LXP Business Model Canvas

Download LXP’s Complete Business Model Canvas: Ready Template to Plan, Pitch & Scale

Unlock LXP’s strategic playbook with our full Business Model Canvas—an actionable, section-by-section breakdown of value propositions, customer segments, revenue streams, and cost structure. Perfect for entrepreneurs, investors, and consultants who want a ready-to-use, editable template in Word and Excel to benchmark, plan, or pitch. Download the complete canvas to see how LXP scales and where the biggest opportunities lie.

Partnerships

Institutional Joint Venture Partners

LXP forms institutional joint ventures with sovereign wealth funds and global insurers—e.g., 2024 co-investments totaling $1.2B—to co-fund mega logistics hubs, letting the REIT apply its asset-management expertise while cutting direct capital exposure to costly developments. This approach preserves portfolio diversification and supports pursuit of 100k+ sqm facilities in top-tier markets without overconcentrating balance-sheet risk.

Commercial Real Estate Brokerage Firms

The company keeps close ties with national brokerages CBRE, JLL, and Cushman & Wakefield to source off-market deals and capture tenant moves; these firms reported handling roughly 60% of US institutional CRE transactions in 2024, giving LXP preferential access to ~$2.1B in vetted opportunities. By end-2025, these partnerships will be critical to sustaining 95%+ portfolio occupancy via proactive tenant sourcing informed by localized demand shifts.

General Contractors and Developers

LXP relies on trusted general contractors and developers to deliver Class A industrial space on schedule and budget; in 2024 contractors helped complete 3.2M sq ft of LXP projects with average cost variance under 3%, meeting e-commerce specs for clear heights ≥36 ft and 50+ dock doors. Strong developer ties secure land and labor in Sunbelt markets—Texas, Florida, Arizona—where LXP saw 18% revenue growth in 2024.

Financial Institutions and Lenders

Long-standing ties with major investment banks give LXP access to $500M+ in revolving credit and term facilities, enabling rapid bolt-on acquisitions when market windows open; in 2025 LXP used $120M of revolver capacity to close two deals within 45 days.

Maintaining a strong credit profile (net leverage ~3.0x, interest coverage >4x) lets LXP refinance at competitive spreads—recently locking a 5-year term at SOFR+325bps despite 2024–25 rate volatility.

- Revolver capacity: $500M+

- 2025 bolt-on spend: $120M used

- Net leverage: ~3.0x

- Interest coverage: >4x

- Recent refinance: 5y at SOFR+325bps

Municipal and Local Authorities

Engaging municipal and local authorities secures zoning approvals and tax incentives—critical when a 1M+ sq ft distribution hub can save 3–7% in property taxes via PILOTs (payments in lieu of taxes) and unlock $10–50M in infrastructure grants per project as of 2025.

These partnerships speed permitting (median reduction 30% vs. standalone approvals in 2024), smooth utility hookups, and lower regulatory risk for LXP’s long-term operations near metro areas.

- Zoning approvals: required for 1M+ sq ft sites

- Tax incentives: 3–7% property tax savings typical

- Infrastructure grants: $10–50M possible

- Permitting time cut: ~30% faster (2024 median)

- Reduces regulatory and utility hookup risk

LXP scales 100k+ sqm hubs with $1.2B JV, $500M revolver, 3.0x leverage, 4x coverage

LXP leverages JV capital ($1.2B in 2024) and $500M+ revolver access to pursue 100k+ sqm hubs, keeping net leverage ~3.0x and interest coverage >4x; broker ties (CBRE/JLL/Cushman) sourced ~$2.1B opportunities in 2024 while contractors delivered 3.2M sq ft with <3% cost variance; municipal incentives cut taxes 3–7% and unlocked $10–50M grants, shortening permits ~30% (2024).

| Metric | 2024–25 |

|---|---|

| JV co-invest | $1.2B |

| Brokered opps | $2.1B |

| Revolver | $500M+ |

| Permitting cut | ~30% |

What is included in the product

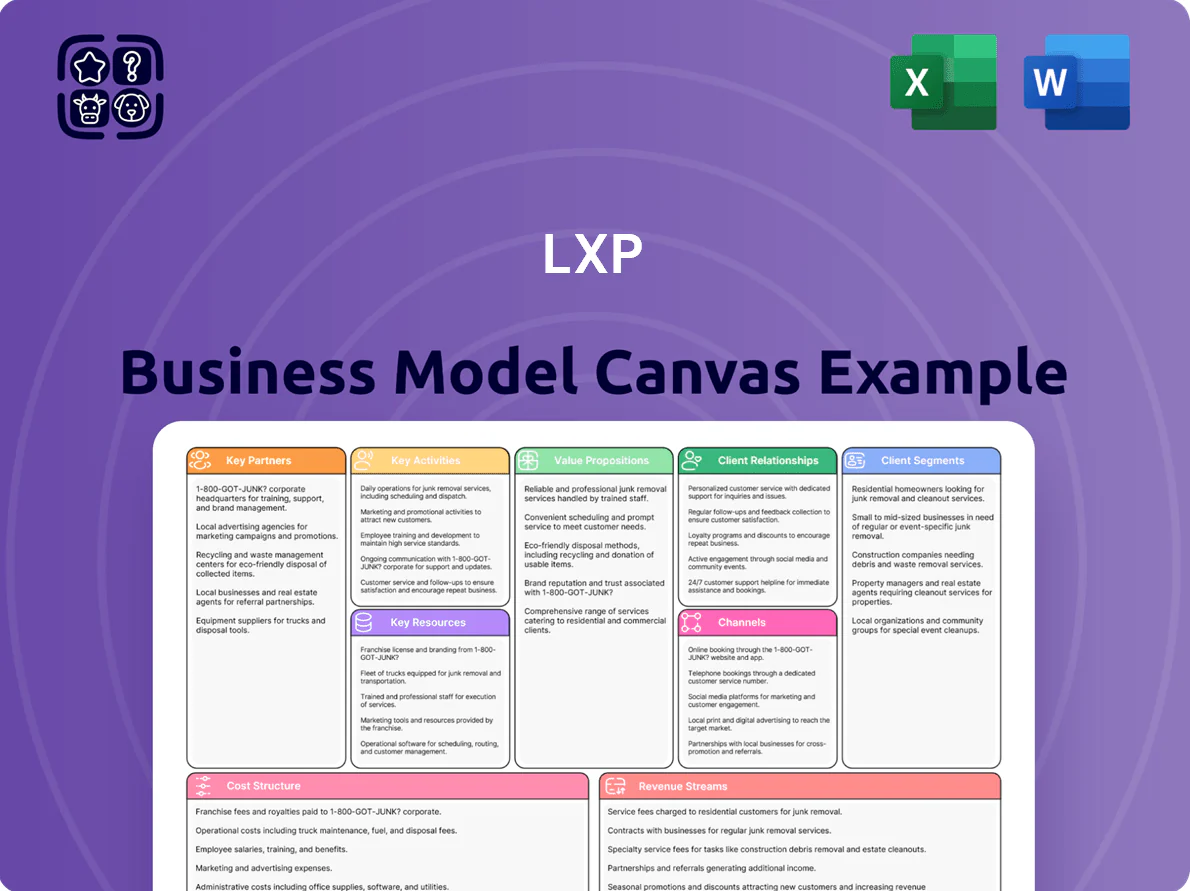

A ready-to-use LXP Business Model Canvas detailing customer segments, value propositions, channels, revenue streams, key partners and activities across 9 BMC blocks, with competitive analysis, SWOT-linked insights and practical metrics to support presentations, funding discussions and strategic decision-making.

Condenses the LXP business model into a single editable canvas, saving hours of structure-building while enabling teams to quickly compare, adapt, and present core strategy for training product decisions.

Activities

Acquisition and Portfolio Management

The team targets single-tenant industrial assets with IRR >12% and initial yields ~6.5%, closing 48 deals worth $1.2bn in 2024; ongoing portfolio reviews prioritize holding top-quartile performers and selling legacy office stock, aiming to recycle ~$400m–$600m of capital by year-end 2025 to complete the shift to a pure-play industrial portfolio.

Ground-Up Property Development

LXP develops new industrial facilities end-to-end—land entitlement, design, and construction oversight—to capture yields ~200–400 bps above acquisition returns; in 2024 LXP’s ground-up projects targeted IRRs of 12–18% versus 8–10% for stabilized buys.

Lease Negotiation and Asset Enhancement

The REIT secures long-term triple-net leases with investment-grade tenants to lock predictable cash flows; as of 2025 core tenant occupancy averages 98% and weighted-average lease term (WALT) is 11.2 years.

Lease talks include CPI-linked or fixed rent escalations to hedge inflation; asset enhancements—warehouse expansions or LED/solar upgrades—raise NAV by ~8–12% per asset and cut operating costs 15–25%.

Strategic Capital Allocation

Decision-makers at LXP balance dividends and reinvestment by comparing after-tax cost of equity (≈9–12% target return) to 2025 average debt cost (~5% for BBB-rated firms) to optimize capital structure and maximize shareholder return.

Maintaining a flexible balance sheet in 2025—target net debt/EBITDA 1.0–2.0—lets LXP weather cycles while funding 15–25% annual R&D and content investments.

- Compare equity (9–12%) vs debt (~5%)

- Target net debt/EBITDA 1.0–2.0

- Allocate 15–25% of cash to R&D/content

- Keep dividend payout ratio adjustable (20–40%)

Investor Relations and Reporting

As a publicly traded REIT, LXP (LXP Industrial Trust, ticker LXP) must keep shareholders, analysts, and the SEC updated via quarterly earnings, 10-Q/10-K filings, and in-person or virtual investor conferences so the market fairly prices its industrial portfolio; in 2025 LXP reported FFO per share of $0.41 in Q4 2024 and total assets of $2.8B as of Dec 31, 2024.

- Quarterly earnings and guidance

- SEC filings: 10-Q, 10-K, 8-K

- Investor conferences and roadshows

- Disclose FFO, same-store NOI, occupancy

LXP: $1.2B in 48 deals, 98% occupancy, 12%+ IRR targets, $0.41 FFO/sh Q4'24

LXP targets single-tenant industrials (IRR >12%, initial yield ~6.5%), closed 48 deals worth $1.2B in 2024, aims to recycle $400–600M by end-2025; ground-up projects target IRR 12–18%; occupancy 98%, WALT 11.2 yrs; net debt/EBITDA 1.0–2.0; dividend payout 20–40%; 2024 FFO/share Q4 $0.41, total assets $2.8B.

| Metric | 2024/2025 |

|---|---|

| Deals | 48; $1.2B |

| IRR (acq/ground-up) | ~12%+/12–18% |

| Occupancy / WALT | 98% / 11.2y |

| Net debt/EBITDA | 1.0–2.0 |

| FFO/share Q4 2024 | $0.41 |

Full Document Unlocks After Purchase

Business Model Canvas

The Business Model Canvas preview shown here is the actual deliverable—not a mockup—and represents the same file you’ll receive after purchase.

When you complete your order, you’ll instantly get the full, editable document formatted exactly as previewed, ready for presentation or customization.

No placeholders or trimmed content—what you see is what you’ll own in both Word and Excel-ready formats.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download LXP’s Complete Business Model Canvas: Ready Template to Plan, Pitch & Scale

Unlock LXP’s strategic playbook with our full Business Model Canvas—an actionable, section-by-section breakdown of value propositions, customer segments, revenue streams, and cost structure. Perfect for entrepreneurs, investors, and consultants who want a ready-to-use, editable template in Word and Excel to benchmark, plan, or pitch. Download the complete canvas to see how LXP scales and where the biggest opportunities lie.

Partnerships

Institutional Joint Venture Partners

LXP forms institutional joint ventures with sovereign wealth funds and global insurers—e.g., 2024 co-investments totaling $1.2B—to co-fund mega logistics hubs, letting the REIT apply its asset-management expertise while cutting direct capital exposure to costly developments. This approach preserves portfolio diversification and supports pursuit of 100k+ sqm facilities in top-tier markets without overconcentrating balance-sheet risk.

Commercial Real Estate Brokerage Firms

The company keeps close ties with national brokerages CBRE, JLL, and Cushman & Wakefield to source off-market deals and capture tenant moves; these firms reported handling roughly 60% of US institutional CRE transactions in 2024, giving LXP preferential access to ~$2.1B in vetted opportunities. By end-2025, these partnerships will be critical to sustaining 95%+ portfolio occupancy via proactive tenant sourcing informed by localized demand shifts.

General Contractors and Developers

LXP relies on trusted general contractors and developers to deliver Class A industrial space on schedule and budget; in 2024 contractors helped complete 3.2M sq ft of LXP projects with average cost variance under 3%, meeting e-commerce specs for clear heights ≥36 ft and 50+ dock doors. Strong developer ties secure land and labor in Sunbelt markets—Texas, Florida, Arizona—where LXP saw 18% revenue growth in 2024.

Financial Institutions and Lenders

Long-standing ties with major investment banks give LXP access to $500M+ in revolving credit and term facilities, enabling rapid bolt-on acquisitions when market windows open; in 2025 LXP used $120M of revolver capacity to close two deals within 45 days.

Maintaining a strong credit profile (net leverage ~3.0x, interest coverage >4x) lets LXP refinance at competitive spreads—recently locking a 5-year term at SOFR+325bps despite 2024–25 rate volatility.

- Revolver capacity: $500M+

- 2025 bolt-on spend: $120M used

- Net leverage: ~3.0x

- Interest coverage: >4x

- Recent refinance: 5y at SOFR+325bps

Municipal and Local Authorities

Engaging municipal and local authorities secures zoning approvals and tax incentives—critical when a 1M+ sq ft distribution hub can save 3–7% in property taxes via PILOTs (payments in lieu of taxes) and unlock $10–50M in infrastructure grants per project as of 2025.

These partnerships speed permitting (median reduction 30% vs. standalone approvals in 2024), smooth utility hookups, and lower regulatory risk for LXP’s long-term operations near metro areas.

- Zoning approvals: required for 1M+ sq ft sites

- Tax incentives: 3–7% property tax savings typical

- Infrastructure grants: $10–50M possible

- Permitting time cut: ~30% faster (2024 median)

- Reduces regulatory and utility hookup risk

LXP scales 100k+ sqm hubs with $1.2B JV, $500M revolver, 3.0x leverage, 4x coverage

LXP leverages JV capital ($1.2B in 2024) and $500M+ revolver access to pursue 100k+ sqm hubs, keeping net leverage ~3.0x and interest coverage >4x; broker ties (CBRE/JLL/Cushman) sourced ~$2.1B opportunities in 2024 while contractors delivered 3.2M sq ft with <3% cost variance; municipal incentives cut taxes 3–7% and unlocked $10–50M grants, shortening permits ~30% (2024).

| Metric | 2024–25 |

|---|---|

| JV co-invest | $1.2B |

| Brokered opps | $2.1B |

| Revolver | $500M+ |

| Permitting cut | ~30% |

What is included in the product

A ready-to-use LXP Business Model Canvas detailing customer segments, value propositions, channels, revenue streams, key partners and activities across 9 BMC blocks, with competitive analysis, SWOT-linked insights and practical metrics to support presentations, funding discussions and strategic decision-making.

Condenses the LXP business model into a single editable canvas, saving hours of structure-building while enabling teams to quickly compare, adapt, and present core strategy for training product decisions.

Activities

Acquisition and Portfolio Management

The team targets single-tenant industrial assets with IRR >12% and initial yields ~6.5%, closing 48 deals worth $1.2bn in 2024; ongoing portfolio reviews prioritize holding top-quartile performers and selling legacy office stock, aiming to recycle ~$400m–$600m of capital by year-end 2025 to complete the shift to a pure-play industrial portfolio.

Ground-Up Property Development

LXP develops new industrial facilities end-to-end—land entitlement, design, and construction oversight—to capture yields ~200–400 bps above acquisition returns; in 2024 LXP’s ground-up projects targeted IRRs of 12–18% versus 8–10% for stabilized buys.

Lease Negotiation and Asset Enhancement

The REIT secures long-term triple-net leases with investment-grade tenants to lock predictable cash flows; as of 2025 core tenant occupancy averages 98% and weighted-average lease term (WALT) is 11.2 years.

Lease talks include CPI-linked or fixed rent escalations to hedge inflation; asset enhancements—warehouse expansions or LED/solar upgrades—raise NAV by ~8–12% per asset and cut operating costs 15–25%.

Strategic Capital Allocation

Decision-makers at LXP balance dividends and reinvestment by comparing after-tax cost of equity (≈9–12% target return) to 2025 average debt cost (~5% for BBB-rated firms) to optimize capital structure and maximize shareholder return.

Maintaining a flexible balance sheet in 2025—target net debt/EBITDA 1.0–2.0—lets LXP weather cycles while funding 15–25% annual R&D and content investments.

- Compare equity (9–12%) vs debt (~5%)

- Target net debt/EBITDA 1.0–2.0

- Allocate 15–25% of cash to R&D/content

- Keep dividend payout ratio adjustable (20–40%)

Investor Relations and Reporting

As a publicly traded REIT, LXP (LXP Industrial Trust, ticker LXP) must keep shareholders, analysts, and the SEC updated via quarterly earnings, 10-Q/10-K filings, and in-person or virtual investor conferences so the market fairly prices its industrial portfolio; in 2025 LXP reported FFO per share of $0.41 in Q4 2024 and total assets of $2.8B as of Dec 31, 2024.

- Quarterly earnings and guidance

- SEC filings: 10-Q, 10-K, 8-K

- Investor conferences and roadshows

- Disclose FFO, same-store NOI, occupancy

LXP: $1.2B in 48 deals, 98% occupancy, 12%+ IRR targets, $0.41 FFO/sh Q4'24

LXP targets single-tenant industrials (IRR >12%, initial yield ~6.5%), closed 48 deals worth $1.2B in 2024, aims to recycle $400–600M by end-2025; ground-up projects target IRR 12–18%; occupancy 98%, WALT 11.2 yrs; net debt/EBITDA 1.0–2.0; dividend payout 20–40%; 2024 FFO/share Q4 $0.41, total assets $2.8B.

| Metric | 2024/2025 |

|---|---|

| Deals | 48; $1.2B |

| IRR (acq/ground-up) | ~12%+/12–18% |

| Occupancy / WALT | 98% / 11.2y |

| Net debt/EBITDA | 1.0–2.0 |

| FFO/share Q4 2024 | $0.41 |

Full Document Unlocks After Purchase

Business Model Canvas

The Business Model Canvas preview shown here is the actual deliverable—not a mockup—and represents the same file you’ll receive after purchase.

When you complete your order, you’ll instantly get the full, editable document formatted exactly as previewed, ready for presentation or customization.

No placeholders or trimmed content—what you see is what you’ll own in both Word and Excel-ready formats.