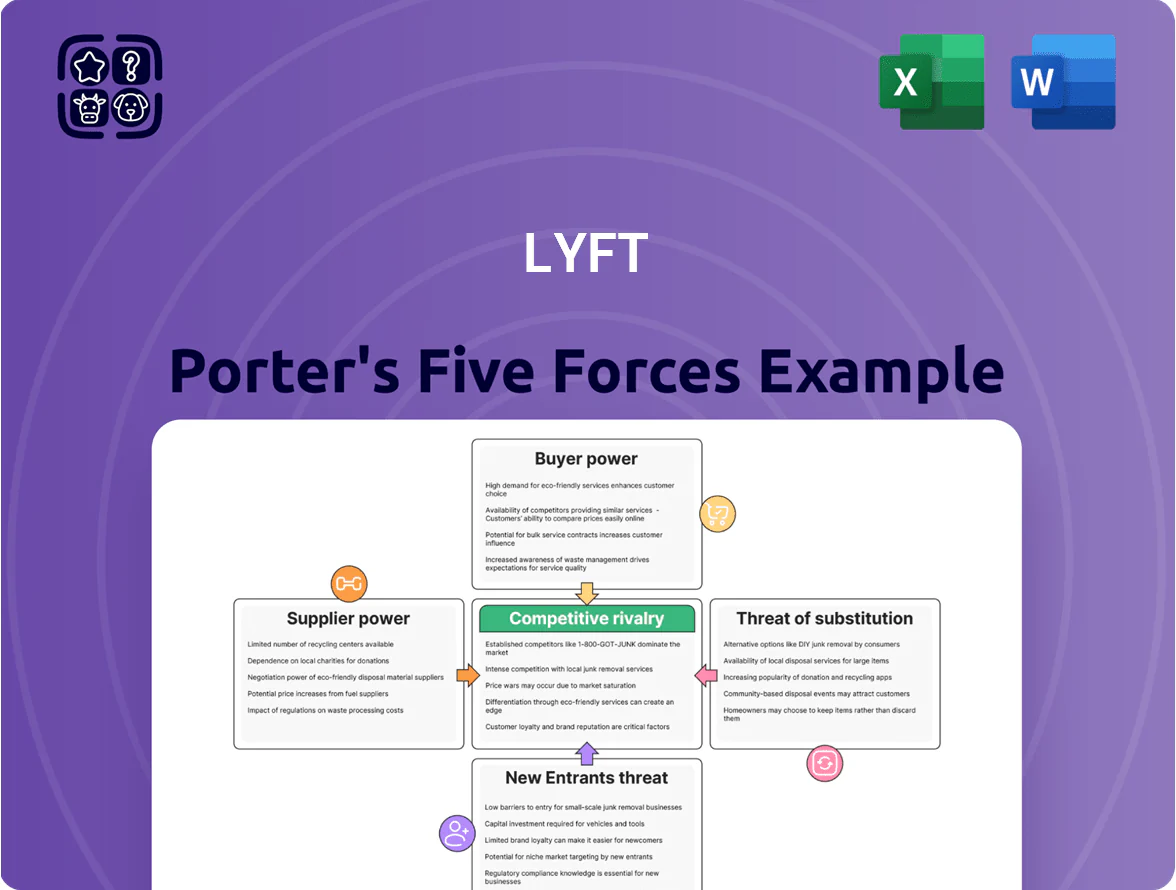

Lyft Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Lyft operates in a high-stakes ride-hailing market where intense rivalry, regulatory hurdles, and buyer price sensitivity shape outcomes; supplier power is moderate given driver flexibility, while substitutes and potential entrants keep margins under pressure. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Lyft’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Driver Labor Market Dynamics

Drivers supply labor and vehicles; by Q3 2025 Lyft had ~1.2M active drivers in the US, up 8% year-over-year, boosting their collective bargaining power as labor rules shifted toward worker protections in 2024–25.

Rising demand for flexible gig work and regulatory changes increased leverage, so Lyft spent ~$1.1B on driver incentives and benefits in 2024 and must keep adjusting pay, bonuses, and insurance to curb churn to Uber or W-2 jobs.

Cloud Infrastructure Dependency

Lyft depends on third-party cloud providers like Amazon Web Services (AWS) for ride-matching and data; in 2024 Lyft spent roughly $200–260 million on cloud and data services, making migration costly and slow.

That dependency gives suppliers pricing power—AWS fee hikes or outages can raise Lyft’s cost per ride and squeeze 2024 adjusted EBITDA margin (negative 7%–10%), directly hitting profitability.

Autonomous Technology Developers

As Lyft shifts to driverless rides, it relies heavily on autonomous tech suppliers for lidar, perception software, and compute—vendors that control scalability and unit costs; Waymo and Motional partnerships show OEMs can charge licensing fees that cut gross margins. Lyft owns no AV stack, so it is bound to partners' roadmaps and IP terms; a 2024 McKinsey estimate valued AV software licensing at $4–8k per vehicle annually, a recurring cost Lyft must absorb or pass to riders.

Fuel and Insurance Providers

Fuel price swings and rising commercial-insurance costs squeeze Lyft’s margins; U.S. pump prices averaged $3.32/gal in 2024 vs $3.02 in 2023, reducing driver availability and prompting Lyft to add surcharges or raise per-mile pay.

Commercial insurance scales with ride volume—Lyft’s FY2024 rides up ~12% gave insurers predictable premiums, so large insurance groups hold steady bargaining power over Lyft’s operating costs.

- 2024 avg U.S. gas $3.32/gal

- Driver supply falls as fuel >$3.00/gal

- Insurance costs rise with +12% ride volume in 2024

- Insurers have steady leverage

Vehicle Fleet and Rental Partners

Lyft’s Express Drive partners—including rental agencies and OEM programs—supply vehicles to drivers who lack cars, giving suppliers strong leverage over a sizable share of Lyft’s workforce (Express Drive covered ~20% of active drivers in 2024 according to Lyft disclosures).

Supply-chain disruptions or a 2022–2025 rise in auto loan rates (retail APRs rose ~150–300 basis points across segments) can cut fleet availability, constraining Lyft’s capacity to add rides and revenue.

- Express Drive ~20% of drivers (2024)

- Supplier control = asset dependency

- Auto loan APRs +150–300 bps (2022–2025)

- Supply shocks can cap growth

Supplier Power Squeezes Lyft: $1.1B Driver Spend, Rising Cloud, AV & Fuel Costs

Suppliers hold moderate-to-high power: ~1.2M US drivers (Q3 2025) and Express Drive fleets (~20% of drivers in 2024) force Lyft to spend ~$1.1B on incentives (2024); cloud costs ~$200–260M and AV licensing $4–8k/vehicle/yr raise unit costs; 2024 gas $3.32/gal and rising insurance/loan rates (+150–300bps) tighten margins.

| Metric | 2024–25 |

|---|---|

| Active drivers (US) | ~1.2M (Q3 2025) |

| Express Drive | ~20% (2024) |

| Driver spend | $1.1B (2024) |

| Cloud spend | $200–260M (2024) |

| Gas | $3.32/gal (2024) |

| AV license | $4–8k/vehicle/yr (est) |

What is included in the product

Tailored Porter's Five Forces analysis for Lyft that uncovers competitive drivers, buyer and supplier power, entry barriers, and substitute threats—highlighting strategic vulnerabilities and opportunities in the ride-hailing and mobility market.

Concise Porter's Five Forces snapshot for Lyft—instantly highlights competitive pressures and regulatory risks to streamline strategic decisions and investor briefings.

Customers Bargaining Power

Low Switching Costs

Passengers face near-zero switching costs between Lyft and rivals like Uber, DoorDash Drive; surveys in 2024 showed 68% of riders use multiple apps, and monthly active rider overlap exceeds 40% in top metros.

This enables riders to choose the cheapest or fastest option—Lyft lost market share in 2023 in several markets where wait times spiked by 15%.

To fight churn Lyft invests in loyalty (Lyft Pink had ~1.2M subscribers in 2024) to create behavioral friction and drive retention.

Price Sensitivity and Transparency

Real-time price transparency lets users compare Lyft fares instantly across apps; a 2024 CivicScience survey found 62% of US riders check multiple platforms before booking. Customers show high sensitivity to surge: Lyft reported ridership drops of ~18% during peak-price events in Q3 2024, constraining Lyft’s ability to raise base fares without immediate demand loss. Riders often wait or switch to transit or micromobility when costs exceed a personal threshold.

Availability of Alternative Mobility

In dense cities, riders can choose public transit, walking, biking, or micromobility, giving customers high leverage—short trips often favor transit or walking since U.S. urban transit ridership was ~6.6B trips in 2023 and average short-ride cost makes rideshare a premium option.

Lyft added bikes and scooters; by 2024 micromobility accounted for ~10–12% of its trips, so integration reduces churn and price sensitivity for short-distance demand.

Corporate and Enterprise Influence

Large enterprise clients using Lyft for Business can demand volume discounts and custom SLAs; in 2024 corporate rides made up an estimated 18% of Lyft’s US revenue, giving these buyers real leverage.

Concentration of buying power lets big accounts threaten full migration to competitors, so Lyft often matches competitive corporate rates to retain contracts—loss of a single large client can cut recurring revenue materially.

- ~18% of US revenue from corporate rides (2024)

- Volume discounts and bespoke terms common

- High churn risk if migration occurs

- Drives competitive corporate pricing

User Feedback and Reputation Power

The digital platform amplifies individual riders: Lyft’s rating system and social media meant a single viral safety complaint can cut weekly bookings sharply; after 2023 safety incidents, app downloads fell ~8% month-over-month in affected markets.

Perceived drops in safety or service drive fast brand erosion and churn; Lyft reports average monthly active riders 15% higher in markets with 4.8+ driver ratings versus 4.6.

Lyft must keep strict quality controls—driver screening, in-app safety tools, 24/7 support—to retain a vocal, empowered user base and protect revenue (2024 net rider revenue $2.9B).

- Ratings + social posts amplify complaints

- Safety dips → rapid booking declines (~8% observed)

- Higher driver ratings correlate with +15% MAU

- Quality controls protect $2.9B rider revenue

High switching, surge sensitivity: Lyft fights churn with Pink and micromobility

Customers have high bargaining power: near-zero switching costs (68% use multiple apps in 2024), realtime fare comparison (62% check platforms), and surge sensitivity (ridership fell ~18% during Q3 2024 peak pricing), forcing Lyft to use loyalty (Lyft Pink ~1.2M) and micromobility (10–12% of trips) to reduce churn.

| Metric | 2023–2024 |

|---|---|

| Riders using multiple apps | 68% (2024) |

| MAU overlap top metros | >40% (2024) |

| Check multiple platforms | 62% (2024) |

| Lyft Pink subscribers | ~1.2M (2024) |

| Micromobility share | 10–12% (2024) |

| Ridership drop during surge | ~18% (Q3 2024) |

| Corporate revenue share | ~18% US revenue (2024) |

Preview Before You Purchase

Lyft Porter's Five Forces Analysis

This preview shows the exact Lyft Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups, fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Lyft operates in a high-stakes ride-hailing market where intense rivalry, regulatory hurdles, and buyer price sensitivity shape outcomes; supplier power is moderate given driver flexibility, while substitutes and potential entrants keep margins under pressure. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Lyft’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Driver Labor Market Dynamics

Drivers supply labor and vehicles; by Q3 2025 Lyft had ~1.2M active drivers in the US, up 8% year-over-year, boosting their collective bargaining power as labor rules shifted toward worker protections in 2024–25.

Rising demand for flexible gig work and regulatory changes increased leverage, so Lyft spent ~$1.1B on driver incentives and benefits in 2024 and must keep adjusting pay, bonuses, and insurance to curb churn to Uber or W-2 jobs.

Cloud Infrastructure Dependency

Lyft depends on third-party cloud providers like Amazon Web Services (AWS) for ride-matching and data; in 2024 Lyft spent roughly $200–260 million on cloud and data services, making migration costly and slow.

That dependency gives suppliers pricing power—AWS fee hikes or outages can raise Lyft’s cost per ride and squeeze 2024 adjusted EBITDA margin (negative 7%–10%), directly hitting profitability.

Autonomous Technology Developers

As Lyft shifts to driverless rides, it relies heavily on autonomous tech suppliers for lidar, perception software, and compute—vendors that control scalability and unit costs; Waymo and Motional partnerships show OEMs can charge licensing fees that cut gross margins. Lyft owns no AV stack, so it is bound to partners' roadmaps and IP terms; a 2024 McKinsey estimate valued AV software licensing at $4–8k per vehicle annually, a recurring cost Lyft must absorb or pass to riders.

Fuel and Insurance Providers

Fuel price swings and rising commercial-insurance costs squeeze Lyft’s margins; U.S. pump prices averaged $3.32/gal in 2024 vs $3.02 in 2023, reducing driver availability and prompting Lyft to add surcharges or raise per-mile pay.

Commercial insurance scales with ride volume—Lyft’s FY2024 rides up ~12% gave insurers predictable premiums, so large insurance groups hold steady bargaining power over Lyft’s operating costs.

- 2024 avg U.S. gas $3.32/gal

- Driver supply falls as fuel >$3.00/gal

- Insurance costs rise with +12% ride volume in 2024

- Insurers have steady leverage

Vehicle Fleet and Rental Partners

Lyft’s Express Drive partners—including rental agencies and OEM programs—supply vehicles to drivers who lack cars, giving suppliers strong leverage over a sizable share of Lyft’s workforce (Express Drive covered ~20% of active drivers in 2024 according to Lyft disclosures).

Supply-chain disruptions or a 2022–2025 rise in auto loan rates (retail APRs rose ~150–300 basis points across segments) can cut fleet availability, constraining Lyft’s capacity to add rides and revenue.

- Express Drive ~20% of drivers (2024)

- Supplier control = asset dependency

- Auto loan APRs +150–300 bps (2022–2025)

- Supply shocks can cap growth

Supplier Power Squeezes Lyft: $1.1B Driver Spend, Rising Cloud, AV & Fuel Costs

Suppliers hold moderate-to-high power: ~1.2M US drivers (Q3 2025) and Express Drive fleets (~20% of drivers in 2024) force Lyft to spend ~$1.1B on incentives (2024); cloud costs ~$200–260M and AV licensing $4–8k/vehicle/yr raise unit costs; 2024 gas $3.32/gal and rising insurance/loan rates (+150–300bps) tighten margins.

| Metric | 2024–25 |

|---|---|

| Active drivers (US) | ~1.2M (Q3 2025) |

| Express Drive | ~20% (2024) |

| Driver spend | $1.1B (2024) |

| Cloud spend | $200–260M (2024) |

| Gas | $3.32/gal (2024) |

| AV license | $4–8k/vehicle/yr (est) |

What is included in the product

Tailored Porter's Five Forces analysis for Lyft that uncovers competitive drivers, buyer and supplier power, entry barriers, and substitute threats—highlighting strategic vulnerabilities and opportunities in the ride-hailing and mobility market.

Concise Porter's Five Forces snapshot for Lyft—instantly highlights competitive pressures and regulatory risks to streamline strategic decisions and investor briefings.

Customers Bargaining Power

Low Switching Costs

Passengers face near-zero switching costs between Lyft and rivals like Uber, DoorDash Drive; surveys in 2024 showed 68% of riders use multiple apps, and monthly active rider overlap exceeds 40% in top metros.

This enables riders to choose the cheapest or fastest option—Lyft lost market share in 2023 in several markets where wait times spiked by 15%.

To fight churn Lyft invests in loyalty (Lyft Pink had ~1.2M subscribers in 2024) to create behavioral friction and drive retention.

Price Sensitivity and Transparency

Real-time price transparency lets users compare Lyft fares instantly across apps; a 2024 CivicScience survey found 62% of US riders check multiple platforms before booking. Customers show high sensitivity to surge: Lyft reported ridership drops of ~18% during peak-price events in Q3 2024, constraining Lyft’s ability to raise base fares without immediate demand loss. Riders often wait or switch to transit or micromobility when costs exceed a personal threshold.

Availability of Alternative Mobility

In dense cities, riders can choose public transit, walking, biking, or micromobility, giving customers high leverage—short trips often favor transit or walking since U.S. urban transit ridership was ~6.6B trips in 2023 and average short-ride cost makes rideshare a premium option.

Lyft added bikes and scooters; by 2024 micromobility accounted for ~10–12% of its trips, so integration reduces churn and price sensitivity for short-distance demand.

Corporate and Enterprise Influence

Large enterprise clients using Lyft for Business can demand volume discounts and custom SLAs; in 2024 corporate rides made up an estimated 18% of Lyft’s US revenue, giving these buyers real leverage.

Concentration of buying power lets big accounts threaten full migration to competitors, so Lyft often matches competitive corporate rates to retain contracts—loss of a single large client can cut recurring revenue materially.

- ~18% of US revenue from corporate rides (2024)

- Volume discounts and bespoke terms common

- High churn risk if migration occurs

- Drives competitive corporate pricing

User Feedback and Reputation Power

The digital platform amplifies individual riders: Lyft’s rating system and social media meant a single viral safety complaint can cut weekly bookings sharply; after 2023 safety incidents, app downloads fell ~8% month-over-month in affected markets.

Perceived drops in safety or service drive fast brand erosion and churn; Lyft reports average monthly active riders 15% higher in markets with 4.8+ driver ratings versus 4.6.

Lyft must keep strict quality controls—driver screening, in-app safety tools, 24/7 support—to retain a vocal, empowered user base and protect revenue (2024 net rider revenue $2.9B).

- Ratings + social posts amplify complaints

- Safety dips → rapid booking declines (~8% observed)

- Higher driver ratings correlate with +15% MAU

- Quality controls protect $2.9B rider revenue

High switching, surge sensitivity: Lyft fights churn with Pink and micromobility

Customers have high bargaining power: near-zero switching costs (68% use multiple apps in 2024), realtime fare comparison (62% check platforms), and surge sensitivity (ridership fell ~18% during Q3 2024 peak pricing), forcing Lyft to use loyalty (Lyft Pink ~1.2M) and micromobility (10–12% of trips) to reduce churn.

| Metric | 2023–2024 |

|---|---|

| Riders using multiple apps | 68% (2024) |

| MAU overlap top metros | >40% (2024) |

| Check multiple platforms | 62% (2024) |

| Lyft Pink subscribers | ~1.2M (2024) |

| Micromobility share | 10–12% (2024) |

| Ridership drop during surge | ~18% (Q3 2024) |

| Corporate revenue share | ~18% US revenue (2024) |

Preview Before You Purchase

Lyft Porter's Five Forces Analysis

This preview shows the exact Lyft Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups, fully formatted and ready to use.