MAA PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

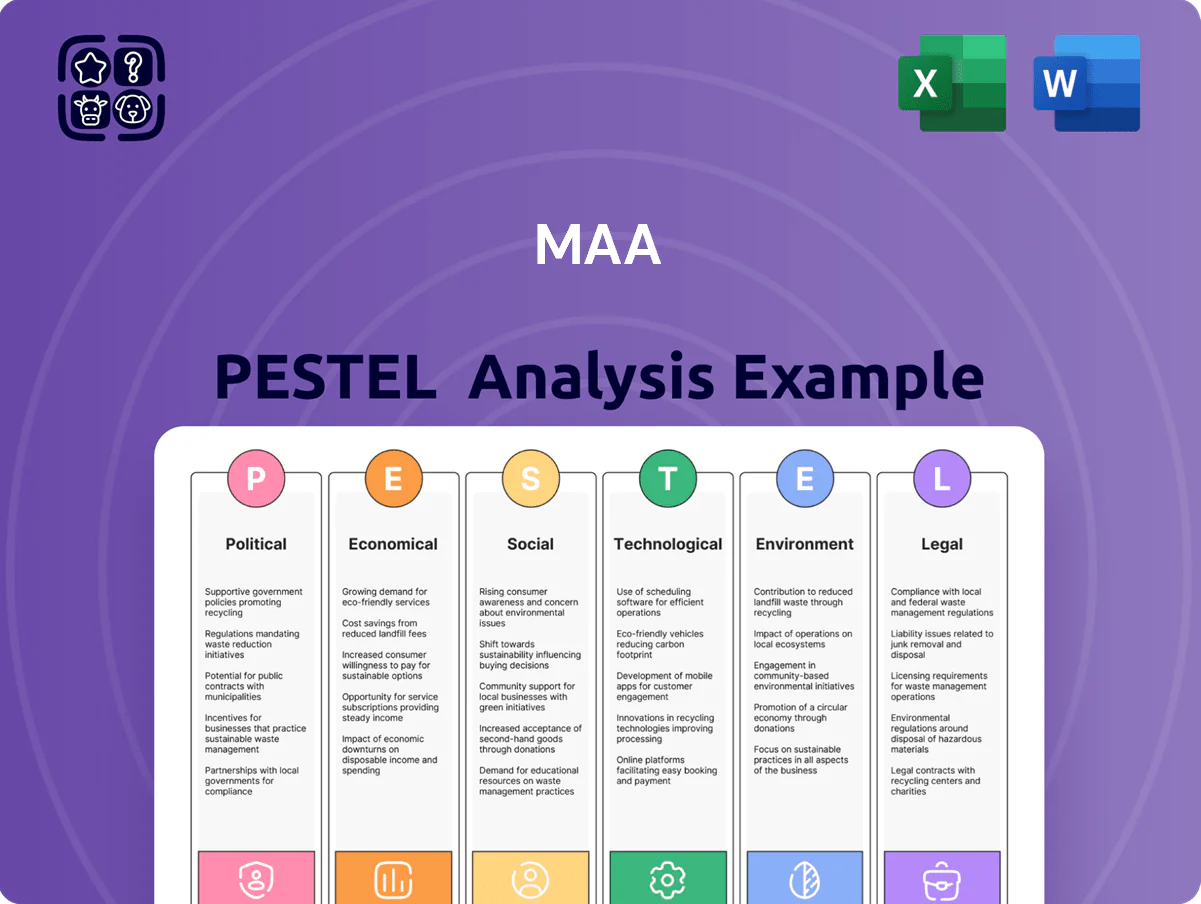

Discover how political, economic, social, technological, legal, and environmental forces are shaping MAA's strategic outlook—our concise PESTLE pinpoints risks and opportunities you can act on today; buy the full analysis for a deep, ready-to-use briefing that fuels smarter investments and strategic plans.

Political factors

Federal Housing Affordability Initiatives

Local Zoning and Land Use Regulations

Political decisions at the municipal level in high-growth cities like Austin and Nashville shape MAA’s development pipeline; Austin added 50,000 residents 2020–2023 and Nashville 30,000, raising local demand but prompting zoning shifts. Changes allowing higher density—Austin’s 2024 code updates permitting mid-rise in some corridors—could increase competing unit supply by an estimated 5–10% in affected submarkets. Conversely, restrictive overlay zones can protect NOI and asset values by limiting new inventory near MAA properties. MAA must engage planning boards proactively to keep redevelopment and $500M+ construction plans compliant and on schedule.

REIT Tax Status and Legislative Stability

As a REIT, MAA is highly sensitive to U.S. tax-code changes governing shareholder distribution of taxable income; the 90% distribution rule lets MAA avoid corporate tax and supported its 2024 dividend yield of ~3.8% on FYE 2024 funds from operations (FFO) per share of $6.10. Political stability of REIT tax-exempt status is critical to MAA’s valuation and capital structure, as loss would raise effective tax rates and cost of capital. Any legislative move to alter the 90% requirement would force MAA to revise dividend policy and retained-earnings strategy, likely reducing payout and altering deployment of capital.

Rent Control and Tenant Protection Proposals

- 12 municipalities considered rent-stabilization in 2024

- Proposed caps typically 3–5% annually

- 2–4% lower rent growth may cut NOI ~1.5–2.5%

- MAA portfolio ~78,000 units requires policy/legal updates

Infrastructure Spending and Regional Growth

Federal and state infrastructure bills in 2021–2025 allocated over $300 billion to transportation and utilities nationwide, with Southeast and Southwest states receiving an estimated $45–60 billion for highways, ports, and grid upgrades, boosting regional connectivity and employment.

These investments increase demand for MAA’s airport-centric and near-infrastructure assets, supporting rent resilience and occupancy as local job growth rates in targeted metros rose 1.2–2.5% annually through 2024.

- >$45–60B regional infrastructure inflows (2021–2025)

- Improved connectivity around MAA assets

- Local job growth +1.2–2.5% annually to 2024

- Portfolio aligned with long-term political investment trends

Housing Aid, Rent Caps & New Supply Pressure Mid‑Tier Rents — MAA Yields 3.8%

| Indicator | Value |

|---|---|

| FY2025 housing funding | $65B |

| Voucher funding increase 2024 | +7% |

| MAA FFO/share (FYE 2024) | $6.10 |

| Dividend yield (2024) | ~3.8% |

| Municipal rent-cap proposals (2024) | 12 cities; 3–5% |

| Infrastructure to SE/SW (2021–25) | $45–60B |

| MAA portfolio units | ~78,000 |

What is included in the product

Explores how external macro-environmental factors uniquely affect the MAA across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented MAA PESTLE summary that relieves prep time by delivering shareable, presentation-ready insights and editable notes for quick alignment across teams and decision-makers.

Economic factors

Interest Rate Environment and Cost of Capital

By end-2025, stabilized Fed funds near 5.25–5.50% enabled MAA to more accurately price debt and budget capex, improving forecast certainty after early-2020s volatility.

Although rates sit well above 2020–2021 lows, predictable borrowing costs support execution of MAA’s capital recycling, with projected 2026 interest expense sensitivity reduced by ~10–15% versus prior uncertainty.

MAA’s access to unsecured debt at spreads near 150–200 bps over Treasuries remains a competitive edge versus smaller, highly leveraged private developers facing higher funding costs and limited liquidity.

Sun Belt Employment Growth and Labor Markets

Sun Belt employment growth, outpacing the U.S. average (2024 payrolls +2.1% vs national +1.2%), underpins MAA’s revenue, as tech and manufacturing relocations raise median household incomes—e.g., Austin and Raleigh saw 2024 wage growth ~4.5%—driving demand for quality rental housing.

Sustained job gains in MAA’s core markets keep portfolio occupancy above industry averages (MAA 2024 average occupancy ~95%), enabling annual rent growth (2024 same-store rent growth ~4–6%) and supporting cash flow stability.

Inflationary Pressure on Operating Expenses

Persistent inflation in labor and materials eroded margins for property management and new construction through 2025, with construction input prices up about 6.5% year-over-year and average wage growth in property services near 4.8% in 2024–25.

MAA leverages scale to secure vendor discounts, reducing procurement cost growth by an estimated 1–2 percentage points versus smaller peers.

Rising property insurance premiums (up ~12% nationally in 2024) and utility costs (electricity +8% YoY in 2024) remain significant uncontrollable headwinds.

Controlling controllable expenses while offsetting insurance and utility inflation is essential for MAA to hit projected NOI growth targets through 2025.

Housing Supply and Demand Equilibrium

Delivery of new apartment units in Sun Belt metros peaked in 2023–24, with completions totaling roughly 240,000 units across top markets, creating a near-term absorption period that tempers MAA’s pricing power and raised concessions by ~150–250 bps in some metros.

Oversupply phases historically pushed retention down 3–6% as tenants trade up to newer product, but MAA’s A- and B+ focus sustains demand—vacancy for midscale units in 2024 averaged ~4.5% versus 6.8% in luxury.

- 2023–24 Sun Belt completions ≈240,000 units

- Concessions rose ~150–250 bps in peak areas

- Retention fell 3–6% during oversupply

- Midscale vacancy ~4.5% vs luxury 6.8% (2024)

Consumer Spending and Disposable Income Trends

The financial health of the American renter directly affects MAA’s revenue; in 2024 renters’ median household income rose ~3.5% while CPI hit ~3.4%, keeping rent burden steady—about 30% of income spent on housing nationally, with lower-income renters spending >50%.

As wage growth lags cost of living, rent-to-income ratios signal delinquency risk; MAA adjusts leasing terms, concessions, and amenity mix in response to regional variations and 2024 metro-level affordability data.

- 2024 national rent burden ≈30%

- Lower-income renters spend >50% on housing

- 2024 median renter income +3.5%, CPI ≈3.4%

- MAA uses regional rent-to-income to set leases/concessions

Sun Belt rent gains offset by rising construction & insurance costs as rates hold ~5.3%

Stable Fed funds ~5.25–5.50% end-2025, unsecured spreads 150–200bps; Sun Belt payrolls +2.1% (2024) with wage growth ~4.5% in Austin/Raleigh; MAA occupancy ~95% and same-store rent growth ~4–6% (2024); construction input prices +6.5% YoY and insurance +12% (2024) pressure NOI.

| Metric | 2024/2025 |

|---|---|

| Fed funds | 5.25–5.50% |

| Unsecured spread | 150–200bps |

| Sun Belt payrolls | +2.1% |

| MAA occupancy | ~95% |

| Rent growth | 4–6% |

| Construction inputs | +6.5% YoY |

| Insurance | +12% |

Preview the Actual Deliverable

MAA PESTLE Analysis

The preview shown here is the exact MAA PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal, and environmental forces are shaping MAA's strategic outlook—our concise PESTLE pinpoints risks and opportunities you can act on today; buy the full analysis for a deep, ready-to-use briefing that fuels smarter investments and strategic plans.

Political factors

Federal Housing Affordability Initiatives

Local Zoning and Land Use Regulations

Political decisions at the municipal level in high-growth cities like Austin and Nashville shape MAA’s development pipeline; Austin added 50,000 residents 2020–2023 and Nashville 30,000, raising local demand but prompting zoning shifts. Changes allowing higher density—Austin’s 2024 code updates permitting mid-rise in some corridors—could increase competing unit supply by an estimated 5–10% in affected submarkets. Conversely, restrictive overlay zones can protect NOI and asset values by limiting new inventory near MAA properties. MAA must engage planning boards proactively to keep redevelopment and $500M+ construction plans compliant and on schedule.

REIT Tax Status and Legislative Stability

As a REIT, MAA is highly sensitive to U.S. tax-code changes governing shareholder distribution of taxable income; the 90% distribution rule lets MAA avoid corporate tax and supported its 2024 dividend yield of ~3.8% on FYE 2024 funds from operations (FFO) per share of $6.10. Political stability of REIT tax-exempt status is critical to MAA’s valuation and capital structure, as loss would raise effective tax rates and cost of capital. Any legislative move to alter the 90% requirement would force MAA to revise dividend policy and retained-earnings strategy, likely reducing payout and altering deployment of capital.

Rent Control and Tenant Protection Proposals

- 12 municipalities considered rent-stabilization in 2024

- Proposed caps typically 3–5% annually

- 2–4% lower rent growth may cut NOI ~1.5–2.5%

- MAA portfolio ~78,000 units requires policy/legal updates

Infrastructure Spending and Regional Growth

Federal and state infrastructure bills in 2021–2025 allocated over $300 billion to transportation and utilities nationwide, with Southeast and Southwest states receiving an estimated $45–60 billion for highways, ports, and grid upgrades, boosting regional connectivity and employment.

These investments increase demand for MAA’s airport-centric and near-infrastructure assets, supporting rent resilience and occupancy as local job growth rates in targeted metros rose 1.2–2.5% annually through 2024.

- >$45–60B regional infrastructure inflows (2021–2025)

- Improved connectivity around MAA assets

- Local job growth +1.2–2.5% annually to 2024

- Portfolio aligned with long-term political investment trends

Housing Aid, Rent Caps & New Supply Pressure Mid‑Tier Rents — MAA Yields 3.8%

| Indicator | Value |

|---|---|

| FY2025 housing funding | $65B |

| Voucher funding increase 2024 | +7% |

| MAA FFO/share (FYE 2024) | $6.10 |

| Dividend yield (2024) | ~3.8% |

| Municipal rent-cap proposals (2024) | 12 cities; 3–5% |

| Infrastructure to SE/SW (2021–25) | $45–60B |

| MAA portfolio units | ~78,000 |

What is included in the product

Explores how external macro-environmental factors uniquely affect the MAA across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented MAA PESTLE summary that relieves prep time by delivering shareable, presentation-ready insights and editable notes for quick alignment across teams and decision-makers.

Economic factors

Interest Rate Environment and Cost of Capital

By end-2025, stabilized Fed funds near 5.25–5.50% enabled MAA to more accurately price debt and budget capex, improving forecast certainty after early-2020s volatility.

Although rates sit well above 2020–2021 lows, predictable borrowing costs support execution of MAA’s capital recycling, with projected 2026 interest expense sensitivity reduced by ~10–15% versus prior uncertainty.

MAA’s access to unsecured debt at spreads near 150–200 bps over Treasuries remains a competitive edge versus smaller, highly leveraged private developers facing higher funding costs and limited liquidity.

Sun Belt Employment Growth and Labor Markets

Sun Belt employment growth, outpacing the U.S. average (2024 payrolls +2.1% vs national +1.2%), underpins MAA’s revenue, as tech and manufacturing relocations raise median household incomes—e.g., Austin and Raleigh saw 2024 wage growth ~4.5%—driving demand for quality rental housing.

Sustained job gains in MAA’s core markets keep portfolio occupancy above industry averages (MAA 2024 average occupancy ~95%), enabling annual rent growth (2024 same-store rent growth ~4–6%) and supporting cash flow stability.

Inflationary Pressure on Operating Expenses

Persistent inflation in labor and materials eroded margins for property management and new construction through 2025, with construction input prices up about 6.5% year-over-year and average wage growth in property services near 4.8% in 2024–25.

MAA leverages scale to secure vendor discounts, reducing procurement cost growth by an estimated 1–2 percentage points versus smaller peers.

Rising property insurance premiums (up ~12% nationally in 2024) and utility costs (electricity +8% YoY in 2024) remain significant uncontrollable headwinds.

Controlling controllable expenses while offsetting insurance and utility inflation is essential for MAA to hit projected NOI growth targets through 2025.

Housing Supply and Demand Equilibrium

Delivery of new apartment units in Sun Belt metros peaked in 2023–24, with completions totaling roughly 240,000 units across top markets, creating a near-term absorption period that tempers MAA’s pricing power and raised concessions by ~150–250 bps in some metros.

Oversupply phases historically pushed retention down 3–6% as tenants trade up to newer product, but MAA’s A- and B+ focus sustains demand—vacancy for midscale units in 2024 averaged ~4.5% versus 6.8% in luxury.

- 2023–24 Sun Belt completions ≈240,000 units

- Concessions rose ~150–250 bps in peak areas

- Retention fell 3–6% during oversupply

- Midscale vacancy ~4.5% vs luxury 6.8% (2024)

Consumer Spending and Disposable Income Trends

The financial health of the American renter directly affects MAA’s revenue; in 2024 renters’ median household income rose ~3.5% while CPI hit ~3.4%, keeping rent burden steady—about 30% of income spent on housing nationally, with lower-income renters spending >50%.

As wage growth lags cost of living, rent-to-income ratios signal delinquency risk; MAA adjusts leasing terms, concessions, and amenity mix in response to regional variations and 2024 metro-level affordability data.

- 2024 national rent burden ≈30%

- Lower-income renters spend >50% on housing

- 2024 median renter income +3.5%, CPI ≈3.4%

- MAA uses regional rent-to-income to set leases/concessions

Sun Belt rent gains offset by rising construction & insurance costs as rates hold ~5.3%

Stable Fed funds ~5.25–5.50% end-2025, unsecured spreads 150–200bps; Sun Belt payrolls +2.1% (2024) with wage growth ~4.5% in Austin/Raleigh; MAA occupancy ~95% and same-store rent growth ~4–6% (2024); construction input prices +6.5% YoY and insurance +12% (2024) pressure NOI.

| Metric | 2024/2025 |

|---|---|

| Fed funds | 5.25–5.50% |

| Unsecured spread | 150–200bps |

| Sun Belt payrolls | +2.1% |

| MAA occupancy | ~95% |

| Rent growth | 4–6% |

| Construction inputs | +6.5% YoY |

| Insurance | +12% |

Preview the Actual Deliverable

MAA PESTLE Analysis

The preview shown here is the exact MAA PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.