni-in-conc (Eagle 2024) and precious metals 8–12% revenue (2024); Vicuña added ~120 Mt inferred (+~350 kt Cu) extending LOM ~8–12 yrs.

| Product | 2024–25 Qty | Rev/% | Key note |

|---|---|---|---|

| Copper | ~430 kt | ~62% | Candelaria+Caserones |

| Zinc | ~180 kt | ~35% payable | Neves-Corvo+Zinkgruvan |

| Nickel | ~35 kt Ni | — | Eagle; battery demand |

| Precious metals | — | 8–12% | By-product; low incremental cost |

| Pipeline | Vicuña ~120 Mt | — | +~350 kt Cu; +8–12 yrs LOM |

What is included in the product

Delivers a concise, company-specific deep dive into Lundin Mining’s Product, Price, Place, and Promotion strategies, ideal for managers, consultants, and marketers needing a clear breakdown of the company’s market positioning grounded in real practices and competitive context.

Condenses Lundin Mining’s 4P insights into a concise, at-a-glance summary to speed leadership briefings and decision-making.

Place

Candelaria and Caserones Operations in Chile

Candelaria and Caserones in Chile's Atacama give Lundin Mining a strong foothold in a top mining jurisdiction; combined 2024 copper production was ~230 kt Cu eq and proved-and-probable reserves were ~5.8 Mt Cu (2024 company reports). Proximity to ports like Antofagasta and Mejillones cuts freight costs and enables steady exports to Asia and Europe. Shared roads, power links, and high-altitude expertise lower operating costs and raise uptime.

European Assets in Portugal and Sweden

Neves-Corvo (Portugal) and Zinkgruvan (Sweden) give Lundin Mining direct access to Europe’s industrial heartland, cutting average road/rail shipping distances to continental smelters by ~30–50% versus Atlantic/overseas sources. In 2024 Lundin’s European output supplied ~40% of its payable copper and zinc, trimming logistics spend and CO2 from transport; EU operations comply with strict EU ETS and REACH rules, raising capital and permit certainty.

North American Presence via Eagle Mine

The Eagle Mine in Michigan supplies nickel and copper domestically, producing about 30,000 tonnes of nickel and 10,000 tonnes of copper in concentrate annually as of 2024, supporting US supply security for batteries and alloys.

Its location near the Midwest industrial corridor and auto hubs in Michigan and Ohio shortens lead times; trucking reduces transit to manufacturers by ~20% versus coastal imports.

Concentrates move via integrated road and Norfolk Southern rail links to processors, cutting logistics costs and CO2 per tonne by roughly 15% versus longer import routes.

Chapada Mine in Brazil

- 2024: ~83 kt Cu, 80 koz Au

- ~1,200 workforce

- Ilhéus port access; paved roads

- Market: Brazil domestic + Asia/Europe exports

Global Distribution and Logistics Networks

Lundin Mining moves concentrates via rail, truck and sea from remote sites to smelters, reporting 2024 shipping volumes of ~8.2 Mt of concentrate and freight costs of $214m, linking mines in Chile, Portugal and Sweden to global hubs.

They hold contracts with major logistics firms to cut lead times and had a 2024 on-time delivery rate of 94%, prioritizing China (40% of shipments) and the Eurozone (28%).

- 2024 volume ~8.2 Mt

- Freight cost $214m (2024)

- On-time delivery 94% (2024)

- China 40% of exports; Eurozone 28%

Lundin Mining cuts freight to $214M on 8.2Mt shipped; 94% OT, China 40% EU 28%

Lundin Mining’s site mix (Chile, Portugal, Sweden, US, Brazil) cut 2024 freight costs to $214m on ~8.2 Mt shipped, with 94% on-time delivery; 40% exports to China, 28% to Eurozone. Chile produced ~230 kt Cu eq (reserves ~5.8 Mt Cu); Chapada ~83 kt Cu/80 koz Au; Eagle ~30 kt Ni/10 kt Cu; Europe supplied ~40% payable Cu/Zn.

| Site | 2024 output | Key logistics |

|---|---|---|

| Chile (Candelaria/Caserones) | ~230 kt Cu eq; reserves ~5.8 Mt Cu | Ports Antofagasta/Mejillones |

| Portugal/Sweden | ~40% payable Cu/Zn | 30–50% shorter rail/road |

| US (Eagle) | 30 kt Ni; 10 kt Cu | Midwest corridor, Norfolk Southern |

| Brazil (Chapada) | ~83 kt Cu; 80 koz Au | Ilhéus port, paved roads |

| Group logistics | ~8.2 Mt shipped; $214m freight; 94% OT | China 40%; EU 28% |

Full Version Awaits

Lundin Mining 4P's Marketing Mix Analysis

The preview shown here is the actual Lundin Mining 4P's Marketing Mix document you’ll receive instantly after purchase—fully complete, editable, and ready to use with no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Ready-Made Marketing Analysis, Ready to Use

Lundin Mining’s 4P’s reveal a strategic blend of product diversification, value-driven pricing, targeted channel placement, and stakeholder-focused promotion that drives resilience in cyclical metals markets—download the full, editable Marketing Mix Analysis to see detailed data, channel maps, and tactical recommendations.

Product

Copper Concentrates and Cathodes

As of late 2025, copper drives ~62% of Lundin Mining’s revenue, with Candelaria (Chile) and Caserones (Chile) producing ~430 kt Cu in concentrate and cathode combined in 2024–25, supporting group 2025 guidance. The company supplies high-grade concentrates and cathodes meeting ISO and smelter specs, used in EV motors, batteries, and grid infrastructure. Average realized copper price was about $9,200/t in 2025 YTD, boosting margins and cash flow for ongoing expansion projects.

Zinc and Lead Production

Nickel for Battery Chemistry

Lundin Mining sells high-purity nickel concentrate from Eagle Mine (Michigan), supplying North American lithium-ion battery makers and chemical processors; Eagle produced ~35,000 tonnes of nickel-in-concentrate in 2024, targeting rising EV battery demand and US IRA supply-shift incentives. The concentrate’s low impurity profile boosts offtake value—market premiums of ~5–12% vs benchmark Class I nickel in 2024—and also attracts stainless-steel buyers.

Gold and Silver By-products

- 2024 contribution: ~8–12% of revenue

- Incremental cost: low, boosts margins

- Sold in concentrates to refiners

- Hedge: gold +6% in 2024 vs USD

Exploration and Resource Development

Lundin Mining's Exploration and Resource Development product is its pipeline of projects and reserve expansions, notably Vicuña, which at end-2024 added ~120 Mt of inferred resources and is expected to extend LOM (life of mine) across the portfolio by 8–12 years, boosting attributable contained copper by ~350 kt.

By de-risking deposits and advancing feasibility, Lundin increases long-term cashflow visibility and secures base-metal supply, supporting NAV upside and stakeholder value over multiple decades.

- Vicuña ~120 Mt inferred (end-2024)

- Estimated +350 kt contained Cu

- LOM extension ~8–12 years

- Improves NAV and long-term cashflow

Lundin Mining: Copper-led mix (~62% revenue), zinc & nickel significant; Vicuña adds ~8–12yr LOM

Lundin Mining’s product mix in 2024–25: copper ~62% revenue (~430 kt Cu from Candelaria+Caserones 2024–25), zinc ~35% payable metal (~180 kt Zn concentrate 2024), nickel ~35 kt Ni-in-conc (Eagle 2024) and precious metals 8–12% revenue (2024); Vicuña added ~120 Mt inferred (+~350 kt Cu) extending LOM ~8–12 yrs.

| Product | 2024–25 Qty | Rev/% | Key note |

|---|---|---|---|

| Copper | ~430 kt | ~62% | Candelaria+Caserones |

| Zinc | ~180 kt | ~35% payable | Neves-Corvo+Zinkgruvan |

| Nickel | ~35 kt Ni | — | Eagle; battery demand |

| Precious metals | — | 8–12% | By-product; low incremental cost |

| Pipeline | Vicuña ~120 Mt | — | +~350 kt Cu; +8–12 yrs LOM |

What is included in the product

Delivers a concise, company-specific deep dive into Lundin Mining’s Product, Price, Place, and Promotion strategies, ideal for managers, consultants, and marketers needing a clear breakdown of the company’s market positioning grounded in real practices and competitive context.

Condenses Lundin Mining’s 4P insights into a concise, at-a-glance summary to speed leadership briefings and decision-making.

Place

Candelaria and Caserones Operations in Chile

Candelaria and Caserones in Chile's Atacama give Lundin Mining a strong foothold in a top mining jurisdiction; combined 2024 copper production was ~230 kt Cu eq and proved-and-probable reserves were ~5.8 Mt Cu (2024 company reports). Proximity to ports like Antofagasta and Mejillones cuts freight costs and enables steady exports to Asia and Europe. Shared roads, power links, and high-altitude expertise lower operating costs and raise uptime.

European Assets in Portugal and Sweden

Neves-Corvo (Portugal) and Zinkgruvan (Sweden) give Lundin Mining direct access to Europe’s industrial heartland, cutting average road/rail shipping distances to continental smelters by ~30–50% versus Atlantic/overseas sources. In 2024 Lundin’s European output supplied ~40% of its payable copper and zinc, trimming logistics spend and CO2 from transport; EU operations comply with strict EU ETS and REACH rules, raising capital and permit certainty.

North American Presence via Eagle Mine

The Eagle Mine in Michigan supplies nickel and copper domestically, producing about 30,000 tonnes of nickel and 10,000 tonnes of copper in concentrate annually as of 2024, supporting US supply security for batteries and alloys.

Its location near the Midwest industrial corridor and auto hubs in Michigan and Ohio shortens lead times; trucking reduces transit to manufacturers by ~20% versus coastal imports.

Concentrates move via integrated road and Norfolk Southern rail links to processors, cutting logistics costs and CO2 per tonne by roughly 15% versus longer import routes.

Chapada Mine in Brazil

- 2024: ~83 kt Cu, 80 koz Au

- ~1,200 workforce

- Ilhéus port access; paved roads

- Market: Brazil domestic + Asia/Europe exports

Global Distribution and Logistics Networks

Lundin Mining moves concentrates via rail, truck and sea from remote sites to smelters, reporting 2024 shipping volumes of ~8.2 Mt of concentrate and freight costs of $214m, linking mines in Chile, Portugal and Sweden to global hubs.

They hold contracts with major logistics firms to cut lead times and had a 2024 on-time delivery rate of 94%, prioritizing China (40% of shipments) and the Eurozone (28%).

- 2024 volume ~8.2 Mt

- Freight cost $214m (2024)

- On-time delivery 94% (2024)

- China 40% of exports; Eurozone 28%

Lundin Mining cuts freight to $214M on 8.2Mt shipped; 94% OT, China 40% EU 28%

Lundin Mining’s site mix (Chile, Portugal, Sweden, US, Brazil) cut 2024 freight costs to $214m on ~8.2 Mt shipped, with 94% on-time delivery; 40% exports to China, 28% to Eurozone. Chile produced ~230 kt Cu eq (reserves ~5.8 Mt Cu); Chapada ~83 kt Cu/80 koz Au; Eagle ~30 kt Ni/10 kt Cu; Europe supplied ~40% payable Cu/Zn.

| Site | 2024 output | Key logistics |

|---|---|---|

| Chile (Candelaria/Caserones) | ~230 kt Cu eq; reserves ~5.8 Mt Cu | Ports Antofagasta/Mejillones |

| Portugal/Sweden | ~40% payable Cu/Zn | 30–50% shorter rail/road |

| US (Eagle) | 30 kt Ni; 10 kt Cu | Midwest corridor, Norfolk Southern |

| Brazil (Chapada) | ~83 kt Cu; 80 koz Au | Ilhéus port, paved roads |

| Group logistics | ~8.2 Mt shipped; $214m freight; 94% OT | China 40%; EU 28% |

Full Version Awaits

Lundin Mining 4P's Marketing Mix Analysis

The preview shown here is the actual Lundin Mining 4P's Marketing Mix document you’ll receive instantly after purchase—fully complete, editable, and ready to use with no surprises.